Mad Hedge Biotech and Healthcare Letter

April 15, 2025

Fiat Lux

Featured Trade:

(THE WEIGHT OF EXPECTATIONS)

(LLY), (NVO)

Mad Hedge Biotech and Healthcare Letter

April 15, 2025

Fiat Lux

Featured Trade:

(THE WEIGHT OF EXPECTATIONS)

(LLY), (NVO)

You know that feeling when you've found the perfect restaurant? The food is exquisite, the atmosphere divine, and then you get the bill—and suddenly you're calculating if selling a kidney is a viable financial strategy.

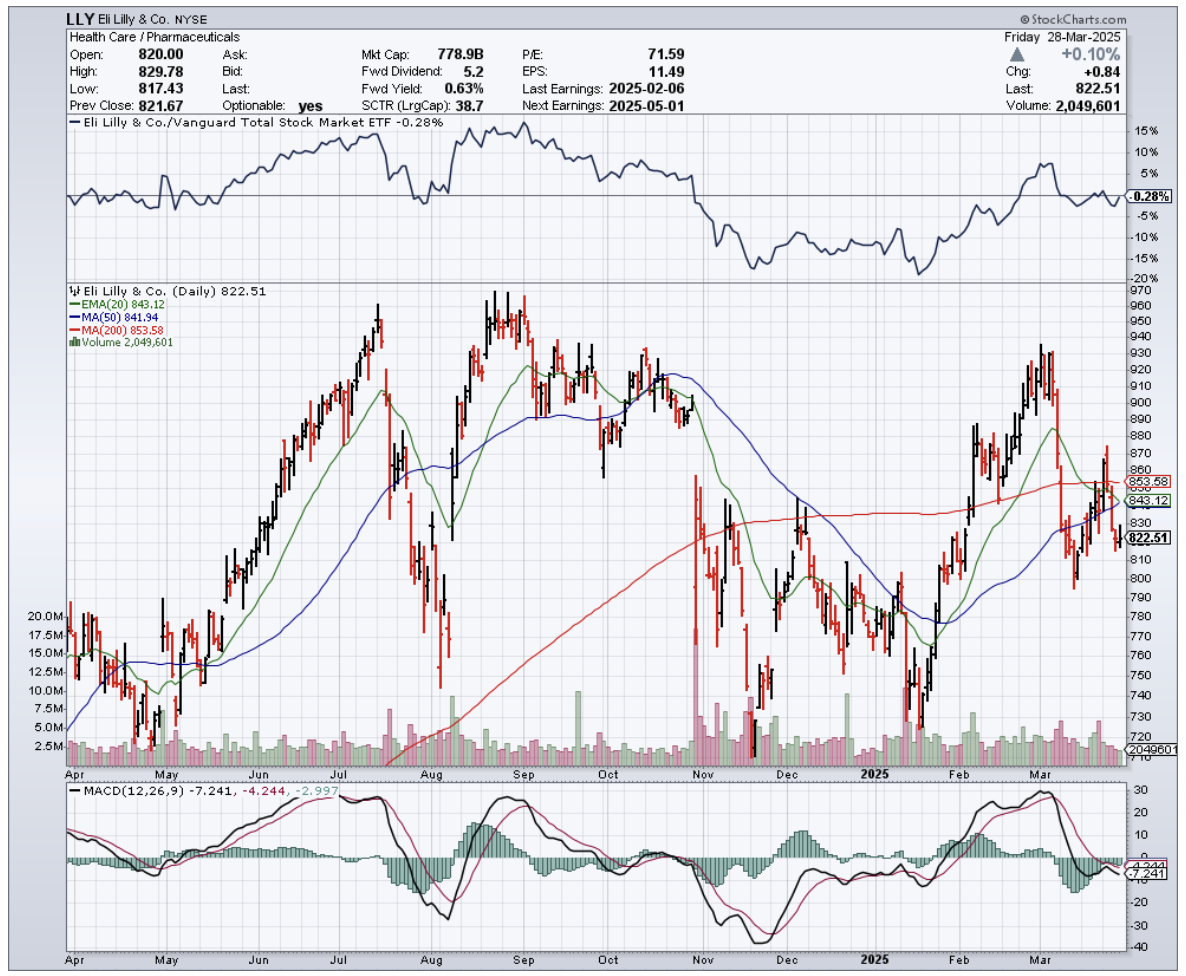

That's essentially my relationship with Eli Lilly (LLY) right now. Phenomenal company, stellar performance, price tag that makes my wallet weep.

I've had a complicated romance with this pharmaceutical juggernaut. Back in my hedge fund days, I learned that timing is everything with pharma stocks. It's like catching the perfect wave off Malibu – ride it too early, you're just splashing in the shallows; too late, and you're eating sand.

When I first spotted Lilly in June 2023, it was set up beautifully. Shares rocketed 56.2% before I downgraded to a 'hold' last February, while the broader market trudged along with a mere 12.3% gain.

Since then, the stock has performed almost exactly as predicted—just a 0.2% gain compared to the S&P 500's 1.33%. More recently, it's dropped 6.9% since January, looking positively rosy next to the broader market's 12.2% decline.

The company's fourth-quarter results read like a biotech investor's fantasy novel. Revenue soared 44.7% year-over-year to $13.53 billion, driven by its dynamic weight-loss duo.

Mounjaro's sales jumped 60.1% to $3.53 billion, while Zepbound exploded from $175.8 million to a jaw-dropping $1.91 billion.

I've watched patients in clinical trials shed substantial weight on these medications—one of my research contacts dropped 43.4 pounds since starting treatment—and I can tell you these drugs are creating waves not just in waistlines but across the entire healthcare sector.

Other stars in Lilly's portfolio include Verzenio for breast cancer (up to $1.56 billion from $1.15 billion), Jardiance for diabetes (climbing to $1.20 billion), and solid gains from Taltz and Humalog.

Only Trulicity disappointed, watching its revenue tumble from $1.67 billion to $1.25 billion—predictably cannibalized by Lilly's newer weight-loss offerings. It's like watching your reliable sedan gathering dust after buying a Tesla.

With this revenue bonanza, profits naturally skyrocketed. Net income more than doubled to $4.41 billion, adjusted profits surged to $4.81 billion, and operating cash flow swung from negative $311.9 million to positive $2.47 billion.

In my decades of following pharmaceutical stocks from Tokyo to Wall Street, I've rarely seen a quarterly performance this impressive. If Lilly were a student, it would be the annoying one breaking the curve for everyone else.

Looking ahead, management projects 2025 revenue between $58-61 billion (a 32.1% increase at midpoint) and adjusted EPS between $22.50-24.

For the upcoming Q1 report on May 1st, analysts anticipate revenue of $12.77 billion (45.6% higher year-over-year) and EPS of $4.70 (nearly double last year's $2.48).

So with all this financial wizardry, why maintain a 'hold'? One word: valuation.

Even using 2025's projected figures, Lilly trades at eye-watering multiples: forward P/E of 33.3, price-to-cash-flow of 27.6, and EV/EBITDA of 21.2.

For context, pharmaceutical peers trade significantly lower. Novo Nordisk (NVO), perhaps the most comparable given its similar weight-loss market success, trades at a P/E of 19.0, price-to-cash-flow of 15.9, and EV/EBITDA of 14.6.

It's like comparing Manhattan real estate to Cleveland—both might be perfectly fine places to live, but one demands a significant premium.

Don't mistake my caution for bearishness. Lilly's product pipeline is robust, highlighted by Retatrutide, which has shown even more impressive weight-loss results—patients lost an average of 24.2% of their body weight (58 pounds) in clinical trials.

The company is also expanding its manufacturing footprint with four new US sites, creating 3,000 permanent jobs. It's acquiring promising treatments like Scorpion Therapeutics' STX-478 for $2.5 billion upfront.

Meanwhile, shareholders enjoyed $4.7 billion in dividends and $2.5 billion in buybacks last year, with a new $15 billion repurchase program and a 15% dividend increase announced for 2025.

I'd compare Lilly's stock to its own weight-loss drugs: remarkably effective, potentially life-changing, but priced at a level that makes you question whether the benefits justify the cost.

If May's results blast past expectations with raised guidance, I'll happily reconsider. Until then, I'm maintaining my 'hold'—admiring from across the room, but not ready to propose just yet.

Mad Hedge Biotech and Healthcare Letter

April 10, 2025

Fiat Lux

Featured Trade:

(THE $5 BILLION SECRET I SPOTTED IN MY DOCTOR'S WAITING ROOM)

(AMGN), (NVO), (LLY), (MRK), (REGN)

Last Tuesday, my orthopedist kept me waiting 40 minutes past my appointment time – just long enough for me to witness what Wall Street's finest analysts have somehow managed to miss.

As I sat thumbing through a dog-eared copy of Golf Digest from 2018, I counted eight different patients called in for Prolia injections.

By the sixth one, I'd put down the magazine and started taking notes on my phone. By the eighth, I was already mentally calculating position sizes for my portfolio.

"You know what you just saw?" my doctor asked when he finally saw me. "That's Amgen's cash cow – $5.4 billion in sales last year for a twice-yearly injection. And guess what? Half these patients will be on it for life."

When I pressed him on competing drugs, he just laughed. "Their sales reps bring the best lunches. But seriously, it works, patients tolerate it, and insurance covers it. In medicine, that's the holy trinity."

While half of Wall Street hyperventilates about which pharmaceutical giant will dominate the weight loss market, and the other half chases whatever shiny tech story came out this morning, they're all missing Amgen (AMGN) – a money-printing machine trading at just 14.9 times earnings with a 3.1% dividend that grows like clockwork.

I've been investing in pharmaceutical companies since I covered Merck's (MRK) explosive growth for The Economist in the late 1970s, and one lesson has remained constant: the market consistently underestimates companies with proven track records during transitions.

Amgen, trading at $307, is a textbook example of this phenomenon right now.

The headline numbers don't initially spark excitement – management is guiding for modest 5% revenue growth and 4% EPS growth this year. But having analyzed hundreds of pharma companies over five decades, I know these conservative guidance figures are often the prelude to significant outperformance.

What matters more is their $5.9 billion R&D investment last year (up 25% from 2023) and the underappreciated potential of their pipeline.

Look beyond the surface, and you'll find Amgen has quietly built something remarkable. While everyone's fixated on Novo Nordisk’s (NVO) Ozempic and Wegovy, few have noticed that Amgen's existing product portfolio is delivering solid results.

Inflammation drug TEZSPIRE grew 71% year-over-year and is approaching the $1 billion annual sales milestone. Oncology drug BLINCYTO jumped 41%, and their cholesterol drug Repatha, combined with bone health treatment EVENITY, delivered $1 billion in year-over-year growth.

The real hidden value lies in Amgen's obesity program. The anti-obesity market that barely existed a few years ago has exploded to $2.2 billion and is projected to grow at 30% annually through 2030.

Eli Lilly (LLY) and Novo Nordisk have seen their market caps soar into the stratosphere on the strength of their GLP-1 drugs, but Amgen's market valuation doesn't reflect any meaningful potential from MariTide, their Phase 3 obesity candidate.

This reminds me of 2012 when I began accumulating Regeneron (REGN) while the market was completely missing the potential of Eylea. That position delivered a 580% return over the following three years.

What's particularly attractive about Amgen is the margin of safety it offers. With a 3.1% dividend yield (backed by a manageable 45% payout ratio and 13 consecutive years of growth), a forward P/E of just 14.9, and a fortress-like 46.3% operating margin, you're being paid to wait for the pipeline to deliver.

The company has been aggressively paying down the debt from its Horizon Therapeutics acquisition, reducing long-term obligations by $6.6 billion last year alone.

Their financial discipline stands in stark contrast to many of the speculative biotech plays I've been pitched recently. At a dinner with venture capitalists in Boston last week, I listened to presentation after presentation about pre-clinical assets with billion-dollar valuations and no revenue in sight.

Meanwhile, Amgen generated $33.4 billion in sales last year with industry-leading EBITDA margins of 45%.

Of course, there are risks. The upcoming patent expiration of osteoporosis drug Prolia this year creates a revenue gap that needs filling.

The Trump administration's Department of Government Efficiency (DOGE) initiative could potentially impact FDA testing labs, slowing approval timelines. But these concerns are already priced into the stock, while the potential upside from MariTide and other late-stage candidates is not.

Having navigated multiple market cycles since the 1970s, I've learned that the best investments often come when solid companies are temporarily overlooked during market rotations. Amgen remains a proven pharmaceutical innovator with strong cash flows, growing dividends, and a promising pipeline that offers compelling value.

I started building a substantial position in Amgen at around $260 during the post-election pharmaceutical sell-off and have continued to accumulate shares on weakness.

With a reasonable valuation, strong pipeline optionality, and dividend income that beats 10-year Treasury yields, Amgen represents the kind of steady compounder that has consistently outperformed over full market cycles.

In my decades of investing, I've found that buying excellent businesses during periods of unwarranted pessimism is the closest thing to a guaranteed winning formula.

With Amgen, you're essentially being paid a 3.1% annual dividend to own a company that could deliver a major surprise in the obesity market – the same market that transformed Novo Nordisk and Eli Lilly into two of the world's most valuable companies.

Sometimes the smartest investments are like colonoscopies – nobody's excited to talk about them at parties, but they'll save your financial health in the long run.

Mad Hedge Biotech and Healthcare Letter

April 8, 2025

Fiat Lux

Featured Trade:

(YOUR ALL-WEATHER HEALTHCARE FORTRESS)

(CI)

I've stared down bears in Yellowstone, MiGs over Moscow, and market crashes that would make your financial advisor need therapy. But nothing gets my pulse racing like finding a massively mispriced asset hiding in plain sight.

Ladies and gentlemen, I give you Cigna (CI) – the financial equivalent of discovering an abandoned Ferrari with the keys still in the ignition.

Two nights ago, at a private dinner with three healthcare CEOs, I heard something that confirmed what my models have been screaming for months: Cigna isn't just surviving healthcare's perfect storm – it's secretly thriving in it.

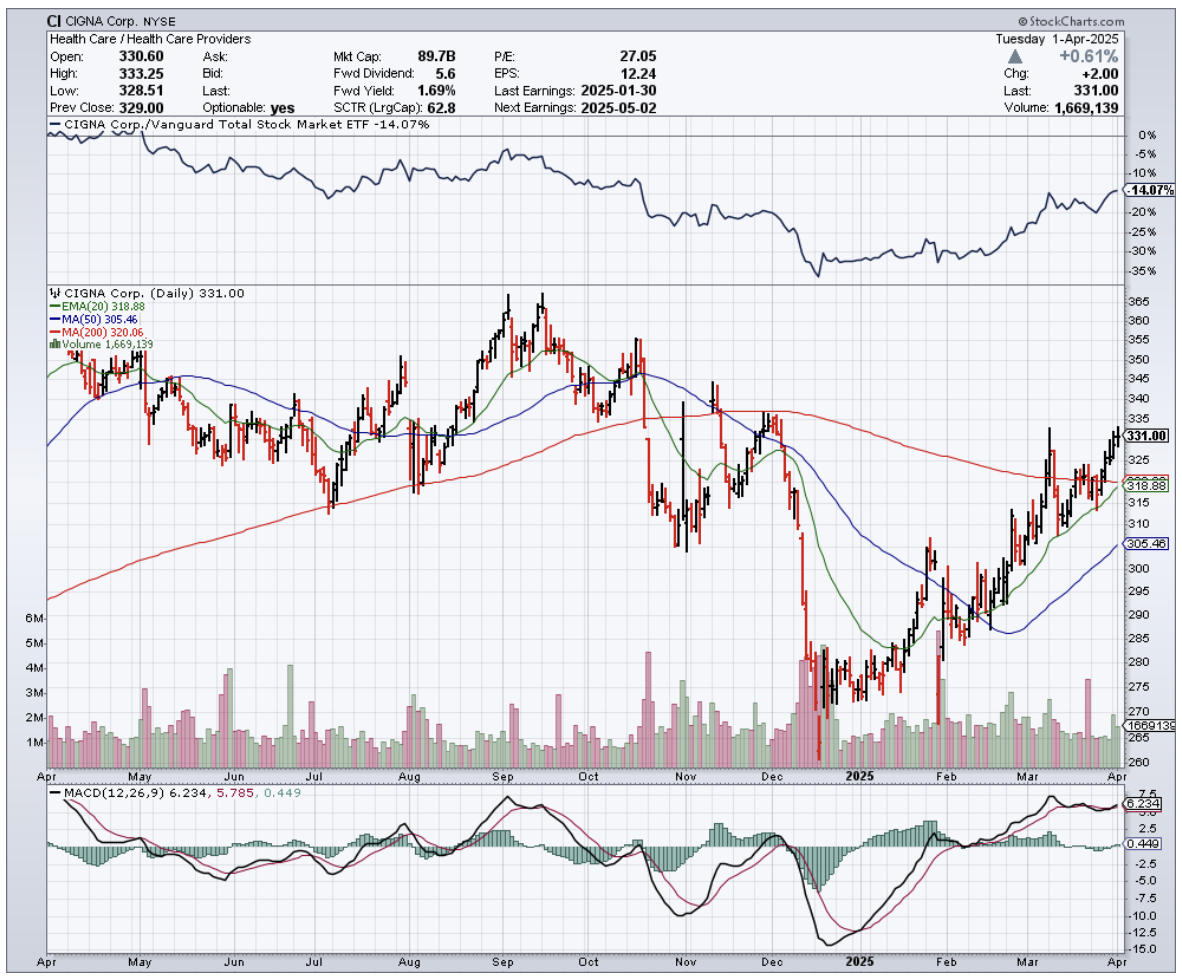

At $331 per share, we're looking at a rare beast: a value play with growth-stock upside.

I've spent enough time hanging around hospital C-suites to know when something smells like money.

Healthcare has been absolutely battered these past couple of years – staffing shortages, skyrocketing utilization rates, and the mother of all pandemic hangovers. Yet here's Cigna, delivering 8-9% year-over-year earnings growth.

What really gets my investment juices flowing is watching Cigna’s strategy play out beautifully. In fact, they just closed their Medicare business sale to HCSC in Q1, a move so smart it makes me want to applaud slowly from across the room.

I was having dinner with Medicare Advantage executives last month, and these folks were practically in tears over reimbursement rates. "It's like trying to run a restaurant where customers expect filet mignon but only want to pay for ground beef," one said, nursing his third scotch.

By reducing Medicare exposure, Cigna is saying, "We'd rather control our destiny than beg government bureaucrats for pennies." Companies that pivot away from heavily regulated, margin-compressed businesses typically emerge looking like they've been on a financial fitness program.

Here's the cherry on top – practically all proceeds from the Medicare divestiture are funding stock buybacks.

Cigna already has a track record of reducing share count that would make other CEOs jealous. One of my former students who now runs healthcare equity research at a bulge bracket bank messaged me privately that his team is dramatically underestimating the EPS impact – like forecasting a drizzle when there's a monsoon coming.

As both an insurer and pharmacy benefits manager, Cigna occupies rarefied air. Their ability to steer members toward lower-cost biosimilars isn't just smart business – it's practically printing money.

During my last Mad Hedge Fund Trader conference, I arranged a private tour of Cigna's specialty pharmacy operations for some of our Concierge members, and what I saw confirmed my thesis: their integration of medical and pharmacy data gives them insights that would make McKinsey consultants salivate.

And can we talk about prior authorization? If you've dealt with health insurance, you know it's bureaucratic torture that makes the DMV seem like a day spa. Remarkably, Cigna is reducing these requirements.

A Cigna EVP I've known since our Harvard Business School days told me over golf that their internal data shows customer retention improving by double digits from these changes alone.

Let's get down to the numbers. Like I said earlier, even during healthcare's darkest days, Cigna delivered 8-9% EPS growth. Using that as my bear case and applying a conservative 3% terminal growth rate, we're looking at a fair value of $432.79 per share.

But if they execute on their 10-14% EPS growth strategy, the fair value jumps to $508.40. That's 33-53% upside from current levels – the kind of return profile that usually comes with significantly more risk.

In 40 years of trading everything from Japanese derivatives during the Nikkei bubble to Texas fracking plays, I've learned that when everyone panics about an industry, the smart money quietly pounces on the gems.

Cigna isn't just any healthcare company – it's the one with enough foresight to shed Medicare exposure right before what my Washington contacts warn will be a reimbursement bloodbath.

Mark my words: By this time next year, when I'm recounting this trade over sake in Tokyo, Cigna won't be our little secret anymore – and neither will the 33%+ returns sitting on the table right now.

Well, that's enough financial wisdom for one day. My trading screens are flashing, my yacht captain's texting, and somewhere in the Himalayas, a summit is wondering where I've been.

Mad Hedge Biotech and Healthcare Letter

April 3, 2025

Fiat Lux

Featured Trade:

(MIND THE GAP)

(DHR)

Last Thursday, I found myself trapped in an elevator with the former head of R&D at one of Boston's leading life sciences companies – a guy I've known since my Tokyo days in the late '70s.

After we established that neither of us knew how to hack the elevator controls (disappointing, since he has three engineering degrees from MIT), he leaned in and whispered, "You know what's crazy? Everyone's obsessing over AI stocks while Danaher is sitting there at nearly a 30% discount to historical valuations."

The elevator started moving before I could press him for details, but his comment sent me down a research rabbit hole that kept me up until 3 AM.

My old friend wasn't wrong. Danaher (DHR) has quietly become one of the most compelling value opportunities in the life sciences sector.

While lesser investors are chasing the latest semiconductor hype, DHR is trading at 26.9x forward earnings – a substantial discount to its five-year average multiple of 30.2x – all while positioning itself for what looks like a significant rebound in 2026.

I've been tracking Danaher since their earliest acquisition days in the late 1990s, and their current setup reminds me of late 2018 when they were preparing to acquire GE's biopharma business.

Back then, short-term concerns created a buying opportunity that delivered a 150% return over the next three years.

Today's discount stems from China's Volume-Based Procurement initiative and lower respiratory testing revenues at Cepheid – both temporary headwinds that mask the company's extraordinary long-term potential.

What most market participants are missing is that Danaher's core growth engine – its Biotechnology segment – is showing undeniable signs of life.

Their latest quarterly orders grew over 30% year-over-year, marking the sixth consecutive quarter of high single-digit sequential growth.

After two years of inventory destocking that felt like watching paint dry (if the paint cost $10,000 per gallon), the bioprocessing business has returned to positive growth territory.

The company's Life Sciences segment also turned positive last quarter, benefiting from Chinese stimulus funding that took longer than expected to materialize – sort of like waiting for your teenager to clean their room, but with billions of dollars at stake.

While Q1 will face tough year-over-year comparisons due to a large energy project last year, management expects growth to accelerate through 2025, culminating in a major Pall customer project in Q4.

Now, Danaher does face legitimate near-term challenges. Their Diagnostics segment is battling headwinds from China's VBP initiative, which accelerated unexpectedly in late 2024.

Management now estimates a $150 million impact for 2025 on top of the $50 million already absorbed in 2024. They've also guided for respiratory testing revenue to drop from $1.95 billion to $1.7 billion this year.

But here's where things get interesting. The flu season is turning out to be significantly more severe than anticipated – one of the worst in 15 years according to CDC data I reviewed yesterday.

This suggests management's respiratory testing guidance could prove conservative. Meanwhile, their non-respiratory portfolio is growing at mid-teens rates, with their women's health multiplex vaginitis panel increasing by over 20%.

What truly separates sophisticated investors from the herd is understanding that Danaher's management team rarely sits idle during challenging periods.

True to form, they've implemented a cost reduction program targeting at least $150 million in annual savings, focused specifically on offsetting the VBP impact in China and the Diagnostics segment.

This isn't their first rodeo with margin pressure – they've maintained their remarkable 30-year track record of operational improvement through far worse conditions.

The long-term growth thesis remains rock solid. The bioprocessing business is perfectly positioned to capitalize on biologics and biosimilar adoption as major patents expire in coming years.

According to management, there are approximately 600 FDA-approved biologics today with over 20,000 in the pipeline. Their Cytiva business supports over 90% of global monoclonal antibody manufacturing volumes – a stunning competitive position in one of healthcare's fastest-growing segments.

For perspective, it's like owning the only company that makes drill bits during a massive oil boom.

I've analyzed Danaher's forward P/E ratio across multiple market cycles, and the current valuation represents a compelling entry point for patient investors.

At 24x 2026 earnings estimates, the stock is pricing in virtually zero multiple expansion despite the company's historical premium to the market. The consensus expects EPS to grow from $7.66 in 2025 to $8.58 in 2026 – a 12% increase that looks conservative given the margin expansion potential as revenues recover.

I've started building a position at these levels, with plans to add on any further weakness. While timing the absolute bottom is a fool's errand (believe me, I've tried and have the investment scars to prove it), the current valuation provides a meaningful margin of safety.

I'm targeting a return to at least 28-30x forward earnings over the next 18-24 months as growth visibility improves, which would translate to approximately 25-30% upside from current levels.

As a veteran of both market crashes and faulty elevators, I've learned one crucial lesson: the key difference between being stuck in an elevator and stuck in an undervalued stock is that only one of them lets you press the “up” button when you've reached the bottom.

And if Danaher delivers as expected, I might just start hanging out in more broken elevators looking for my next investment idea.

Mad Hedge Biotech and Healthcare Letter

April 1, 2025

Fiat Lux

Featured Trade:

(HOW ONE SMUG DANE MADE ME EAT MY WORDS)

(NVO), (LLY), (ULIHF), (LXRX)

Back in 2008, I found myself in a private dining room at Copenhagen's Noma restaurant – then barely known outside culinary circles – seated next to a senior Novo Nordisk (NVO) executive who couldn't stop talking about their early-stage GLP-1 research.

"This will change diabetes treatment forever," he insisted between bites of moss and lichen. I nodded politely while thinking he'd had too much aquavit. Fast forward to today, and I've never been happier to have been dead wrong.

That same GLP-1 technology now powers Ozempic and Wegovy, creating a weight-loss revolution that's transformed both waistlines and balance sheets.

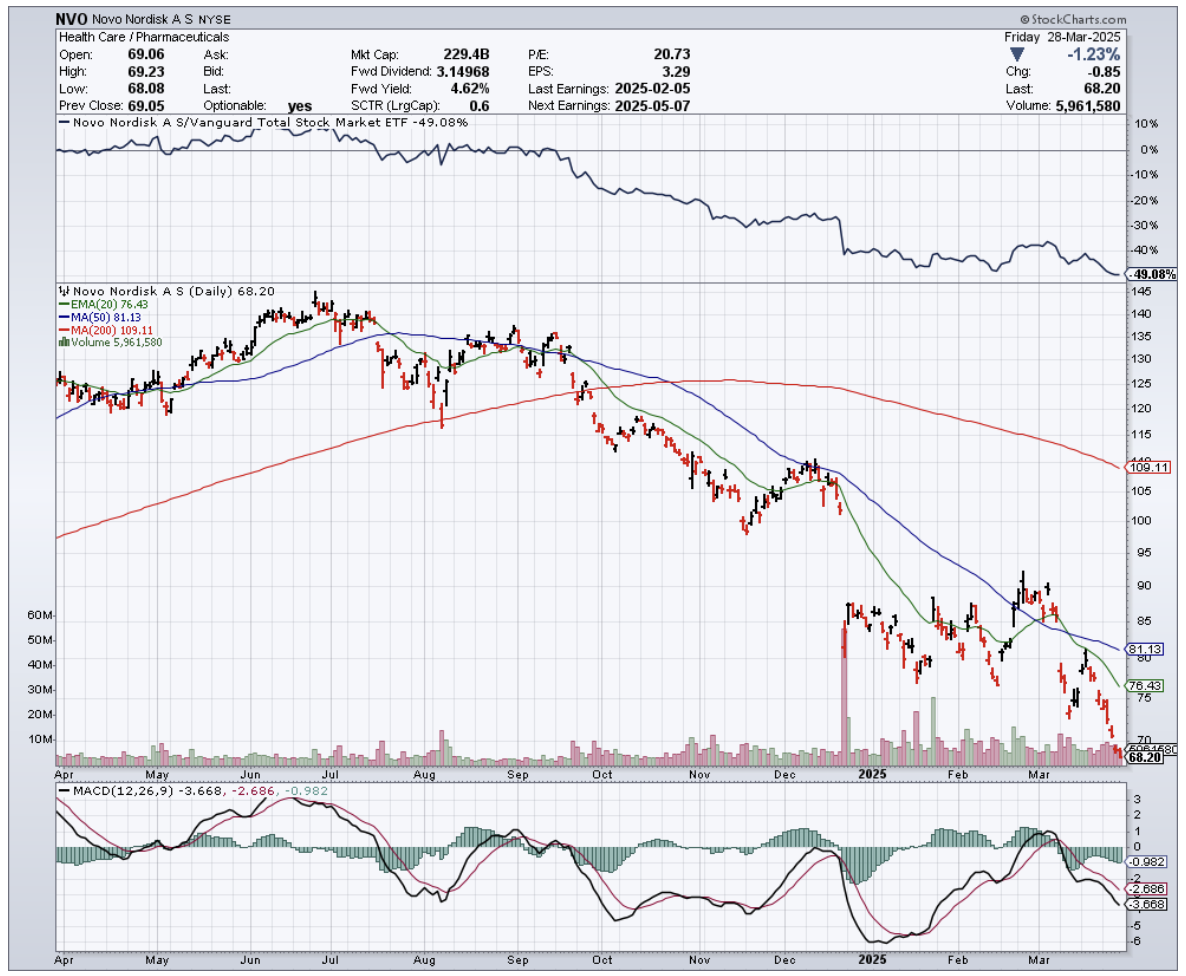

But here's what has me reaching for my trading account: Novo Nordisk's stock has somehow crashed 50% since last summer, creating what might be the buying opportunity of the decade in the pharmaceutical space.

Meanwhile, their American rival Eli Lilly (LLY) has remained relatively stable despite identical market challenges. Let's dissect this peculiar divergence.

The facts paint a compelling picture: Novo Nordisk remains the undisputed global leader in the GLP-1 segment with a commanding 55.1% market share.

Their quarterly revenue hit $11.95 billion, up 25.13% year-over-year – not quite matching Lilly's impressive 44.7% growth, but still exceptional by any standard.

What's particularly striking is the valuation disconnect. Novo now trades at just 17.9x forward earnings compared to Lilly's 35.4x multiple. That gives Novo a PEG ratio of 0.97 – catnip for value investors hunting growth at a reasonable price.

The Danish giant's financial position remains rock-solid with lower net debt ($10.6B vs. Lilly's $31B) and a superior debt/EBITDA ratio. Their EBIT margin stands at an impressive 48.2% versus Lilly's 38.9%.

The precipitous stock decline stems from two primary concerns: recent clinical trial results for their next-generation Cagrisema showed 22.7% weight loss versus their 25% target, and potential U.S. tariffs could pressure margins on European-manufactured drugs. Both fears seem drastically overblown.

For context, Novo's monthly RSI has dropped below 40 – a rare technical signal that has occurred only three times this century (2002, 2009, and 2016), with each instance preceding returns exceeding 500% before the next correction.

Historical patterns aren't guaranteed, but they certainly make me sit up straighter in my trading chair.

The company isn't standing still either. They've committed $4.1 billion to expand U.S. manufacturing facilities, reducing tariff exposure.

They've also signed deals worth up to $3 billion with United Laboratories (ULIHF) and Lexicon Pharmaceuticals (LXRX) to bolster their weight-loss drug pipeline, ensuring they remain competitive with Lilly's offerings.

Last month at a healthcare conference in Boston, I cornered a veteran endocrinologist who's been prescribing these medications since their approval.

"The competition between Lilly and Novo is creating better outcomes for patients," she told me. "But from a prescription perspective, we still reach for Novo's products first in most cases."

That kind of clinical preference creates a moat that's difficult to quantify on balance sheets but enormously valuable over the long term.

While Eli Lilly deserves its premium valuation with a more diversified therapeutic portfolio spanning oncology, immunology, and neurology, Novo's singular focus on diabetes and obesity has created unparalleled expertise in categories representing massive long-term growth markets.

The obesity treatment market alone is projected to grow at 22% annually, with GLP-1 drugs leading the charge. Approximately 25% of the world's population will be obese by 2035, and Western markets like the U.S. and Europe (Novo's primary territories) will see the highest rates.

Both companies will thrive in this expanding market, but at current prices, Novo represents a superior investment opportunity. Analyst consensus targets suggest 57% upside potential for Novo versus 23% for Lilly.

I've initiated a position in Novo Nordisk at these levels while maintaining a smaller holding in Lilly for diversification. After all, in pharma investing, sometimes the most profitable opportunities emerge when the market overreacts to short-term concerns.

As for that Danish executive from 2008? He retired to a villa overlooking the Øresund Strait last year. I sent him a congratulatory gift basket filled with moss and lichen – a reminder of where billion-dollar ideas sometimes begin.