Mad Hedge Biotech and Healthcare Letter

May 23, 2024

Fiat Lux

Featured Trade:

(A DIVIDEND DERBY WINNER)

(ABT)

Mad Hedge Biotech and Healthcare Letter

May 23, 2024

Fiat Lux

Featured Trade:

(A DIVIDEND DERBY WINNER)

(ABT)

When you're at a racetrack, eyeing the horses before the big race, you're not just looking for a quick win. You want a stallion that'll keep delivering, race after race.

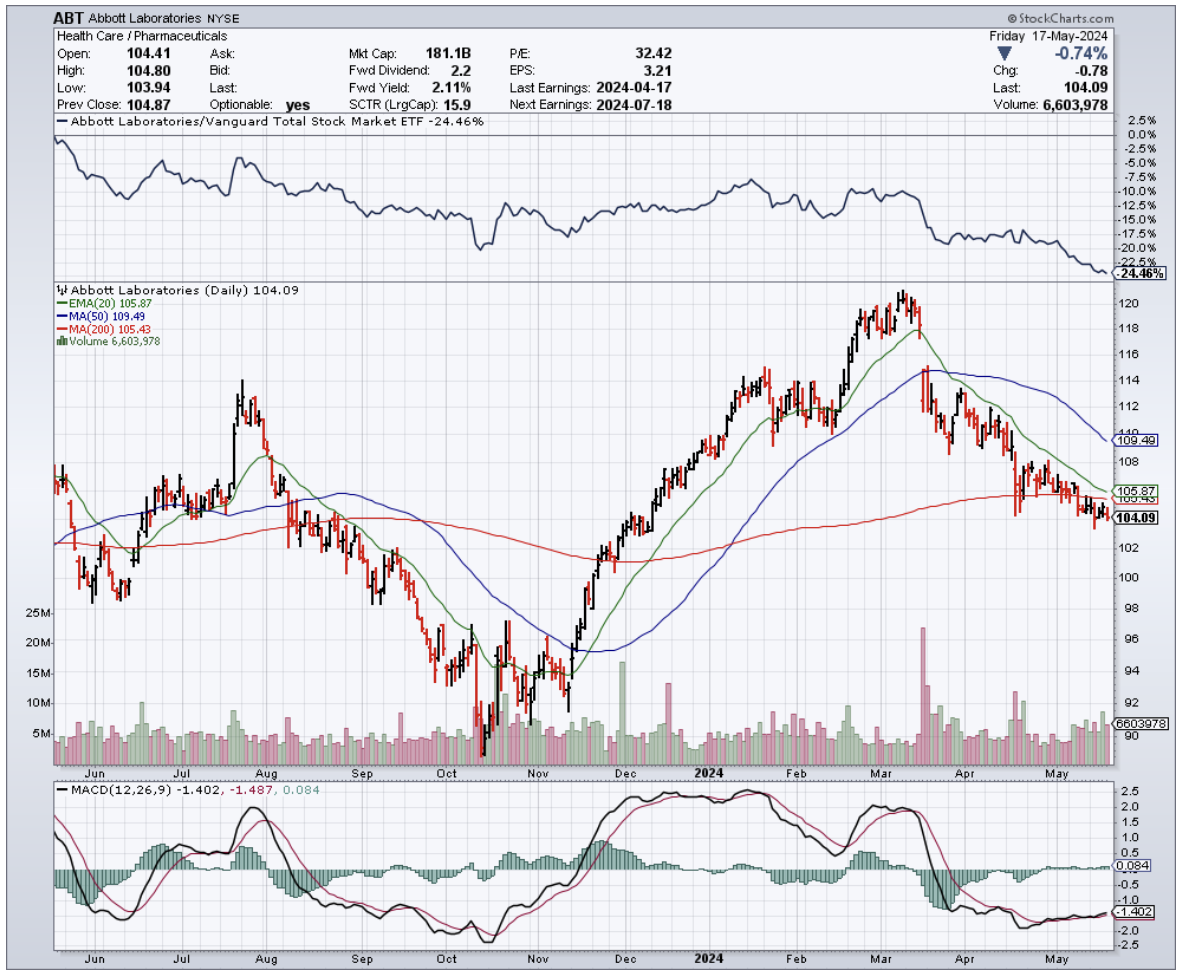

Well, that's exactly what we're hunting for in the stock market – companies that can keep those dividend payouts growing year after year. And if there's one thoroughbred you won't want to miss, it's Abbott Laboratories (ABT).

This biotech and healthcare giant isn't just keeping pace; it's setting the darned pace. Abbott is dominating the medical devices arena, a sector projected to skyrocket from $518.5 billion in 2023 to a whopping $886.8 billion by 2032. That's a steady 6.3% annual growth rate.

However, Abbott's not content with just one race – they've got their fingers in the lucrative pies of diagnostics and nutritional products, too.

But hold your horses, partner. Abbott isn't some one-trick pony. They've got their fingers in the lucrative pies of diagnostics and nutritional products too. Earlier this year, I gave this stock a thumbs-up, and it's only become more of a hot ticket since.

Fresh off their first-quarter reveal in April, Abbott's core business – think medical devices, diagnostics, and even baby formula – grew organically by an impressive 10.8% year-over-year.

This marks the fifth consecutive quarter of double-digit growth, so we're not just talking about a lucky streak here.

From what I can see, their Medical Devices segment is the real workhorse, surging 14.2% over the previous year. Their FreeStyle Libre device isn't just flying off the shelves, it's practically teleporting, with sales up 23% from last year. And with the FDA's recent green light for innovative products like TriClip and Amulet, Abbott isn't just playing in the major leagues, they're calling the shots.

Their Nutrition sector wasn't a slouch either, pulling in $2.1 billion in sales, a 5.1% increase over last year. Abbott's new Protality shake, launched in January, is specifically designed for those on weight loss journeys, adding another feather to their growth cap. Needless

Even their Diagnostics segment, which saw a dip due to the waning of COVID-19 testing, showed underlying strength in non-COVID testing. Their recent clearance for a concussion diagnostic test proves they're not slowing down on the innovation front.

When it comes to financials, Abbott is built like a brick house. With rock-solid interest coverage and debt servicing capacity, it's no wonder analysts are predicting a steady climb in their earnings. They've got a pipeline of new products and a market that's bouncing back from the pandemic, creating a recipe for success.

And don't even get me started on the dividends. Sure, Abbott's 2.1% yield might seem modest, but it's the growth story that's truly captivating.

Over the past decade, they've seen a staggering 11.4% annual growth in dividends. This ain't no stagnant stock, folks; it's a purebred built for speed.

Of course, no investment is without its bucking broncos. Abbott's still wrestling with the drop-off in pandemic-related revenues, and while their R&D spending is admirable, there's no guarantee those investments will always pay off. And let's not forget the ever-present threat of cyberattacks—a risk for any big player in today's world.

Still, while there might be a few hurdles in the race, Abbott Laboratories is a thoroughbred built for the long haul. With a rock-solid balance sheet, a track record of innovation, and a dividend that's been growing faster than a foal in springtime, this is a stock that's hard to beat.

And right now, the odds are in your favor. This company’s shares have been trading at a discount. So if you're ready to saddle up with a dividend growth thoroughbred, it's time to consider adding Abbott Laboratories to your stable. Because when it comes to the dividend derby, this is one horse you'll want to back.

Mad Hedge Biotech and Healthcare Letter

May 21, 2024

Fiat Lux

Featured Trade:

(THE FAT’S IN THE FIRE)

(RHHBY), (LLY), (NVO), (AMGN), (VKTX), (PFE), (MRK), (SNY), (ABT)

Well, well, well, look who's decided to crash the obesity-drug party. Roche (RHHBY), the Swiss pharmaceutical giant, has just unveiled some pretty impressive early-stage results for its weight-loss drug, CT-388. And let me tell you, this could be the start of something big.

Now, I know what you're thinking: "Another weight-loss drug? Yawn." But trust me, this is no ordinary contender.

In a small trial, patients who received CT-388 saw an average placebo-adjusted weight loss of 18.8% after just 24 weeks. That's right, 18.8%.

While it's hard to compare trials, experts are saying these numbers might even give Eli Lilly's (LLY) Zepbound, the current king of the market, a run for its money.

Let's take a step back and look at the bigger picture. The obesity drug market has been on fire lately, with everyone going gaga over these miracle pills.

Lilly and Novo Nordisk (NVO) have been dominating the scene with their drugs, Zepbound and Wegovy, but that hasn't stopped a whole host of other companies from trying to get a piece of the pie.

Merck (MRK), Sanofi (SNY), Abbott Labs (ABT), and Eisai have all tried their hand at weight-loss drugs and ultimately thrown in the towel.

More recently, Pfizer's (PFE) daily oral pill, danuglipron, has faced hurdles due to side effects. Amgen's (AMGN) drug, MariTide, is in Phase 2 studies and showing promise. And let's not forget Viking Therapeutics' (VKTX) VK2735, which has earned the nickname "twincretin" for its dual targeting of GLP-1 and GIP receptors.

So, what makes Roche's CT-388 so special?

Well, for starters, it's a GLP-1/GIP receptor agonist, which is similar to Lilly's Zepbound. In the Phase 1 trial, all participants achieved more than 5% weight loss, with 85% losing more than 10%, 70% shedding more than 15%, and a whopping 45% dropping more than 20% of their body weight. That's some serious weight loss.

Of course, there were some side effects, mainly mild to moderate gastrointestinal issues, but hey, that's the price you pay for looking fabulous, right? Roche is also testing CT-388 in patients with Type 2 diabetes, so stay tuned for updates on that front.

Now, I know you're all dying to know how CT-388 stacks up against the competition.

Notably, the drug's data looks strong compared to earlier studies of Zepbound. In fact, CT-388's efficacy results appeared "numerically higher" than Zepbound's.

But let's not get ahead of ourselves. Lilly still has a multi-year lead on Roche, so CT-388 isn't an immediate threat. However, it does suggest that the future of this rapidly growing market is up for grabs.

Now, let's talk about Roche. It’s the world's seventh-largest pharma company by market cap, sitting at around $205 billion. They pulled in $65 billion in revenue in 2023, second only to Johnson & Johnson (JNJ).

But here's the kicker—they've been struggling with growth, and their share price has taken a hit, down more than 25% over the past three years.

Contrast that with Eli Lilly and Novo Nordisk. Lilly's share price shot up 290% in three years, and Novo's climbed 226%.

Even though their revenues were less than half of Roche's in 2023, their market caps are sky-high. Why? Because of their blockbuster GLP-1 agonist drugs, Zepbound and Wegovy, which have shown jaw-dropping weight-loss results.

But could CT-388 be the underdog story Roche needs?

With the obesity market estimated to reach a staggering $100 billion by 2030, and over 1 billion people worldwide suffering from obesity, the potential is enormous.

Of course, there's still a long way to go for CT-388. Cross-trial comparisons can be tricky, and Roche's Phase 1 trial was much smaller than Lilly's pivotal study of Zepbound.

Plus, we don't have all the juicy details on patient characteristics, dose titration, and long-term weight loss just yet.

But here's the thing: Roche has scale and infrastructure on its side. It could potentially outmuscle smaller players like Viking and Boehringer Ingelheim.

And if CT-388 can match or even surpass the performance of current and future GLP-1 agonists? Well, let's just say those peak revenue forecasts might be in for a surprise.

So, is Roche the dark horse you should bet on in the obesity-drug race? If you're looking to get in on the action without paying the premium commanded by Lilly and Novo, or taking on the higher risk of smaller players, Roche might just be the ticket.

With promising mid-single-digit revenue growth on the horizon and a strong position in other areas like oncology and autoimmune disorders, Roche could be a smart play for anyone keen on the obesity drug market.

As for me? Well, you know I love an underdog story. And CT-388 might just be the Cinderella story of the year. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

May 16, 2024

Fiat Lux

Featured Trade:

(THE COMEBACK KID OF VACCINES)

(NVAX), (SNY), (BNTX), (PFE)

What a rollercoaster it’s been for Novavax (NVAX). Their latest Q1 2024 earnings were a mixed bag—they beat EPS expectations but missed on revenue. A far cry from when they were the undisputed rising star of the biotech world, their stock soaring a mind-boggling 6000% during the peak pandemic days.

Back then, they were the hotshots, but lately, the big leagues with the right connections had been sweeping opportunities right out from under them. Until now.

Earlier this week, Novavax’s shares took off like a rocket, even hitting a mind-blowing 175% jump in premarket trading at one point. That's right – 175%!

Turns out, those Q1 earnings weren't all doom and gloom. Sure, they missed on revenue, but their net loss got chopped in half compared to last year, and revenue still managed to grow by a respectable 16%. This isn't just a rebound; it's a sign that Novavax might just be back in the game.

But let's be real, the main reason behind this stock explosion is their shiny new deal with Sanofi (SNY), a heavyweight in the pharma world. We're talking a cool $1.2 billion.

Remember, Novavax was once the darling of the biotech scene during the pandemic, their stock soaring a mind-boggling 6000%. But lately, they've struggled to secure the big partnerships needed to really make a splash in the market. This Sanofi deal? It's the lifeline they've been waiting for.

This isn't just any partnership. Sanofi's shelling out a cool $500 million upfront, with another $700 million on the line if certain milestones are met, all for a piece of the Novavax COVID-19 vaccine pie and a chance to collaborate on future projects.

Now, Sanofi isn't exactly known for throwing money around willy-nilly, so this is a major vote of confidence. What's got them so excited?

Novavax's not-so-secret weapon: Matrix-M, a revolutionary adjuvant technology that's got the potential to shake up the vaccine world.

Think of Matrix-M as a personal trainer for your immune system. It doesn't fight the disease itself, but it whips your body's defenses into shape, making them stronger and more effective at fighting off infection.

To understand this better, imagine you're going into a boxing match. The vaccine is the boxer, ready to throw punches at the virus. But Matrix-M is the coach in their corner, giving them the extra training and conditioning they need to deliver a knockout blow.

Novavax isn't just using this personal trainer for their COVID vaccine. They're exploring how to use it to coach our immune systems in fighting all kinds of diseases, even the heavyweights like cancer. It's like having a secret weapon that could revolutionize how we approach health and wellness.

That means Matrix-M technology has the potential to open up a whole new world of treatment options and revenue streams. It's like investing in a gym that's developing a revolutionary new training program – the potential gains could be huge.

Now, this tech isn't a sure thing yet, but Sanofi's backing is a big deal. It's a vote of confidence that screams, "We believe in you, Novavax!"

And when a pharma giant like Sanofi puts their money where their mouth is, you know they see serious potential in those nanoparticle innovations and adjuvant magic. After all, who better to mass-produce a vaccine than one of the biggest players in the game?

This isn't just about COVID-19, either. This is about building a foundation for a whole new generation of vaccines, the kind that could rewrite the rules of healthcare as we know it.

Novavax isn't just sitting back and waiting, either. They're already gearing up for Phase III trials of a combo COVID-19-Influenza vaccine and diving headfirst into cutting-edge mucosal vaccine technology and high-density nanoparticles.

And let's not forget the cold, hard cash this deal brings to Novavax.

With half of Sanofi's investment expected to hit their bank account in just 10 days, Novavax's 2024 financial outlook is looking a lot brighter. They're now projecting revenues between $970 million and $1.17 billion – a serious boost for a company that's seen its share of financial turbulence.

Novavax might have been down for the count, but they're not out of the fight. With Sanofi backing them up, they've got a real shot at becoming a major player in vaccine innovation again.

For investors, this could be a chance to get in on the ground floor of a comeback story that could be the stuff of legend.

Mad Hedge Biotech and Healthcare Letter

May 14, 2024

Fiat Lux

Featured Trade:

(EARS TO THE GROUND)

(REGN), (LLY), (FENC)

When your kid is part of a cutting-edge trial for hearing restoration, you're practically glued to their every reaction. That's the case for the parents of the first little one to receive Regeneron's (REGN) experimental gene therapy, DB-OTO.

This groundbreaking treatment delivers the missing otoferlin protein to the sensory hair cells in the ear, restoring signal transmission and, theoretically, giving these kids the gift of hearing.

The baby, part of the CHORD trial, started responding to sounds at home way before the docs officially confirmed it.

"Beautiful" is Regeneron described this early sign of progress. Turns out, nothing beats seeing your kid react to the world of sound for the first time.

Let me give you the basics of this therapy. So, imagine the sensory hair cells in your ear as a team of tiny dancers. They groove to the vibrations of sound, signaling to your auditory nerve and ultimately your brain.

Kids with this specific genetic hearing loss have the dancers, but they're out of sync – they can't communicate that signal to the brain. DB-OTO is like giving these dancers a choreographer, delivering the missing otoferlin protein, and restoring the signal transmission.

Actually, DB-OTO isn't entirely a Regeneron creation. They snagged it up when they acquired Decibel for $109 million in 2023. But this wasn’t a hostile takeover – these two companies had been working hand-in-hand on DB-OTO since 2017, making the deal a no-brainer. Heck, Regeneron even brought over the team behind the project to keep things running smoothly.

And as it turns out, Regeneron and Decibel didn't have to reinvent the wheel (or the eardrum) with their delivery method.

They took a page from the cochlear implant playbook, making it easier for ear, nose, and throat docs (ENTs) to jump on board when this therapy eventually hits the market. They figured that they could just take this groundbreaking technology and make it work with techniques surgeons already know like the back of their hands. Smart move, right?

One unexpected twist? The family noticed the kid's voice sounded less harsh without the cochlear implant.

Now, that's not a hard data point, but it hints that DB-OTO might offer something unique: a more natural hearing experience compared to cochlear implants, which tend to have a robotic sound that takes some getting used to. Cochlear implants bypass the ear altogether, zapping the auditory nerve directly. Effective, sure, but not exactly the most elegant solution.

It's not just about regaining hearing – it's about unlocking a child's world. Regeneron’s ASGCT presentation showcased patient 1's incredible journey: responding to sounds at 3 weeks, meaningful sounds by 6 months, and even hearing with the cochlear implant turned off at 24 weeks.

A second 4-year-old patient is also showing promising signs, with improved hearing at the same early time points. Side effects? Nothing more than a common ear infection, which was easily treated.

But this wasn't an overnight miracle. Regeneron and Decibel brainstormed this idea six years ago, putting their heads together to figure out where they could make a real difference. They seem to have found their niche.

And they didn't just buy one therapy – they snagged a whole pipeline of possibilities. There's AAV.103 for a different type of hearing loss, and AAV.104 for another genetic form. They're even tackling balance issues, because apparently, ears do more than just listen. These additional therapies fit into Regeneron's broader strategy of becoming a leader in the auditory space.

Next, let's talk dollars and cents, shall we?

Regeneron shelled out $213 million (if you include those fancy CVRs) for Decibel. That's a hefty bet, but they're banking on DB-OTO getting regulatory approval in multiple countries by 2028. Ambitious? Absolutely. But the potential payoff for patients – and investors – could be worth it.

As expected, Regeneron's not the only one with their stethoscope in this growing market.

Eli Lilly (LLY) wasn't far behind, scooping up Decibel's rival Akouos for a whopping $487 million in late 2022. Plus, they're also gunning for that otoferlin gene therapy prize.

And don't forget Fennec Pharmaceuticals (FENC), who snagged FDA approval for their chemo-induced hearing loss treatment last year. Looks like everyone wants a slice of this pie.

Now, for the data geeks (I know you're out there).

Regeneron's Q1 results were a tad underwhelming for Wall Street, with EPS at $9.55 (below the $10.17 estimate) and revenue dipping slightly to $3.15 billion, mostly due to the COVID drug Ronapreve drying up.

But take that out of the equation, and revenue actually grew 7%. Not that bad.

And there's good news elsewhere. Sales of Dupixent and Libtayo are soaring, up 24% and a whopping 45% respectively. That's where the future lies.

Sure, they've had some bumps in the road (the FDA rejecting odronextamab wasn't ideal), but their Eylea HD launch is gaining steam, with $200 million in sales already.

These successes, coupled with the potential of DB-OTO and the other auditory therapies, paint a promising picture for Regeneron's future growth.

So, what should you do? Keep your eyes on their pipeline, especially those new oncology and weight-loss treatments. And with a $3 billion stock buyback plan, Regeneron's showing they're confident in their future.

This might not be a slam dunk, but it's a bet on a company that's not afraid to swing for the fences in the biotech game. With a strong pipeline, a track record of innovation, and the financial muscle to back it up, Regeneron is positioning itself to be a major player in this growing market.

For those willing to ride out the bumps, the long-term payoff could be music to their ears.

Mad Hedge Biotech and Healthcare Letter

May 9, 2024

Fiat Lux

Featured Trade:

(A HIGH-RISK, HIGH REWARD BIOTECH PLAY)

(CRSP), (VRTX), (DNA)

Ah, the "golden age of biotech" — remember when that was the phrase du jour? Well, it might not be on everyone’s lips these days, but let me tell you, the biotech arena still holds some golden tickets for those with an eye for long-term gems.

These hotbeds of innovation aren’t just cooking up your everyday aspirin; they’re on the front lines battling the big beasts like rare diseases and crafting cures that might have seemed like sci-fi a few decades ago.

So, why should we keep our wallets ready for biotech? Simple: life-saving meds aren't exactly impulse buys at the checkout counter. People need these drugs, economy be darned. And that, my friends, brings us to a biotech belle of the ball: Crispr Therapeutics (CRSP).

Now, if you’re hunting for the disruptors of the disruptors, cast your eyes on CRISPR/Cas9 gene-editing technology. And leading the charge? Crispr Therapeutics, of course. Their new FDA-approved therapy, Casgevy? Think of it as a microscopic search-and-replace function for your genes, pinpointing the exact spot that needs fixing. Snipping out a faulty gene? Child's play for CRISPR.

This isn't just about editing genes willy-nilly. This technology, honed and shepherded through the halls of academia, now bears the fruit of a Nobel Prize in Chemistry in 2020 — a tip of the hat to one of CRISPR Therapeutics’ founders, Charpentier.

With exclusive rights to this CRISPR/Cas9 tech, they’re not just playing in the minor leagues; they’re major league players with the FDA-approved Casgevy aimed at tackling sickle cell disease (SCD).

If you’re feeling more cautious, however, then Vertex Pharmaceuticals (VRTX) might be a steadier ride. It’s a bigger boat with more therapies on the market.

But if you’re feeling a bit more Maverick, a direct bet on Crispr Therapeutics could be your kind of play. Smaller in size, sure, but with a direct line to the gains (or pains) from Casgevy, and boy, does biotech love a high stakes game.

So, what does throwing your chips in with CRISPR entail? Let's unwrap this.

First off, their Casgevy is a pioneering ex vivo CRISPR-Cas9 therapy—think of it as a pit stop where cells are tuned up outside the body before being put back in the race. It’s already got the green light from the FDA for not one, but two heavy hitters: sickle cell disease and transfusion-dependent beta-thalassemia (TDT).

But here’s the rub: despite these big wins, CRISPR’s stock has been more or less jogging in place for five years. Why? It seems the market’s giving the side-eye to the commercial rollout of these therapies. But hold up—shouldn’t the stock be climbing as these treatments start to hit the market?

Well, the game here is more marathon than sprint. We're talking about a potential addressable market for these treatments that’s just aching to be tapped into. But there’s a catch—the price tag is a whopper at $2.2 million a pop. That’s a lot of zeroes.

Now, let’s do some napkin math.

If CRISPR could corner the market on all SCD and TDT patients across the US and EU, we're looking at a ballpark figure of around $38.6 billion in potential revenue. And here's the kicker: the real puzzle is figuring out how many of these folks will actually get treated with Casgevy, given the steep costs and varied insurance landscapes.

Yet, if CRISPR can snag just a slice of this market, even with a high discount rate factored in for all the risk, the numbers start to look pretty tasty.

Imagine if they treated all these patients over a decade—ka-ching! That’s an NPV (net present value) that could potentially justify CRISPR’s current market cap all on its own.

Overall, investing in CRISPR Therapeutics could be akin to buying a stake in Genentech (DNA) back in the day—before they hit the biotech jackpot.

With Casgevy already approved and more potential blockbusters in the pipeline, CRISPR isn't just about today’s gains; it’s about betting on a biotech future that could be as revolutionary as the invention of the wheel—if the wheel could edit your DNA, that is.

What’s the verdict then? If you’re game for a ride on the wild side of biotech with a company that’s rewriting the genetic code of healthcare, CRISPR Therapeutics might just be the stock to watch. So buckle up because it’s going to be an exciting ride.