September 13, 2023

(AN ALTERNATIVE INCOME INVESTMENT TO BONDS)

September 13, 2023

Hello everyone.

Many of us are on the lookout to increase our income.

There are some ways to do this.

We know with interest rates surging our cash in savings accounts receive higher yield and 90-day T-bills also offer a good 5%+ yield.

But is there anything else besides Bonds where investors can find robust returns?

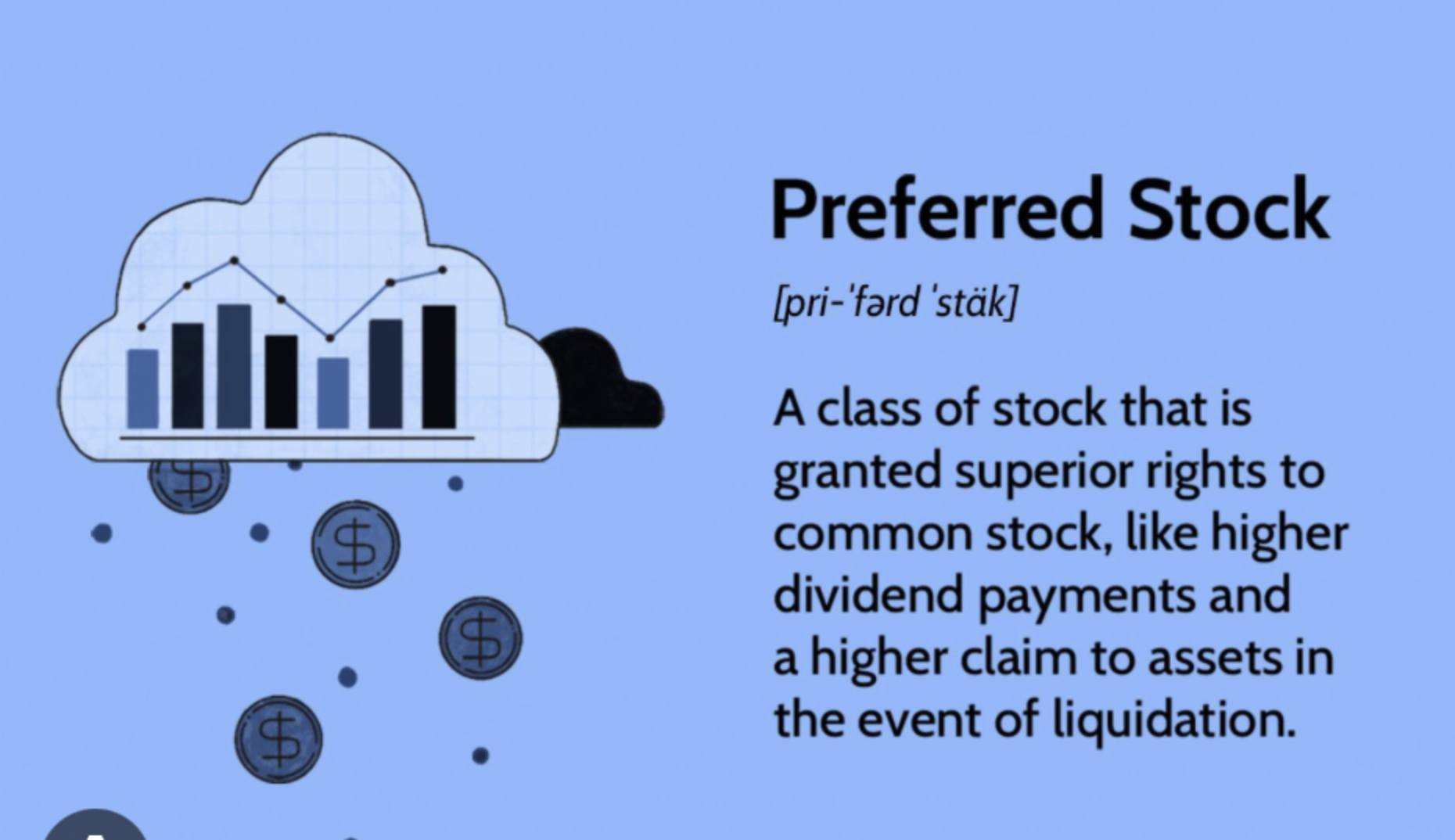

Preferred stocks are one option that comes to mind. Both my mother and I owned these in the 1990’s and early 2000’s. They combine elements of stocks and bonds in one investment.

Preferreds are attractive because they provide the stability of fixed-dividend payments, which is bond-like, but they also offer equity like appreciation. So, it is a nice balance. (Note, that the equity price appreciation is often lower than common stock.)

Bonds are offering 5%+ right now, but a preferred stock gets investment grade security that yields 6.5% - which is solid income – without taking on too much credit risk.

Most investors are attracted to preferred stocks because they offer more consistent dividends than common shares and higher payments than bonds. Preferreds are issued with a fixed par value and pay dividends based on a percentage of that par, usually at a fixed rate. Let’s say that a preferred stock had a par value of $100 per share and paid an 8% dividend. To calculate the dividend, you would need to multiply 8% by $100 (the par value), which comes out to an annual dividend of $8 per share. If dividend payments are made quarterly, each payment will be $2 per share.

One downside of preferreds is that they don’t have the same voting rights as common shareholders. The company is not beholden to preferred shareholders the way it is to traditional equity shareholders.

To recognise a preferred stock, look for a P at the end of the ticker symbol.

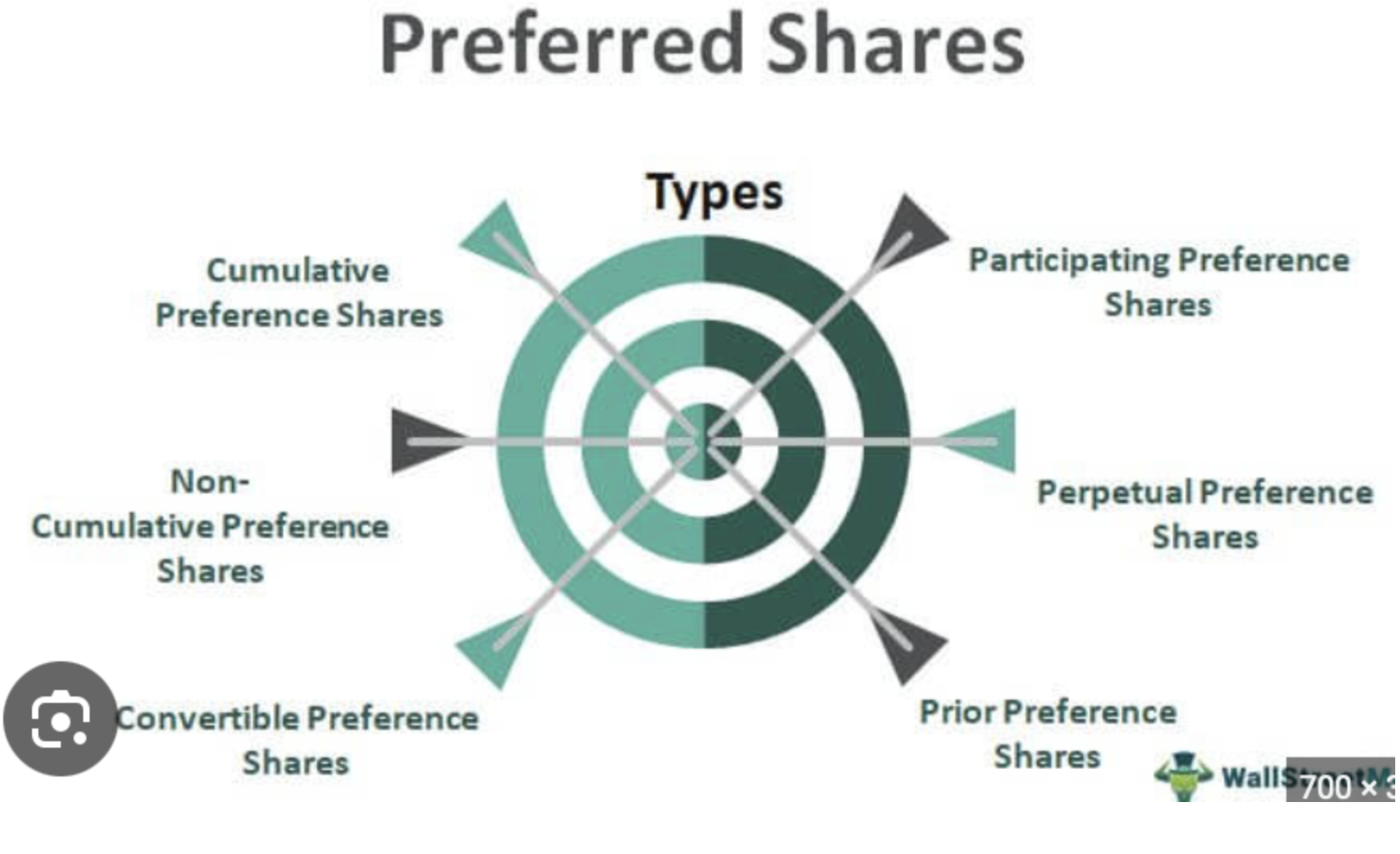

There are four types of preferred shares:

Convertible, Cumulative, Non-Cumulative, Participatory:

Convertible shares are preferred shares that can be exchanged for common shares at a fixed rate. This can be very lucrative for preferred shareholders if the market value of common shares increases. (This is the type of preferred shares my mother and I held). Once the shares have been exchanged the shareholder gives up the benefit of a fixed dividend and cannot convert common shares back to preferred shares.

Cumulative preferred shares have a clause that protects the investor against a downturn in company profits. If revenues are down, the issuing company may not be able to afford to pay dividends. Cumulative shares require that any unpaid dividends must be paid to preferred shareholders before any dividends can be paid to common shareholders. If a company guarantees dividends of $10 per preference share but cannot afford to pay for three consecutive years, it must pay a $40 cumulative dividend in the fourth year before any other dividends can be paid.

Non-Cumulative shares do not entitle an investor to missed dividends. (If one year the company decides not to pay dividends, they won’t pay it the next year. As a result, the investor loses his or her right to claim any unpaid dividends.) Interest on a non-cumulative deposit is paid on a regular basis, whereas interest on a cumulative deposit is paid at maturity.

Participatory Preferred shares provide an additional profit guarantee to shareholders. All preference shares have a fixed dividend rate, which is their chief benefit. However, on top of that chief benefit, participatory shares guarantee additional dividends in the event that the issuing company meets certain financial goals. So, for example, if the company has a really good year and meets a predetermined profit target, holders of participatory shares receive dividend payments above the normal fixed rate.

Instead of looking for single stocks that offer preferreds, you could look at SPDR ICE Preferred Securities ETF (ticker: PSK), which yields 6.5%.

You could also look at ETF’s that focus on dividend paying stocks which offer another avenue for income. Pro-Shares S&P Dividend Aristocrats ETF (NOBL) is one that comes to mind. It’s an $11.65 billion fund that tracks the S&P 500 Dividend Aristocrat Index. The yield is 1.95% and year to date return is 4.43%.

The yield doesn’t appear crash hot when you first see it, but long-term, you have to remember this is stock investing, and therefore you get the opportunity for price appreciation. So, over the long term you will most probably receive better returns those bonds.

The much talked about recession that may happen or may not happen, whether it be hard, soft or in the middle of those descriptions is background noise at the moment, but it is always wise to hold high quality companies in a stock portfolio, and companies that have dividends which keep growing tend to be those high-quality companies.

Happy Wednesday.

Cheers

Jacquie