AI Gets Into Military Conflict

Palantir (PLTR) sold off on its earnings report, but that doesn’t mean it’s a bad stock.

Sometimes stocks can’t live up to their potential in the short-term, but long-term they should have no problem.

Growth slowed down a little and there is worry that revenue is too reliant on sources from America.

It’s positioned as an American-first company and the CEO Alex Karp doesn’t shy away from that fact.

The company is positioned perfectly as the best-in-class AI war stock and that label goes quite far in 2024.

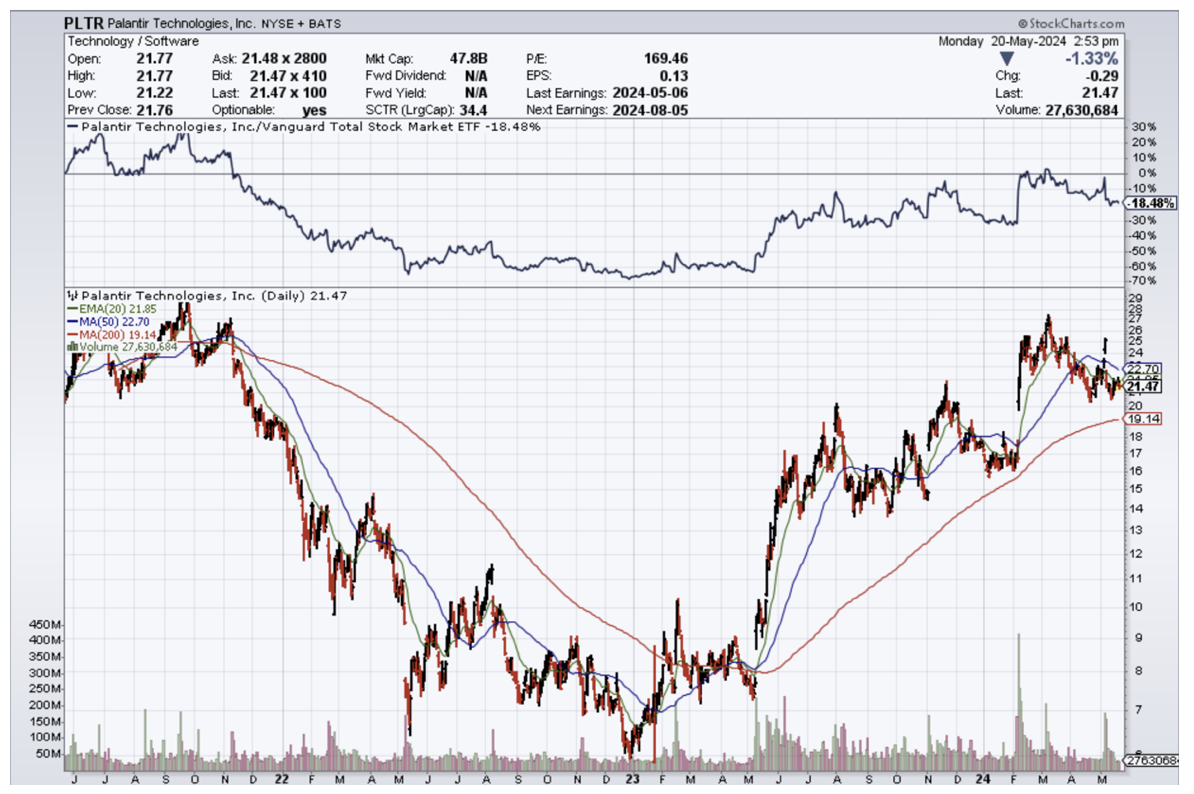

The business model does well when an explosion of conflict breaks out around the globe and one could argue that has been the case since 2022.

So it’s not a shocker to find out that the stock has done quite well since 2022 after tanking before that.

As the wars pile up, the company shares intel with agencies that pay for their knowledge through software and AI modeling.

They also offer companies a chance to use Palantir software to optimize their commercial business models.

If you haven’t heard, the Pentagon has failed audits for 6 years on the trot with trillions of bucks unaccounted for.

Even if PLTR investments are accounted for, the point is that money is pouring into the defense side of the equation.

This stock is certainly a “recession-proof” tech stock, and I would not say that PLTRs relatively short history brings uncertainty with it.

In the first quarter of 2024, Palantir's revenue of $634 million increased by 21%. While that is a considerable increase, it does not compare to a stock like Nvidia, which has experienced triple-digit revenue growth in recent quarters.

Additionally, the full-year 2024 revenue forecast calls for just under $2.7 billion. That would mean a 20% annual revenue growth rate, which may seem a little light when compared to other growth stocks.

PLTR’s U.S. commercial customer account rose 69% compared to year-ago levels.

Furthermore, when talking about its latest artificial intelligence platform (AIP), the company has reported eye-popping productivity gains. Palantir stated on its quarter-one earnings call that Lowe's utilized AI in its customer service department and reduced overdue tasks by 75%. Also, Cleveland Clinic was impressed enough to commit to a 10-year plan to deploy AIP across a network of hospitals.

In total, I do believe that PLTR will make major headway on the commercial side of revenue while profiting from the stable government revenue.

In a new era of AI, companies want to reduce tasks and optimize operations translating into bountiful revenue growth for PLTR.

Granted, the 20% revenue growth isn’t stuff of legends, but I do see a roadmap to double the company’s valuation from $50 billion to $100 billion if they execute well and keep improving the product.

That being said, buy incrementally on big dips of over 10% and that should be an effective strategy if a reader holds this stock long term.