A Tale Of Two Shots

The smell of antiseptic and sounds of beeping monitors filled the air as I walked through a Tokyo hospital ward back in 1975.

As a fresh UCLA biochemistry graduate working in Japan, I was visiting a friend who had contracted hepatitis B - a common affliction in Asia at the time.

Little did I know that decades later, I'd be analyzing a company that would revolutionize not just hepatitis treatment, but potentially end the AIDS epidemic as we know it.

That company is Gilead Sciences (GILD), and they just delivered a knockout Q4 that has Wall Street's attention.

But the real story here isn't in the numbers - though believe me, we'll get to those. It's about what's coming next.

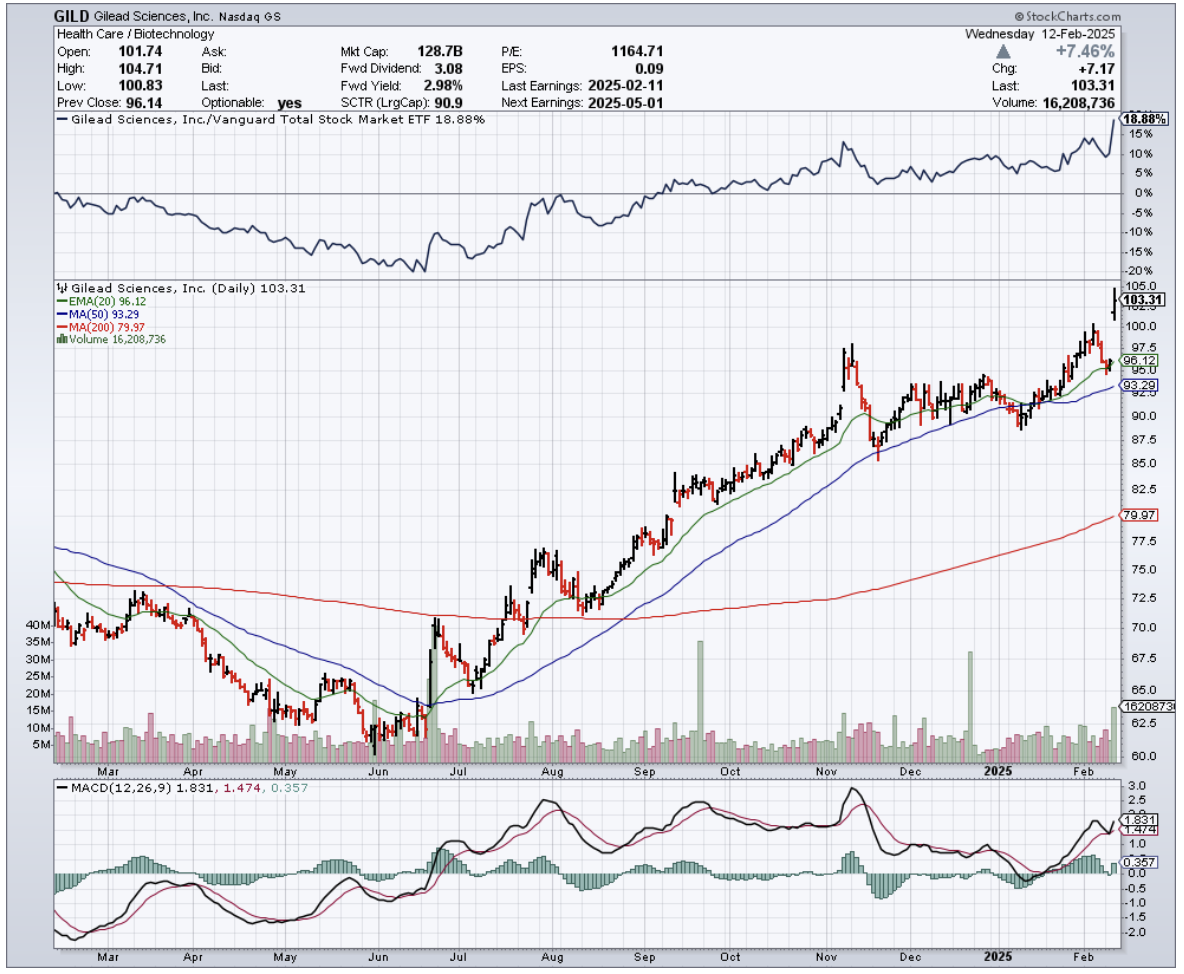

Last week, Gilead reported Q4 revenue of $7.57 billion, beating estimates by $420 million. Not too shabby for a company some analysts had written off as past its prime.

And here’s another thing that got my attention: their new HIV prevention treatment, lenacapavir, achieved something I've rarely seen in four decades of following biotech - a standing ovation at the AIDS 2024 conference.

Why? Because it worked. Not just worked - it was 100% effective in one trial and 99.9% in another.

For perspective, that's like pitching a perfect game in the World Series, twice. And instead of daily pills, we're talking about two shots per year.

The FDA is expected to weigh in by summer 2025, and after seeing results like these, I'd bet my vintage Japanese sake collection on approval.

The numbers tell quite a story. Gilead's HIV franchise grew 16% year-over-year, with their flagship drug Biktarvy now commanding over 50% market share.

Even with Medicare Part D changes taking a $1 billion bite out of 2025 revenues (thanks, IRA), management still guided for $28.2-28.6 billion in revenue.

That's not just maintaining course - that's sailing straight through a hurricane without spilling your coffee.

Their oncology business isn't sleeping either. Trodelvy hit $1.3 billion in 2024 sales, up 19% from last year.

Their cell therapies Yescarta and Tecartus are performing like seasoned kabuki actors, bringing in $390 million and $98 million respectively in Q4.

On top of these, Gilead has over 50 clinical programs running simultaneously.

For those keeping score at home, that's more shots on goal than a World Cup final. And they don't face any major patent cliffs until late 2033 - practically an eternity in biotech years.

Speaking of shots on goal, let's talk about that stock price.

Shares have climbed from $71 to around $100 since my last recommendation. Not bad, but given what's in the pipeline, I think we're still in the early innings here.

The company's latest breakthrough, Livdelzi for liver disease, already pulled in $30 million in its first quarter.

Some analysts are talking about $2 billion in peak sales - and having seen my share of liver disease cases during my time in Asia, I wouldn't be surprised if they're being conservative.

Looking ahead to 2025, Gilead has several potential catalysts.

Two major Trodelvy trial readouts, potential lenacapavir approvals worldwide, and expansion into new markets.

They've come a long way since their Harvoni glory days of 2015, transforming from a one-hit wonder into a diversified powerhouse.

Is the stock cheap? Not as cheap as when I first recommended it. But with lenacapavir looking like it could change the game in HIV prevention, this feels like watching Microsoft (MSFT) in the early days of Windows - you know something big is coming, even if you can't quite see the whole picture yet.

The last time I saw scientific results this promising was during China's opening up in the late 1970s, when decades of isolated research suddenly became available to the world.

As for my friend from that Tokyo hospital? He recovered fully, thanks to medical advances that seemed impossible at the time.

Today's impossibilities have a funny way of becoming tomorrow's breakthroughs - and that's exactly why I'm rating Gilead a strong buy on any dips.