Mad Hedge Biotech and Healthcare Letter

September 26, 2024

Fiat Lux

Featured Trade:

(GOWN UP FOR SUCCESS)

(UHS)

Mad Hedge Biotech and Healthcare Letter

September 26, 2024

Fiat Lux

Featured Trade:

(GOWN UP FOR SUCCESS)

(UHS)

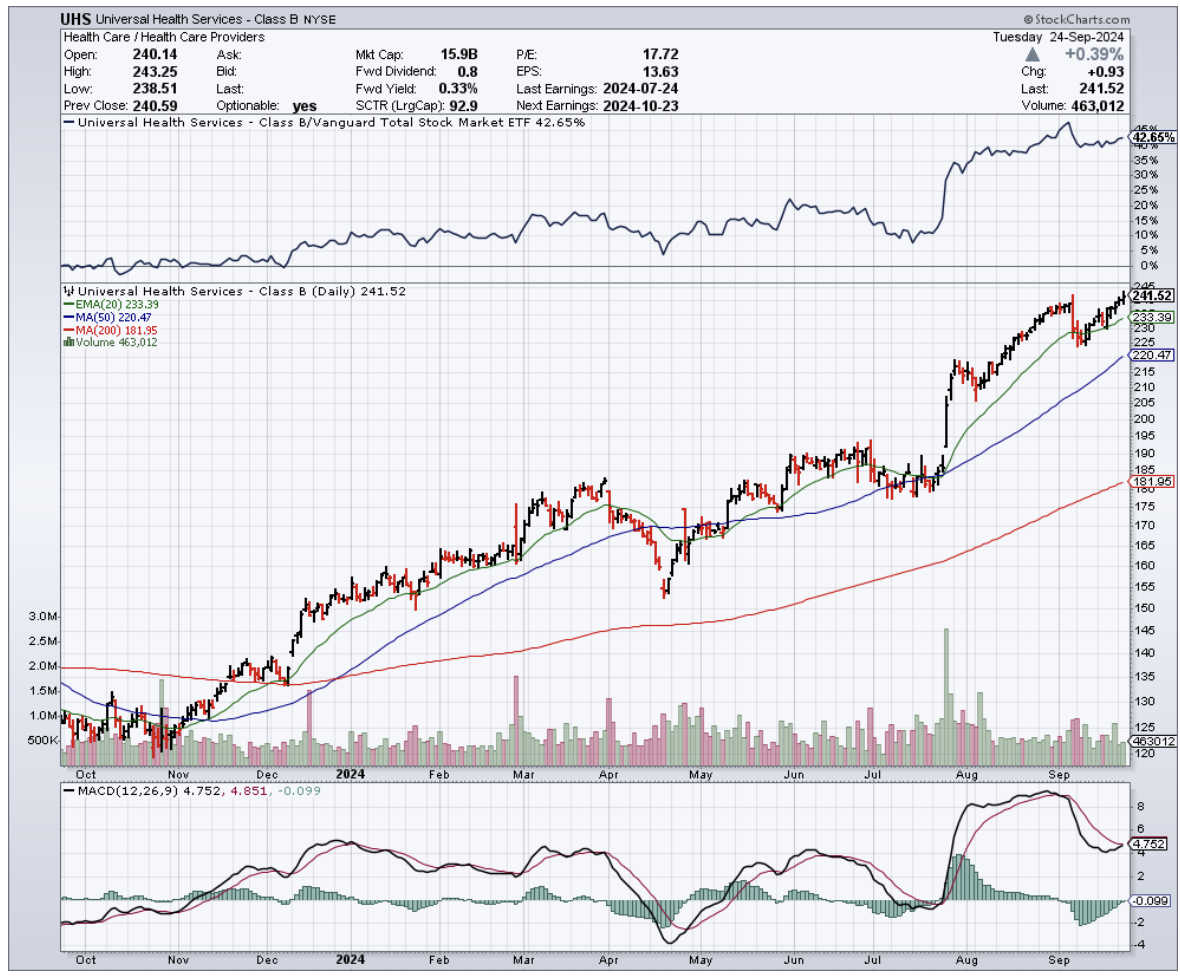

Well, folks, it looks like we've stumbled upon a diamond in the rough in the healthcare sector. Universal Health Services (UHS) has caught my eye, and let me tell you, it's not just because I've spent more time in hospitals lately than I care to admit. (Note to self: skydiving and arthritis don't mix.)

Now, I've been around a while, and I've learned to spot a good deal when I see one. UHS is trading at a valuation that's making my wallet itch. We're talking about a forward P/E of just 13x based on analysts' 2025 EPS estimates of $17.85.

To put that in perspective, it's like finding a Rolex at a yard sale - the Medical Care Facilities industry is strutting around with a 17x forward P/E.

And here's where it gets really interesting. UHS is sporting a PEG ratio of 0.62. For those of you who dozed off during Finance 101, that's like getting a growth stock at a value price. The industry average is sitting pretty at 1.56, making UHS look like an absolute steal.

Now, let's talk about what UHS actually does. They're in the business of owning and operating acute care hospitals, outpatient facilities, and behavioral healthcare centers.

As of Q2 2024, they've got 359 inpatient facilities and 48 outpatient joints spread across 39 states, D.C., Puerto Rico, and even jolly old England.

The company operates under two main segments: Acute Care Hospital Services, which brings in about 87% of the bacon, and Behavioral Health Services, accounting for the remaining 13%.

Inpatient revenue from both segments makes up roughly 64% of total revenue, with outpatient services filling in the rest.

Now, here's where things get even more interesting. The global hospital services market is expected to expand quickly – we're talking about a 6.4% annual growth rate, potentially hitting $21 billion by 2032.

But UHS isn't just sitting pretty waiting for the market to grow. Oh no, they're expanding faster than a tech startup with too much venture capital.

They've got plans for 12 new freestanding emergency departments, a 150-bed acute care hospital under construction in Vegas (because what happens in Vegas... might need medical attention), a 136-bed hospital in D.C. set to open in spring 2025, and a 150-bed facility in Palm Beach Gardens, Florida, ready to roll in spring 2026.

And let's not forget about their Behavioral Health segment. They recently opened a 128-bed behavioral hospital in California and are cooking up a 96-bed joint venture in West Michigan.

Now, I've seen my fair share of companies promise the moon and deliver a mere pebble, but UHS seems to be putting their money where their mouth is.

Just in Q2 2024, they saw their gross margin jump from 39% to 42.6% year-over-year. Operating income margin? Up from 7.9% to 11.2%. Net income margin? A healthy increase from 4.8% to 7.4%.

And they're not just calling it a lucky quarter - they're expecting to keep this party going for the next few periods.

With all this good news, UHS has bumped up their 2024 EPS guidance by a whopping 17% to $15.80 per diluted share.

On top of all these, they've also increased their stock repurchase program by $1 billion, bringing the total authorization to $1.228 billion.

For those of you who slept through that part of business school too, that's like making your slice of the pie bigger without having to bake a new one.

Now, I'm not saying UHS is without risks. They've got a high concentration of revenue in California, Nevada, and Texas. It's like they're betting big on blackjack, roulette, and Texas Hold'em all at once. Any major changes in these states' regulations, economy, or even weather patterns could hit UHS hard.

They're also heavily reliant on Medicare and Medicaid reimbursements. So if Uncle Sam decides to tighten the purse strings, UHS could feel the pinch.

Plus, they're required to treat emergency patients regardless of their ability to pay. A sudden influx of non-paying customers could put a dent in their profits faster than you can say "insurance claim denied."

But overall, the prognosis for UHS looks good. With their margin increases, strong earnings growth, positive stock momentum, and that juicy low valuation, they're poised to be the frontrunners of the global hospital services market.

In my decades of watching the markets, I've learned that sometimes the best opportunities come wrapped in hospital gowns rather than pinstripe suits. UHS might just be one of those opportunities.

I suggest you add it to your watchlist. And if the market hiccups and gives us a dip? Well, that might just be the perfect time to scoop some up for your portfolio.

Mad Hedge Biotech and Healthcare Letter

September 24, 2024

Fiat Lux

Featured Trade:

(KNOW WHEN TO HOLD ‘EM)

(LLY), (NVO), (VKTX)

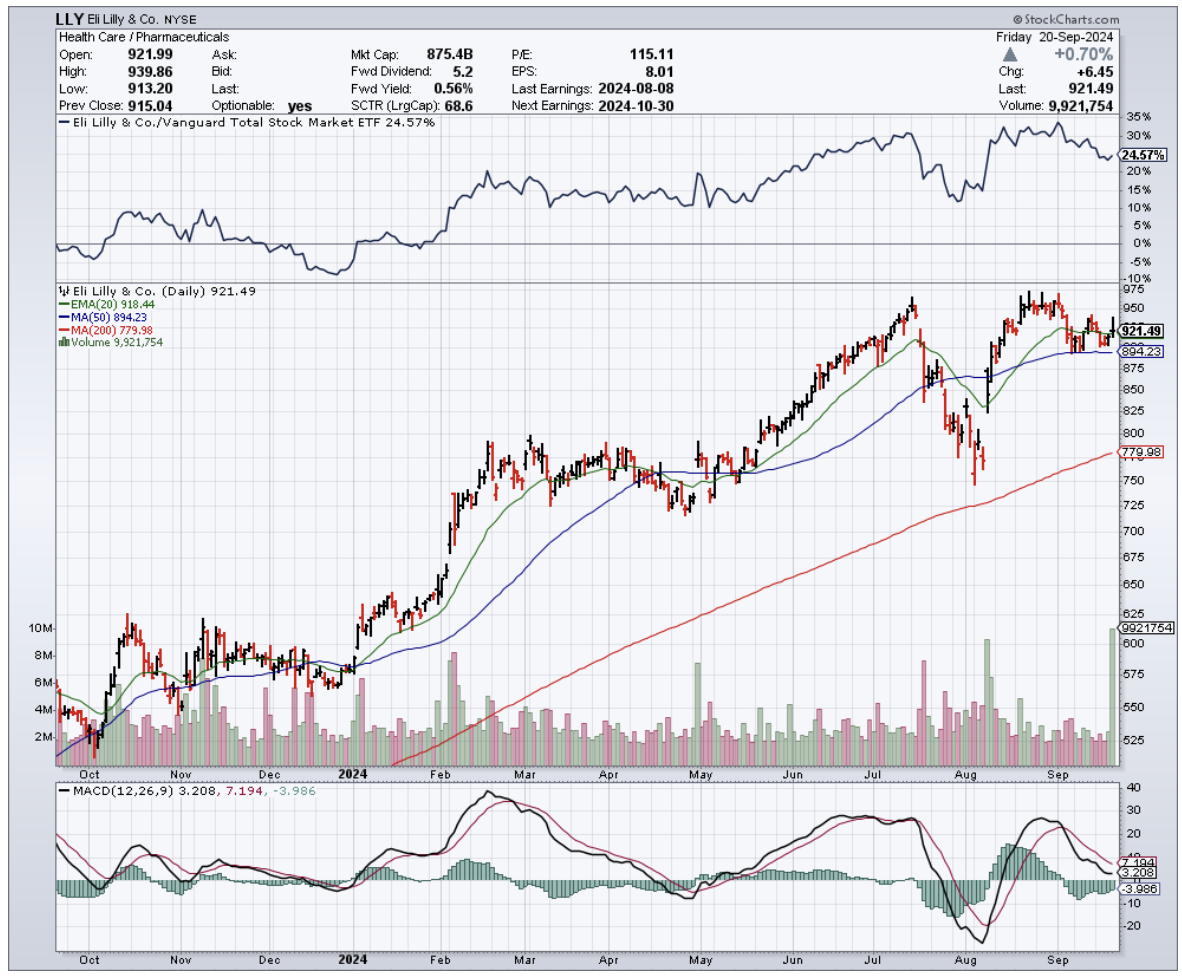

Ever stumble upon a treasure chest you almost walked past? That's how I feel about Eli Lilly (LLY) these days. When I last weighed in on LLY earlier this year, I was hesitant, pretty much like a seasoned sailor eyeing stormy seas.

The stock's valuations at the time were sky-high, especially when stacked against its arch-rival Novo Nordisk A/S (NVO). But the market, ever the trickster, loves to flip the script when you least expect it.

Since May, LLY has soared by an impressive 24.5%, leaving most of its pharmaceutical peers scrambling in its wake. Only Viking Therapeutics (VKTX) has managed to keep pace in this high-stakes race.

So, what's ignited this rocket?

For starters, Eli Lilly finally ironed out the kinks in its supply chain. By early August 2024, the shortages plaguing their weight-loss blockbuster, Mounjaro, were a thing of the past.

Those bottlenecks had put a damper on Mounjaro's performance in the first half of 2024, but now the gates have swung wide open.

But that's not all. LLY's got some serious production muscle coming online from the first half of 2025. This isn't just adding fuel to the fire — it's like pouring jet fuel on a bonfire.

That means we could see Mounjaro and Zepbound sales shooting for the moon in late 2024.

Now, here's the masterstroke. In January 2024, Eli Lilly launched LillyDirect, a direct-to-consumer platform that's nothing short of ingenious.

By slashing prices for self-pay patients on Zepbound, they're not just expanding their market reach—they're throwing a wrench into the burgeoning market for compounded GLP-1 drugs.

Let's crunch some numbers for more context.

A four-week supply of 2.5 mg Zepbound via LillyDirect costs $399 out of pocket. That's in the same ballpark as the $199 monthly fee charged by telehealth platforms like Hims & Hers Health (HIMS) for compounded GLP-1 injectables.

Contrast that with the eye-watering $1,790 monthly price tag for Novo Nordisk's Ozempic or the $1,990 for Wegovy, and it's clear why Lilly's strategy is turning heads and opening wallets.

All this momentum has Lilly's management grinning like the cat that ate the canary. They've bumped up their 2024 revenue guidance to a staggering $46 billion — a 34.8% year-over-year leap.

As for earnings, they're forecasting an adjusted EPS of $16.35, a jaw-dropping 158.7% increase from last year. Even a market veteran like me has to tip his hat.

Wall Street analysts are also joining the party, projecting Lilly's top and bottom lines to grow at a compound annual growth rate of 26.1% and 66.7%, respectively, through 2026.

Now, you might be scratching your head and thinking, "Isn't LLY overvalued at this point?"

Surprisingly, despite a forward P/E ratio of 55.39x — well above its historical averages — Lilly's forward PEG ratio sits at a comfortable 1.30x. That's lower than its 5-year mean of 2.19x and even the sector median of 2.00x.

In plain English, there's still some juice left in this orange for value investors.

But let's not get ahead of ourselves. Viking Therapeutics is hot on Lilly's heels with its VK2735 candidate, boasting impressive Phase 3 trial results.

Imagine 14.7% weight loss from baseline in just 13 weeks with their injectable version — that's actually warp speed compared to Lilly's current offerings.

And it's not just Viking sharpening their knives. The GLP-1 arena is set to become a battlefield, with up to 16 new drugs potentially launching by 2029.

So, where does that leave us? I'm cautiously upgrading Eli Lilly to a Buy, but I'm keeping my eyes wide open.

The market is frothy, perhaps a bit too exuberant for my taste. You might want to hold your horses and wait for a pullback into the $780–$845 range before jumping in.

Keep an eye on Lilly's balance sheet, too. Expansion at this scale doesn’t come cheap.

The company’s net debt has swelled to $25.53 billion, a hefty 59.6% increase from last year. Annualized interest expenses are creeping up as well, now at $734.4 million.

It’s not a five-alarm fire, but it’s smoke worth watching.

Eli Lilly has made bold moves in the GLP-1 market, positioning itself as a leader while others scramble to catch up. The question is, are you ready to take a seat at the table?

After all, in the words of the great Kenny Rogers, "You've got to know when to hold 'em, know when to fold 'em." And right now, LLY's hand is looking pretty strong.

Mad Hedge Biotech and Healthcare Letter

September 19, 2024

Fiat Lux

Featured Trade:

(THE KING’S SPEECH)

(ABT), (DXCM), (LLY), (NVO)

Warren Buffett once said, “Time is the friend of the wonderful company.” If that's true, Abbott Laboratories (ABT) must be Father Time's BFF because this centenarian healthcare heavyweight has been befriending our wallets for longer than most of us have been alive.

First things first: Abbott's not just any dividend stock. It's a bona fide Dividend King, having hiked its payout for over 50 consecutive years. But let's not get too misty-eyed about history.

What's got my attention is Abbott's current form. This isn't your typical sleepy pharma stock. Abbott's been flexing its muscles across multiple segments, showing growth that could very well be a worthy competition against any Silicon Valley startup.

In the first half of this year, Abbott saw positive growth in all but one segment. The laggard? Diagnostics, which took a hit as COVID-19 testing went the way of the dodo. But hey, you can't win 'em all, right?

Now, let's talk dividends. Abbott's currently yielding a respectable 1.9%, outpacing the S&P 500's measly 1.3%. With a payout ratio of 67%, there's still room for this dividend to grow.

But where's the real excitement? Two words: diabetes care.

Abbott's continuous glucose monitoring devices are hotter than a two-dollar pistol, driving 19% organic growth in the first two quarters. With diabetes becoming a bigger epidemic than we anticipated, this could be Abbott's golden goose.

Just look at the skyrocketing stocks of diabetes-focused companies like Eli Lilly (LLY) and Novo Nordisk (NVO). Different products, same lucrative market.

Abbott's FreeStyle Libre CGM system isn't just some gadget. It’s actually a genuine life-changer that's raking in $1.6 billion in quarterly sales and growing 20% year-over-year. In a market where DexCom (DXCM) is nipping at their heels, that's no small feat.

But Abbott's not resting on its laurels. They're expanding into over-the-counter CGM systems like Lingo and Libre Rio, leveraging a decade of international experience to capture more U.S. market share. It's like they're aiming to slap a diabetes monitor on every wrist in America.

And here's the kicker: the number of people living with diabetes is projected to hit 643 million by 2030 and a whopping 783 million by 2045. If that’s not the definition of a growing market, then I don’t know what is.

But Abbott isn't a one-trick pony. While they're busy trying to corner the diabetes market, they're also cooking up a storm in other areas.

Take their cardiac care lineup, for instance. Abbott's dabbling in electrophysiology with their EnSite X EP System, equipped with something called Omnipolar Technology. Sounds like something out of a sci-fi flick, right? Well, it's making cardiac mapping more precise than a Swiss watchmaker, giving arrhythmia patients a fighting chance.

But that’s not where it ends. Abbott's TriClip system is tackling tricuspid valve repair like a pro wrestler pinning an opponent. And don't get me started on their Esprit dissolvable stent. It's like the James Bond of the vascular world - it does its job and then disappears without a trace.

So, while diabetes care might be Abbott's current chart-topper right now, they've got a whole album of potential hits in the works. From glucose monitors to heart repair, Abbott's making moves that could have investors' portfolios beating as steadily as a healthy heart.

And as for you nervous nellies out there, Abbott's beta value of 0.7 suggests it's more stable than a three-legged stool. Perfect for those of you who break out in hives at the mere mention of volatility.

Now, it hasn't all been smooth sailing. Abbott recently faced a trial over claims its preterm infant formula caused a dangerous disease. But don't start panic-selling just yet.

JPMorgan and Barclays reckon the liability is likely to be smaller than a gnat's appetite. Abbott's management is confident, too, probably because the product in question accounts for a whopping... wait for it... $9 million in revenue. That's pocket change for a company like Abbott.

Looking ahead, Abbott's firing on all cylinders. They're seeing 9.3% organic revenue growth (excluding their COVID products), and they're so confident they've raised their full-year guidance.

Meanwhile, valuation-wise, Abbott's looking pretty good. With double-digit earnings growth expected and an AA-credit rating (better than some countries I could name), this stock could easily outperform the market.

So, what's the bottom line? Abbott's got the stability of a Dividend King, the growth potential of a tech startup, and more irons in the fire than a blacksmith's shop.

It's trading at a fair price, and with its track record of innovation and dividend growth, this could be your ticket to a healthier portfolio. After all, in the race for returns, slow and steady often wins more than just participation trophies. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

September 17, 2024

Fiat Lux

Featured Trade:

(A JAB WELL DONE OR A SHOT IN THE DARK)

(MRNA), (RHHBY), (NVS), (BMY)

Moderna (MRNA), the wunderkind of the COVID vaccine era, is facing a bit of a hangover. Remember when this biotech darling was riding high on vaccine sales? Well, those days are looking as distant as your last booster shot.

The company's stock had a decent first half, climbing about 20%. They even scored a win with their new RSV vaccine approval. But hold your horses, because things are getting a bit dicey.

Last month, Moderna had to revise its COVID vaccine revenue downward. Translation: people aren't lining up for jabs like they used to.

And just last week? They dropped another bombshell: Moderna's planning to slash its annual R&D spending by over $1 billion starting in 2027. On top of that, they're also pulling the plug on five programs.

But wait, there's more. Remember when Moderna was supposed to break even in 2026? Well, now they're saying it'll be 2028. That's like telling your date you'll be there in 5 minutes, then showing up two hours later.

Now, let's talk numbers. The consensus for 2025 sales was sitting pretty at $3.9 billion. Moderna's new projection? A potential downside of $2.5 billion, with a best-case scenario of $3.5 billion. As for 2024, they're looking at $3 to $3.5 billion.

And here's another head-scratcher: Despite 800,000 people over 65 in the U.S. being hospitalized last season, only 41% of this population has the COVID vaccine. Compare that to 74% with the flu vaccine. It looks like people trust the old-school flu shot more than the new kid on the block.

So, what's Moderna's game plan? They're focusing on delivering 10 products over the next three years. That's down from their previous bold claim of 15 new products in five years.

Here’s what CEO Stéphane Bancel has to say about this: "The size of our late-stage pipeline combined with the challenge of launching products means we must now focus on delivering these 10 products to patients, slow down the pace of new R&D investment, and build our commercial business."

In other words, they bit off more than they could chew and now they're trying to swallow.

Moderna's slashing its R&D investment for 2025 through 2028 by 20%, down to $16 billion. That's a $4 billion haircut.

But here's the twist - they're actually increasing investment in oncology, presumably to hopefully build a portfolio that could rival the likes of Roche (RHHBY), Novartis (NVS), and Bristol Myers Squibb (BMY).

Now, before you start thinking it's all doom and gloom, let's look at the silver lining.

Moderna expects its respiratory vaccines to be profitable this year and beyond. They're also aiming to file for approval of three new products by year-end: a next-gen COVID vaccine, a combo flu/COVID vaccine, and an RSV vaccine for younger high-risk adults.

Now, is Moderna a buy or a sell? Well, that really depends on your investment style.

Moderna's in a tight spot, but it's not game over. They're trimming the fat, focusing on what works, and betting big on oncology.

Plus, they actually have the cash to see this strategy through. So, they won't need to pass around the collection plate to reach their break-even goal. Their current situation is admittedly not pretty, but it's not a death spiral either.

For most of us, this is where the rubber meets the road. If you're up on Moderna, consider taking some profits, but don't bail completely. This could be a classic "buy the dip" opportunity for the bold.

Remembert, biotech is boom or bust, and Moderna's loaded pipeline needs just one hit to soar. Their combo vaccines could be game-changers if they pan out. And let's not forget, they cracked the mRNA code - that's not small potatoes in the world of drug development.

Bottom line: If you're risk-averse, look elsewhere. But for those with iron stomachs and long-term vision, this might be your chance to snag a potential biotech giant on sale.

Mad Hedge Biotech and Healthcare Letter

September 12, 2024

Fiat Lux

Featured Trade:

(A SURPRISE UPPERCUT)

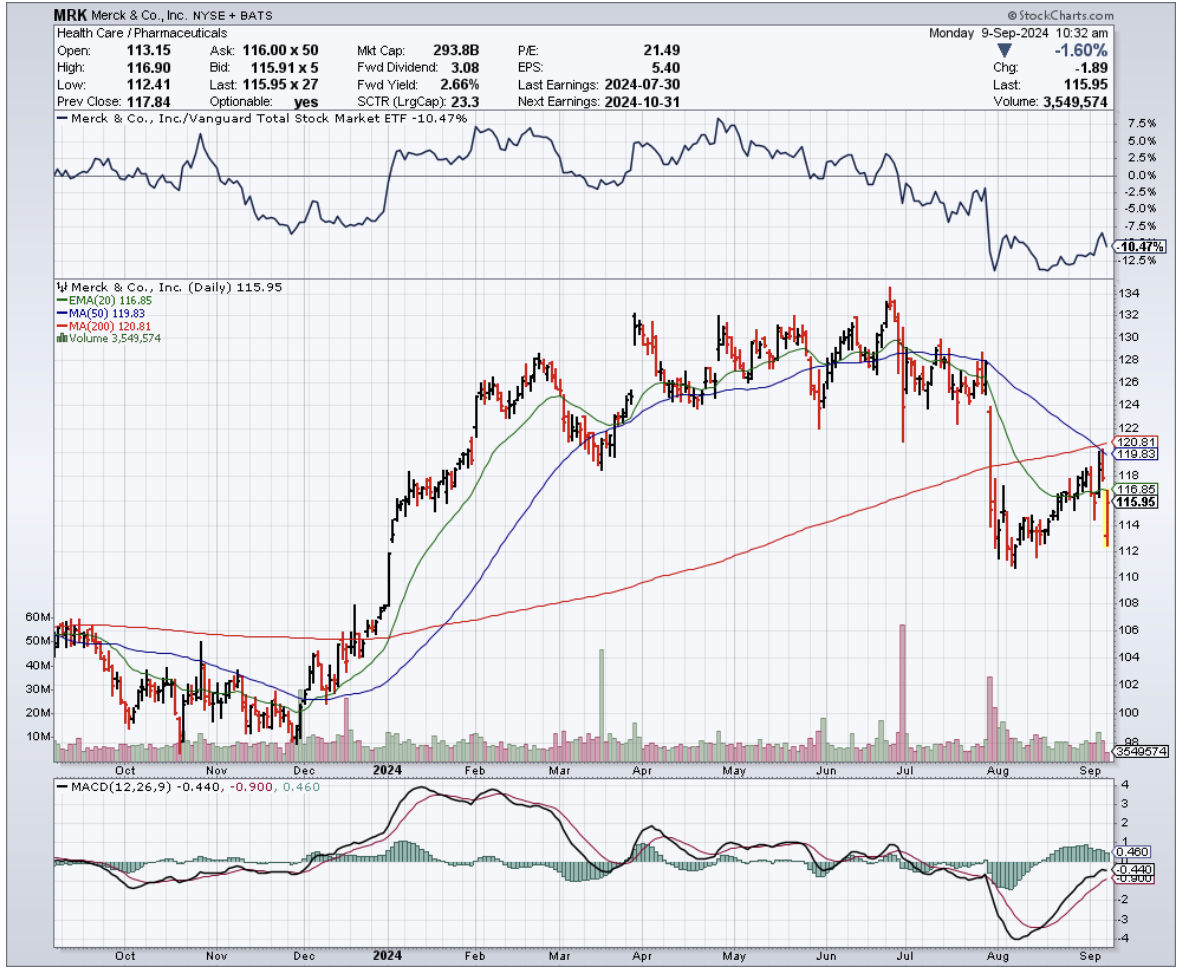

(MRK), (SMMT)

Remember when Muhammad Ali got knocked down by Joe Frazier? Well, Merck (MRK) just had its Ali moment, courtesy of a plucky little biotech named Summit Therapeutics (SMMT).

Ivonescimab, a cancer drug developed by this relatively under-the-radar biotech company, just gave Merck's golden goose, Keytruda, a serious run for its money—and not by a small margin.

In a recent announcement, Summit Therapeutics revealed that Ivonescimab reduced the risk of disease progression or death by a whopping 49% compared to Keytruda. Let that sink in for a moment

In the trial, aptly named HARMONi-2 (these folks love their capitalization), Ivonescimab held tumor progression at bay for a median of 11.1 months. Keytruda? A mere 5.8 months.

Needless to say, Summit just landed a haymaker that has Merck seeing stars.

Now, before you rush to dump your Merck stock faster than a hot potato, let's put this in perspective. The trial was conducted in China with Summit's collaboration partner, Akeso. It's a significant result, no doubt, but we're not talking FDA approval just yet.

Still, Wall Street took notice. Summit's stock shot up 61% in Monday's premarket while Merck's stock took a hit.

But here's where it gets interesting. Merck's been the undisputed heavyweight champ of pharma for years, with Keytruda as its championship belt. This wonder drug has been laying billion-dollar eggs for nearly a decade, and the nest keeps growing.

In 2022, the Keytruda market was valued at $20.8 billion, and by 2023, it raked in a staggering $25.01 billion.

With AbbVie’s (ABBV) Humira out of the running, projections for 2024 now peg Keytruda as the top-ranked drug worldwide, with sales expected to surpass $27 billion.

By 2032, it's expected to soar to $45.9 billion, with a compound annual growth rate (CAGR) of 9.20% from 2024 to 2032.

Just last quarter, Keytruda accounted for a whopping 45% of Merck’s $16.1 billion revenue—that’s $7.3 billion from a single drug. Talk about putting all your eggs in one basket.

And therein lies the rub. Keytruda's patent expires in 2028. That's not tomorrow, but in the pharma world, it's just around the corner.

It's like watching the countdown timer on a bomb in an action movie - you know it's coming, but you can't look away.

Merck's not blind to this. They've been diversifying as fast as they could.

Their next largest product, Gardasil, brought in $2.5 billion last quarter, growing at a modest 4%. Not Keytruda numbers, but nothing to sneeze at.

They're also betting big on new drugs. There's Winrevair, a treatment for pulmonary arterial hypertension that could bring in up to $11 billion by 2029.

Then there's Capvaxive, a pneumococcal vaccine that could hit $1 billion in sales by 2027. And let's not forget their $5.5 billion deal with Daiichi Sankyo for three antibody-drug conjugates.

So, what's the play here? Merck's trading at 15 times next year's earnings. That's like finding a designer suit at a thrift store price.

The stock's up 5.3% this year, lagging behind the S&P 500's 16% growth. Some might see a bargain, others a warning sign.

Here's my take: Merck's got challenges, no doubt. But they've also got a track record of success and a pipeline that could make a pharmacist drool.

If you've got the patience of Job and the stomach for biotech's wild rides, Merck could be a solid long-term play.

But don't take your eyes off Summit Therapeutics. They’ve just proved they can punch above their weight class.

Besides, in this high-stakes arena of biotech, where one breakthrough can knock the competition to the mat, it’s the unexpected contenders that often deliver the biggest surprises. So, keep your eyes on the ring—the next round promises to be a thriller.