Mad Hedge Biotech and Healthcare Letter

August 22, 2024

Fiat Lux

Featured Trade:

(BITING OFF MORE THAN THEY CAN CHEW)

(LLY), (NVO), (CTLT), (ZLDPF), (RHHBY), (AMGN), (PFE), (LZAGY), (TMO)

Mad Hedge Biotech and Healthcare Letter

August 22, 2024

Fiat Lux

Featured Trade:

(BITING OFF MORE THAN THEY CAN CHEW)

(LLY), (NVO), (CTLT), (ZLDPF), (RHHBY), (AMGN), (PFE), (LZAGY), (TMO)

"If you build it, they will come." But what happens when they come before you've finished building?

That's the billion-dollar question facing the makers of GLP-1 weight loss drugs.

GLP-1 drugs, the newest darlings of the pharmaceutical world, are selling like hotcakes. Eli Lilly (LLY) and Novo Nordisk (NVO), the current heavyweights in this arena, raked in a whopping $10.4 billion and $6.85 billion respectively last year.

Basically, the demand is there, but the supply? Well, that's another story.

So far, Lilly and Novo have been throwing money at the problem like it's going out of style. We're talking billions here. Novo's earmarked $6.5 billion for production this year alone, while Lilly's already shelled out $5.3 billion to beef up its manufacturing muscle. They're expanding facilities faster than you can say "miracle weight loss drug."

But even that's not enough. Lilly admits the industry needs at least 10 to 15 dedicated sites to even come close to meeting demand.

It's like trying to serve a five-course meal to a packed restaurant with just one chef and a microwave.

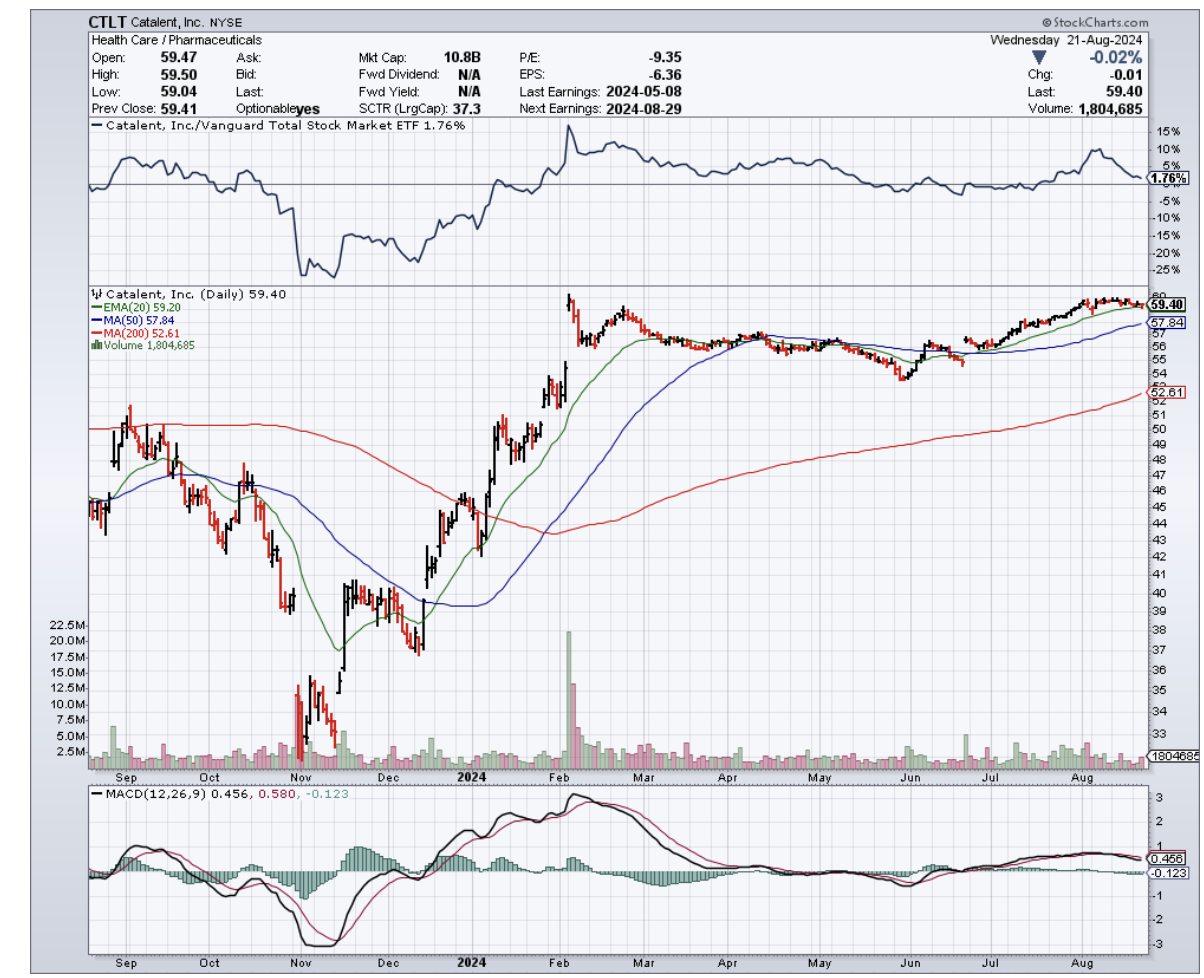

And let's not forget about the price tag on these manufacturing sites. Novo just dropped $11 billion to buy three fill-finish sites from Catalent (CTLT). Talk about paying a premium for prime real estate.

While Lilly and Novo scramble to ramp up production, their manufacturing woes have created a window of opportunity for competitors eyeing a slice of the GLP-1 pie.

Boehringer Ingelheim and Zealand Pharma (ZLDPF) are closest to market with their Phase 3 drug survodutide.

Meanwhile, Roche (RHHBY) and Amgen (AMGN) aren't far behind in Phase 2. Even Pfizer's (PFE) dipping its toes in the water with an early-stage drug.

But here's where it gets interesting for us who want a piece of the action. These newcomers are facing a manufacturing dilemma of their own.

Do they build their own facilities and risk being late to the party? Or do they outsource and potentially lose control over production?

Some, like Boehringer and Roche, are already talking about using third-party manufacturers. It's like hiring a catering company instead of building your own restaurant – less upfront cost, but you're at the mercy of someone else's kitchen.

Enter the contract manufacturing organizations (CMOs), the unsung heroes of the pharmaceutical world who might just hold the key to unlocking the full potential of the GLP-1 market.

Let’s take a look at the big players in this space.

Lonza Group (LZAGY), with its $6.6 billion in annual revenue and 10% market share in biologics contract manufacturing, is a force to be reckoned with. They're not just sitting on their laurels either – they're pumping $850 million into a new biologics facility in Switzerland.

Then there's Thermo Fisher Scientific (TMO), the 800-pound gorilla of the industry. With a cool $44.9 billion in revenue last year and an 8% to 10% market share in contract manufacturing, they're a go-to partner for big pharma.

They've been on a shopping spree too, scooping up Pharmaceutical Product Development (PPD) for $17.4 billion to boost their manufacturing capabilities.

And, of course, let's not forget about Catalent. They might have sold some facilities to Novo, but they're still a major player with $4.8 billion in revenue last year. They're betting big on biologics, with plans to increase capacity by 40% by 2025.

As for those looking for growth potential, keep an eye on Samsung Biologics. They're the new kid on the block, with a 30% compound annual growth rate over the past five years and the world's largest single-site biologics manufacturing facility.

So, there you have it. The obesity epidemic is a tragedy, but it's also a trillion-dollar opportunity.

With half the population projected to be obese by 2030, this isn't just a health crisis—it's a financial frontier.

The GLP-1 market is poised to balloon to $130 billion, creating a feeding frenzy for those ready to capitalize on the supply squeeze.

But here's the real meat of the matter: in this gold rush, it's not just the drug developers who are striking it rich. The real winners are the manufacturers—those with the capacity to meet the insatiable demand. They're the ones handing out the "shovels" in this weight loss bonanza.

So while everyone else is focused on the flashy GLP-1 drugs, I suggest you also keep a watchful eye on these behind-the-scenes players.

Now, if you'll excuse me, I'm off to patent my groundbreaking idea: GLP-1-infused kale chips. Who says you can't have your cake and eat it too?

Mad Hedge Biotech and Healthcare Letter

August 20, 2024

Fiat Lux

Featured Trade:

(POX POPULI)

(BVNRY), (EBS), (GOVX), (SIGA), (CMRX), (TNXP), (TMO), (ABT), (MRNA), (PFE)

Hold onto your hazmat suits because the world of infectious diseases just got a lot more interesting. And if you're someone with a stomach for volatility, you might want to pay attention.

Mpox is back, and it's brought a nasty new cousin to the party. The World Health Organization (WHO) just hit the big red button, declaring the mpox outbreak a public health emergency of international concern (PHEIC). That's fancy talk for "this is serious, people."

Let's break it down. We're not dealing with your garden-variety mpox here. This is a new strain, dubbed Clade Ib, and it's tearing through central Africa like a bull in a china shop.

The Democratic Republic of Congo (DRC) has seen over 15,600 cases so far this year, more than all of last year. And it's not staying put.

Kenya, Burundi, Rwanda, and Uganda are all reporting their first-ever mpox cases. It's like watching a virus go on a world tour, minus the t-shirts and overpriced concessions.

Now, before you start panic-buying toilet paper again, the Centers for Disease Control and Prevention (CDC) says the risk to the U.S. is very low.

But they're still telling healthcare providers to keep their eyes peeled for any funky rashes on patients who've been globe-trotting lately.

So, what do we do with this information? Well, let's talk vaccines.

Bavarian Nordic (BVNRY), the company behind the most widely used mpox vaccine, has seen its stock jump more than 30% since the WHO's announcement. It's like they won the pharmaceutical lottery.

And Uncle Sam's not shy about showing them some love – the U.S. Department of Health and Human Services just placed a $156.8 million order for a bulk vaccine product.

But they're not the only player in town.

Emergent Biosolutions (EBS), another vaccine manufacturer, also saw its stock surge when the news broke.

Even GeoVax Labs (GOVX) saw its stock shoot up 40% yesterday morning. Not bad for a company most people had never heard of last week. They're working on an MVA vaccine – that's Modified Vaccinia Ankara for you science nerds out there. It's the go-to choice for folks with weakened immune systems.

But it's not all sunshine and rainbows in vaccine land.

Siga Technologies (SIGA) released some disappointing trial data for their antiviral drug TPOXX. Turns out, it's not much better than a sugar pill for treating mpox.

Other companies are also jockeying for position.

Chimerix (CMRX) is developing brincidofovir, an antiviral that could potentially treat mpox. Tonix Pharmaceuticals (TNXP) is working on TNX-801, a live-virus vaccine candidate.

And let's not forget the diagnostic giants like Thermo Fisher Scientific (TMO) and Abbott Laboratories (ABT). After all, in the world of infectious diseases, being able to spot the bad guy quickly is half the battle.

Even the big guns of the COVID-19 vaccine world, Moderna (MRNA) and Pfizer (PFE), might decide to flex their mRNA muscles in the mpox arena. And with their track record, who's going to bet against them?

But here's the million-dollar question: Is this a golden opportunity for investors, or a potential minefield? The answer, as always in the stock market, is "it depends."

On one hand, companies directly involved in mpox vaccines, treatments, and diagnostics could see their stocks soar if the outbreak worsens.

On the other hand, the biotech sector is about as stable as a jenga tower in an earthquake. Today's miracle drug could be tomorrow's cautionary tale.

The smart money isn't putting all its eggs in the mpox basket. Diversification is still the name of the game. Remember, this outbreak could fizzle out as quickly as it started, leaving one-trick ponies high and dry.

Plus, let's always keep in mind the wild card in all this: government contracts.

In the world of infectious diseases, Uncle Sam often holds the purse strings. Keep your ear to the ground for any whispers of government funding or contracts. That kind of news can send stocks into the stratosphere faster than you can say "public health emergency."

So, what's the bottom line? The mpox outbreak is creating some intriguing opportunities in the biotech sector. But as with any investment, don't let the fear of missing out cloud your judgment.

And remember, in the stock market, as in epidemiology, it's all about managing risk.

In the meantime, maybe skip that bushmeat sandwich on your next African safari. Just a thought.

Mad Hedge Biotech and Healthcare Letter

August 15, 2024

Fiat Lux

Featured Trade:

(THE INCREDIBLE BULK)

(LLY), (NVO), (RHHBY), (AMGN), (PFE), (VKTX)

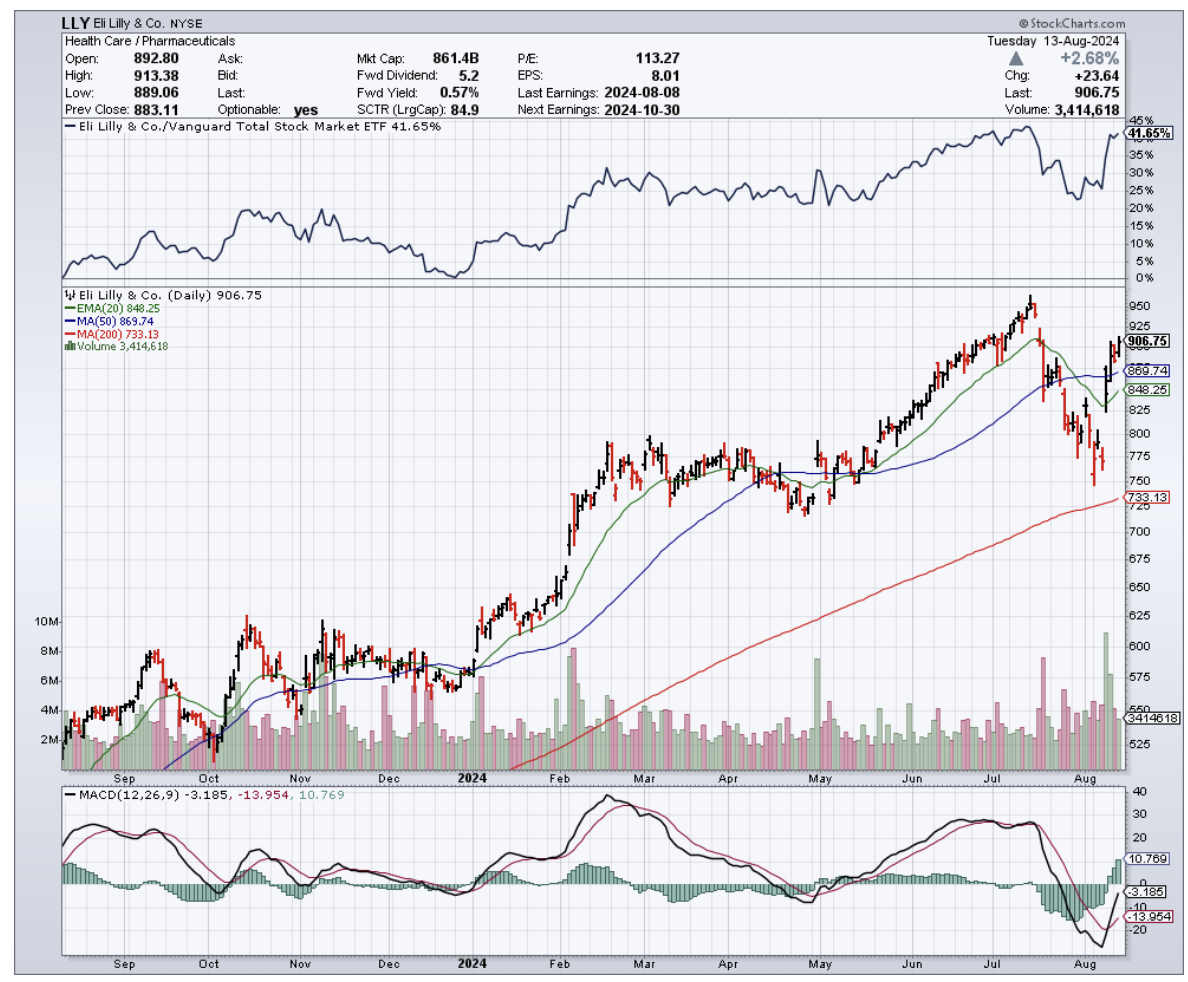

Well, slap me silly and call me a contrarian. A few years back, when Eli Lilly's (LLY) market cap was under $500 billion, everyone thought it was just another faceless pharma giant on the Street.

But holy molecule, Batman! Today, Lilly isn't just knocking on the door of the trillion-dollar club—it's about to blow it off its hinges. Let's dive into Lilly's Q2 2024 earnings, shall we?

Revenue? Up 36% year-on-year to $11.3 billion. Operating income? Nearly doubled to $3.72 billion. Net income? $2.97 billion, up 86%. EPS? $3.28 on a GAAP basis, or $3.92 if you like your numbers massaged.

Now, I've seen more bubbles pop than a kid with a roll of bubble wrap, but this isn't froth - this is rocket fuel.

Lilly's guidance for 2024 is now $45.4 billion - $46.6 billion in revenue. That's $3 billion more than they were projecting a few months ago. Talk about sandbagging.

No wonder Lilly's share price has shot up 18% in the past few days.

Next, let's take a look at what’s driving this growth: tirzepatide, which is marketed as Mounjaro for diabetes and Zepbound for obesity.

In Q2, Mounjaro raked in $3.1 billion, up from $1.8 billion in Q1. Zepbound, which only hit the market in November, brought in $1.24 billion, more than doubling its Q1 performance.

Combined, that's $4.34 billion in a single quarter from one molecule. To put that in perspective, that's more than some entire countries' GDPs.

But Lilly isn't a one-trick pony. Let's take a quick tour of their other divisions.

Oncology grew to $2.16 billion, up from $1.67 billion last year, largely thanks to breast cancer therapy Verzenio.

This drug could hit $5 billion in sales this year, putting it firmly in blockbuster territory. Not bad for a drug that doesn't even cure baldness.

Immunology saw Taltz and Olumiant bring in $825 million and $228 million, respectively.

With mirikizumab finally approved last October and lebrikizumab likely to overcome its manufacturing hiccups, this division could double in size by decade's end.

It's like watching a caterpillar turn into a butterfly, if butterflies were worth billions of dollars.

Even neuroscience, which saw a dip to $339.5 million from $387.2 million last year, has a potential game-changer up its sleeve.

Donanemab, now approved as Kisunla for Alzheimer's, could bring in $5 billion annually.

Add in remternetug, another Alzheimer's therapy in the pipeline, and we could be looking at a $10 billion per year business by 2030.

That's a lot of people remembering where they left their keys.

Now, I know what you're thinking. "So, what’s the catch?" Well, you're not wrong to be skeptical. This is pharma, after all, and things can go south faster than a New Yorker fleeing to Florida for tax reasons.

The main risk? Competition. Every pharma company worth its salt is working on GLP-1 agonists.

Novo Nordisk (NVO) is already in the game with semaglutide (Wegovy and Ozempic), and others like Roche (RHHBY), Amgen (AMGN), and Pfizer (PFE) are nipping at Lilly's heels.

There's also the possibility of long-term side effects we haven't seen yet, or the risk that the healthcare system buckles under the weight of demand for these pricey drugs.

After all, we're talking about drugs that cost more per year than a decent used car.

But here's the thing: Lilly has a massive head start. They're not just leading the race – they're lapping the competition.

And they're not resting on their laurels either.

They've got orforglipron, an oral GLP-1 agonist, in Phase 3 trials. Then there's retatrutide, nicknamed "triple-G," which has shown even more impressive weight loss results than tirzepatide.

So, where does this leave us? Well, I expect Lilly to become the first trillion-dollar pharma company. Yes, you read that right. A trillion dollars.

Is their valuation justified? Based on current numbers, probably not.

But we're not betting on current numbers, we're betting on the future. And let me tell you, Lilly's future is dazzling.

Remember, just a few years ago, a $20 billion-a-year drug was considered the pinnacle of pharma success.

Tirzepatide could blow past that mark before the decade's out. And that's just one drug in Lilly's impressive arsenal.

Of course, there's always the risk that another company could swoop in with an even better GLP-1 agonist. My money's on Roche, Pfizer, or Viking (VKTX) if anyone's going to pull it off.

For now, though, Lilly's the thoroughbred in this race, and I wouldn't bet against them unless I suddenly developed a burning desire to live in a cardboard box.

That being said, predicting where this wild market is heading? That's like trying to catch lightning in a bottle while blindfolded and riding a unicycle.

But in the case of Lilly, I think even a blind squirrel could see this nut coming.

So, strap in because it’s going to be one hell of a ride, and this particular acorn might just grow into the mightiest oak on Wall Street. You wouldn’t want to miss out on the shade it'll provide in the years to come.

Mad Hedge Biotech and Healthcare Letter

August 13, 2024

Fiat Lux

Featured Trade:

(THE RISE OF THE STEADY EDDIES)

(CNC), (UNH), (PFE), (JNJ), (ABBV), (LLY), (BIO), (UHS), (WAT), (AMGN), (REGN), (VRTX), (CRSP), (MRNA)

Think of the market as a body fighting off an infection. Tech stocks might be the flashy antibodies, but healthcare is the steady, reliable immune system, keeping things stable when the going gets tough. And right now, that immune system is looking stronger than ever.

Skeptical? I get it. We've heard the hype about healthcare before. But this time, it's different.

The Healthcare Select Sector SPDR ETF (XLV) has been on a tear, up 9.3% this year as of Thursday's close. That's nearly keeping pace with the broader S&P 500's 12% gain - a remarkable feat in a market that's been anything but stable.

But what's even more impressive is the turnaround. Back in mid-July, XLV was lagging behind like a three-legged horse in the Kentucky Derby, up only 8.3% while the S&P 500 was showing off with an 18% gain.

In fact, out of the 63 healthcare stocks in the S&P 500, only a dozen have been slacking off since July. The rest? They've been outperforming like it's going out of style.

So what changed?

Well, it wasn't so much that healthcare stocks suddenly discovered the fountain of youth. No, my friends, it was more like the rest of the market decided to take a swan dive off the high board.

You see, while tech stocks were busy doing their best Icarus impression – flying too close to the sun and then plummeting back to earth – healthcare stocks were steady as she goes. It's like the old tortoise and hare story, except in this version, the hare got distracted by shiny objects and ran off a cliff.

Now, let's shine the spotlight on some of the key players driving this healthcare rally.

Remember those health insurers everyone was worried about back in spring? The ones that had investors biting their nails over the future of Medicare Advantage? Well, they've made a comeback.

The S&P 500 Managed Health Care index was down 12% in mid-April, looking about as healthy as a chain smoker with a Big Mac habit. But now? It's up 4.5% since the start of the year.

Companies like Centene (CNC) and UnitedHealth Group (UNH) have bounced back faster than a rubber band on steroids.

And it's not just the insurers. Big Pharma's been flexing, too.

Pfizer (PFE), the company that became a household name faster than you can say "vaccine," is holding steady. Johnson & Johnson (JNJ) is up 2.2%, probably thanks to all that baby powder they're not selling anymore.

Meanwhile, AbbVie’s (ABBV) up 11% since July. These guys are like the Energizer Bunny of the pharma world – they just keep going and going.

But the real showstopper? Eli Lilly (LLY). This biopharma has been on a tear since the beginning of 2024. Up 45% on the year at one point, they've been climbing faster than a squirrel up a tree with a dog in hot pursuit.

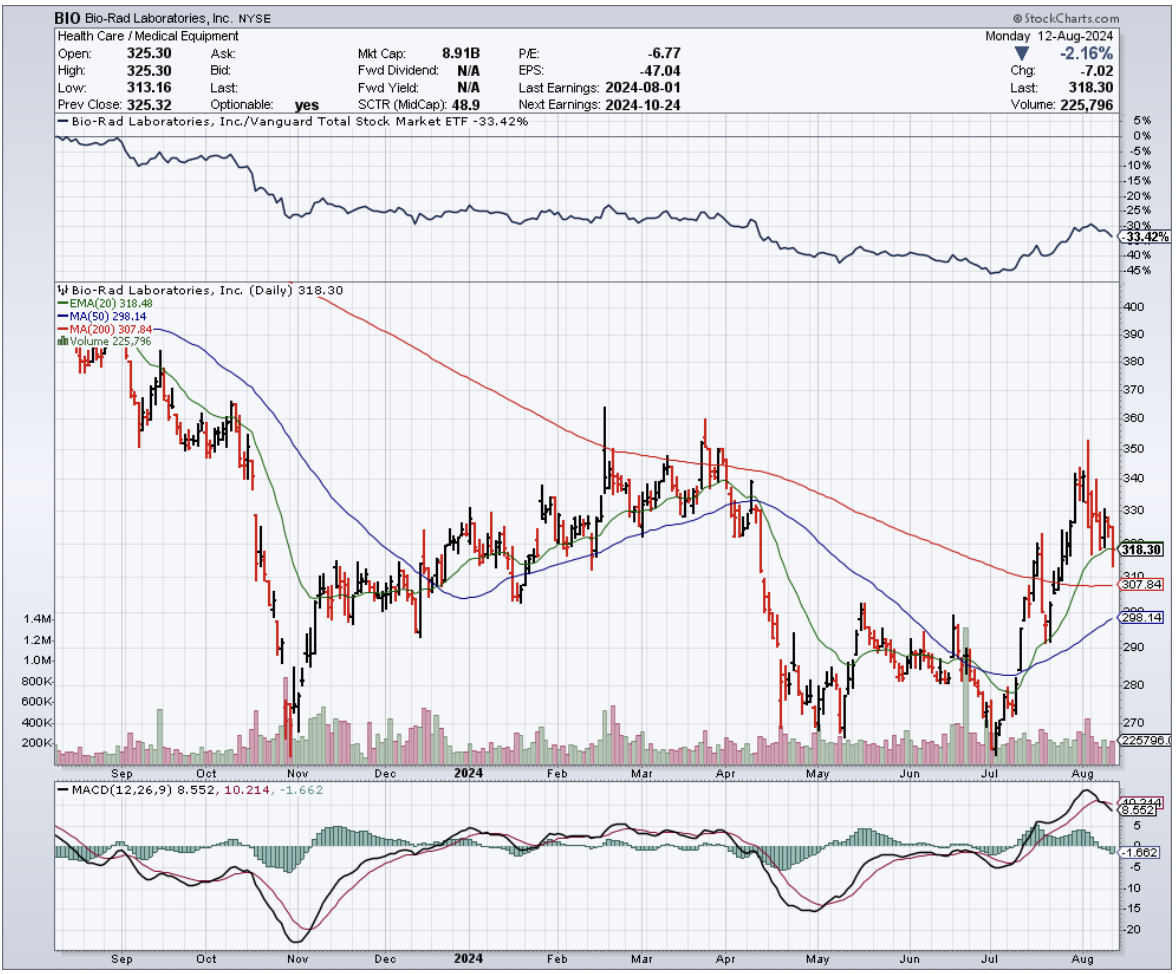

Then, there are companies like Bio-Rad Laboratories (BIO), up 20% since July. Universal Health Services (UHS)? Up 18% since July. Waters (WAT), the life sciences tools folks? Up 15%.

Even the biotechs are out to impress.

Amgen (AMGN), the granddaddy of biotech, is up 10% year-to-date. They're selling drugs like Prolia and Enbrel faster than hotcakes at a lumberjack convention.

And Amgen’s pipeline? It’s packed with potential blockbusters, setting the stage for further expansion in the future.

Gilead Sciences (GILD)? Up 15% year-to-date. Turns out, their COVID-19 treatment, Remdesivir, is back in vogue like bell-bottom jeans. And their HIV and hepatitis C drugs? They're still growing stronger.

But the real rock star of biotech? That'd be Regeneron Pharmaceuticals (REGN). These guys are up over 30% year-to-date. They're treating everything from eye diseases to cancer to inflammation.

Vertex Pharmaceuticals (VRTX) is another one to watch. Up 12% this year, they've got the cystic fibrosis market cornered. And they're not stopping there – they're expanding faster thanks to their collaboration with the likes of Crispr Therapeutics (CRSP).

Now that I’ve mentioned gene therapy, I know you're wondering about Moderna (MRNA). After all, weren’t they the darlings of the COVID era? Well, yes and no.

Their stock's down about 35% year-to-date, but don't count them out just yet. Their mRNA technology is hotter than a jalapeño popper fresh out of the fryer. They might be down, but they're definitely not out.

So, what's the takeaway here? I suggest you keep your eyes peeled on the biotechnology and healthcare sectors. After all, in this market, the best offense might just be a good defense – and what's more defensive than betting on the sector that keeps us all alive and kicking?

Mad Hedge Biotech and Healthcare Letter

August 8, 2024

Fiat Lux

Featured Trade:

(WHEN A+ PROFITS MEET C-VALUATION)

(AMGN), (ABBV), (GILD)

It's time we talk about Amgen (AMGN), that biotech giant that's been acting more like a sleepy bear than the roaring lion it once was.

Don't get me wrong. I've got a soft spot for Amgen. Having personally witnessed the struggles of cancer survivors who sampled their wares, I can tell you their stuff works. It's like rocket fuel for your immune system.

But as an investor? Well, that's where things get messy.

Amgen's definitely no slouch. It's the 5th largest component of the Dow Jones Industrial Average.

For us dinosaurs who still think the Dow matters (guilty as charged), that's like being the biggest, baddest T-Rex in Jurassic Park. But we all know how that movie ended, don't we?

In the S&P 500 jungle, Amgen's the 40th largest beast and the 9th largest in the healthcare sector. Impressive, sure, but so was the Titanic before it met that iceberg.

Amgen’s work in therapeutics, from Epogen and Aranesp boosting red blood cell counts to Neupogen and Neulasta enhancing immune systems, makes it indispensable in the healthcare sector.

Still, I have to dig deeper. Amgen’s profitability is stellar, boasting an A+ grade, which checks a significant box in my evaluation criteria.

However, the valuation, growth, and momentum reveal a picture that’s less rosy. Amgen isn’t the growth powerhouse it once was compared to its sector peers like AbbVie (ABBV) and Gilead Sciences (GILD), and its valuation is teetering on the edge of extravagant. The price has surged, rendering it "overvalued."

Even when considering its price-to-sales ratio—a favorite metric of mine—Amgen is near its 10-year peak at 6x sales.

That's not just expensive – it's "I'll have what they're having" territory. Sure, lots of big stocks are trading at nosebleed levels, especially in tech. But just because everyone's jumping off the valuation cliff doesn't mean we should join the lemming parade.

Now, everyone knows I’m a dividend junkie. I like my yields high and my risks low. It's a bit like my approach to mountain climbing—I want the view, but I'd rather not plummet to my doom getting there.

At first glance, Amgen looks tempting. The dividend is safe, consistent, and growing. But context is key.

The healthcare sector, using the XLV ETF as a proxy, yields only 1.5%. Amgen's 2.66% yield beats that handily, but it's toward the low end of its 7-year range.

To make it worthwhile as a long-term holding, Amgen would need to offer a yield in the 3.2%-3.5% range and demonstrate a clear bottoming pattern in its stock price. We're not there yet, folks.

Next, let’s talk charts. Looking at its stock price, if this were an EKG, we'd be calling a code blue.

Amgen’s chart shows a stock struggling to breach its trendline, with two potential target zones below the current price that it might hit.

While anything is possible in investing, I see those lower price areas as more likely than Amgen soaring 15% to fresh highs.

Could Amgen surprise us all and rocket up 15%? Sure, and I could win "Dancing with the Stars." Anything's possible, but I wouldn't bet my last dollar on either.

But here’s the kicker—Amgen's not alone in this boat. The whole market seems to have decided to party like it's 1999, forgetting that what goes up must come down. When it does, it'll be faster than my descent from 90,000 feet in that MiG.

Still, I'm not saying Amgen's destined for the biotech graveyard. At this point, it's not a "never buy," but a "not at this price."

I like to think of it as a hibernating bear. When that yield creeps up and the price comes down, it might be time to poke it with a stick.

If it stretches and growls with renewed vigor, you’ll want to be ready to jump in. Until then, let’s enjoy the show from a safe distance.