Chip Manufacturers - A Way to Play 5G

From every minor data point coming from the semiconductor industry, we are seeing a tidal wave of new demand that is fueling a new megatrend of accelerated chip consumption.

We, yet again, get more confirmation from tech firms that this revenue surge is real and is happening as we speak.

Chip equipment makers have to be the best bet in tech of 2021, and I will explain why.

We are experiencing an assortment of macro and technology factors fueling robust demand for semiconductors.

As the world continues to navigate a health solution, the digital transformation of the economy is moving into warp speed.

Companies are reformulating the way they operate, and there is a dramatic pull for advanced technology.

This advanced technology needs a high volume of chips.

Consumers are now making digital-centered choices about the way they spend their time and the products and services they buy.

The benefits cannot be ignored and since new ways of working offer compelling advantages in terms of time and productivity, they will be irreversible.

Here are three examples driving increasing silicon consumption.

First, cloud service providers are predicting data center capex growth of more than 15% this year on top of record spending in 2020.

Second, due to the broader adoption of 5G handsets, silicon content in smartphones is growing at double-digit rates.

Third, in automotive, where there are known supply shortfalls since 2018, chip consumption is expected to expand more than 15% this year, translating these factors to heavy industry investments.

The IoT, communications, auto, power, and sensor markets are expected to grow even faster and are on track to exceed $3 billion of revenue for 2021.

This past year was a strong recovery year with spending up more than 30% and is set to continue.

The result is a strong demand environment for wafer fab equipment, and we believe this strength is sustainable well beyond 2021.

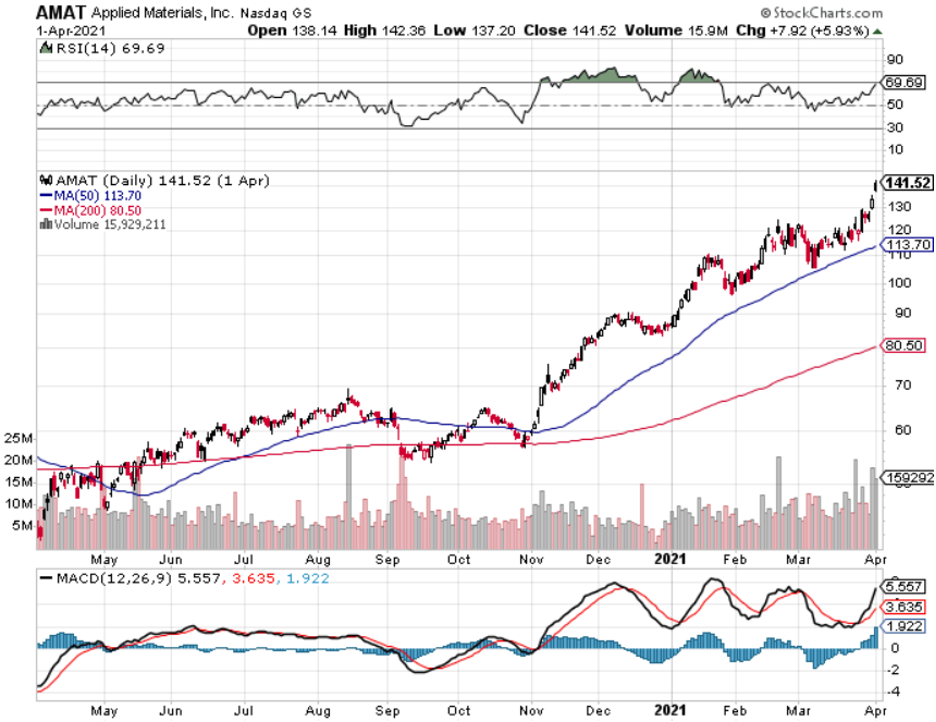

Investors should be looking at wafer fab equipment companies like Applied Materials (AMAT).

When you look at wafer fab equipment intensities, that's wafer fab equipment revenues as a percentage of semiconductor industry revenues, they are well below recent peaks in all three of the device segments: foundry/logic, NAND, and DRAM.

I would recommend one of the most important U.S. wafer fab manufacturers Applied Materials (AMAT) in order to capture the sweet spot of the explosion in chip demand in 2021 and the need to satisfy this demand.

The supply isn’t there and these capital investments mean more building of capacity which is great for (AMAT).

(AMAT) revenues for the first fiscal quarter were up 26% compared to the same period last year.

At the midpoint of Q2 guidance, semi systems will be up around 50% year on year.

There are a number of factors contributing to this overperformance.

(AMAT) has the broadest portfolio of products and capabilities, spanning materials creation, modification, removal, and analysis.

These technologies, combined with their ability to connect in unique ways, are fundamental to enabling customers' power, performance, and cost road maps.

(AMAT)’s latest-generation products have strong momentum, and more than 25% of 2021 revenues will come from critical applications that they have targeted and won since 2018.

Also, over the past few years, (AMAT) started introducing a new class of highly differentiated products that are called Integrated Materials Solutions, or IMS.

(AMAT)’s IMS products can combine multiple process technologies with onboard metrology and sensors within a single system that is capable of enabling unique films, structures, and devices.

Over the past five years, they have grown IMS services business at a compound annual growth rate of 12%, which is twice as fast as (AMAT)’s installed base growth.

Their renewal rates for these agreements are also extraordinarily high at over 90%.

I also see encouraging leading indicators of future growth, including higher OLED adoption in the smartphone market with the vast majority of 5G handsets being equipped with OLED screens and increasing OLED consumption beyond phones in TVs and IT applications.

The manufacturing of more chip equipment will all culminate with (AMAT)’s share price demonstrably higher by the end of 2021.

We are at the beginning of a boom in the wafer fab investment cycle and companies such as (AMAT) will be outsized winners in this 5G economic cycle with major investments into chip equipment taking place in 2021.