Buy The Tourist Platform Tech Stock

Any type of selloff in Airbnb (ABNB) shares will be short-lived as we approach the summer Olympics and European soccer summer tournament.

Global Events of a month-long will get people out of their homes and spending their cash.

These premium events will move the needle for Airbnb revenue-wise in Europe.

The heart of world travel is Western Europe so it’s convenient that these mega-events are in France and Germany and not in some backwater.

Better luck next time if you haven’t locked up your Airbnb in Germany or France by now.

Travelers even have the option to stay through September and enjoy the annual Oktoberfest in Bavaria.

There isn’t lodging to be found in Western Europe in the summer months and even though the economy is starting to weaken around the edges, we are still in for another summer of travel post-pandemic style.

Tourists are splurging like there is no tomorrow held up by the higher income bracket.

Italy is famous for hosting 8 million Americans per year and is otherwise known as Americans' favorite European destination.

That number is poised to balloon to 12 million by 2030 and that means revenue growth for Airbnb as Italian Airbnb’s are rampant everywhere you go in Italy.

As for the company, the business model has been doing great ever since CEO and Founder Brian Chesky put a tight leash on expenses after being caught wrongfooted during the pandemic.

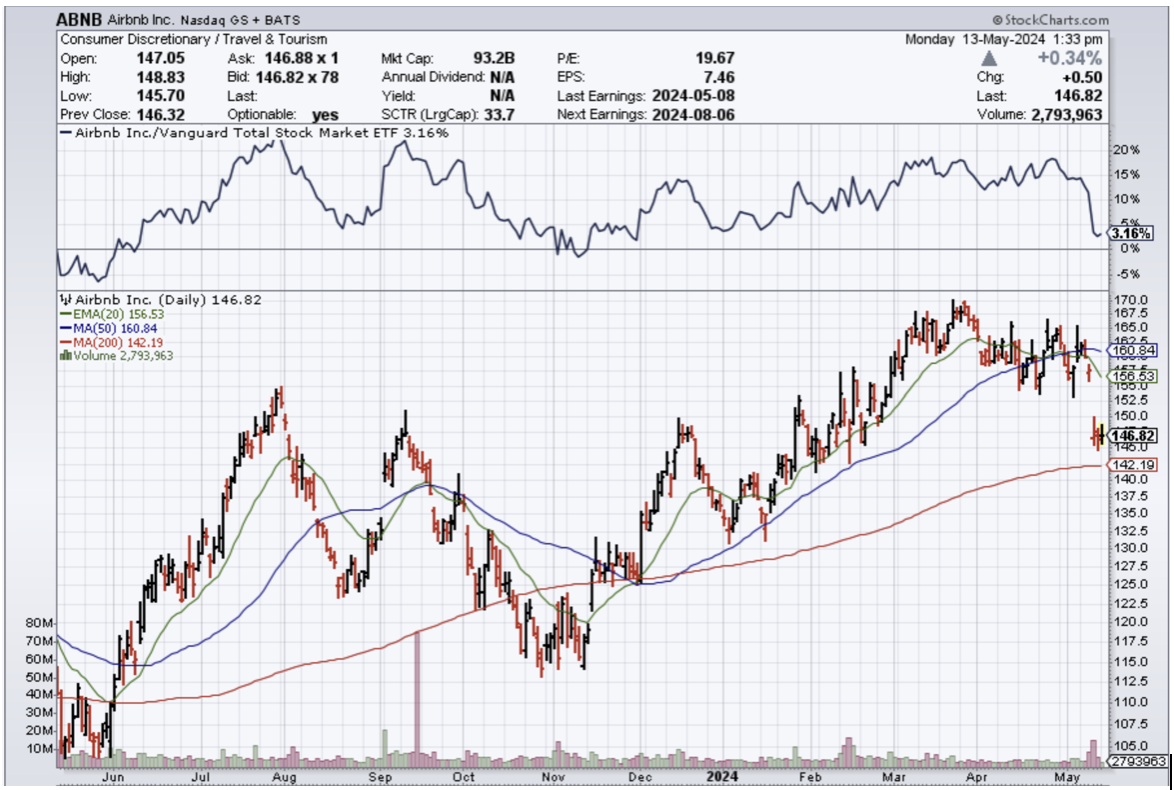

The stock sold off on the earnings even with the nice beat and the Mad Hedge tech letter executed a call spread on the underlying shares.

Weak guidance has been a hallmark of this past earnings season as the economy softens.

Management needs a lower bar to jump over for later this year.

Revenue increased 18% year over year to $2.14 billion last quarter, ahead of the $2.06 billion consensus.

The surge in profit margins was due in part to a shift in the Easter holiday to the first quarter, strong interest income, and leverage from its revenue growth and cost discipline.

The stock is now down 13% from its year-to-date peak and at its lowest point in close to three months.

Airbnb competes with hotels and other types of overnight accommodations, but its closest competitors are other home-sharing platforms like Expedia's VRBO.

But Airbnb already dominates the home-sharing niche with a leading market share among those platforms, and the company appeared to strengthen its position in the first quarter. Revenue at Expedia (EXPE) increased 8% in the period, while its B2C division which includes VRBO was up just 3%.

Competitors have been unable to overcome the powerful network effect present on Airbnb's platform, allowing it to continue growing its lead.

The shareholder returns program is beefing up.

The company continues to return capital to shareholders, buying back $750 million in stock last quarter. With $2.5 billion in total share repurchases over the past year,

Airbnb has reduced its shares outstanding by nearly 3% over that period. While 3% might not sound like much, this strategy compounds over time, and Airbnb should be able to increase buybacks as profits grow.

Additionally, the company is benefiting from higher interest rates as it's on track to generate close to $1 billion in interest income this year, giving it a significant boost on the bottom line.

I’m betting on an uptick in shareholder interest in the short term at these price levels.

I was a little uncomfortable chasing it higher from $170, but $150 is more reasonable and I do believe the Fed pivot tailwinds could catapult us into profits with this trade.