Another Gem In The Chip Industry

The hottest part of the tech industry is the build-out of the AI infrastructure.

Millions of data centers are needed equipped with high-speed chips to facilitate the miracle that is artificial intelligence.

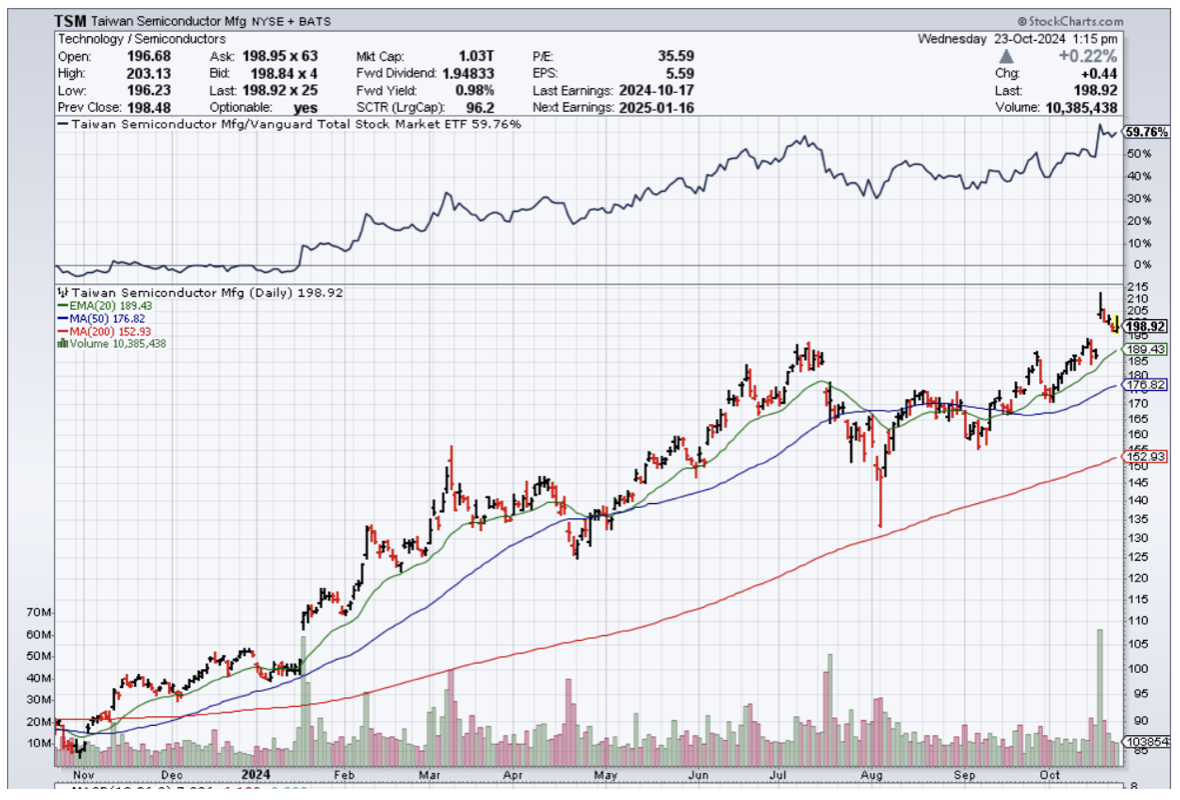

One of the leading companies right in the heat of the battle is Taiwan Semiconductor Manufacturing (TSM).

Why is TSM so important?

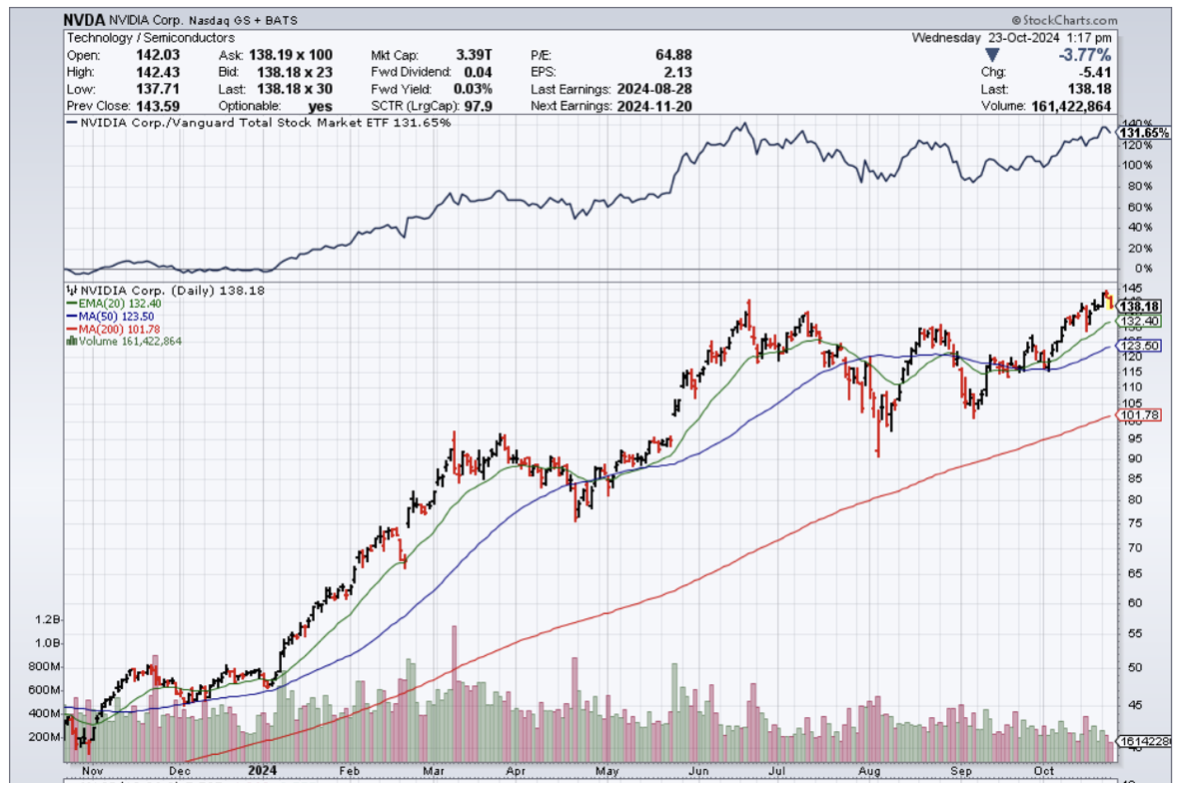

Nvidia (NVDA) outsources the manufacturing of its chip designs; TSM is the one doing the building, and that will mean a highly strategic position in AI moving forward.

TSM's other customers include several tech heavyweights like Advanced Micro Devices and Apple.

TSM has carved out a solid advantage in producing leading-edge logic chips used in advanced computing technologies such as AI and 5G mobile networks.

TSM is the world leader in manufacturing these specialized semiconductor chips, with an estimated 90% share of this market.

A key factor in TSM's market dominance is customer demand for chips using its three-nanometer (nm) semiconductor manufacturing process. Referred to as 3nm, this technology creates chips with greater microprocessor speed, lower energy consumption, and exceptional computational power without increasing chip size.

This 3nm tech looks like a game-changer for TSM. The process produces better chips than its older 7nm technology, which was once responsible for over a third of the company's revenue a mere three years ago. Just last year, TSM's 3nm-related revenue was a tiny 6% of third-quarter sales. But the rapid rise of AI drove 3nm income to reach 20% of quarter three revenue this year.

As 3nm-manufactured chips become more widely adopted, TSM's market share in this sector is expected to grow. This is because TSM's 3nm process generates higher yields and power efficiencies compared to those made by such competitors as Samsung.

TSM's 3nm strengths position the firm for revenue growth in the coming years. The market for the technology is forecast to skyrocket from $1.4 billion in 2023 to $26.5 billion by 2032.

With its 3nm process taking off, TSM experienced strong sales in the third quarter as revenue rose 36% year over year to $23.5 billion.

TSM's long-term sales potential looks to get a boost from the expansion of its chip fabrication facilities. Because leading-edge logic chips are needed for advanced computing, the U.S. government is incentivizing TSM to build semiconductor factories in the United States.

The underlying stock has delivered a 92% performance in the first 10 months of the year.

They certainly didn’t get left behind by the success of Nvidia, and I believe as we move forward, their strategic importance to the industry will grow and fortify.

I don’t believe that there is any slowdown in the pipeline coming any time soon.

The rhetoric from the AI chip management has been bragging about the over-demand and undersupply of chips.

This has created a massive surge in the profits for AI chip firms.

In the short term, the only negative that comes to mind would be that chip firms could be the victim of their own success reflected in overheated stock price trends.

We are due for a pullback, and that would certainly constitute as a buy-the-dip moment.

We have not seen the best of TSM yet, the best is yet to come.