The AI Train Keeps Chugging

If anyone needs another AI data point, the tech market just delivered us a juicy one with an outstanding earnings call with Broadcom (AVGO) and its CEO Hock Tan.

The AI enterprise build-out has been developing in full-force and investors are pouring money into the foundation of the AI future.

That is currently where the AI profits currently lie.

The software companies have missed out on that profit in the short-term, but since many are also involved in the AI infrastructure spend, they can turn to their investors and ask for a mark-up in owned shares.

This won’t always be the case, and I do believe we are fast reaching an inflection point where shareholders will demand more from their capital and not just more AI data centers and more modern AI semiconductor chips.

I am talking about meaningful revenue growth directly tied to AI spend – we don’t have that yet.

At some point, there needs to be an application from all of this money spent and return on capital.

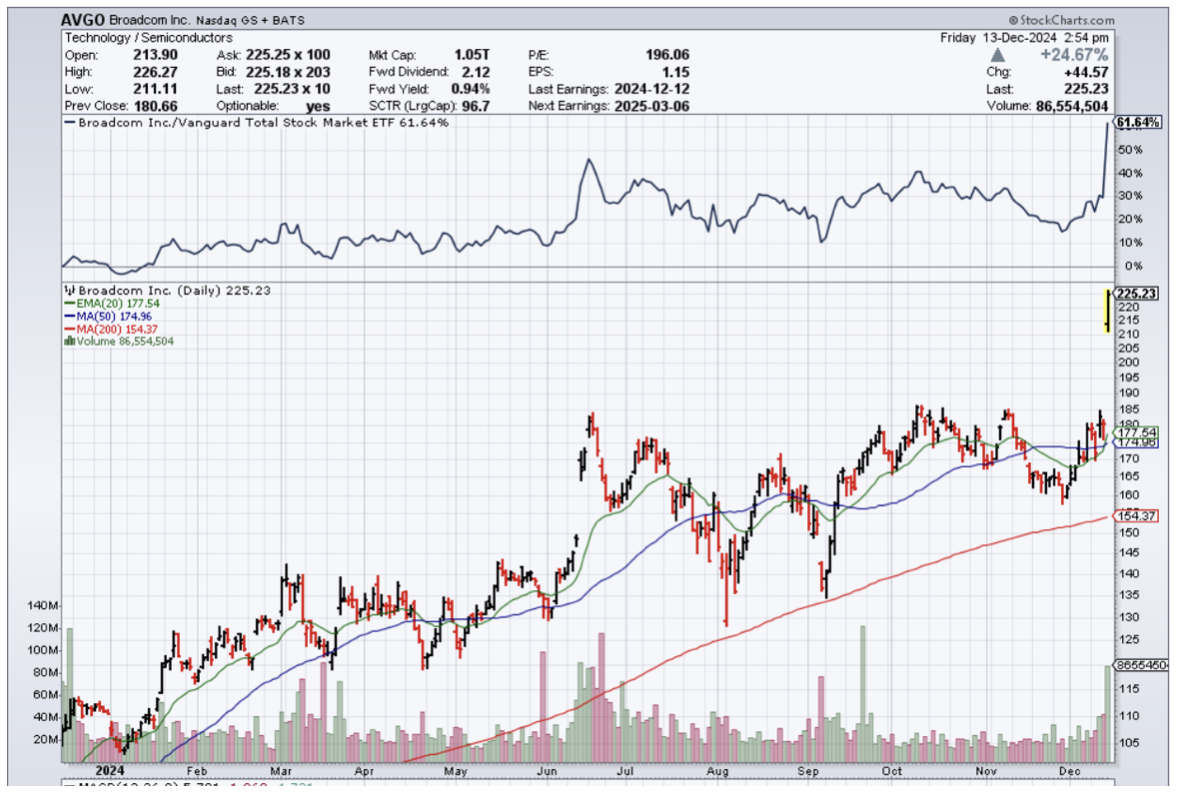

In the meantime, Mr. Market is cheering the success of AVGO and the stock is up 25% today at the time of this writing signaling investors will continue to back this AI infrastructure spend into 2025 and possibly beyond.

Broadcom CEO Hock Tan said the company expects its custom AI chips will generate between $60 billion and $90 billion in revenue over the next three years from its three existing hyperscaler customers, whom the company did not name. Tan reiterated his belief that each of the three hyperscalers will deploy 1 million clusters of its custom AI chips called XPUs by 2025.

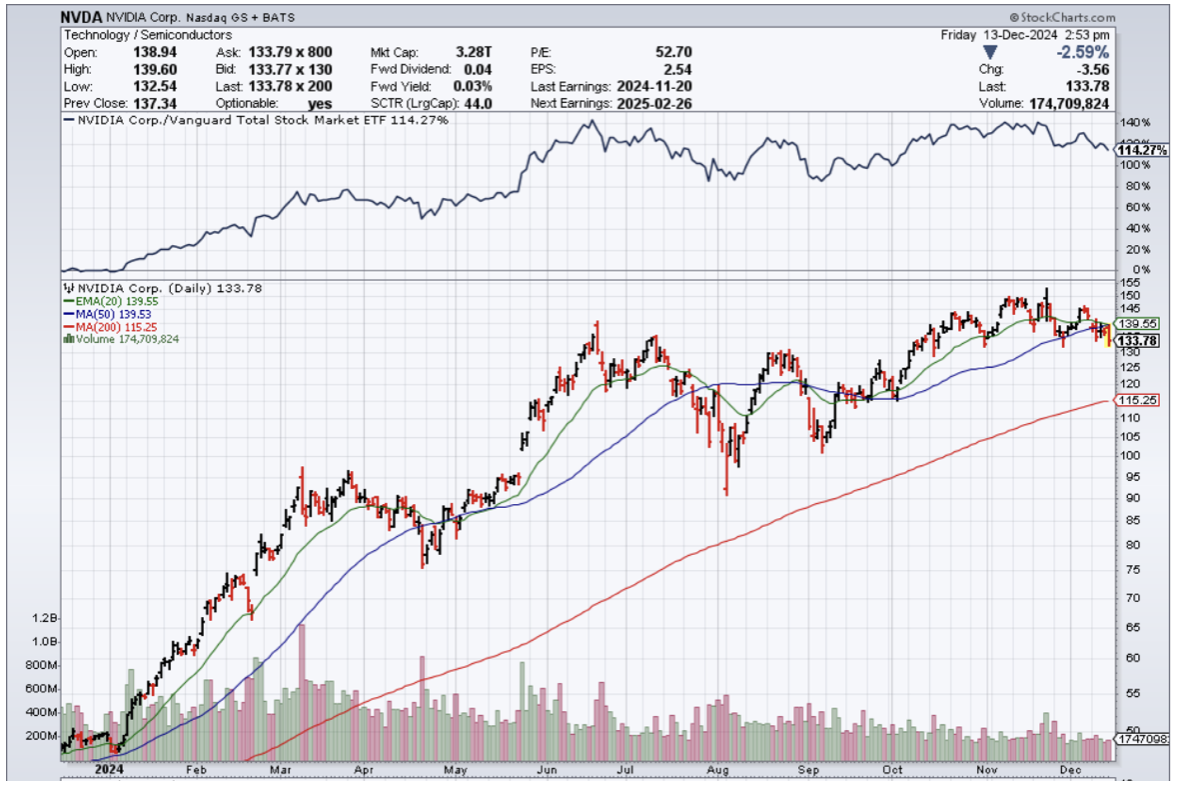

Apple is reportedly working with Broadcom to develop an AI server chip. The move by tech giants to make their own server chips is meant to cut costs and scale back their reliance on Nvidia’s (NVDA) GPUs (graphics processing units).

That trend is reflected in the industry at large. The AI chip market is set to grow 74% in 2025, while the semiconductor market overall is projected to grow just 12% next year.

We are seeing this type of binary divergence in tech firms like Dell and Oracle.

Many of these legacy tech companies are attempting to wean themselves from a legacy business that is expanding in the low single digits.

From a technical perspective, any dip to the $200 level will be a strong buy for AVGO.

I believe they continue to pivot into the AI infrastructure build while partnering with companies that can aid this type of success.

They will continue to invest in products related to AI, mainly chips, which will be installed in a wide array of businesses like data centers, consumer electronics like smartphones and laptops, and electric vehicles.

AVGO has been a hot company for quite a while, and even though not quite an Nvidia, I do believe AVGO stock is a solid backup option for tech investors looking for some diversification.