Avoid This Korean eCommerce Company

I might characterize Coupang (CPNG) as something akin to China’s JD.com.

It's an e-commerce company that has fulfillment solutions, not dissimilar to Amazon (AMZN) Fulfillment. They also have storefronts that they provide for businesses, which isn't dissimilar to say, a Shopify (SHOP).

Even combining aspects of Amazon and Shopify are there but they don’t have the powerful AWS cloud business.

Similar to JD.com (JD), which is a Chinese e-commerce platform, Coupang has differentiated itself by owning its entire logistics and delivery system.

What is different about Coupang versus the other players in Korean e-commerce is that they own their own inventory for the most part.

That means that they have inventory sitting on their balance sheets.

They have responsibility for pushing that through. But it also means, since they directly negotiate with the manufacturers of these items, they're able, for the most part, to get lower prices.

Total Korean e-commerce spend was $128 billion in 2019, which is expected to grow to $206 billion by 2024, implying a CAGR of approximately 10%.

This is where Coupang has a chance but in a rising interest rate environment and with competition on the New York exchanges from Amazon (AMZN), Shopify (SHOP), even MercadoLibre (MELI), I don’t believe Coupang is more attractive than these 3 in its current form as it relates to American investors pouring money into their stock.

Is it an advantage if 70% of Koreans live within seven miles of the Coupang logistic centers?

Certainly, there is that train of thought.

The massive investments into fulfillment centers mean they can surpass the delivery speed of many of its competitors because South Korea is essentially one capital city with millions upon millions hovering on top of each other like many other parts of Asia.

The problem I can have with this scenario is that margins could suffer because a busy Korean lifestyle doesn't lend itself to things like in-store shopping as readily as it does in the United States, and it could manifest itself with Koreans tapping into higher frequency in which they buy online which will push up total spend, but margins will decrease because you are buying stuff that won’t move the needle higher because you've paid for the service.

I can easily see someone just buying one item for delivery in the morning and doing that seven days per week.

Now I need a set of tweezers, I'm going to order that. Tomorrow, I need cotton pads, I’m going to order that.

Over time, operating margin will get butchered with a business like this.

And what do you know? I’m right, they have been losing billions upon billions the past few years with no end in sight.

How long will the external investors subsidize their losses?

At a broader level, mobile phone penetration is already at 96% of Koreans and 40% of Koreans order groceries online, so it’s hard for me to digest where the addressable market can expand from here because they have already collected so much of the available harvest.

This IPO does feel a little bit like an ex-growth dump on the retail investor and that’s not saying shares can’t appreciate at all, but investors believing this is the next Amazon are sorely mistaken.

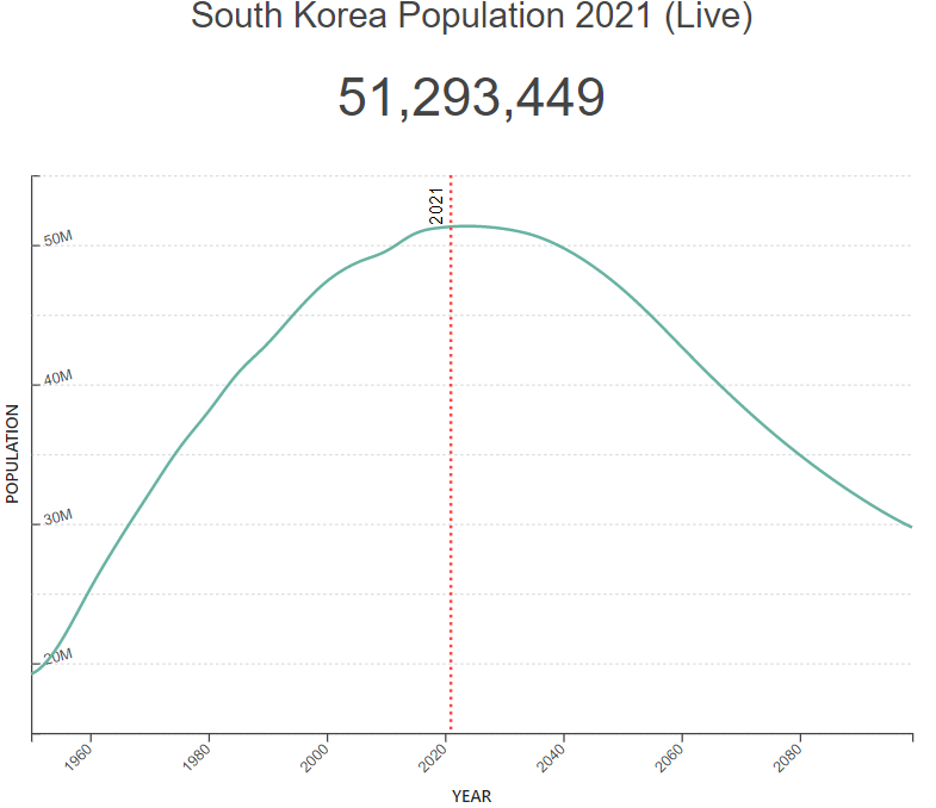

They are not Amazon, not even close, and they are also confined to one small market where the population has peaked and will start decreasing in numbers.

The population is only 15% of the U.S. and incomes in the U.S. are vastly higher, so how does Coupang become an Amazon without the AWS business?

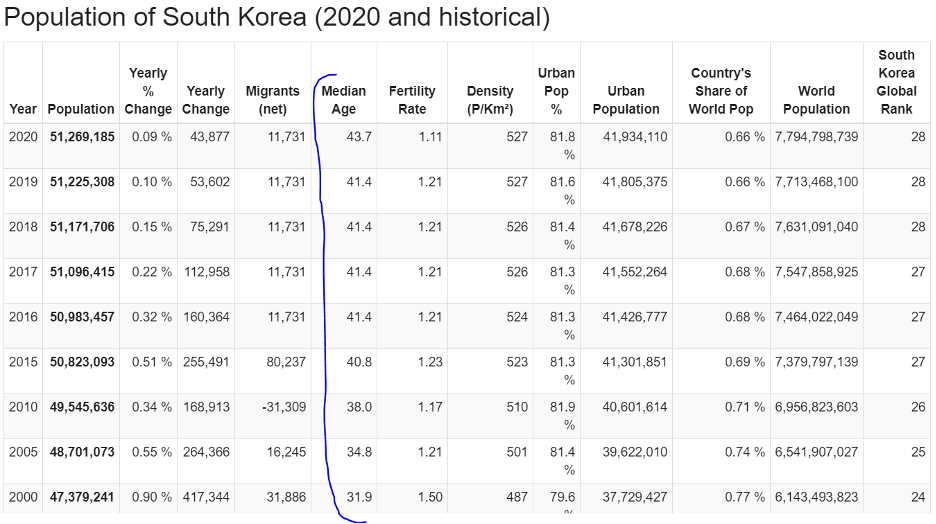

Just as disturbing, the median age in Korea has ballooned from 31.9 in 2000 to 43.7 in 2020 and this cohort doesn’t strike me as the group in the glory years of family formation, peak spend, or technological know-how.

As the Korean population starts to decline in 2025 and the median age creeps up from 43.7 to 50, then aside from adult diapers, where does the incremental growth come from in Korea?

I just don’t see it.

Personal incomes are going to rise at an annualized rate of about 3% every year and I believe much of the total spend will be fought out attempting to woo the big buyers which offer a point of attack for competition that should come around in the next 2 to 3 years.

They also have Coupang Eats, not dissimilar to Grubhub (GRUB) or Uber (UBER) Eats. They have grocery delivery, and even an integrated payment processor. All of these things that took Amazon much longer to build out, admittedly, were a little before their time there, Coupang has already integrated that into the platform.

For this, I give them credit, but they are still nothing like Amazon in terms of potency and scale.

In 2019, active customers rose 34% and that’s what a prototypical growth company should do.

It’s not shocking.

Then an analyst would think that with covid and all that public chaos pinning consumers at home, surely, Coupang would grow active customers by 50% of even 60% in 2020, right?

But active customers only grew 18% in 2020, and they provided zero insight about why active customer growth slowed nearly in half year-over-year, and that for me shows, Coupang is severely limited by what Korea can offer in terms of growth and total spend.

If readers want to get into the Korean economy then I would advise to wait on other Korean homegrown entrepreneur-led startups with IPOs in the pipeline by Krafton Inc., the creator of hit game PUBG, and the country’s biggest mobile-only bank Kakao Bank. Unlike Coupang, those firms are profitable.

Ultimately, total e-commerce spend for all Internet buyers in Korea is expected to grow from approximately $2,600 in 2019 to approximately $4,300 in 2024 on a per buyer basis and Coupang will take advantage of that but I don’t foresee the 30% annual rise in underlying shares that others do.

I can definitely visualize a grind up with periodical substantial selloffs because of missed targets and disappointing forecasts.

That’s not the type of price action I want to see.

The signs point to Coupang maturing immediately and the executive management creating a special clause to allow them to dump shares right after the IPO illustrates that this tech company will stall out moving forward.

Normally, management must wait 6 months after going public before the lock-up period ends.

Highly unusual and can you believe it? They even gave stock shares to their courier drivers at the IPO, making me pause, then come to the conclusion that I rather invest in a tech company returning incremental value to the shareholders and not the manual labor that is paid by an hourly wage. How bizarre!

Avoid Coupang like the plague.