Big Risks To Tech Dissipate

I don’t believe the tech sector is toast and it isn’t true to say that the burnt crust is the only part left over.

There is still vitality in it at the core of the tech sector ($COMPQ).

Granted, the trajectory left isn’t enough to propel tech stocks to a meteoric rise, but tech stocks should perform quite robustly in the run-up to the next earnings report.

So for all that are waiting for the bubble to burst – wait a little longer my friends.

In the meantime, let’s take a quick barometer of some of the outsized risks to big tech and ponder about the idea that outside or indirect events could possibly takedown tech shares.

China bailed the world out of the last three recessions and now they are a risk to drag down the rest of the world.

In each case, China's high growth and massive issuance of stimulus kick-started global expansion, and now that is gone with the wind.

China's model of economic development which worked so brilliantly in the boost phase, is now out of potency.

If American tech shares are sideswiped by global contagion, don’t bet on China to come bail out the radical overlords of Silicon Valley. China has its own problems and is entirely focused on that.

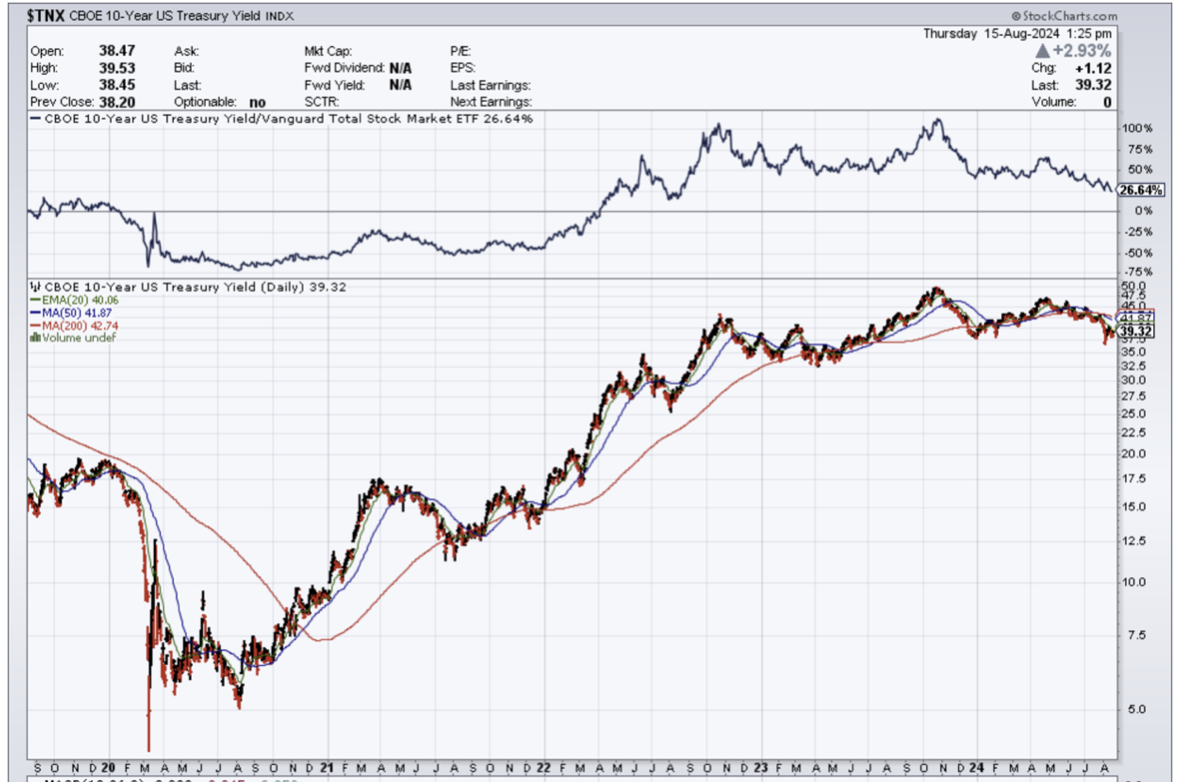

The era of zero-interest rates and unlimited government borrowing has ended. As Japan has shown, even at insane low rates ($TNX) of 1%, interest payments on skyrocketing government debt eventually consume virtually all tax revenues.

Japan was the black swan that could have cratered the tech market. Instead, it was a mild selloff yet manageable selloff creating a beautiful entry point for most of tech stocks.

Money is coming off the sideline to join in on a sharp rally into the U.S. presidential election so in the end the Japanese currency (FXY) risk was basically much-a-do-about-nothing.

At the start of the cycle, global debt levels (government and private sector) were low. Now they are high. The boost phase of debt expansion and debt-funded spending is over, and we're in the stagnation-decline phase where adding debt generates diminishing returns.

The era of low inflation has also ended for multiple reasons, but the tech shares have proven they can unequivocally march higher in an era of high inflation.

This is ironically due to tech being better positioned than other industries on a relative basis, because of their strong moats and iron-clad balance sheets.

The resilience in tech also echoes the idea that every company has become a tech company by integrating its products and revenue streams into daily business operations.

Tech productivity boom is hardly a one-off so as readers fret, please don’t think shares will magically drop to zero.

Dips are being bought and prices will go higher in the short term.

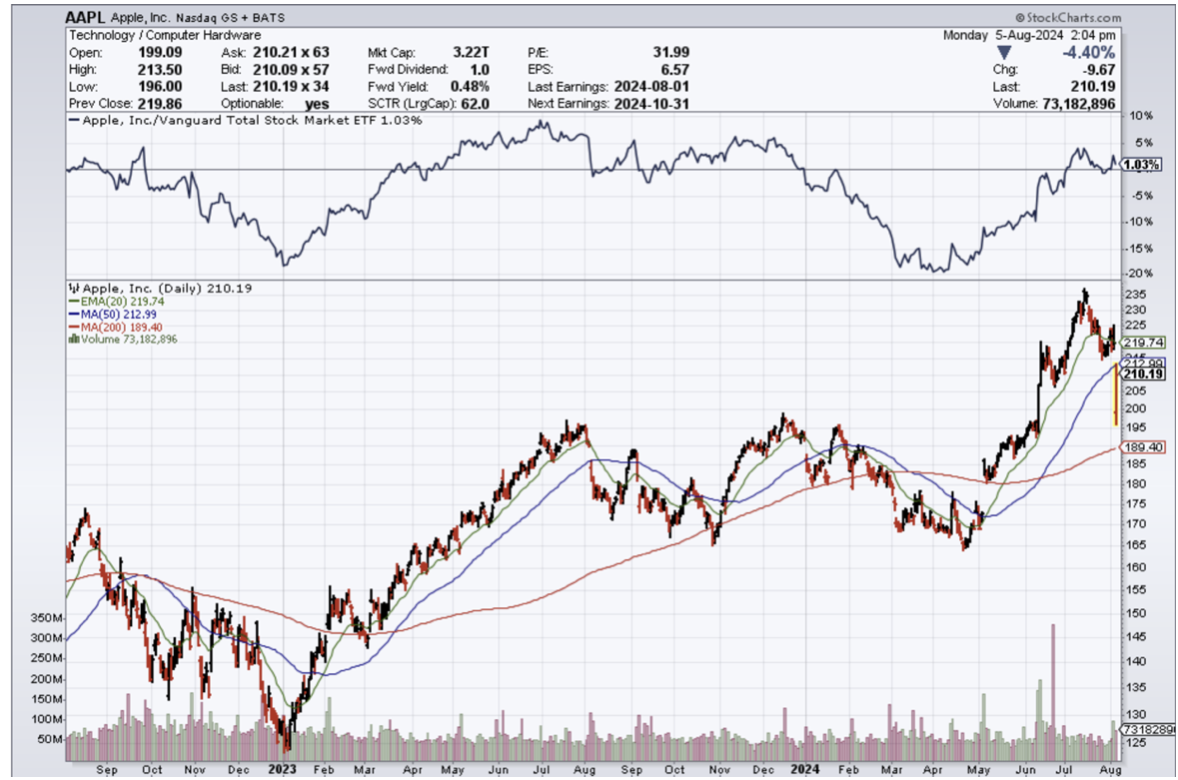

Economists were in awe in the early 1990s by the productivity stemming from the tremendous investments made in personal and corporate computers, a boom launched in the mid-1980s with Apple's (AAPL) Macintosh and desktop publishing, and Microsoft's Mac-clone Windows operating system.

By the mid-1990s, productivity continued to rise and the emergence of the Internet triggered the adoption of most of the population to get online and do business.

All the doomsday prophets who said high debt and high interest rates were the cocktails to finally stop tech stocks in their tracks got it completely wrong.

I am not saying debt and high interest rates are positive for equities, but tech has been able to skillfully navigate the headwinds with their excellent management skills and pivot towards leanness.

The buzz around AI holds still has a lot to prove, but the market is still celebrating its deflection of the Japanese yen carry trade.

I am not saying that tech shares will never have to confront anything that can drag them down meaningfully, but many of the high risks have either been postponed or dealt with.

We are in a position where tech should steamroll into the end of the year barring some type of crazy event.