Mad Hedge Biotech and Healthcare Letter

May 1, 2025

Fiat Lux

Featured Trade:

(TELEHEALTH'S NEW WEIGHT CLASS)

(HIMS), (NVO)

Mad Hedge Biotech and Healthcare Letter

May 1, 2025

Fiat Lux

Featured Trade:

(TELEHEALTH'S NEW WEIGHT CLASS)

(HIMS), (NVO)

Clinging to Mount Everest at 20,000 feet, fingers numb and oxygen tank hissing like an annoyed cobra, I had an epiphany that would later serve me well on Wall Street: the most promising paths aren't always the obvious ones — they're the routes that quietly keep you alive while everyone else is busy with their cameras and guided tours.

That same principle is quietly guiding Hims & Hers Health (HIMS) right now.

While the market obsesses over their new Wegovy partnership with Novo Nordisk (NVO), sending HIMS stock jumping 25% to $35, savvy investors should look deeper.

The company isn't suddenly becoming a weight-loss play — they're eliminating doubt and positioning themselves at the center of healthcare's digital transformation.

This reminds me of a pattern I've observed across decades of tracking successful businesses and leaders. The most effective ones don't chase trends. Instead, they position themselves to win regardless of which way the wind blows.

I witnessed this firsthand during a memorable interview with Deng Xiaoping back in the late 70s. Despite the chaotic economic landscape he inherited, his focus remained steadfastly on fundamentals rather than fleeting opportunities.

That's precisely the Hims playbook with these GLP-1 partnerships.

Fascinatingly, they're charging $599 monthly for Wegovy — $100 more than Novo's direct offering.

In my decades managing hedge fund portfolios, I've learned that pricing power is the ultimate business aphrodisiac. It signals you have something people genuinely value enough to pay a premium for.

Wall Street, in its infinite wisdom, is once again squinting at the wrong spreadsheet.

Hims projects $2.35 billion in 2025 revenue, with $725 million from weight management alone — a forecast that completely excluded branded GLP-1s. Their core business in sexual health, dermatology, and mental wellness already generates $1.2 billion annually.

That's 83% of revenue from decidedly non-injectable sources!

Their growth figures are impressive, too: 60% projected sales growth and 70% adjusted EBITDA growth. Yet HIMS trades at just 3.5x 2025 revenue estimates.

If I pitched you a company growing this fast in any other sector at that multiple, you'd think I was selling oceanfront property in Nebraska.

But what truly separates Hims from competitors is retention. Their internal data shows 70% patient retention after 12 weeks, compared to 42% in standard clinical settings. Their users interact with providers three times more frequently in the first month and five times more over three months.

That's not marginally better — it's an entirely different universe of care.

Like those guerrilla fighters I once interviewed in Southeast Asia, who held territory against superior forces by knowing the terrain better — Hims isn’t just in the healthcare war, they know exactly where to strike.

The stock previously touched $70 after posting 95% year-over-year growth in Q4. It retreated on fears about GLP-1 access that were largely imaginary.

Now it's climbing again on news that merely confirms what company executives already knew: their business model doesn't hinge on any single medication.

This situation reminds me of trading Japanese equities in the late '80s—watching rational people make irrational decisions based on incomplete information. The market is simultaneously overvaluing the importance of GLP-1s while undervaluing Hims' overall growth trajectory.

With $300 million in projected 2025 adjusted EBITDA (13% margins), expanding to 20% as they scale, HIMS at 27x EBITDA represents the kind of opportunity that makes me sit up straighter in my ergonomic chair. That multiple would make perfect sense for a company growing at half this rate.

What's more telling than spreadsheets, though, is customer loyalty. During my years managing portfolios worth more than some small nations' GDPs, I developed a simple litmus test: if a company disappeared tomorrow, would its customers feel inconvenienced or devastated?

Hims has clearly crossed into "devastated" territory for its growing user base - the kind of emotional moat that Warren Buffett probably dreams about between bites of his McDonald's breakfast.

For those hunting increasingly endangered species - growth with reasonable valuation, momentum with sustainable model, actual substance beneath the hype - HIMS offers a compelling specimen. These GLP-1 deals aren't the main story; they're just the latest chapter in a much longer narrative about healthcare's digital transformation.

And if there’s one thing I’ve learned from diving shipwrecks in Truk Lagoon to decoding market trends from Tokyo to New York — it’s that the journey tells you more than any single milestone ever could.

This one looks increasingly profitable for those with the patience to stay the course.

Mad Hedge Biotech and Healthcare Letter

April 29, 2025

Fiat Lux

Featured Trade:

(BIOTECH’S AWKWARD MIDDLE CHILD)

(GILD), (VRTX), (AMGN), (BMY)

Well, folks, I've been trading biotech stocks since before most of today's analysts had their first internships.

After countless dinners with pharma execs and more investor conferences than I care to remember, there's one thing I've learned about this sector – these stocks are a lot like the experimental drugs themselves: sometimes miraculous, sometimes disappointing, and always requiring patience.

That brings us to Gilead Sciences (GILD), which has recently pulled off the financial equivalent of finding a $100 bill in an old jacket: a 90% gain since May 2024.

If you're an income-focused investor eyeing GILD's promising yield like a prospector spotting gold, I'd suggest taking a breath before you stake your claim.

After diving into this company's financial innards with the ruthless precision of a veteran hedge fund manager, I've uncovered some fascinating contradictions.

First off, GILD has undergone a remarkable transformation, shedding its growth-focused biotech skin to become what I call a "mature dividend machine" – offering 9 consecutive years of dividend increases since 2015.

Its current annual dividend of $3.16 per share yields 2.99%, significantly outpacing the biotechnology sector average of 1.92%. Not too bad for a company that cut its teeth on groundbreaking HIV and COVID treatments.

But here's where things get interesting. Despite GILD's revenue looking as seasonal as a summer blockbuster (with predictably lower earnings in the first half of each year), the company's fundamentals show troubling signs beneath the surface.

While Q1 2025 revenue was expected to land around $6.77 billion, the company's economic profitability has fallen off a cliff since 2024. Blame it on negative net income in early 2024 and a Cash Tax Rate that jumped from 25.4% to 30.6% faster than a trader fleeing a market crash.

The historical performance tells an even more sobering tale. From IPO to 2015, GILD delivered average annual returns of 32.25% in 79% of years – performance that would make even the most jaded investor whistle.

But since 2015? The stock managed profits in only 50% of years with an anemic average return of 0.99%, which translates to a 2.17% loss when adjusted for inflation. Ouch.

You might say that the entire sector's going through a rough patch these days, and I would have agreed with you except there are several biotechs still performing well.

Take Vertex Pharmaceuticals (VRTX). Those guys are up 36.7% over the past 52 weeks.

Or consider Amgen (AMGN), whose dividend is growing at a mouth-watering 8.94% annually over five years – nearly triple what GILD is serving up to its shareholders.

Even BioMarin (BMRN), a company most retail investors couldn't pick out of a lineup, has been quietly crushing it with 27.3% revenue growth while GILD's top line moves sideways like a crab with performance anxiety.

And don't get me started on Bristol Myers Squibb (BMY). Despite facing their own patent cliff dramas, they're maintaining a forward P/E of just 7.2 – practically giving away shares – while offering a dividend yield of 4.7%.

So, let me tell you something the glossy investor presentations won't: GILD's forward P/E ratio of 13.35x looks attractively cheap compared to the healthcare sector's 20.13x and the S&P 500's 18.60x.

After having had drinks with several institutional investment managers last week, though, I can assure you that discount exists for a reason.

The smart money has correctly identified that this company is no longer growing profitably, and certain whispers about their pipeline aren't inspiring confidence.

For dividend investors hoping to beat inflation while preserving capital, GILD presents a mixed bag. The dividend growth continues but remains stubbornly below inflation, creating a slow leak in real returns.

And, look, I know the Trump White House isn't exactly making life easy for companies like Gilead. Over whiskey last month with a former FDA bigwig (who shall remain nameless), I heard some concerning murmurs about potential cuts to HIV prevention programs.

Bad news when you're sitting on 40% of the U.S. PrEP market like GILD is.

Bottom line? I'm sticking with "hold" for now. The smart money moves when the smart money knows, and my Rolodex isn't flashing buy signals yet.

I've watched enough biotech darlings flame out to know that patience outperforms panic every time.

When GILD shows signs of recapturing that pre-2014 magic, you'll hear it from me before the CNBC talking heads catch wind of it.

Mad Hedge Biotech and Healthcare Letter

April 24, 2025

Fiat Lux

Featured Trade:

(DIVIDEND HUNTING IN BEAR COUNTRY)

(BMY)

One stock in the pharmaceutical sector has been calling to me lately like a siren song amid market turbulence.

I'm talking about Bristol-Myers Squibb Co. (BMY), which has taken a beating in the March-April selloff but is dangling a forward estimated 5% dividend yield while generating a whopping 14% annual free cash flow — tops among the largest drug names.

I've been watching this one since January, when it first dipped below $52. Like a patient fisherman, I've been waiting for just the right moment to cast my line. That moment appears to be now, as BMY slides toward the $50 mark amid broader market jitters and sector rotation. It’s remarkable how often Wall Street throws the proverbial baby out with the bathwater during these periodic fits of selling.

The beauty of BMY is not just valuation. It’s historically proven itself as a financial bomb shelter — outperforming the S&P 500 in four major recessions since 1990.

During the 2020 pandemic, it returned 36% vs. the S&P’s 26%. In the Great Recession, it gained 13% while the broader market fell 16%.

During the 1990 Persian Gulf War recession, it delivered a jaw-dropping 76%.

And here’s one more kicker: BMY’s current 14% free cash flow yield is nearly 10% higher than equivalent cash investment yields — among the best “relative yields” it’s posted in 35 years.

On top of that, its 5%+ dividend towers over the S&P’s 1.3% and Big Pharma’s 3.65% median.

This is a rare setup where both the cash yield and the ability to sustain it align — a combination that’s very hard to beat in a defensive play.

Of course, no stock is bulletproof. BMY will need to navigate patent cliffs and increased regulatory scrutiny on drug pricing.

Wall Street is also pricing in little to no growth in the near term — and that’s probably fair. But the current setup suggests BMY could still outperform, especially if the S&P enters a decline in 2025.

This defensive mindset is why Warren Buffett and other veterans have been moving to abnormally extreme levels of cash since 2024. They're battening down the hatches while the financial seas are still relatively calm.

And speaking of smart investors, I had lunch last week at Tadich Grill with a hedge fund manager I’ve known for decades. When I mentioned I was looking for defensive plays, he immediately brought up BMY.

“What’s rare these days,” he said, “is a company with both a high dividend and the cash flow to actually back it up.” He then showed me his firm’s spreadsheets — stress-tested across recession scenarios back to Nixon — and BMY held firm.

Having run similar models myself (if not quite as colour-coded), I nodded in agreement.

At the current ~$50 share price, BMY’s free cash flow yield stands near 14%. That’s nearly 10% better than risk-free Treasury rates and more than double the Big Pharma peer group median of 6.15%.

So what could go wrong? A steeper summer selloff. Or an aggressive federal move to mandate drug pricing — a risk that’s always on the table, but rarely moves quickly. Supply chain issues, especially for ingredients sourced from China, are also worth watching.

That said, BMY has manufacturing facilities globally, and 71% of its revenue comes from the US. That gives it some insulation if trade tensions flare.

But here’s the thing: those risks hit all major pharma companies. BMY starts from a stronger base: better cash flow, better history, better defensive positioning.

My view? BMY is worth owning for its super-sized dividend and battle-tested resilience. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 22, 2025

Fiat Lux

Featured Trade:

(NO MORE TEARS)

(JNJ)

Remember when your mom told you to eat your vegetables? "They're boring but good for you," she'd insist while you eyed that chocolate cake across the room.

Well, in today's market, Johnson & Johnson (JNJ) is that plate of nutritious broccoli – not the sexiest option on the table, but exactly what your financial diet needs.

And if Q1 earnings are any indication, this particular vegetable is secretly packed with more flavor than the market gave it credit for.

Their recent earnings report confirms what I've been telling anyone who would listen: this pharmaceutical tortoise is quietly outpacing flashier hares.

Sales increased 2.4% year-over-year to $21.9 billion, exceeding analyst expectations and demonstrating that steady growth doesn't need to make headlines to fill portfolios.

While the headline diluted EPS was an eye-popping $4.54 (up over 235%), those savvy enough will look at the adjusted figure of $2.77 (excluding one-time charges) for a more realistic picture of operational performance.

Diving deeper into the numbers reveals a company firing on multiple cylinders.

The MedTech division grew 4.1% to $8 billion, with cardiovascular products leading the charge at 17.7% growth.

Meanwhile, Pharmaceuticals grew 4.2% to $13.87 billion, with oncology growing an impressive 20% to $5.68 billion.

Multiple myeloma therapy Darzalex continues its blockbuster trajectory at $3.24 billion, while the approval of Rybrevant in non-small-cell lung cancer adds yet another potential multi-billion dollar earner to the medicine cabinet.

Now, let's talk about pharmaceutical patent cliffs.

Stelara, JNJ's immunology golden goose, is mid-plummet, with Q1 revenues down 33% to $1.63 billion. As expected, though, JNJ has been quietly lining up replacements.

Their immunology bullpen includes nipocalimab (sporting FDA Fast Track status) and icotrokinra (which cleared skin in 84% of adolescent psoriasis patients).

You can actually practically smell the confidence wafting from management's quarterly statements.

They've bumped their full-year revenue guidance to $91.6-$92.4 billion and hiked the quarterly dividend by 4.8% to $1.30 per share. That makes 63 consecutive years of dividend increases.

I'd be remiss not to mention the twin storm clouds hovering over our healthcare heavyweight.

First, there's the $6.97 billion charge for talc lawsuits after a bankruptcy judge essentially told JNJ their "Texas two-step" legal maneuver was more of a stumble.

Second, the Trump administration's threatened 25% pharmaceutical tariffs. With roughly 44% of Q1 revenues coming from overseas ($9.6 billion compared to $12.3 billion domestic), JNJ isn't completely sheltered from cross-border economic squabbles.

But here's where JNJ's strategic thinking earns my respect: they're doubling down on America with a $55 billion U.S. expansion planned over the next four years.

Back when I was launching hedge funds in the late '80s, I quickly learned to separate companies that merely react to policy changes from those that anticipate and adapt. JNJ falls firmly in the latter category.

For the number-crunchers among you (my people!), JNJ trades at 25.6 times earnings with a price-to-free-cash-flow ratio of 19.95. I ran this through my DCF model using a 10% discount rate.

The math suggests JNJ needs approximately 5% annual free cash flow growth to justify today's price.

With MedTech projected to grow 5-7% annually and Pharmaceuticals showing similar potential, plus those steady share buybacks reducing the float at 1.14% yearly, my spreadsheets spit out an intrinsic value of about $168.39 per share – roughly 7% above where we stand today.

Not a screaming bargain, but a fair price for a company that's mastered the art of sustainable growth.

JNJ won't make you the star of your next cocktail party investment brag-fest. But when markets start convulsing like they've touched a live wire, these steady healthcare veterans tend to keep their vital signs stable.

While your trendier holdings might need intensive care during volatility, JNJ has spent over a century perfecting the art of financial first aid.

In a market that often leaves investors reaching for tissues, JNJ's steady performance lives up to its most famous promise: no more tears.

Mad Hedge Biotech and Healthcare Letter

April 17, 2025

Fiat Lux

Featured Trade:

(THIS BIG PHARMA'S GRAND DIVORCE SHOWS PROMISE)

(NVS), (SDZNY), (MRK), (RHHBY)

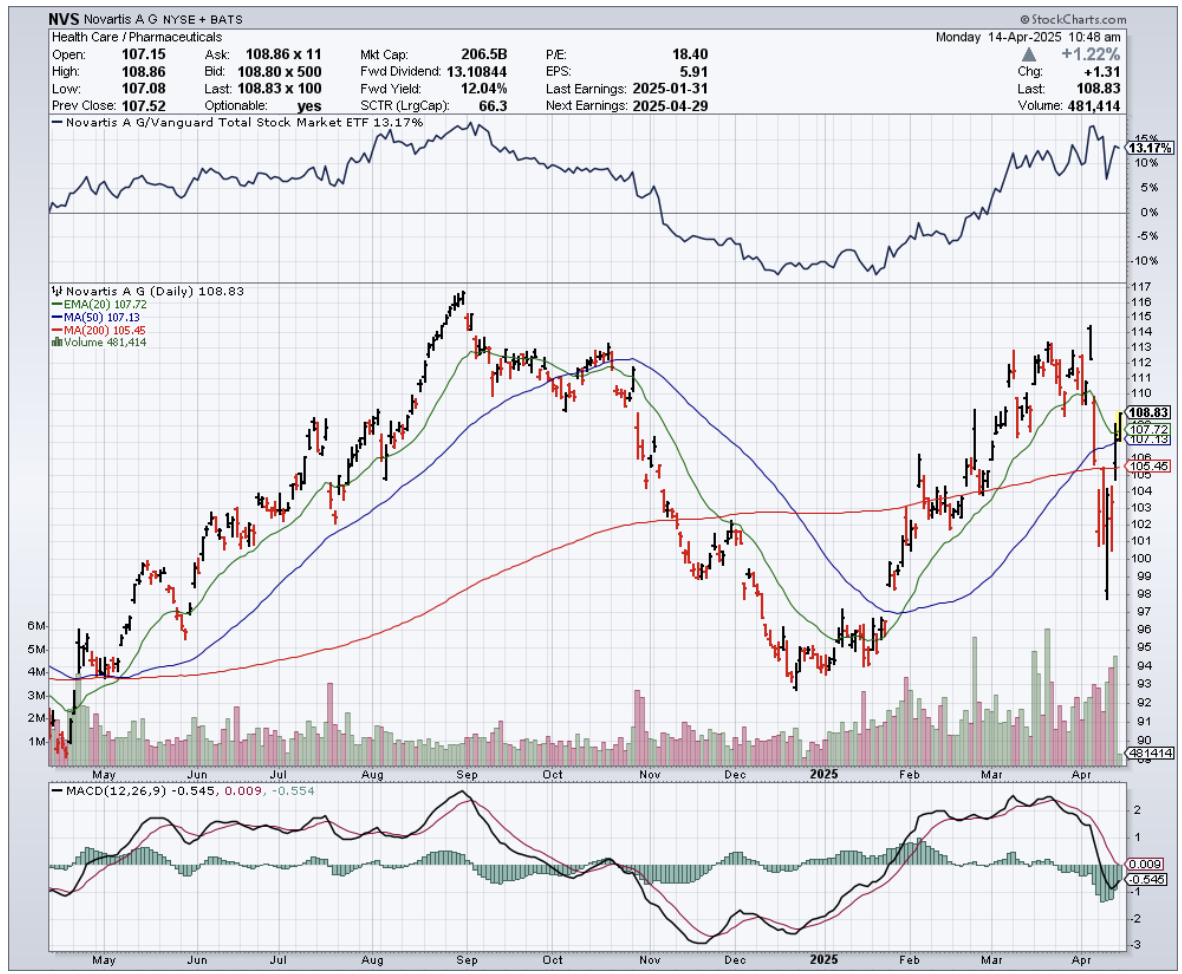

While most corporate breakups end with shareholders reaching for antacids, Novartis (NVS) investors are popping champagne instead.

The Swiss pharmaceutical giant's 2023 divorce from its generics business Sandoz (SDZNY) has transformed the company from a pharmaceutical conglomerate into a focused innovation machine – and the numbers would make even the most jaded among us whistle in appreciation.

I've watched pharmaceutical reorganizations for decades, and most resemble rearranging deck chairs on the Titanic. But Novartis has executed something genuinely transformative.

By jettisoning vaccines, ophthalmology, and generics, they've engineered a corporate metamorphosis that delivered 10% revenue growth to $51.7 billion in 2024.

Novartis now operates with laser focus on four therapeutic areas. Entresto, their heart failure medication, generated $7.8 billion in 2024 – up 31% year-over-year. That's roughly the GDP of Montenegro flowing from a single pill.

Cosentyx pulled in $6.1 billion (up 25%), while Kisqali and Kesimpta both jumped nearly 50%. These aren't merely drugs; they're annuities with patent protection.

The scale defies easy comprehension: nearly 300 million patients worldwide received Novartis medications in 2024. That's treating almost every American, then adding Japan for good measure. When pharma executives dream of market penetration, this is what they see before their alarm clocks rudely interrupt.

What separates Novartis from the pack is their capital allocation strategy. They're investing $9 billion annually in R&D – not throwing darts at a scientific board but methodically advancing a pipeline designed to replace blockbusters as patents expire.

Their 2024 acquisition of Chinook Therapeutics exemplifies this approach: precise, strategic, and focused on enhancing their nephrology portfolio rather than empire-building.

The geographic distribution of Novartis's revenue reveals similar strategic clarity. While 43% comes from the United States, their China strategy deserves special attention. Sales there surged over 20% in local currency during 2024.

Having tracked emerging markets throughout my career, I recognize the pattern – Novartis is positioning itself at the confluence of demographic shifts, increasing chronic disease prevalence, and expanding healthcare access.

For those who prefer hard numbers to market philosophy, Novartis delivered EBIT growth of 29% to $16.3 billion, with operating margins expanding to 31.55%. Net profit jumped to $11.9 billion, with margins at 23% – among the industry's highest.

Despite returning $15.9 billion to shareholders through dividends and buybacks, their balance sheet remains fortress-like.

Net debt stands at just $18 billion, with a Net Debt/EBITDA ratio below 1x – meaning they could extinguish their entire debt in less than a year with current cash flows.

Unlike pharmaceutical giants that bet everything on a single therapeutic area, Novartis has positioned itself as a formidable player across multiple high-value niches.

In oncology, rather than challenging Merck (MRK) or Roche (RHHBY) directly, they've developed unique assets like Pluvicto and Kisqali that face minimal head-on competition.

For cardiology, while Entresto faces patent expiration in 2025, they're already advancing next-generation therapies like Leqvio.

Meanwhile, the global prescription drug market exceeded $1.7 trillion in 2024 and should grow at 7.7% annually through 2030. Novartis has strategically positioned itself precisely where that growth curve steepens most dramatically.

No investment thesis is complete without acknowledging risks, and Novartis faces several significant challenges.

Entresto's patent cliff in 2025 creates a $7.8 billion revenue gap that needs filling. Cosentyx follows in 2027-2028.

Without Sandoz, they can't offset these losses with their own generics. Pricing pressure from Medicare and competition from other pharmaceutical giants present additional headwinds.

And pharmaceutical innovation remains inherently unpredictable – even with billions in R&D, clinical trials fail with alarming regularity.

Despite these concerns, Novartis shares still appear undervalued after rising nearly 19% over the past year.

The company trades at a P/E of 18.69x – substantially below the industry average of 55.91x. Its EV/EBITDA ratio of 10.97x represents a significant discount to peers.

Throughout my market-watching career, I've developed healthy skepticism toward corporate transformations. They typically generate more PowerPoint slides than actual results.

But Novartis has delivered tangible financial improvements that flow directly to shareholders. For those seeking healthcare exposure without betting on clinical-stage biotechs with binary outcomes, Novartis offers a compelling package of growth, income, and relative stability wrapped in Swiss precision. I suggest you buy the dip.