August 26, 2024

(WILL NVIDIA’S EARNINGS JUICE THE MARKET, PUT IT TO SLEEP OR TANK IT?)

August 26, 2024

Hello everyone

Week ahead calendar

Monday Aug. 26

8:30 a.m. Durable Orders (July)

Previous: -6.6%

Forecast: 4%

10:30 a.m. Dallas Fed Index (August)

Tuesday Aug. 27

9:00 a.m. FHFA Home Price Index (June)

9:00 a.m. S&P500 /Case Shiller Home Price Indices (June)

10:00 a.m. Consumer Confidence (August)

10:00 a.m. Richmond Fed Index (August)

9:30 p.m. Australia CPI Indicator

Previous: 3.8%

Forecast: 3.4%

Wednesday Aug. 28

No notable economic data.

Earnings: Nvidia, Bath & Body Works, J.M. Smucker, Salesforce, CrowdStrike, NetApp, HP

Thursday Aug. 29

8:30 a.m. Continuing Jobless Claims (08/17)

8:30 a.m. GDP second preliminary (Q2)

8:30 a.m. Initial Claims (08/24)

8:30 a.m. Wholesale Inventories preliminary (July)

10:00 a.m. Pending Home Sales Index (July)

Earnings: Campbell Soup, Best Buy, Dollar General, Autodesk, Ulta Beauty, Lululemon Athletica

Friday Aug. 30

8:30 a.m. PCE Deflator (July)

8:30 a.m. Personal Consumption Expenditure (July)

Previous: 2.6%

Forecast: 2.6%

8:30 a.m. Personal Income (July)

9:45 a.m. Chicago PMI (August)

10:00 a.m. Michigan Sentiment final (August)

This week is dominated by Nvidia earnings which are out Wednesday.

They will be closely watched as a guide to the direction of the whole sector, and the market as a whole.

On Aug. 5 we saw Nvidia shares fall as low as $90.69 per share amid a broader market sell-off, as well as reports of delays on its Blackwell chips. (Here, I told everyone to add weight). Now, they’ve surged more than 40%, to about $125 per share currently, as traders rushed to buy the dip.

CEO, Jensen Huang has revealed that the newest generation of its chips cost around $10 billion in research and development. Now, that is a huge barrier to entry for any competitor.

There are high expectations ahead of these results, so there is a possibility that the stock and the market could either act benignly to Nvidia’s numbers or dive.

Also noteworthy of attention this week is the July personal consumption expenditures price index (PCE). The numbers here could show that the Federal Reserve is well on its way to its 2% inflation objective, as the central bank prepares to cut rates in September – an action that Chair Jerome Powell last Friday indicated in his Jackson Hole speech.

“The time has come for policy to adjust…the direction of travel is clear, and the timing and pace of rate cuts will depend on incoming data, the evolving outlook, and the balance of risks.”

A softer inflation print implies investors can turn their attention to the labour market – next month’s job’s report, which could determine whether the Fed lowers rates by a quarter or half-percentage point in September.

Markets are currently pricing in the likelihood the key overnight lending rate will fall one percentage point by the end of the year to a range 4.25% - 4.5%.

Wall Street is bullish. But the journey from now until the end of the year may be fraught with turbulence, and high drama. Don’t forget we are in a seasonally weak period for stocks, and we are also heading into the U.S. presidential election. Add to that the ongoing geopolitical risks around the globe.

By and large, Wall Street is still shrugging its shoulders at world events and mapping out its own path.

But black swans are always lurking: what if the Fed back peddles on a 50pt rate cut, and what if the conflicts around the world escalate? And what if we are blindsided by something that is totally out of left field?

As I highlighted in an earlier post from a piece entitled – think backwards: think what can go wrong and then take steps to shore up your world against sudden shocks. Even more importantly, check your behaviour, and know what action to take after a shock takes place.

MARKET UPDATE

S&P500

We are still in an uptrend, but exhaustion is approaching. In the short term, the market’s strong rally from its 5,119 corrective Wave 4 low of October 5 is nearing completion and could well peak in the short term.

Then we are at a juncture. Either the market will correct to a Wave ii of Wave 5, enabling this final fifth wave advance to subdivide and extend considerably further over coming weeks/months before the bull market is exhausted, or it will mark the completion of Wave 5 itself, ushering in a bear market.

I am inclined to favour the former and am looking for the market to reach our H & S target of 5,735 or even rally towards 6,000 before exhaustion.

GOLD

The yellow metal continues in an uptrend after it showed a sustained break through the $2,500 level.

Support = $2,470/$2,500

Targets = mid $2,500’s and then on to $2,670.

BITCOIN

It’s possible to interpret a completed corrective structure here, which should enable the resumption of the coin’s uptrend.

Support= around $62,700/$61,500

Next Resistance = around $69,300

QI CORNER

PSYCHOLOGY CORNER

If It Fits, Take It

Take every setup that fits your system when it crosses your path. No amount of over-analysis will tell whether it really will work or not, but as long as it fits your setup, it’s good to take. When we over-scrutinize well-fitting setups, we create tension and anxiety. Take every opportunity that fits and allows you to trade in harmony with the market and put your faith in your setup, not your overly critical mind.

Know When to Cash Out

Regardless of whether you have a great analysis of what you think the market is going to do, you must develop a clear plan for exiting a trade a winner. Without a clear trigger, many traders will hold on, expecting (and hoping) the market will move in the direction their analysis indicated. The problem is the market doesn’t always go in the way well-thought-out analysis said it would. Have a trigger in place to take your profits rather than let the market deliver a clear exit sign.

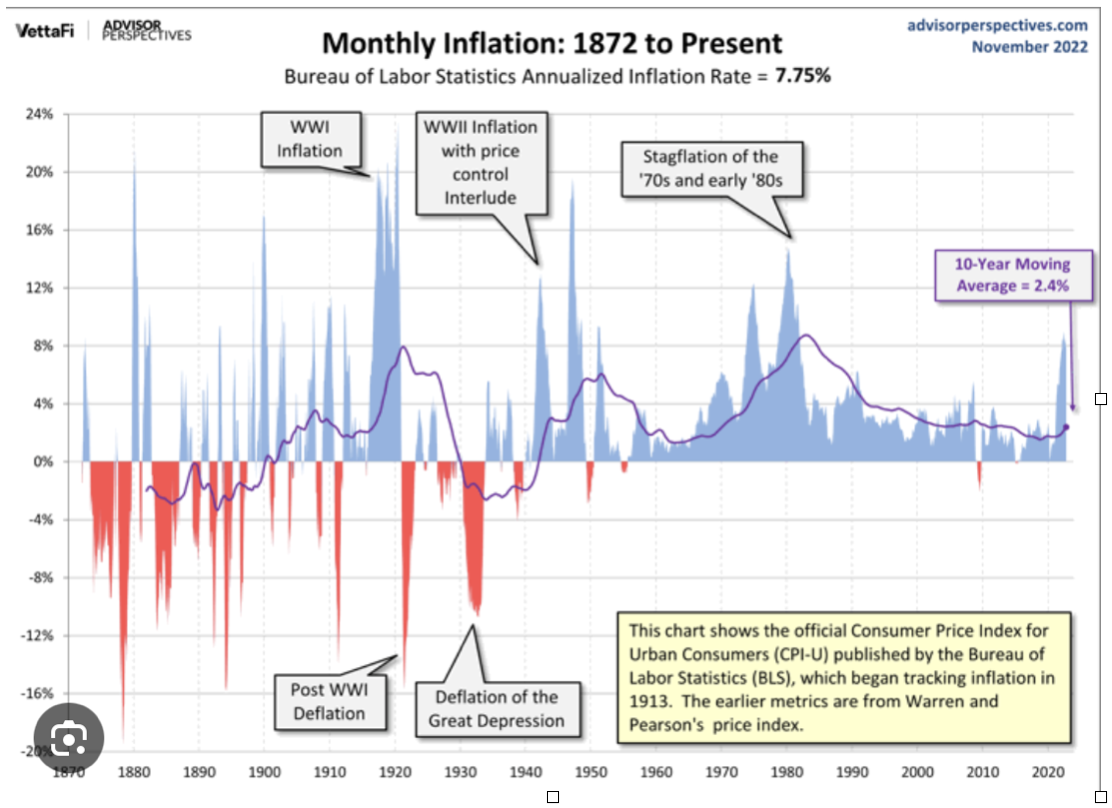

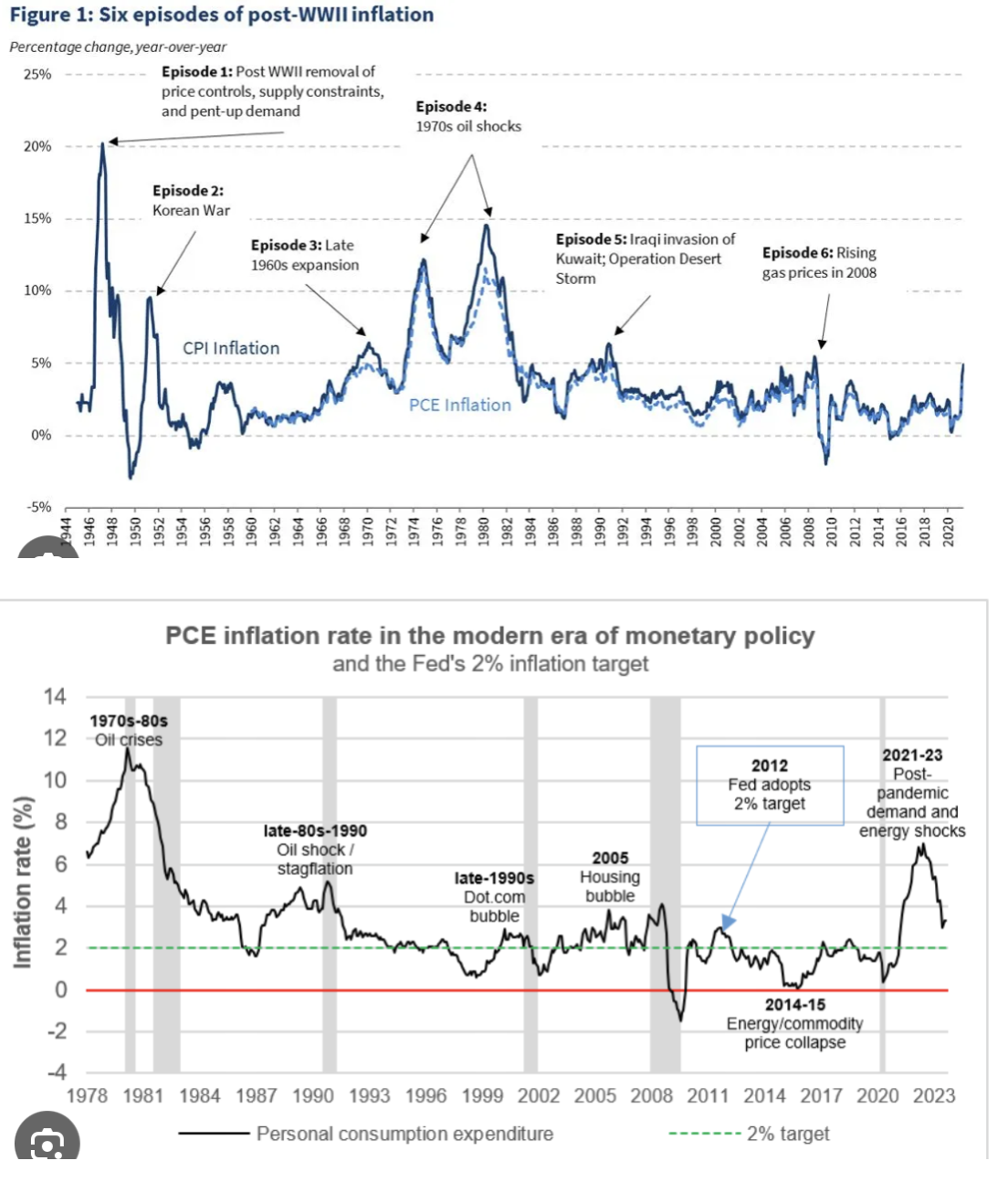

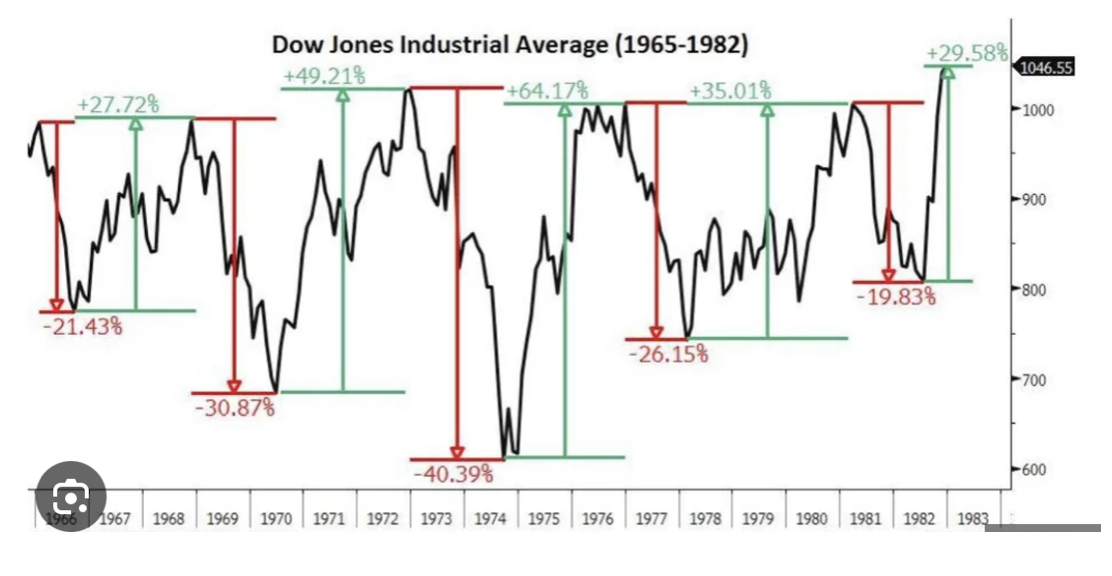

HISTORY CORNER

A period of Great Inflation lasted from 1965-1982.

Over the nearly two decades it lasted, the global monetary system established during World War II was abandoned, there were four economic recessions, two severe energy shortages, and the unprecedented peacetime implementation of wage and price controls. Siegel saw it as “the greatest failure of American macroeconomic policy in the postwar period.”

But out of failure can also come change, and that became evident in macroeconomic theory, and the rules that today guide the monetary policies of the Federal Reserve and other central banks around the world. If the Great Inflation was a consequence of a great failure of American macroeconomic policy, its conquest should be counted as a triumph.

SOMETHING TO THINK ABOUT

“He who buys what he does not need steals from himself.” – Swedish Proverb

Cheers

Jacquie