Accounting Standards Could Take Down Supermicro

Super Micro Computer (SMCI) has some dubious management and accounting methods and it is coming back to haunt them with the potential boot from the Nasdaq index.

In fact, they are really cutting it close to secure their existence inside the index, because they haven’t offered any clear updates yet.

It is hard to believe they have loitered around not making any decisions to replace their accounting firm.

The optics is terrible because it appears as if no reputable accounting firm is willing to take their account.

There is fudging the numbers and then there is outright fraud and the situation at SMCI suggest the latter.

Remember, the world is still waiting to hear when SMCI will file their 2024 year-end report with the Securities and Exchange Commission, and why it was late.

That report is something many expected would be filed alongside the company’s June fourth-quarter earnings but was not.

The company’s auditor, Ernst & Young, stepped down in October, and Super Micro said last week that it was still trying to find a new one.

A public tech company that can’t find an auditor, because their accounting practices are so toxic, nobody wants to touch it with a 10-foot pole.

Even though the company sells a great chip wanted by many other companies, the stock has crashed by almost 90%.

Getting delisted from the Nasdaq could be next if Super Micro doesn’t file a compliance plan by the Monday deadline or if the exchange rejects the company’s submission. Super Micro could also get an extension from the Nasdaq, giving it months to come into compliance. The company said Thursday that it would provide a plan to the Nasdaq in time.

The Nasdaq says it looks at several factors when evaluating a plan of compliance, including the reasons for the late filing, upcoming corporate events, the overall financial status of the company and the likelihood of a company filing an audited report within 180 days. The review can also look at information provided by outside auditors, the SEC or other regulators.

Between 2015 and 2017, Super Micro misstated financials and published key filings late, according to the SEC. It was delisted from the Nasdaq in 2017 and was relisted two years later.

In the short term, the bigger worry for Super Micro is whether customers and suppliers start to bail.

It’s hard to crash a stock when sales more than doubled last year to nearly $15 billion and many analysts believe they can do $25 billion in sales in 2025.

The mismanagement is on an extreme level here to the point where if you buy stock in this company, they might be delisted and it will be hard to get a refund on that stock.

Then there is the real hit to the reputation because vendors must think that if SMCI’s accounting practices are so bad, then what perhaps customers should be worried about the chip products too.

Where there is smoke – there is fire.

It’s nothing good for SMCI and the optics keep going from bad to worse.

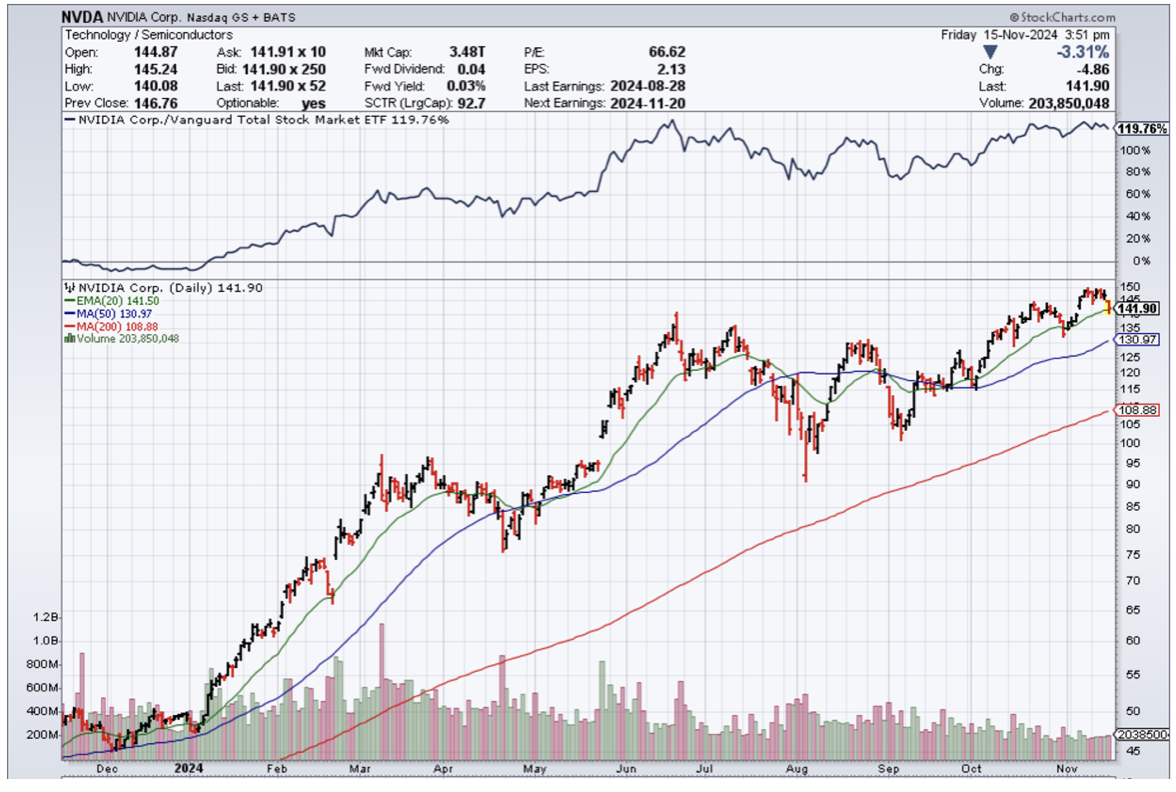

Luckily, Nvidia has said that doesn’t really affect them and so any sort of contagion risk is confined.

The trading around the chip stocks have been incredibly volatile with the surge after the election then the profit taking this week.

Chip stocks would be a great buy the dip coming up.