Mad Hedge Biotech and Healthcare Letter

April 2, 2024

Fiat Lux

Featured Trade:

(BREATHE EASY)

(MRK), (JNJ)

Mad Hedge Biotech and Healthcare Letter

April 2, 2024

Fiat Lux

Featured Trade:

(BREATHE EASY)

(MRK), (JNJ)

It looks like Merck (MRK) just scored a major touchdown in the drug wars, which might make the looming Keytruda patent expiration sting a little less.

Remember when Merck dropped $11.5 billion on Acceleron back in 2021 to get their hands on Winrevair (then known as Sotatercept)? That was a seriously gutsy move to soften the blow when their Keytruda goldmine started drying up.

Talk about a gamble. Acceleron didn't even have their Phase 3 trial results in hand yet. A lot of people were scratching their heads at the time, thinking maybe Merck had lost their marbles.

But fast-forward to today, those Phase 3 results drop, and here we are. Turns out Merck knows a thing or two about playing the long game.

Their new drug, Winrevair, which just got the FDA thumbs up for a rare heart condition, tackles a serious heart condition called pulmonary arterial hypertension (PAH).

PAH is no joke – it basically strangles your lungs and heart, drastically shortening your lifespan. Unlike those old PAH drugs like Uptravi from Johnson & Johnson (JNJ), Winrevair's got a completely different way of fighting back. That could be huge for patients who aren't getting enough relief with current options.

Winrevair targets that messed-up TGF-beta pathway, trying to reverse some of the damage caused by this disease.

Although PAH might be rare, affecting an estimated 15 to 50 people per million in the United States and Europe, those who suffer from it are often desperate for effective treatments.

The global PAH market is already worth a staggering $7.3 billion annually and is projected to hit $12.18 billion by 2032.

Merck's timing couldn't be better. Not only did Winrevair sail through approval, but it also dodged all those nasty black box warnings and extra safety hoops some drugs have to jump through.

Translation: this drug is about to hit the market full speed ahead.

Given the promise of this new drug, Merck must be popping champagne corks right about now. No restrictions mean doctors can prescribe this stuff far and wide – that's a probable goldmine, especially for a serious disease like PAH.

Let's not forget why all this matters. Keytruda was a $25 billion cash cow for Merck in 2023, making up a huge chunk of their revenue. Those cheap knock-offs are coming in 2028, ready to eat into that sweet slice of the pie.

But thanks to Wenrevair, that future doesn’t seem too daunting anymore.

Merck has set a price of $14,000 per vial for Winrevair, translating to an average annual cost of $212,000 per patient. While this may seem steep, it reflects the drug's potential to improve the lives of PAH sufferers and secure Merck's financial future.

Actually, analysts are predicting peak sales of a mind-boggling $11 billion – maybe even $8 billion at the low end. Either way, that's a massive lifeline for Merck as they brace for the dreaded Keytruda patent cliff in 2028.

In fact, Winrevair could pull in $500 million this year alone, jumping to $3 billion by 2027. Talk about a growth spurt.

With Winrevair set to change the PAH treatment landscape, investors can breathe easy knowing that Merck has a new ace up its sleeve.

After all, this drug is practically guaranteed to be another blockbuster, which is great news considering the looming Keytruda patent expiration in 2028.

Merck's audacious $11 billion bet on Acceleron seems to be paying off – Winrevair could easily bring in $30 billion over its lifespan.

But let's not get too carried away – Winrevair won't single-handedly save Merck in the long run. They'll need more hits to keep outperforming the competition.

For now, Merck seems like a decent hold. It's got reasonable growth potential, and you might even want to nab some shares if the price dips.

Mad Hedge Biotech and Healthcare Letter

March 28, 2024

Fiat Lux

Featured Trade:

(WALL STREET'S NEW HAPPY PILL)

(JNJ), (SEEL), (NUMI), (AITAI)

Who would've thought a drug that was once the go-to for keeping soldiers from feeling their limbs getting stitched up in 'Nam would find itself in the limelight, decades later, for something entirely different?

And who's the reason behind this resurgence? None other than Mr. Elon Musk, alongside memories of Matthew Perry, and a growing chorus of folks battling the blues.

Musk, in one of his late-night (or is it early morning?) tweet-a-thons and in a recent interview with Don Lemon, drops that he's dabbling in ketamine — not for kicks, but for a "negative chemical state," doctor's orders, of course. Once every couple of weeks, a small dose.

This coming from a guy who's brainstorming how to send us to Mars while running a social media circus.

Now, before we dive deeper, here's a quick primer on ketamine.

Born in the labs of Parke Davis in the 60s and tested on unsuspecting prisoners (yikes), it was the anesthetic dream.

By 1970, ketamine earns the FDA's gold star as a trusty anesthetic. But here's where it gets interesting – patients start raving about feeling surprisingly chipper after surgery. Scientists, naturally, get that “wait a minute, that's not supposed to happen” look on their faces.

By the time the 90s rolled in, scientists had discovered that this battleground drug might be a secret weapon against depression.

All those positive patient reports sparked a firestorm of studies, and suddenly ketamine's the underdog superhero taking on treatment-resistant depression, PTSD, and more.

Fast forward to 2019, and the FDA green-lights a derivative, esketamine, delivered via nasal spray, marking a new era in the treatment of severe depression.

Interestingly, despite esketamine’s presence in the market, doctors are still heavily prescribing the original stuff. Why?

Because it works, undeniably so, and those prescriptions are through the roof – up fivefold since 2017.

Actually, despite being a bit player compared to the heavyweight category of cancer research, mental health is a quietly exploding segment.

In fact, the market for ketamine's mental health revolution is massive, and that's not just feel-good talk. We're looking at over 264 million people globally battling depression alone.

Add to that the millions more struggling with PTSD, OCD, and a growing list of treatment-resistant conditions – it's a staggering potential patient base.

With mental health taking center stage these days, analysts predict the ketamine market could explode to $1.05 billion by 2027. That translates to a CAGR of 16.5% from 2020 – not just growth, but a serious acceleration.

Naturally, this has companies salivating. Big pharma like Johnson & Johnson (JNJ) is in the game – their Spravato spray raked in $164 million in 2020, and that was just their opening act.

But the real excitement is with the innovators: companies like Seelos Therapeutics (SEEL), with their focus on new delivery methods, Numinus Wellness (NUMI) building out a whole network of ketamine-assisted therapy clinics, and ATAI Life Sciences (ATAI) betting big on psychedelic-focused research.

So, are you seeing those dollar signs flashing yet? Because with ketamine, there might just be some serious gold to be found.

Sure, J&J's pulling in the cash, but that's just the tip of the iceberg. The companies blazing the trails – tweaking formulas, reimagining delivery methods, building whole new treatment models – those are the ones with that “make it big” potential.

Still, it’s important to be realistic here. After all, biotech investing is a rollercoaster, not a Sunday stroll. We're talking FDA approvals, trial setbacks, the whole wild ride.

Ketamine, with its trippy backstory and game-changing possibilities, is the embodiment of that risk-reward gamble. Its story is about second chances, unexpected breakthroughs, and pushing the limits of what we thought possible for mental health. And yeah, it's also about those sweet, sweet returns for investors willing to take that leap.

So here's my suggestion: throw this drug, and the companies pushing the envelope with it, straight onto your watchlist. Keep tabs on the clinical trials, the news about those new delivery methods, the regulatory updates.

This space is just getting warmed up, and you don't want to miss the boat when things start taking off. Ketamine might have started out in the shadows, but its future? Well, that could shine pretty bright.

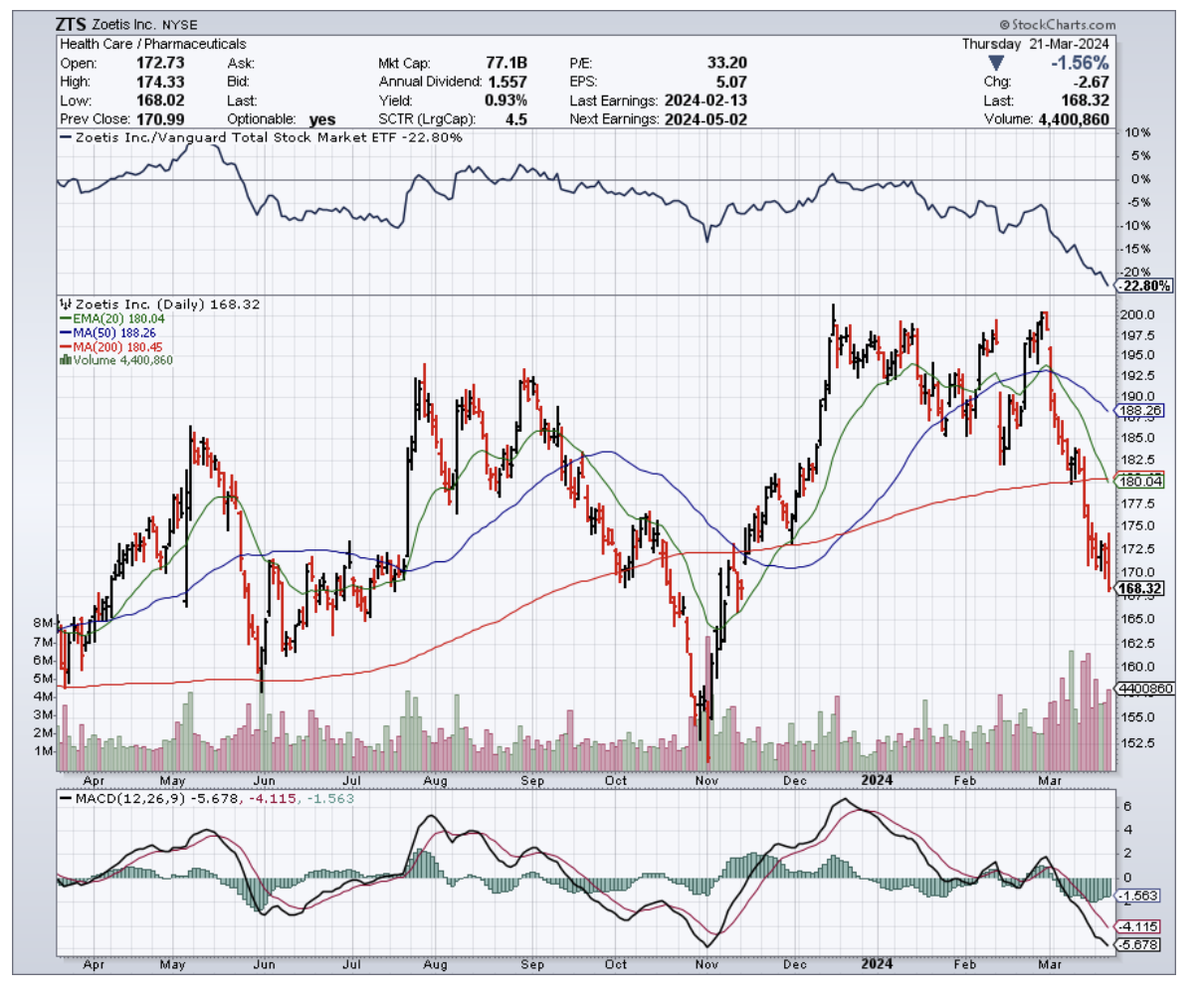

Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE TOP DOG IN ANIMAL HEALTHCARE)

(ZTS), (AMGN), (PFE), (JNJ), (ELAN)

You've likely witnessed a scene like this: You're at the park, and you see a young couple playing fetch with their golden retriever.

The dog is absolutely loving life, jumping and bounding after the ball, tail wagging furiously. It's a heartwarming scene, and it's one that's becoming more and more common these days.

In fact, just the other day, over coffee, a veterinarian buddy of mine spilled the beans.

"You wouldn't believe how people are pampering their pets these days," she said, shaking her head in amusement. "It's no longer just about the basics—food and health. Nope, we're talking top-tier, VIP treatment. They're ready to drop serious cash to ensure their furry friends are living their best lives."

It's a whole new world for pets, and their owners are leading the charge, wallets wide open.

And that is where Zoetis (ZTS) comes in. This company is the top dog (pun intended) in the animal healthcare space, and it's been making some serious waves in the market lately.

Now, I know what you're thinking - "What about those big-shot human healthcare stocks like Amgen (AMGN), Johnson & Johnson (JNJ), and Pfizer (PFE)?"

Well, let me tell you, Zoetis has been giving them a run for their money since spinning off from Pfizer back in 2013. This company has been posting positive annual EPS growth every single year, with an average annual EPS growth rate of a whopping 15.9%.

But that's not all — Zoetis has also been dishing out some seriously impressive dividend growth, with a CAGR of nearly 25% since it was spun off. That's right, this stock is checking all the boxes for dividend growth investors.

And if you think this is just an income play, think again.

Zoetis has been absolutely crushing the S&P 500, posting price returns of 492% compared to the market's measly 176% gains over the last decade.

So, what's the secret behind Zoetis' success?

Well, it all comes down to our furry (and sometimes scaly) friends. You see, people are lonelier than ever these days, and they're turning to pets for that much-needed companionship.

The US Surgeon General even called loneliness an epidemic, sounding the alarm on its dire impacts on health, likening its risks to smoking up to 15 cigarettes a day.

From the gripping claws of loneliness among young adults to the isolation felt by mothers with young children, the pandemic has only deepened this crisis, affecting a staggering 36% of Americans.

More than that, this loneliness trend isn't just about having a buddy to binge-watch Netflix (NFLX) with. It's actually impacting our species' survival. Studies show that sexual activity is on the decline, and technology is distorting the way we interact with each other.

It's a bit of a downer, I know, but here's where Zoetis shines through. As people turn to pets for love and affection, they're also shelling out some serious cash to keep their furry friends healthy and happy.

The American Pet Products Association says that nearly 87 million U.S. households own pets (roughly 66%), and it's not just the younger generations who are getting in on the action. Baby Boomers and Gen Xers are also big-time pet owners.

What does all this pet love mean for the industry? Well, the pet industry is expected to be a $150 billion behemoth in 2024.

Now, what really sets Zoetis apart from the pack? It all comes down to pricing power and growth potential.

In the animal health market, drug prices aren't determined by pesky regulations, government buyers, or PBMs. That means Zoetis can charge premium prices for their trusted, name-brand drugs without having to jump through hoops.

Plus, with less competition in the animal health space, Zoetis' products have longer growth runways and aren't constantly battling generic copycats.

For context, Elanco (ELAN), Zoetis' pure-play competitor, only managed to bring in $4.4 billion in sales.

So, what's the bottom line here?

Zoetis is a best-in-breed play on the booming animal healthcare market, with a safe and growing dividend to boot. As this sell-off continues, Zoetis keeps climbing higher on my personal watch list. I'm ready to back up the truck and load up on shares come April when I put my March dividends to work.

If you're looking for a unique way to play the healthcare space with a company that's got plenty of bark and bite, Zoetis might just be the stock for you.

Mad Hedge Biotech and Healthcare Letter

March 21, 2024

Fiat Lux

Featured Trade:

(THE COMEBACK STORY WE'RE ALL HERE FOR)

(PFE), (GSK), (LON)

Well, well, well. Pfizer (PFE) has been on a bit of a wild ride lately, hasn't it? Its shares have taken a nosedive, dropping over 50% since the company’s glory days in late 2021.

But before you start yelling "timber!" and running for cover, hear me out. I have a hunch that Pfizer's still got a few tricks up its sleeve that might just turn this ship around.

First off, let's talk about the elephant in the room: Pfizer's been playing a little corporate cost-saving efforts with its recent dealings with Haleon (LON), aka the Advil folks.

Remember when Pfizer and GlaxoSmithKline (GSK) decided to spin off their consumer health bits into Haleon back in 2022?

Well, now Pfizer's looking to offload a chunk of those Haleon shares for a cool $3 billion. That would take their stake from a whopping 32% to a more manageable 24%.

And as for GSK? This British biopharma is doing the same, slimming down to just 4.2%. It's like a corporate weight loss challenge, and both are ready to get lean and mean.

That's not all though. Pfizer has been on a shopping spree, dropping a jaw-dropping $43 billion on Seagen, a rising star in the cancer game.

Admittedly, this is a bold move. But, Pfizer's betting big that Seagen's going to be the game-changer they need.

And with Seagen's lymphoma drug, Adcetris, already knocking it out of the park for certain cancer patients, it might just be a bet that pays off big time.

Now, let's talk strategy. Pfizer execs recently revealed that the company would be all about innovation and pinching pennies this year.

Post-Seagen acquisition, they're laser-focused on making oncology the star of the show while also hunting down a whopping $4 billion in savings in 2024.

It's like they're trimming the fat to build some serious financial muscle, even as they brace for some of their cash cows to start slowing down.

Now, I know what you might be thinking. "But what about that Super Bowl ad? How does that fit into Pfizer's grand plan?" Honestly, I'm not entirely sure.

But what I do know is that Pfizer's oncology game is looking stronger than ever. With the FDA giving the green light for one of their leukemia treatments, Besponsa, for the kids, it's clear that Pfizer's cancer-fighting future is as bright as Times Square on New Year's Eve.

Still, Pfizer's not just relying on cost-cutting and its Seagen acquisition to weather the storm. They've got a pipeline bursting with potential, with 31 projects in phase 3 alone, which is corporate-speak for "almost ready to blow your socks off."

That's like having 31 lottery tickets, and you've got to believe that at least a few of them are going to hit the jackpot.

And with new stars like Padcev from the Seagen deal and their shiny RSV vaccine Abrysvo hitting the market, the sales needle is looking to jump up, not down.

I've been singing Pfizer's praises for a while now, and I still stand by that. Sure, their stocks have taken a hit, but that doesn't mean the fat lady's singing just yet.

If anything, it's just the intermission before the big finale. Pfizer's gearing up for a second act that's going to have us all on the edge of our seats, popcorn in hand, ready for the comeback of the century.

So, what's the bottom line here? Well, I think Pfizer's playing the long game. With a dividend yield that's like finding a twenty in your old coat pocket, they're saying, "Stick with us, we've got plans." And from where I'm sitting, those plans look pretty darn good.

Mad Hedge Biotech and Healthcare Letter

March 19, 2024

Fiat Lux

Featured Trade:

(NOT JUST A ONE-TRICK PONY, BUT A BIOTECH THOROUGHBRED)

(LLY), (NVO), (PFE), (AMGN)

I've been around the block a few times when it comes to investing, and let me tell you, I know a thing or two about spotting a winner. And right now, there's one name in the biotechnology and healthcare world that's caught my eye like a shiny new penny: Eli Lilly (LLY).

First off, let's talk about Lilly's recent partnership with Amazon Pharmacy (AMZN). This pair is bringing the future to us, offering direct home delivery of Lilly's medications, including the much-talked-about weight-loss drug Zepbound.

You heard that right. Thanks to this partnership, you can now get your hands on Lilly's weight-loss wonder drug, Zepbound, without ever leaving your couch.

Approved last year for obesity treatment, Zepbound is shaping up to be a blockbuster. And let's not forget about LillyDirect, the platform making all this possible, blending healthcare provision with top-notch delivery service.

Since launching in 2020, Amazon Pharmacy has been on a mission to simplify how we get our prescriptions, and teaming up with Eli Lilly only turbocharges this mission.

Now, let's talk about Lilly’s financials. This biotech’s market cap has ballooned to an eye-watering $700 billion, thanks to a 130% surge over the past year.

The buzz around Zepbound, showing potential for a 27% reduction in body weight, has investors sitting up and taking notice.

But I hear you ask, "Have I missed the boat on Eli Lilly?" My take? Not at all.

In fact, I think this stock could easily double in value and even surpass the trillion-dollar mark within the next five years. It's a bold prediction, but I've been around long enough to know a sure thing when I see it.

With obesity rates tripling since 1975 and more than half of the global population predicted to become obese or overweight by 2035, the demand for effective treatments like these is going to skyrocket.

Actually, the market for weight loss treatments is projected to reach $100 billion by 2030. And Lilly? They're ready to ride that wave all the way to the bank.

To date, Lilly only has one strong competitor in this space: Novo Nordisk (NVO). While other pharma giants, like Pfizer (PFE) and Amgen (AMGN), are trying their best to gain traction, these two are leaps and bounds ahead.

Now, I know what you might be thinking. "Isn't it expensive to develop these cutting-edge treatments?" You bet your bottom dollar it is.

Lilly isn't afraid to put its money where its mouth is. They're investing heavily in manufacturing capacity to keep up with the inevitable surge in demand. It's a bold move, but that's what separates the winners from the also-rans in the biotech race.

That’s not where it ends though. Lilly has another ace up its sleeve: donanemab, their early Alzheimer's treatment. This could also be a potential competitor of Biogen (BIIB) and Tokyo’s Eisai’s (ESALY) lecanemab, currently marketed as Leqembi.

Sure, the FDA might have put a temporary hold on Lilly’s candidate’s approval, but I've seen this rodeo before. It's just a minor bump in the road for this potentially game-changing drug.

If donanemab gets the green light, it could add billions more to Lilly's already impressive revenue streams. For perspective, the market for Alzheimer’s treatments is predicted to reach $6 billion to $8 billion by 2025 and record $15.5 billion by 2031.

Of course, no investment is without risk. But when I look at Eli Lilly, I see a company that's firing on all cylinders.

They're making strategic partnerships, investing boldly in their future, and have a track record of success that's the envy of the industry.

With a pipeline full of promising treatments, I believe Lilly is poised to gallop its way to even greater heights in the years to come.

So if you're looking for a biotech thoroughbred with a pedigree of success and a bright future ahead, I'd say Lilly is a horse worth betting on.