BioTech Alert - (AMGN) September 26, 2019 - BUY

When John identifies a strategic exit point, he will send you an alert with specific trade information as to what security to sell, when to sell it, and at what price. Most often, it will be to TAKE PROFITS, but, on rare occasions, it will be to exercise a STOP LOSS at a predetermined price to adhere to strict risk management discipline.

Trade Alert - (AMGN) - BUY

BUY the Amazon (AMGN) shares on the next substantial dip

Amgen’s New Blockbuster Drug

As an impoverished undergraduate at UCLA during the early 1970s, I had the privilege to work for Dr. Winston Salser, considered the most brilliant scientist in America who never won a Nobel prize.

His team was trying to break the genetic code by learning how to sequence DNA, working with molecules supplied by Dr. James Watson of Harvard University. After years of toiling, we did it. In the end, his partner, Dr. Mark Boyer, got the prize. The work later became the basis for the burgeoning human genomics industry of today.

As for me, I received my work study pay of $1.00 an hour and an exciting entry on my resume, which no one has read for decades.

In 1980, Dr. Salser went on to help found a company with a name that then sounded like it came out of a science fiction novel, Applied Molecular Genetics, with $200,000 in seed capital. Today, that company is known as Amgen (AMGN).

The company went public in 1983, and Dr. Salser, who had been wearing the same seedy tweed jacket with the worn elbows for 30 years, suddenly became a millionaire. Amgen went on to create a series of blockbuster drugs, including Epogen, which is used to accelerate red blood cell growth in cancer patients.

In the ultimate irony, it was Epogen that extended my late wife’s life by four years when she had breast cancer in the 1990s. I remember putting the $1,000 a shot cost on my American Express card because the insurance company wouldn’t pay for it. Today, it will pay. All the other patients who couldn’t afford Epogen died.

Amgen’s market capitulation has since soared from the initial IPO value of $43.1 million to a staggering $117 billion today. A $1,000 investment in Amgen in 1983 would be worth $2.72 million today.

Well, guess what?

AMGEN (AMG) is on the brink of another medical breakthrough. The company has revealed that its experimental drug, AMG 510, exhibited the ability to significantly shrink the size of cancer tumors by an unbelievable 50%. The results were from the early-stage trials performed on advanced lung cancer patients.

In a nutshell, AMG 510 could become the first-ever approved treatment that can target a mutated type of a gene called KRAS, which is one of the most common mutations involved in non-small cell lung cancer (NSCLC). The American Cancer Society identified NSCLC as the leading cause of cancer death, accounting for 85% of lung cancers. Thank you, Philip Morris.

For decades, researchers have been searching for ways to address KRAS mutations, with the sought-after solution dubbed as the "white whale of drug discovery." With the first proof-of-concept presented a mere six years ago, the rapid development of Amgen’s experimental drug has enormously impressed researchers in the field.

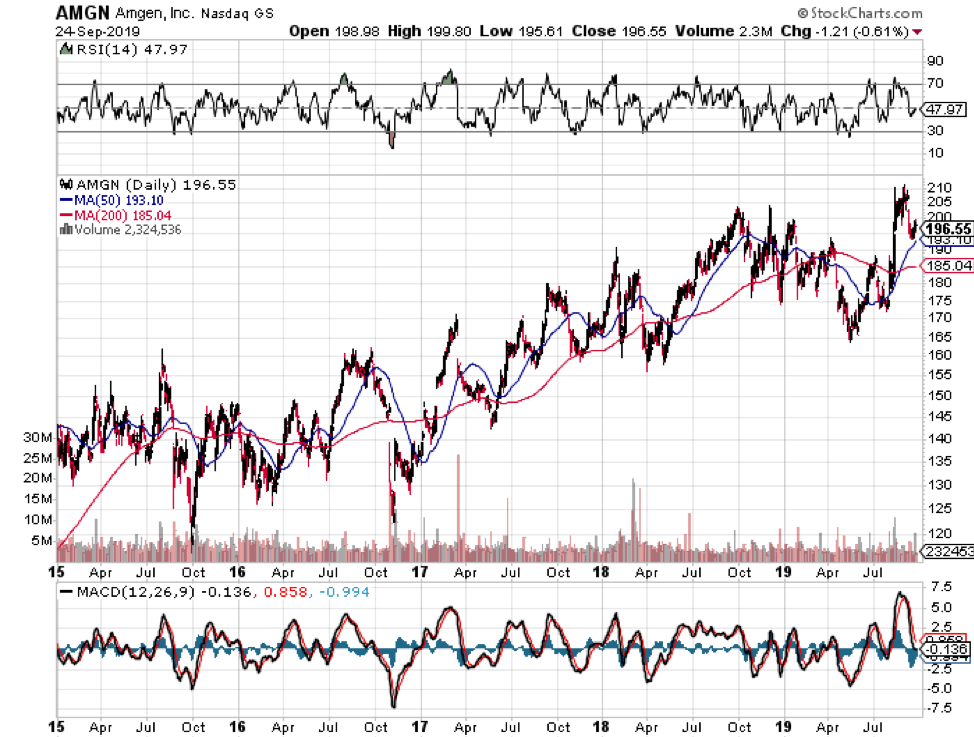

Simply put, this drug is a game-changer for particular types of cancer. Subsequently, its success will bring incredible profits for Amgen shareholders. You can see this on the chart below. (AMGN) is about to break out of a three-year double top to a substantial new all-time high

The announcement of AMG 510’s promising results saw a jump in Amgen shares of only 6.1%, a new all-time high. That means there is plenty of room to run. While this drug remains in its initial trial phase, the fact that it addresses a huge unmet need in oncology makes it a prime candidate in becoming the next blockbuster drug for Amgen.

Aside from lung cancer, this drug is also aimed at providing treatment for colorectal cancer and pancreatic cancer. To date, AMG 510 sales is estimated to reach more than $1 billion and peak at $2 billion.

With the extremely attractive market for this particular drug, it comes as no surprise the Amgen is not alone in the race.

So far, two more biopharma companies are looking to develop similar medications: GlaxoSmithKline Plc (GSK) and Mirati Therapeutics (MRTX). While the former has yet to reveal the covalent inhibitor drug it’s currently developing, reports indicate that Mirati’s work involves a drug called MRTX849. Aside from these, no other information has been released by the two companies.

While these are encouraging results vis-à-vis its oncology department, how is Amgen doing so far this year through?

AMG 510 isn’t the only story at Amgen. Its recent $13.4 billion purchase of Otezla, the blockbuster psoriasis and psoriatic-arthritis drug at the center of the turbulent merger involving Celgene Corporation (CELGN) and Bristol-Myers Squibb Co (BMY). This purchase, albeit on the expensive side, will be a tremendous boost to Amgen’s weakening top side.

Although pipelines are widely regarded as the lifeblood of any biotech company, Amgen’s portfolio currently heavily skews toward programs in their early stages of the study. In fact, the company has 24 programs in Phase 1 compared to the measly five programs in their late stages.

Based on its earnings report in the first quarter of 2019, Amgen recorded $5.6 billion in total revenues. This matches the amount the company reported during the same quarter in 2018. Despite the promising projects in its pipeline, Amgen’s product sales saw a 1% dip globally.

However, its new products showed double-digit increases in the first quarter. Osteoporosis and hypercalcemia drug Prolia reported a 20% increase while cardiovascular medication Repatha also showed a 15% revenue jump during the first quarter. Even the revenues for relapsed multiple myeloma treatment Kyprolis showed a 10% rise in this period.

As for its earnings per share (EPS), Amgen is strolling at a lowly 12.53 multiple. This indicates an EPS growth of 14.8% this year, which could lead to a projected 5.25% EPS growth for 2020.

Meanwhile, Amgen’s positive outlook particularly with AMG 510 as an additional blockbuster drug in its portfolio prompted the company to adjust its earnings expectations for this year. In terms of its expected revenue, Amgen raised it from $21.8 billion to $22.9 billion range to $22 billion to $22.9 billion.

Given the recent developments in Amgen, the company shares are now an attractive “BUY”. I don’t necessarily mean buy today, but buy during the next substantial dip in the market which could be taking place shortly.