How Cisco Systems Got Its Mojo Back

Studying the history of the 1849 California Gold Rush, there is not a single miner who is known today.

But the merchants who sold them shovels, food, and blue jeans have banks, hotels, and universities everywhere with names like Huntington, Stanford, Crocker, and Hopkins.

The modern-day Levi and shovel slingers come in the form of the internet infrastructure equipment manufacturer Cisco Systems (CSCO).

Not only does 85% of Internet traffic navigate across Cisco's Systems' powerful routers, Cisco is also run online, from product orders to intra staff circulation of information.

A myriad of tech companies will largely use Cisco's network infrastructure to keep their operations at the cutting edge.

Cisco (CSCO) is an American technology conglomerate headquartered in the heart of Silicon Valley, that builds, manufactures, and peddles networking hardware and telecommunications equipment.

Cisco (CSCO) has finally come in from the cold after a long, hard 2-year slog that finally saw them return to revenue growth.

Quarter after quarter, Cisco (CSCO) was prisoned in the penalty box for sticking with their fading legacy business of network hardware solutions.

Even accumulating a massive $67 billion in profits from abroad, the company failed to impress investor sentiment as revenue sequentially dipped.

How did Cisco (CSCO) get their mojo back?

Cisco finally adopted the SaaS (Service as a subscription) model that has been put to great use by all the high flyers. The one-time fee has been replaced by annual recurring charge generating a perpetual income stream.

The shift means 33% of income is now recurring subscription revenue, comprising 52% of the company's software sales. Cisco (CSCO) made US$5.5 billion from recurring software and subscription in the recent quarter.

Re-calibrating the business model has caused the deferred revenue segment to explode from a pedestrian 6%, just 10 quarters ago, to an impressive 33% now.

The progress has evoked broad based, positive investor sentiment and Cisco is just in the first phase of this secular trend.

Cisco hopes to transition as much business as it can to cloud-based subscriptions to enhance the customer experience.

One of the solutions offered is Cisco UCS Services for data centers. The data center aids business and has a spectacular future ahead of it. Services are aligned with business needs by unique network-based optimization. Cisco Data Center Services cuts operating costs while offering customers a high standard of service.

The plan for their subscription model is to offer pricing that is less than the one-time fee model, but offer premium add-ons to the base model. This incremental quality improvement will justify the recurring model also increase revenue per customer.

The advanced subscriptions will offer the newest cloud-based solutions that Cisco develops and gives impetus towards the SaaS model which has been a boon for the entire tech sector.

Data center was up double digits in the recent quarter, driven by server products as well as the HyperFlex offerings that drew in 2,400 new customers. Security tools have seen a rise in momentum, up 6% QOQ.

Total revenue was up 3% to $11.9 billion, and guidance growth for the next quarter was set at 3% to 5% on the back of the SaaS model, while maintaining vibrant operating margins of 31.7%, and a guided gross margin rate expected in the range of 63% to 64%. These are fantastic numbers.

The second part of the revitalization plan is the $66 billion of repatriated cash. $31 billion will go directly into share buybacks "over the next 18 to 24 months."

Cisco continues to prop up the dividend and remains committed to returning cash, thus exciting institutional investors. Cisco announced a $0.04 boost to the quarterly dividend to $0.33 per share, up 14% YOY.

Acquisitions are also a critical part of the overall strategy, as it always has been. Cloud-based Broadsoft was one of the latest companies scooped up by Cisco.

The company provides the building blocks for service providers to build cloud-based communications services such as voice, video, and web. BroadSoft was founded in 1998 and is headquartered in Maryland.

These little purchases may seem insignificant, but synergistic acquisitions added 80 basis points to the bottom line, and overall inorganic impact bumps up another 0.5 point to about 130 basis points.

Cisco (CSCO) will still be net cash positive of $10 billion to $12 billion and will scour the field for more acquisitions that will levitate growth and improve the product.

When you consider that Cisco's growth is occurring amid a backdrop of a robust domestic and global economy, and amid a trend for all companies to adopt a comprehensive digital blueprint then Cisco is perfectly placed to sell its services to cloud converts.

The digital bias is in the nascent phase, and once brick and mortar grapple with digitization and scalability or extinction, the trend will swiftly compound.

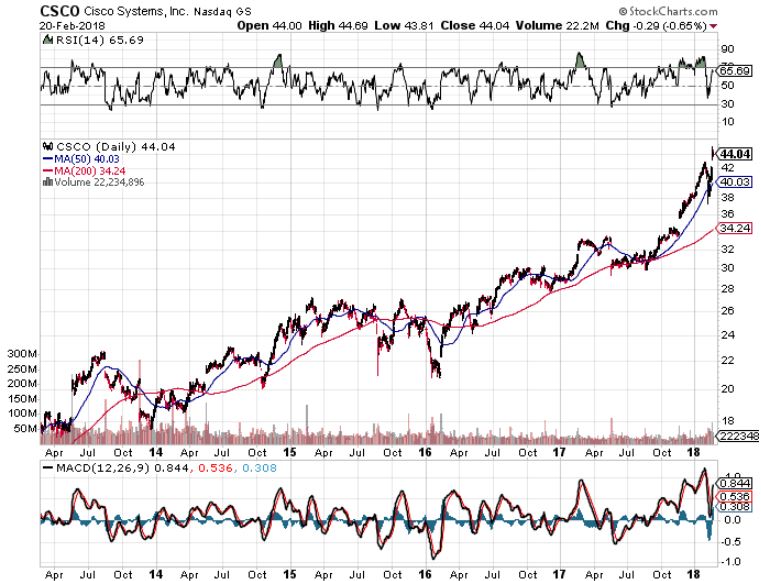

The modernization of the business model explains the surge in Cisco's share price from 2016. The shares have rocketed by an amazing 158% since then. Before that, they were stigmatized as a dying, archaic business that languished for years.

If investors cannot identify new growth drivers on the short-term horizon, they bail out. The two-pronged approach of their subscription model and reallocation capital plan will solidify the accelerating growth rhetoric. In other words, they now have a new "story" to sell.

Their peer group consists of Hewlett Packard (HPE), China's Huawei, Juniper Networks (JNPR), and Finland's Nokia (NOK). Microsoft (MSFT) and Cisco have demonstrated that tech dinosaurs can reinvent, reload, and revitalize a business model on the brink.

Such is the beauty of the digital economy where tinkering with a business model is just a few clicks away.

To learn more about Cisco Systems please click here.