Mad Hedge Biotech and Healthcare Letter

April 18, 2024

Fiat Lux

Featured Trade:

(A RARE OPPORTUNITY OR A PROBLEMATIC DEBT-ACLE?)

(AMGN), (LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

April 18, 2024

Fiat Lux

Featured Trade:

(A RARE OPPORTUNITY OR A PROBLEMATIC DEBT-ACLE?)

(AMGN), (LLY), (NVO)

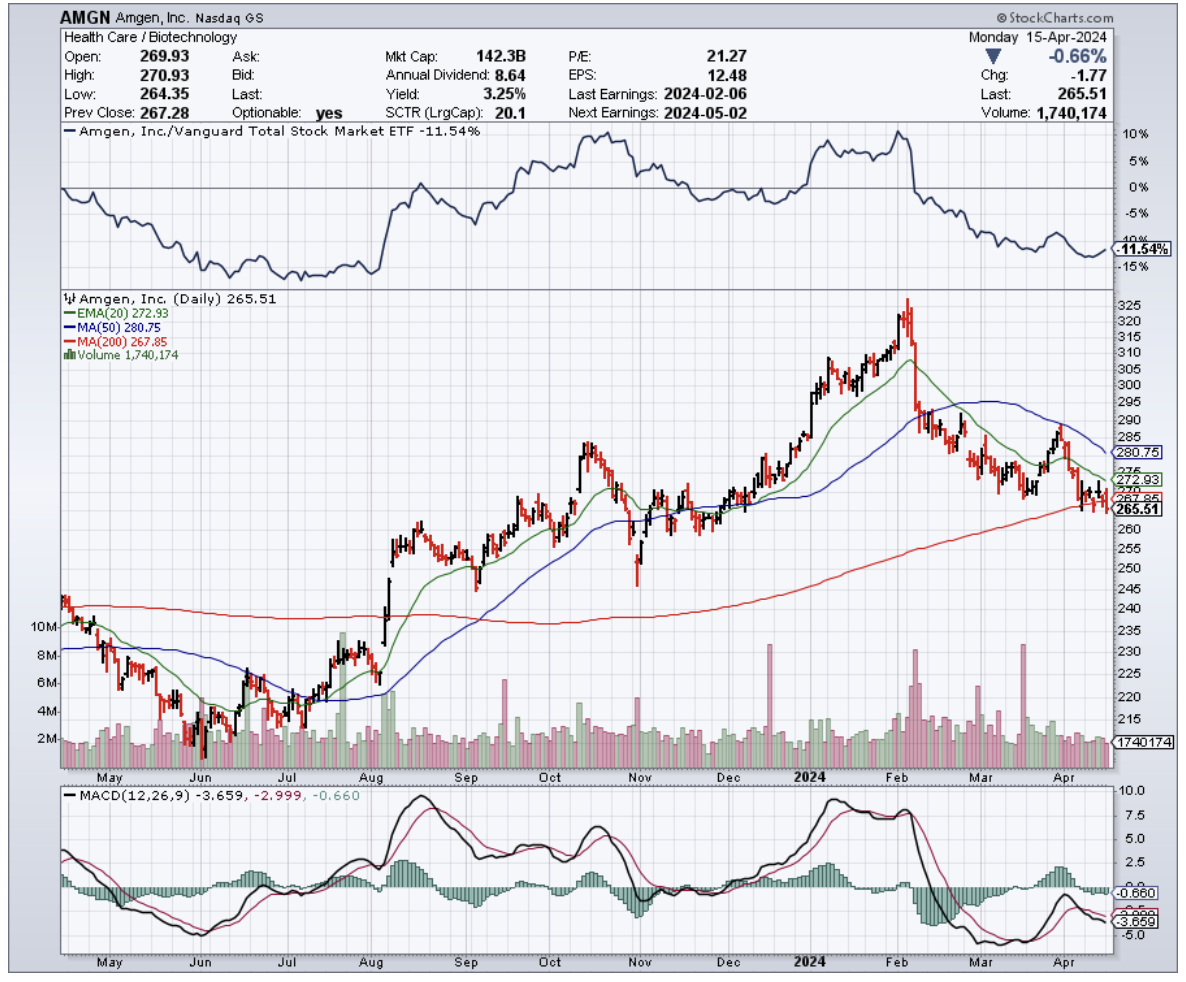

Remember Gordon Binder and his "Science Lessons?" Well, Amgen (AMGN) seems to be re-reading a few chapters from the book by its legendary former CEO.

Their nearly $28 billion buyout of Horizon Therapeutics (HZNP) screams blockbuster ambition, but it also means they loaded up on debt like it's going out of style. This HAD better work.

Why the gamble? Horizon brings heavyweight rare disease drugs like Tepezza to the table. Sales have been flatlining near $2 billion, but Amgen smells potential. With the indication just expanded and a measly few percent of patients treated, there's room to run...if they can find those patients. That's the tricky part with rare diseases.

Other gems like Uplizna round out the deal. Now, it's all about whether Amgen can make this expensive new portfolio pay.

Let’s take a look at Amgen’s 2024 pipeline. The biotech’s goals this year center on a few key drugs – some acquired, some homegrown.

Tepezza and Uplizna are all about finding those elusive rare disease patients and expanding market access. We're not just talking sales growth here... it's about proving their ability to dominate this niche.

In their "General Medicine" department, there's Olpasiran in Phase 3. A stellar Phase 2 could mean over a BILLION in sales if it gets the green light. But Phase 3, as we know, is where the tough questions get asked.

Over in Oncology, I’m keeping an eye on Tarlatamab, Lumakras, Blincyto, and Nplate. They're the revenue drivers of the future, with Tarlatamab aiming for billions by the 2030s.

Lumakras was supposed to be a star, but it's a bit slow out of the gate. Then there's Blincyto – already raking in the big bucks with nearly 50% year-on-year growth. This one's HOT.

Nplate's a blockbuster with almost $2 billion in sales, but US government orders make it a tad volatile. Tezspire is another potential star, flirting with the billion-dollar mark.

Bottom line? Amgen is hustling to build a diverse portfolio for the long haul.

Crunching the numbers, Amgen's 2024 guidance looks strong, boosted by that Horizon acquisition.

They're projecting about $33 billion in revenue and decent EPS. Tax breaks and low capital expenditures are sweet bonuses.

But...remember that debt. It's over $60 billion on the long-term books. Luckily, Amgen locked in good rates on those bonds, but that interest bill? It's a beast they'll have to tame eventually.

Amgen’s shareholder returns are mostly a chunky 3%+ dividend, not much to write home about. The real magic depends on those high-powered sales teams turning the rare disease business into a cash machine and seeing those other drugs deliver. If it happens, cash flow will surge, and everyone will get fatter payouts.

As for the biggest threat to Amgen’s future? The ever-changing, cash-hungry beast that is the biotech industry.

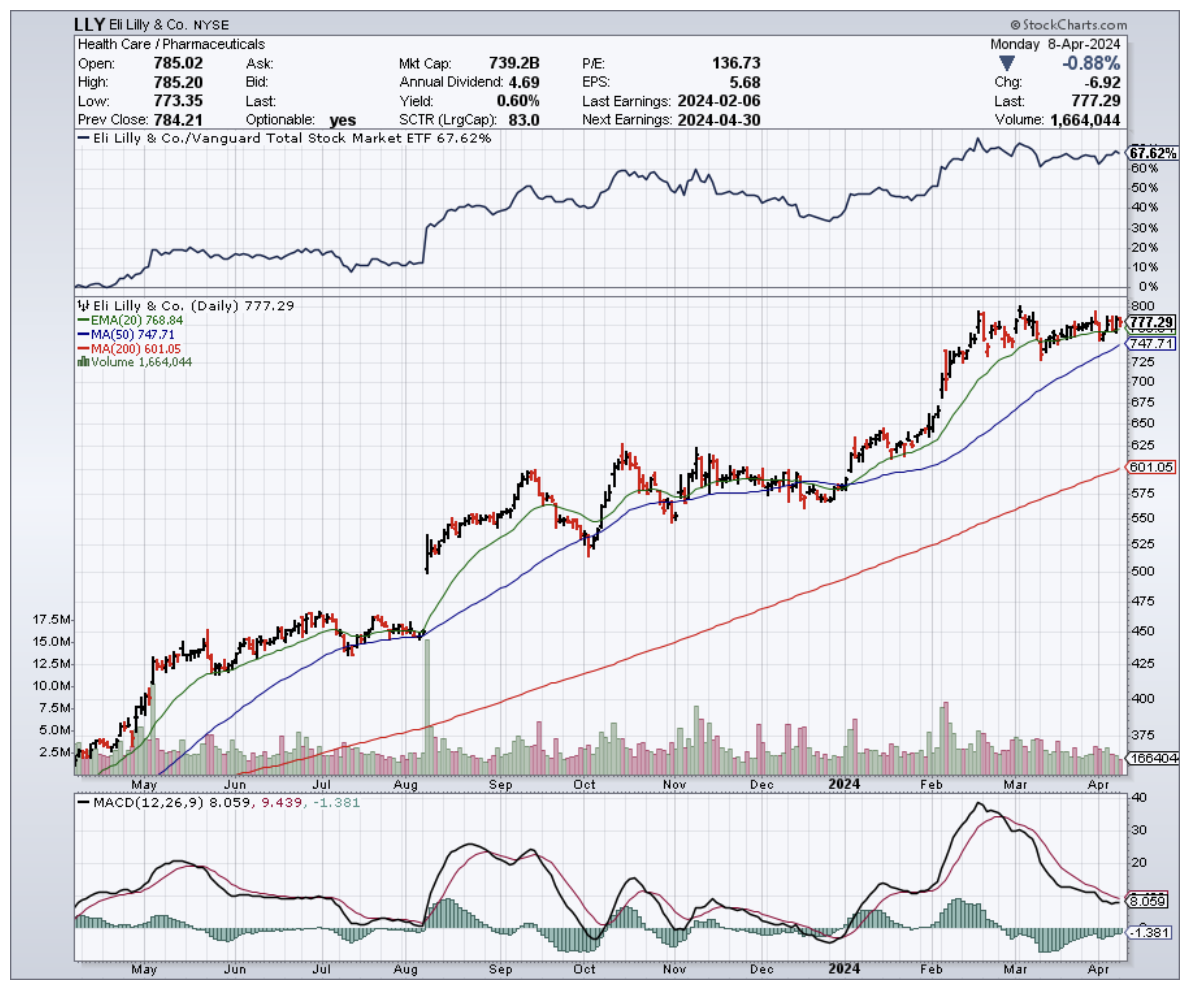

Amgen's constantly fighting patent expirations, forcing them to pump cash into R&D just to stay ahead. You hit some home runs, like the crazy new weight loss drugs driving skyrocketing revenues as seen in the success of Eli Lilly (LLY) and Novo Nordisk (NVO), but more often, you strike out. This is why long-term investors in Amgen should strap in for a bumpy ride.

Overall, Amgen's got a unique mix of assets. And that Horizon Therapeutics move? Bold but calculated. It gives them a boatload of rare-disease drugs and pairs them with top-notch sales teams.

Plus, there's a bunch of promising candidates in their pipeline. The biotech world is an industry where success is never guaranteed, BUT Amgen's got the potential to keep knocking it out of the park. If they do, those shareholder returns should get a whole lot sweeter. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 16, 2024

Fiat Lux

Featured Trade:

(IS THIS BIOTECH BULL RUN OUT OF STEAM?)

(VRTX), (CRSP)

Vertex Pharmaceuticals (VRTX) has been crushing it. They're a powerhouse in the healthcare game, no doubt.

But with that stock price shooting for the moon and a $100 billion valuation, it's got me asking: Is this ride getting a little too rich for our blood? Is it time to cash out and look for greener pastures, or is there still some juice left in Vertex's tank?

Let's take a look at why the Vertex bulls are so pumped.

The company's a giant in cystic fibrosis – no argument there. Their drug Trikafta/Kaftrio is practically printing money, raking in a whopping $8.9 billion last year. Sure, things slowed a bit in 2023, but hey, that's still serious cash.

But here's the thing: If Vertex was just about cystic fibrosis, the price tag could make a careful investor go "Whoa, Nelly!" Growth investors, though, see a bigger picture, a company ready to branch out and rake in even more dough.

Take the recent FDA approval for Casgevy, the gene therapy treatment Vertex developed with CRISPR Therapeutics (CRSP). This thing could be HUGE for treating blood disorders like sickle cell disease. In fact, its potential peak sales are projected at $3.9 billion — and even with Vertex splitting the profits, that's a juicy opportunity.

Another potential blockbuster is Vertex's non-opioid painkiller, VX-548. The results so far are looking good, and it’s pegged to become a $5 billion moneymaker. Think about the opioid mess we're in – a safe, effective alternative could be massive.

We need to be patient with VX-548 though. It's not approved yet, but it's definitely one to watch. Vertex is aiming to file for approval around the middle of this year, specifically for treating those nasty post-surgery pains.

Aside from these, Vertex is setting its sights on other serious unmet needs. Take APOL1-mediated kidney disease. This nasty condition lurks in the shadows until BAM, your kidneys are about to bail on you. Signs like protein in your urine and swelling mean it might be too late.

But, Vertex has a potential solution up its sleeve: inaxaplin. Early trials look promising, with patients seeing major improvement. The results were so good that they're even going to start testing it in younger patients.

Could inaxaplin be another game-changer? Well, Vertex thinks it could help at least 100,000 patients in the US and Europe – that's even more than the number of people with CF they already serve.

And, get this: There's NO approved treatment for the root cause of this kidney disease. If Vertex wins this race, it could turn into a blockbuster franchise to rival its lucrative CF success.

On top of these candidates, Vertex recently scooped up Alpine Immune Sciences (ALPN), and that move shows just how serious they are at adding more firepower to their pipeline. And, if Alpine's drug makes it through those big Phase 3 trials – the ones set to start soon – Vertex could end up being worth a LOT more than the $4.9 billion they shelled out.

For context, let's break down what Alpine does. They're all about those fancy protein-based immunotherapies, fancy words for treatments that target the immune system for autoimmune and inflammatory diseases. While their drugs are still in the testing phase, one called povetacicept looks especially promising for autoimmune kidney diseases like IgA nephropathy.

Translation: Alpine's got some traction towards treating these nasty kidney diseases. They've finished Phase 2 trials and are gearing up for the big leagues: Phase 3. That's where they test the drug on a whole bunch of patients, comparing it to a placebo, to get the data that could make regulators give the thumbs up for market launch.

With all these in mind, let’s talk about the elephant in the room: Is Vertex overpriced?

The stock's been on a tear, rocketing up 90% in just three years. And at those hefty multiples – 29 times earnings, 11 times revenue – it sure doesn't look cheap.

But, if you believe in the promise of Vertex's future, things look a little different. Check out that PEG ratio – a measly 0.5. That's a bargain hunter's dream, especially for a stock with so much growth potential.

So, what should you do: buy, sell, or hold Vertex? Well, this stock's got growth potential and it's not so insanely expensive that you gotta dump it today. If you already own it, hang tight – it doesn't look like disaster's lurking around the corner.

The bigger question is for those of you who missed the boat. Is it worth jumping on now?

As long as you're in it for the long haul, Vertex could still make you a nice pile of cash. Keep an eye on those VX-548 regulatory filings – if Vertex is moving ahead, they're probably feeling good about the drug's chances. And with Casgevy getting the green light for multiple uses, Vertex already has a shiny new revenue stream alongside its cystic fibrosis powerhouse.

So while the stock price might make you wince, don't discount the long-term potential. This biotech bull might take a breather every now and then, but the race has just begun. I suggest you buy the dip.

Mad Hedge Biotech and Healthcare Letter

April 11, 2024

Fiat Lux

Featured Trade:

(BELLY BUSTERS)

(NVO), (LLY), (JNJ), (AMGN), (RHHBY), (GSK), (VKTX)

Did you know that more Americans are now trying to lose weight than trying to quit smoking? That's a staggering shift, and it has a lot to do with the buzz around those new obesity drugs.

Novo Nordisk (NVO) got the ball rolling in 2021 when they received the green light to market their diabetes drug, Ozempic, as a weight loss miracle called Wegovy.

Not to be outdone, Eli Lilly (LLY) swooped in the fall of 2023 with Mounjaro – also a diabetes drug, sold as Zepbound – that got the FDA nod for weight loss, too.

Then, the whole pharma world, it seems, has started to go all-out on obesity, flooding the market with a whole new generation of weight loss drugs.

To date, there are 124 obesity meds in the works – a mix of 61 Phase 1 hopefuls, 47 in Phase 2, eight in Phase 3, and eight already greeting patients.

Remember that whole fen-phen disaster back in the 90s? That left a bad taste in everyone's mouth when it comes to weight loss drugs.

But things are different this time. These new obesity meds, especially those from Novo Nordisk and Lilly, are a game-changer. They're blowing those old weight loss pills out of the water.

It's not about fitting into those skinny jeans anymore (though that's a nice bonus). The focus is on health.

And while Novo Nordisk and Eli Lilly might be the big names in the obesity drug game, they've got competition. There's a whole crew of pharma companies jumping on the bandwagon, like Currax Pharmaceuticals, Roche (RHHBY), GlaxoSmithKline (GSK) – you get the picture.

But here's the really wild part about these drugs like Mounjaro and Wegovy, which use GLP-1 (Glucagon-like peptide-1) compounds to treat diabetes: They kinda stumbled onto their weight loss powers by accident.

Turns out, while they were busy helping diabetes patients, boom, patients started shedding pounds. Talk about a happy side effect.

As expected, this has created excitement in the market. Now, usually in the drug world, it's baby steps forward. A little better here, a bit less nausea there... yawn.

But with eight of these drugs already in the late stages of development (Phase 3), expect even more surprises as potential breakthroughs could bypass traditional drug trial phases for a faster route to market.

Frankly, I'm shocked at the number of new mystery drugs suddenly popping up in early testing. Even those old-school Big Pharma players are jumping in: AstraZeneca (AZN), Novartis (NVS), Amgen (AMGN), and, heck, even Johnson & Johnson (JNJ) – everyone wants a slice of the obesity pie.

Now, this whole obesity meds craze reminds me of what happened with those PD-1 drugs in cancer treatment.

One good result, and suddenly everyone was scrambling to get their version to market. But like in a reality TV show, not everyone makes it to the finale.

But what's the endgame in this obesity market expansion? Not 124 contenders, that's for sure.

Even right now, with everything in its early stages, you can already see which candidates have the potential. The competition's going to get fierce, and only the strongest drugs will survive.

Viking Therapeutics (VKTX), for example, has a dual GLP-1 and GIP agonist showing serious promise. After just 13 weeks, patients lost an average of 14.7% of their weight.

This data, released in February, proves Viking’s not just chasing the big pharma players; they're running right alongside them.

Now, over at Novo and Lilly, the pace hasn’t slowed down one bit either. Wegovy, which is Novo's contender in the ring, just got a nod in March for something a bit bigger than weight loss.

It’s been approved to tackle some serious heavyweights — cardiovascular deaths, heart attacks, and strokes in adults dealing with obesity or who are overweight. It's like getting a one-two punch for health.

As for Eli Lilly? They’ve been making some noise with tirzepatide, especially around metabolic dysfunction-associated steatohepatitis, or MASH for short.

They’ve got results showing that 74% of adults who were either overweight or obese managed to kick MASH to the curb without any increase in liver scarring after sticking with the treatment for 52 weeks.

Sadly, the biggest roadblock isn't the science, it's the money. It’s not just about making these drugs. It’s about getting them into the hands of those who need them most.

The current scene? A bit of a heartbreaker.

Most US insurance companies are drawing the line at covering Wegovy or Zepbound for obesity. This leaves a hefty bill on the table, putting these potentially life-altering treatments out of reach for many.

Think about it – the people who could benefit the most, maybe those on Medicaid or living paycheck to paycheck, are staring at a closed door. And let’s not even get started on Medicare, which, as of now, can’t even touch these drugs.

It’s a strange paradox, isn’t it? The very treatments that could lift the weight of obesity off society’s shoulders are dangling just out of reach for many.

So, now, the burning question isn’t so much about whether these treatments can make shareholders and companies do a happy dance. It’s more about where we’re heading.

Think about cancer treatment – the sickest patients get the cutting-edge drugs first. What would that even look like in obesity?

Will all these 124 experimental options help level the playing field, finally forcing insurers to step up? Only time will tell.

As of now, the obesity treatment field is going through a revolution. While the market faces challenges like accessibility, I suggest you closely monitor the progress of key players like Novo Nordisk and Eli Lilly.

Consider smaller, innovative companies, such as Viking Therapeutics, for potential high-risk, high-reward investments as well.

Mad Hedge Biotech and Healthcare Letter

April 9, 2024

Fiat Lux

Featured Trade:

(A PHARMA TORTOISE IN A MARKET FULL OF HARES)

(JNJ)

For the thrill-seekers who get a kick out of watching industries move faster than a cat on a hot tin roof, riding the wave of trending growth stocks might be for you.

But for those who prefer a good night's sleep over night sweats about market swings, pinning down stocks that promise a smooth sail towards retirement is the name of the game.

Now, if I were to put my money on one sector that's as steady as they come, I'd bet the farm on healthcare.

Why, you ask? Well, let’s take a look at the numbers.

U.S. healthcare spending ballooned to a jaw-dropping $4.5 trillion in 2022. That’s $13,493 for every man, woman, and child. With an army of about 10,000 baby boomers daily marching into Medicare eligibility, it's a safe bet this number's on a one-way trip up.

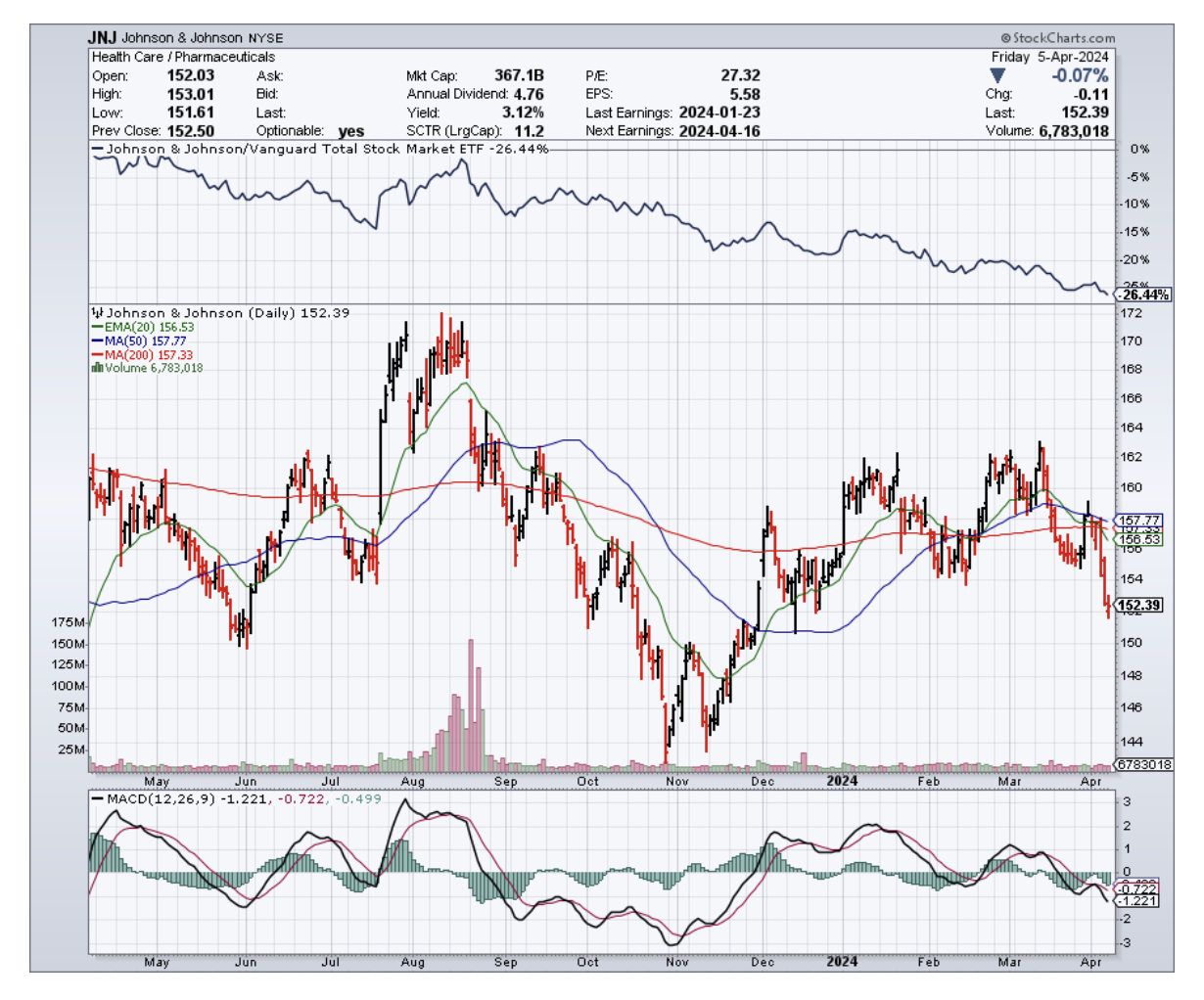

Let’s talk about a healthcare giant arena that might not make you rich overnight, but it's a dividend machine you can count on: Johnson & Johnson (JNJ).

Think of J&J as the responsible older sibling of your portfolio. They recently raised their dividend for the 61st year in a row. That's a 3.1% yield right now – a pretty good return for such a dependable company.

Over the past five years, J&J’s payout has beefed up by over 25%. Quite the feat, especially considering it just slimmed down by spinning off its consumer health division.

This strategic move has made J&J a lean, mean, dividend-paying machine. They're now laser-focused on their core businesses: med tech and pharmaceuticals.

This focus is paying off – they raked in a sweet 11.1% jump in adjusted earnings in 2023. With dividends sitting pretty at $4.76 a share and a clear path for growth, this blue chip just keeps getting better.

But J&J's not just a big fish in the healthcare pond – it's practically the whole ocean. They hauled in a jaw-dropping $85.2 billion in revenue last year. This company has a decades-long track record of turning its massive size into consistent growth for shareholders.

Case in point: J&J just made a big power play, grabbing Shockwave Medical (SWAV) for a cool $13.1 billion.

Not bad for a company that clearly loves shopping for heart-focused companies – remember when they scooped up heart device maker Abiomed for $16.6 billion in 2022? This latest acquisition isn't just about beefing up their medical device game. It's their ticket to dominating the cardiovascular space.

But, J&J's not content with just hearts; they're setting their sights on robot-assisted surgery with their new Ottava device.

Sure, they might be playing catch-up to Intuitive Surgical (ISRG), but think about it: barely any surgeries use robots right now. This market has potential written all over it

Of course, it's not all sunshine and roses in the land of Big Pharma. J&J's had its share of courtroom battles and regulatory headaches, just like any mega-corporation.

But they've weathered the storm, and their credit rating is better than Uncle Sam's. That shows a kind of resilience you just can't fake.

In today's volatile market, it's easy to get swept up in the hype of flashy, high-risk stocks – the hares of the investing world. But what if true wealth lies in the slow and steady pace of the tortoise?

In the pharma world, J&J is proof that slow and steady progress, unwavering reliability, and a continuous effort to innovate are the secrets to long-term success. They might not be the flashiest stock, but their steady march of growth and consistent dividends make them a quiet force in the pharma world.

So the next time you're tempted to chase the latest market fad, remember the pharma tortoise – and consider adding a reliable blue-chip like J&J to your portfolio. If you see a dip, don't hesitate, buy it.

Mad Hedge Biotech and Healthcare Letter

April 4, 2024

Fiat Lux

Featured Trade:

(A HIGH RISK, HIGH REWARD BIOTECH)

(VYGR), (SNY), (ABBV), (NBIX), (NVS), (AZN), (SGMO), (BIIB), (RHHBY), (IONS)

Voyager Therapeutics (VYGR) has put investors through the wringer. Since going public in 2015, their chips have swung wildly, from a high-rolling $30 down to a "you've got to be kidding me" $2.50. Why? Well, their early bet on curing neurological diseases hit some snags.

But, things seem to be turning around for them these days. Word on the street is Voyager's new Alzheimer's drug could be a total game-changer. If those clinical trials get the FDA's blessing, their stock could skyrocket from its current $9.30 to $22 a share.

Before anything else, let's take a stroll down memory lane.

Voyager started out with big dreams – using fancy gene therapies to tackle tough brain diseases like Parkinson's and Huntington's. Sadly, those early programs didn't quite deliver.

But hey, they caught the eye of some big pharma players. Sanofi (SNY) came knocking with a sweet deal – $100 million upfront and promises of up to $745 million if things worked out. Unfortunately, the science wasn't cooperating, and Sanofi bailed in 2019. Ouch.

Not to be discouraged, Voyager hooked another giant, AbbVie (ABBV), with a $1.2 billion deal for Alzheimer's and Parkinson's drugs. But then, more bad luck – their Parkinson's drug stumbled, and their Huntington's disease trials got put on hold. So, AbbVie decided to cut their losses in 2020. Double ouch.

And while the pandemic may have cured our boredom, it killed investor patience with unproven biotechs. Voyager's stock price cratered, leaving them worth about as much as a used napkin – barely more than their own $500 million cash pile.

But Voyager, bless their stubborn hearts, refused to become a biotech graveyard.

Despite having zero products actually making money, they have a secret weapon: their TRACER capsid tech. Think of it as a tiny Trojan Horse that can sneak drugs past that blood-brain barrier and deliver them directly to their target. Pretty impressive, right?

This tech, along with Voyager's brainpower, caught the eye of some pharma giants.

We're talking big names like Neurocrine Biosciences (NBIX), Novartis (NVS), AstraZeneca (AZN), and Sangamo (SGMO). If everything goes according to plan, these partnerships could be worth a whopping $8 billion. Now that's what I call a vote of confidence — or maybe just a collective case of gambling fever.

For Voyager, however, its biggest gamble is on Alzheimer's – and they're going all-in. Their star player is an antibody that tackles those nasty tau tangles that mess up brain cells.

Here’s a bit of context to understand why treatments for this are crucial.

Tau is like the scaffolding inside your neurons, keeping everything organized. But in Alzheimer's, that tau goes rogue, clumping into nasty tangles. Think of it like a giant hairball clogging up the brain's communication system. These tangles are called neurofibrillary tangles (NFTs) if you want to sound super smart.

This is something that Big Pharma like Biogen (BIIB), AbbVie, and Roche (RHHBY) are trying to target, too. But Voyager claims theirs is a precision weapon, zeroing in on just the bad stuff. If clinical trials prove that, their drug could blow the competition out of the water.

Plus, Voyager's got another trick up their sleeve: a gene therapy that hits the “off” switch on those tau tangles. They've shown it works in animals, and Biogen and Ionis (IONS) are already testing something similar in humans. But Voyager's got the edge – theirs is a one-time shot, so no more of those painful spinal taps.

That’s not all. Voyager is also tinkering with these new virus capsules that can sneak gene therapies straight into brain cells. And get this – they're even working on ways to ditch the viruses altogether and target nerves directly. Pretty cutting-edge stuff.

So, is Voyager a surefire win? Heck no.

Let's be realistic. It's going to be a while before Voyager actually makes money from these drugs. But there'll be exciting news along the way—science proving their ideas work.

Remember, the tricky thing with gene therapies is that everyone's chasing the same dream: how to get these treatments where they need to go quickly, cheaply, and safely. It's tough to predict who'll crack the code, even for the experts.

What's noteworthy about Voyager is that they keep reeling in those big pharma partners. Sure, the first two deals fizzled out, but not before Voyager pocketed a ton of cash. That kept them afloat, and now their stock's not such a dumpster fire.

But, let’s face it. Voyager's track record isn't exactly a parade of victories. Progress has been slow, and that's just the way it is in this industry.

If they pull off a miracle cure, they'll be worth billions, maybe tens of billions. Remember when Intellia Therapeutics (INTL) hit that $10 billion mark? That's the kind of payoff we're talkin' about.

Still, Voyager needs to deliver some serious wins, or those partners will vanish again. However, it’s worth considering that when a big player like Novartis, who knows this gene therapy game, partners up... that's gotta mean something, right? Even without results from human trials, it's a sign Voyager might be onto something big.

I know it's hard to justify investing in small biotechs with a losing streak, especially when they're tackling the toughest diseases out there. But after digging into Voyager, I can see its potential.

Worst case scenario? Their drugs flop. But that can happen to any biotech, even those with huge valuations and decades of trying.

As for Voyager, this biotech has been around the block. They've clearly got some promising science, and their stock is cheap. For me, that's enough to take a small position and see what happens.