The Largest Shadow Banker and U.S. Tech

In the top-heavy global media landscape, there seems to be this notion that the U.S. and its capital is the primary alpha male swaying asset prices.

The close to $6 trillion in recent stimulus chasing too few services demonstrably has an outsized vote on the matter of asset pricing.

But the dirty little secret about this stimulus is that U.S. private equity is spilling into Nordic and Western European markets effectively forcing a rapid Americanization of asset prices across the Atlantic.

Shadow banks finance financial transactions that are too risky for banks.

In the US, they already grant half of all loans.

In times of low or even negative interest rates for credit, fewer and fewer investors bring their money to a normal bank, but rather to a so-called shadow bank.

This is a term that has become established to describe a phenomenon for financial participants who are not a bank.

What a shadow bank is is not exactly defined, because there are no shadow banking licenses; but tech companies and the U.S. wielding of this critical function have changed the financial world.

In some cases, a few large private families who now have the means to invest in such funds are also focused on funding through these shadow banks and most of the time to buy American tech stocks.

And they deliberately invest not just in a single fund, but across all countries in the world, and shadow banks make up around a third of the financial sector.

In Germany, it is more than a third and on the EU average, it is almost exactly a third.

Pension funds and pension funds work like small insurance companies: employees of a company pay part of their gross wages directly, free of tax and social security contributions. At the end of their working life, they will then be paid a supplementary pension from the income generated.

The fact that “their” money is mandated to be invested in the global financial markets - at least if people hope to receive a pension after their active working life.

These European pension funds are also turning to U.S. branded shadow banking.

According to the Financial Stability Board, shadow banks had a total of $80 trillion in business in 2021.

Compared to the previous year, this was an increase of 8.5%. The FSB information is based on data from 29 countries. These in turn represent 80% of global economic output.

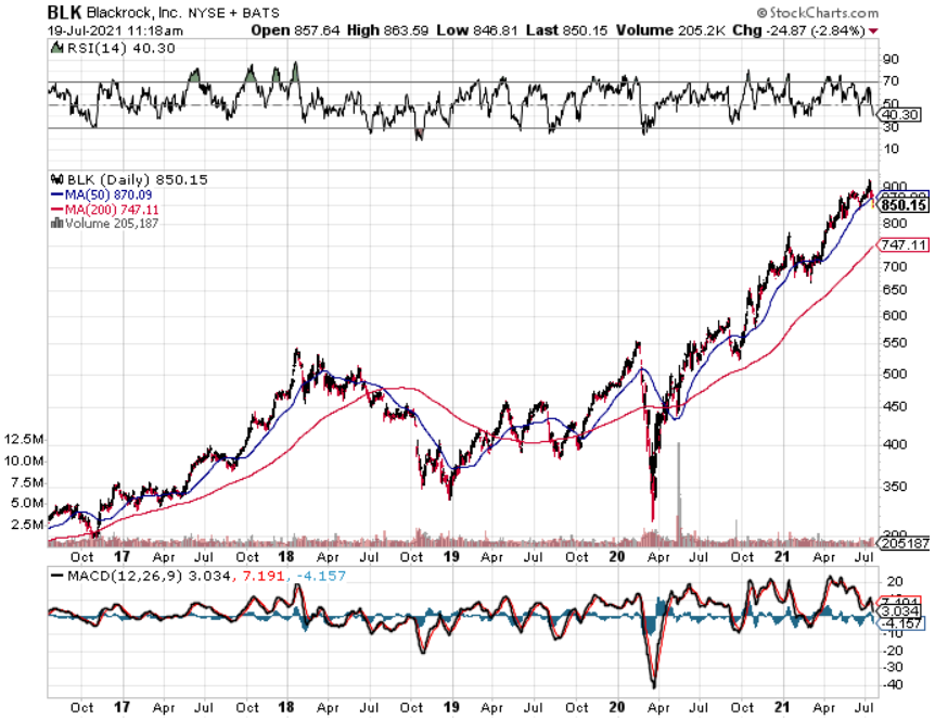

Many deals and transactions are outsourced from the banks now. That means: The financial business tries to circumvent the regulations and the largest shadow bank is BlackRock (BLK) - involved in 20,000 companies.

Many of these outsourced financial service providers are also nothing more than subsidiaries of BlackRock.

This outsourcing offers their customers the prospect of significantly higher interest rates.

BlackRock is an influential major shareholder in all listed global corporations from Europe and the USA.

Although it was founded in 1988, BlackRock was unknown to most people in Germany for decades.

That only changed in 2018, when the politician and lobbyist Friedrich Merz announced his candidacy for the CDU party chairmanship.

At this point in time, Friedrich Merz had been head of the supervisory board of the German offshoot of BlackRock for two years.

This is a company that currently manages a fortune of over nine trillion dollars which is far more than what is produced in Germany, every year, in terms of goods and services - considerably more.

At BlackRock, they harness the smorgasbord of mechanisms that define this new area of shadow banking: hedge funds, VC, real estate, index funds, and money market funds.

BlackRock holds considerable blocks of shares through various subsidiaries, including in normal commercial banks - such as Bank of America, Citigroup, and Deutsche Bank.

But that’s not all.

BlackRock is by far the largest owner in the German share index - with a share of 15 to 17%.

That means: every sixth share of the 30 largest German corporations is controlled by one of the BlackRock funds.

That BlackRock's ownership structure rotates in circles. The asset management companies control themselves, or are actually not subject to any control.

It’s an almost incestuous system where you pursue your own interests through a network of participation. While banks are systemically relevant, BlackRock is still uncontrolled, and they refuse to classify this company as systemically relevant.

But that is BlackRock and that is part of what made them highly successful.

It is extremely well connected. It has long-standing, important politicians in its ranks. Friedrich Merz is just one example in the big picture.

French President Emmanuel Macron recently said he wanted to see the creation of at least 10 tech companies in Europe worth over 100 billion euros each by 2030.

While Europe is now home to many unicorns — start-ups valued at over $1 billion — it is yet to produce a company with the scale of American and Chinese tech giants.

But I am ready to argue that Europeans no longer have control over their own narrative in their own financial system, it is now U.S. private equity.

Assuming that this holds true, even if President Macron’s wish bears fruit, the owners of these “European” tech companies will of course be Americans who are dressed up as European pension funds and maybe even perhaps somehow a company starting with a B and ending with ROCK?

The oversupply of capital from the U.S. that has overcharged U.S. tech shares will get any piece of the action that Europe creates if they are to create a tech renaissance, which I highly doubt.

And the real truth is that any unicorn created in Europe will most likely go public in New York anyway.

The pandemic has also supercharged the influence of Blackrock in Germany and Europe as a whole and that cannot be diminished.

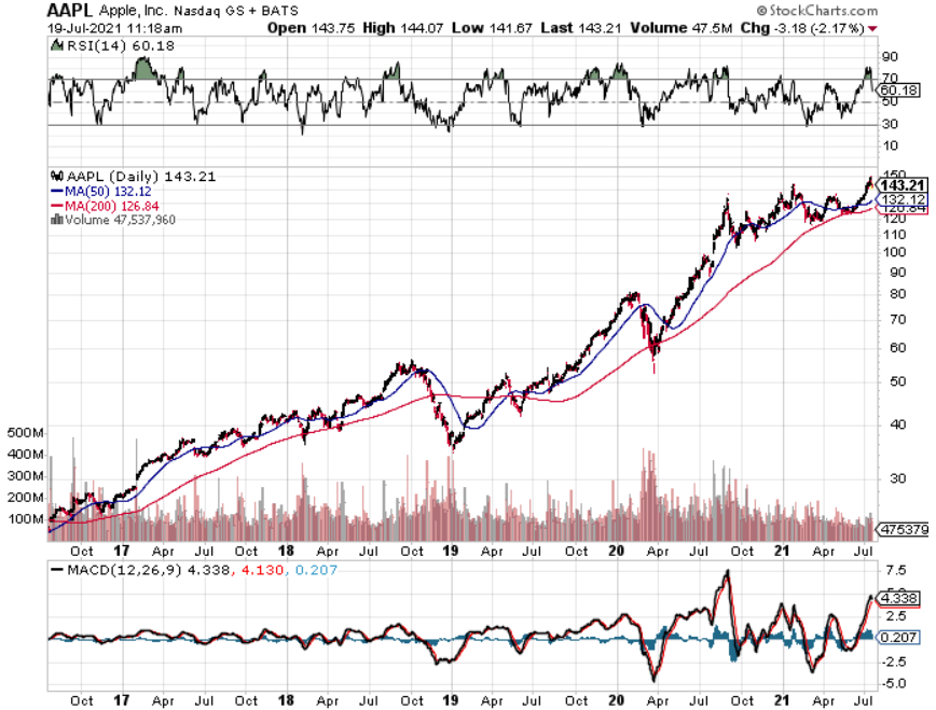

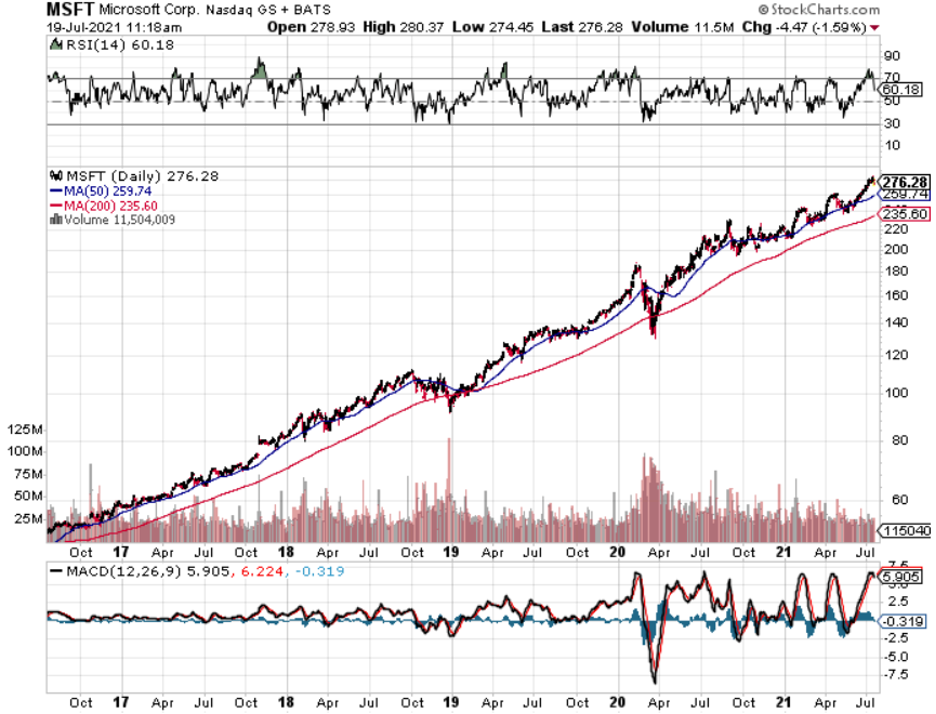

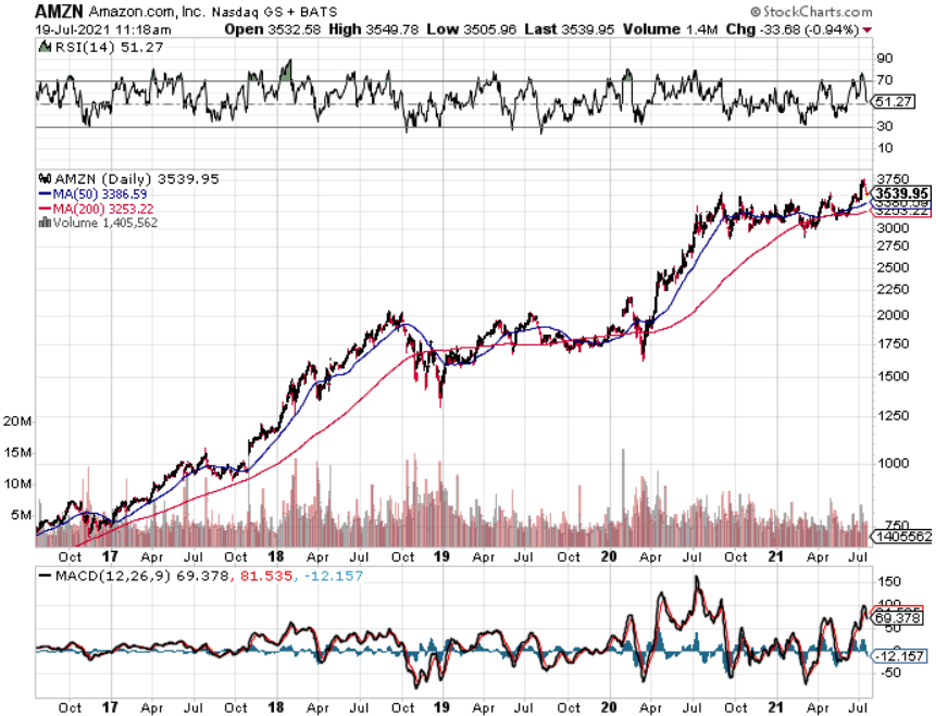

According to Blackrock’s 13F, 10% of their portfolio is Apple (AAPL), Microsoft (MSFT), and Amazon (AMZN) - holding $128 billion in AAPL, $123 billion in MSFT, and only $87 billion in AMZN.

Their largest 7 holdings are in U.S. tech stocks.

This is just a 13F in their main fund, and it wouldn’t be shocking to find out some of their European subsidiaries are also doing the same thing even if not with the same amount of capital.

The European financial system has effectively been gamed by Blackrock and its copycats, so next time you hear of a large Nordic or German equity fund making a big splash in U.S. tech shares, the eventual originator of that decision could be Blackrock.

This is the type of sophistication we are dealing with at this point in global markets and essentially nothing beats the eye test anymore because we have no idea what is happening unless we follow the trail of money.