March 18, 2011 - My Shopping List of Technology Stocks

Featured Trades: (MY SHOPPING LIST OF TECHNOLOGY STOCKS), (AAPL), (CSCO), (HPQ), (ORCL), (GOOG), (INTC), (JDSU), (QQQ), (ROM), (XLK)

3) My Shopping List of Technology Stocks. Hedge fund managers are smacking their lips, maneuvering to take advantage of the recent sharp sell off by technology stocks. They are building shopping lists of where to pounce

at the first sign of another upside breakout, much like a famished tiger might behave. Some of the highest quality names have had the biggest falls, some more than 20%, and they are now flaunting dividend yields greater than the 3.2% found on 10 year Treasury bonds.

Here are the names that I am hearing is on the list:

Apple (AAPL)

Cisco (CSCO)

Hewlett Packard (HPQ)

Oracle (ORCL)

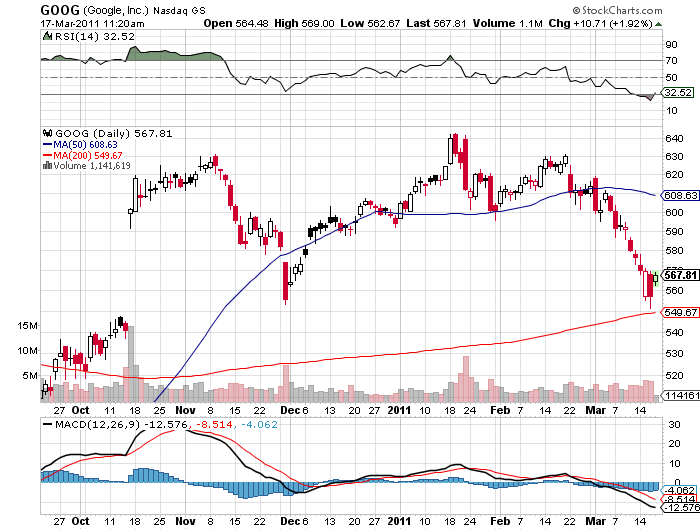

Google (GOOG)

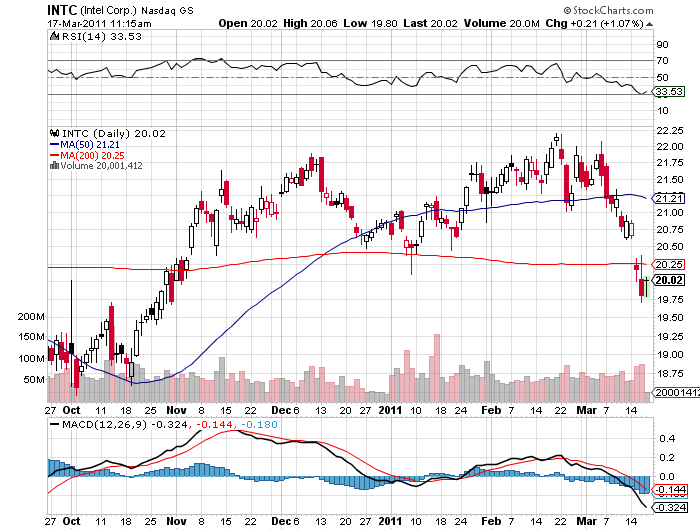

Intel (INTC)

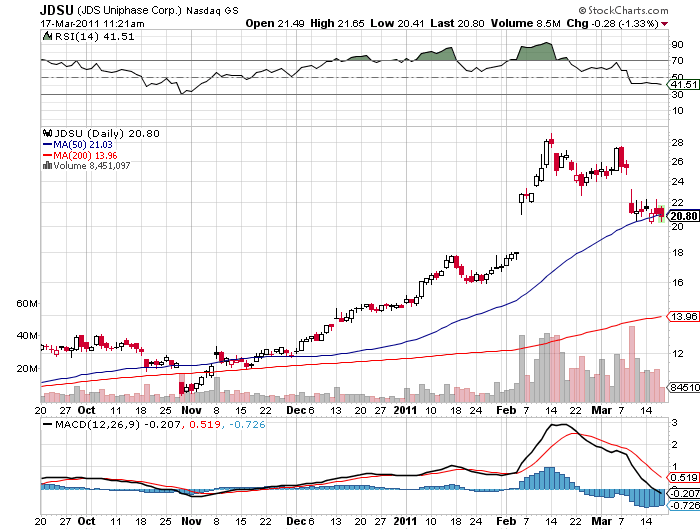

JDSU Uniphase (JDSU)

Look at Intel (INTC), which at $20 is selling at a paltry 11 times earnings and a 3.5% dividend yield, and generates the bulk of its sales in the highest growth sectors of the global economy. After the dotcom bust of 2000, these bad boys spent nearly a decade in the penalty box, shunned by the investing world as the poster boys for wild excess. Think Robert Downey, Jr. on steroids. During this time, cash balances doubled, free cash flows soared, outstanding shares shrank, and multiples fell to a tenth of their bubblicious peaks.

I started recommending this group at the absolute bottom of the market in March, 2009 (click here for the call), and it was no surprise to me when they outperformed almost every sector on the upside. With 60%-80% of their earnings coming from abroad, primarily Asia, I saw them really as foreign stocks wearing cowboy hats, pearl snap buttoned shirts, and Ray Ban aviator sunglasses. They did not need banks, as they are almost entirely self-financed, immunizing them from the credit crunch.

They avoided many of the management errors that torpedoed so many other US firms, like derivatives books, leveraged real estate exposure, and LBO debt, and outright stealing. While their American customers were getting poorer, their two billion overseas customers were getting much richer.

The industry represents the last, best hope that America has for competing globally, as it is our only means of staying on top of the international value added chain. It seems that in addition to bulk commodities like corn, wheat, soybeans, coal, timber, aircraft, weapons, movies, and porn, tech companies are among the few that make things foreigners actually want to buy from us.

The lessons of the bubble made them ultra-conservative in their capital spending, which will lead to product shortages and much higher prices in any recovery. There are short squeezes developing for a whole range of tech components. Memory, for example, has seen no capex at all for three years. They are surfing the wave of innovation, and will cash in big time from the mobile computing revolution, cloud computing, and the virtualization of data centers.

During the last tech bubble, the industry did not have the global market that it does today. Now, demand from the rising emerging market middle class is kicking in, as it is for commodities. The two year tech rally we saw from the 2009 lows could just be the down payment of a decade long bull market in these stocks, which will then end with another bubble down the road. When John Chambers, a first class manager, discusses Cisco's (CSCO) long term outlook, he is so effusive, he sounds like he is on ecstasy.

If you don't want to make any bets on single names, you can look at the Technology Select Sector SPDR (XLK), the PowerShares QQQ (QQQQ), or the leveraged ProShares Ultra Technology (ROM). I'll shoot out a trade alert FOR 'Macro Millionaire' readers when I pull the trigger.