The One Bright Start in the Healthcare Industry

The COVID-19 crisis has yanked the rug from under companies across all industries, and among the businesses that experienced a completely altered landscape these days is the health insurance industry. Imagine a business where sales increase fourfold overnight, but the customers can’t pay.

With the unemployment rate rising to historic levels since the pandemic hit, more people are dropping off commercial coverage rolls. Visits to the doctors and other elective procedures have been postponed indefinitely. Even political talks on healthcare reforms appear to be tabled until 2021.

Overnight, some doctors at country hospitals have seen workloads double and the suicide rate soar, while those in private practice are essentially unemployed.

While healthcare stocks are understandably struggling to survive, there are standouts that managed to take the blow without crumbling to ruins.

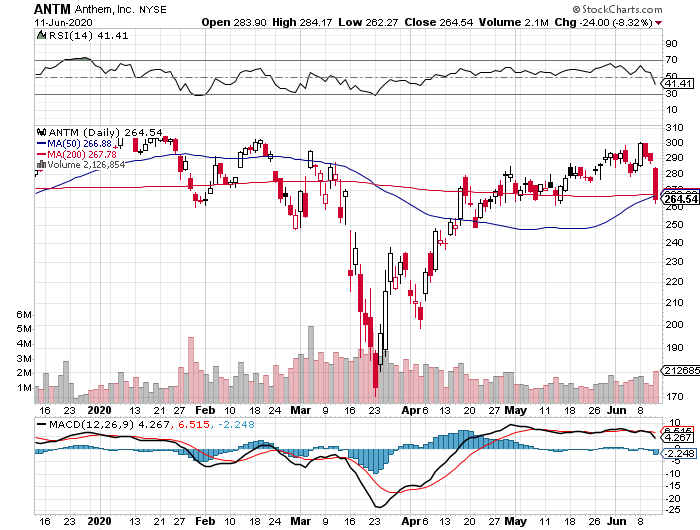

One of them is Anthem (ANTM).

With a market capitalization of $75.78 billion, Anthem is one of the biggest health insurers in the United States today.

Recently, the company wielded its power to offer $2.5 billion worth of premium credits as a form of financial assistance to its members during the pandemic.

This comes in the form of cost-share waivers, extensions for their virtual care coverage, and even assistance for struggling employers to help in maintaining the healthcare of their own employees.

While a lot of companies have been rapidly downgrading 2020 guidance due to the pandemic, Anthem updated its 2020 forecasts to reflect an increase in its adjusted net income from $19.44 per share to an eye-popping $22.30.

This indicates that Anthem has extra bandwidth for growth primarily thanks to its stable revenue stream, increasing membership, and solid earnings.

In its first quarter report for 2020, Anthem’s operating revenues jumped by 20.7% year over year to reach $29.4 billion, with profits from its IngenioRx launch.

As for its net income in the said period, Anthem raked in $1.52 billion or roughly $5.94 per share compared to $5.91 per share in 2019.

Anthem even increased its dividend by 19% in January.

However, it’s Anthem’s cash flow that continues to impress. From 2019 up until the first quarter of this year, Anthem’s cash flow surged by 58% year over year.

One of the main factors that boost the growth of a health insurance company is membership, and Anthem managed to tick off that box as well in the first quarter.

Anthem’s medical enrollment climbed to 42.1 million members, showing off a 3.2% increase year over year. With backing from government business enrollment as well as commercial and specialty businesses, this number is expected to climb higher this year.

Even Anthem’s inorganic growth ventures promise great results, with acquisitions and collaborations continuously boosting the Medicare Advantage growth of the company.

A good example is its acquisition of the Medicaid members in Missouri and Nebraska via WellCare Health at the beginning of 2020. This led to 849,000 lives added to its government business enrollment since 2019.

Meanwhile, its acquisition of AmeriBen added 452,000 members to its commercial and specialty business sector.

Anthem’s takeover of Beacon Health, which is the biggest independent behavioral health firm in the US, serves to further strengthen its position in this sector. This move added roughly 300,000 Medicaid members under Anthem’s coverage.

In terms of adapting to the needs of its members during the pandemic, Anthem is making more aggressive moves to promote its telehealth services.

Although this sector is currently widely associated with Teladoc Health (TDOC), which has a market capitalization of $12.93 billion, the rest of the league is catching up quick.

Since the average cost per telehealth session is roughly $100 less compared to fees paid in visits to the doctor’s office, this is definitely a platform-managed care providers are looking into.

According to Anthem, its telehealth app recorded over 170,000 new downloads since the COVID-19 crisis started.

It also reported a 250% surge in the demand for its virtual care services.

Anthem isn’t the only health insurer joining the telehealth fray. CVS Health (CVS), Humana (HUM), Centene (CNC), and even industry leader UnitedHealth Group (UNH) has been looking into the service.

In this period of uncertainty, choosing a stable company with a robust outlook and sold at a reasonable price is always a wise investment.

With Anthem’s profits projected to grow by roughly 47% over the next years, this company’s future offers security to its investors. Its impressive cash flow also plays a significant role in its higher share valuation.