ServiceNow is Now

After a deluge of positive vaccine news, the bottom line is that there will be more work in 2021.

It has always been about the work.

As much as it seems recently that social media is taking over and that the marketing of work will solve economic problems from Guatemala to Zanzibar instead of the work itself, I have news for you: it won’t.

It is still about the work, and for tech newsletters like this one, it’s about the content and always will be.

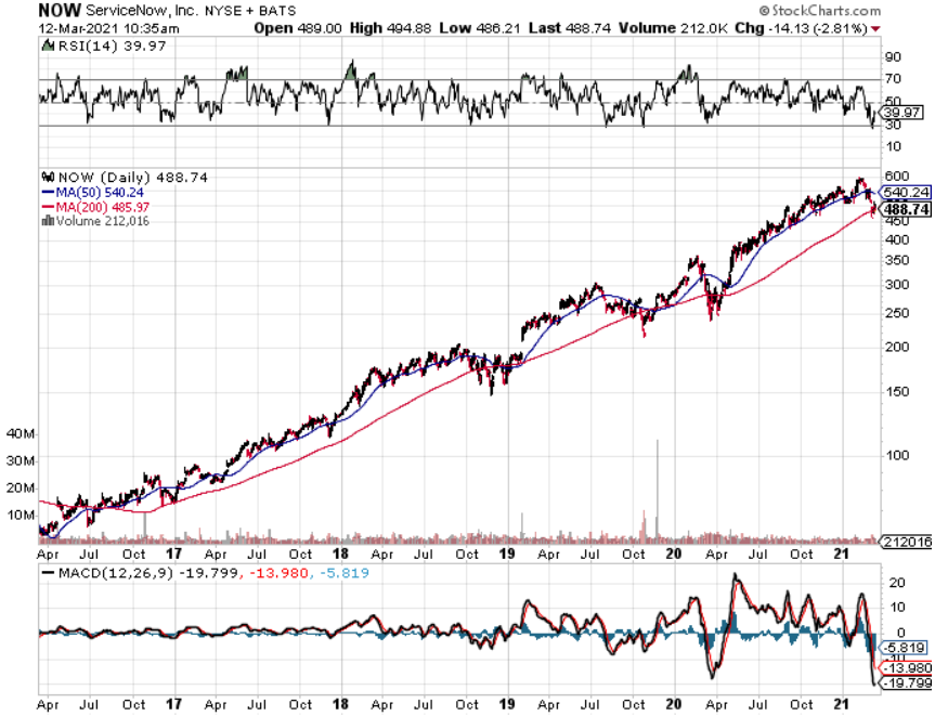

Vaccine-based health solutions will release a torrent of new work opportunities, and tech stock readers need to jump into this workflow automation cloud stock called ServiceNow (NOW).

Digital investments are at an all-time high and are expected to continue expanding.

This is the best place to park investment money betting on future digital-based work growth.

According to IDC, worldwide digital transformation investments will total more than $7.4 trillion by 2044.

The digital economy is firing on all cylinders and ServiceNow is the platform company for digital business.

A quick review of 2020 indicates outperformance.

They significantly beat expectations across the board, bringing heightened momentum into 2021 and beyond.

NOW delivered over 30% organic top line growth, 25% operating margins and $1.4 billion in free cash flow.

Their achievement is a testament to ServiceNow’s strong work culture.

The secular tailwinds of digital transformation, cloud computing, and business model innovation have all intersected at a perfect moment in time.

A paradigm shift is occurring worldwide.

In 2020, for the first time in history, digital transformation spending accelerated despite GDP declining globally.

ServiceNow is enabling a comprehensive solution for the schedule and reporting of vaccination for Scotland's most vulnerable citizens.

Within 12 hours of rollout, the NHS (National Health Service) in Scotland booked over 220,000 appointments.

NOW is literally all about the business workflow maximizing enterprise digital transformation with how every organization in every sector in every location.

Workers are adapting, growing, creating new business models, and empowering themselves to be productive in any environment and in condition.

NOW grew billings by more than 40% year over year organically.

They delivered 89 deals greater than $1 million and now have close to 1,100 customers paying over $1 million annually.

This bounty of sales included landing the largest deal in NOWs history and deal sizes overall keep getting larger.

NOW's renewal rate remained best in class at 99%.

In 2020, they added nearly 700 net new customers, ending the year with almost 6,900 enterprises.

The number of giant deals continues uninterrupted with customers paying NOW $5 million or more in annual contract value (ACV) grew over 40% in fiscal 2020.

One of the U.K.'s big four banks is using multiple ServiceNow products, including a purpose-built new financial services operations product to help transform the way it operates and to deliver better customer experiences.

The bank has seen a 70% uptick in efficiency and improvement of payment processing by integrating the Now Platform into its core banking systems.

These bankers moved from cut and paste, swivel chair manual processes to efficient, automated workflows.

In one case, employees went from managing 10 requests an hour to 10,000 requests in three minutes on the Now Platform.

PayPal (PYPL) recently expanded their relationship with ServiceNow as a key partner for elements of their digital transformation.

Nike is another big name who is using the Now Platform to create better customer and employee experiences.

Other additive deals that are noteworthy are in key sectors such as Booking.com in travel and hospitality, BP in energy, Santander U.K. in banking.

Most cloud stocks are high growth and trot out even higher losses, but now NOW!

They run a tight ship with Q4 operating margin of 22%, a 100-basis-point beat versus guidance, fueled by strong top line outperformance.

For full year 2020, operating margin was 25%, up 300 basis points year over year.

Looking forward, only optimism can be described in the corridors of NOW and for Q1, the company expect subscription revenues between $1.275 billion and $1.28 billion, representing 28% to 29% year-over-year growth.

The cloud revolution is still in the early innings and this company has guaranteed $10 billion in annual sales representing a more than doubling of revenue from the $4.52 billion in 2020.

NOW has a strong product portfolio, a deep focus on building deep customer relationships, and a robust commitment to enabling digital transformation.

This cloud company must be in your top 20 of ones to own and the stock price will benefit from this dynamic business.