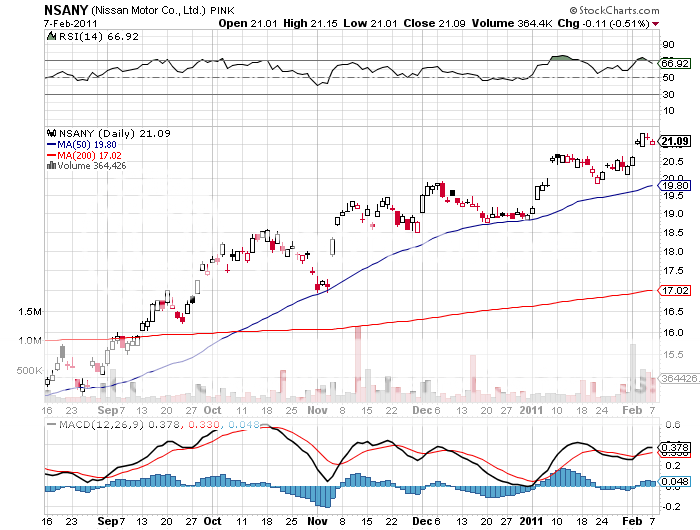

3) Getting Something for Nothing. I just contracted to buy all the gasoline I want at 14 cents a gallon. No, I have not struck oil in my backyard, or come into an inheritance from a long lost Kuwaiti relative. That is the de facto price that PG&E is billing me for a full charge on the all-electric Nissan Leaf that will be delivered to me in December.

That works out to $1.20 to recharge a vehicle that will transport me 100 miles, at the price of five cents a kilowatt hour. This is less than half the 11.8 cent/hour I pay to run the rest of my appliances, and a tiny fraction of the 40 cent/hour peak rate I pay to run the air conditioner in the summer.

PG&E has exactly one engineer to talk to its 10 million customers about this ground breaking new technology, and after much effort, I managed to get him on the phone. I asked who was paying the subsidy? Were those profligate bastards in Washington involved? He answered that there was no subsidy, that power sold at night was cheap because there was no other market.

So I inquired as to who was paying for all of the equipment upgrades, like the new transformers and power lines that were needed? Do I sense the heavy hand of Sacramento? He replied that there was no capital cost because the same infrastructure that delivered power to me during the day would be used to power my car at night. Only a couple of bucks would be spent on the installation of a new 'time of use meter'.

Of course, they have subsidized the hell out of the Leaf itself. The car that is costing me $22,000 here in California sells for $32,000 in Japan. I know we're supposed to be cutting the deficit by eliminating handouts like this. But you'll only take my subsidies by prying my cold dead hands away from them. Take someone else's subsidies, not mine! It is the American thing to do these days.

He did mention that one unanticipated problem had arisen. My ears perked up. Many wealthy Tesla Roadster owners in Los Altos Hills were impressing so many girlfriends with rides that they were requiring multiple daytime recharges, even though they promised to recharge only at night. Not only did this send their electricity bills through the roof, it was causing problems with the grid as well. I guess its all part of the teething process, a cost of making the great leap forward to the next generation. Who knew that Match.com would be involved?

I never thought I'd get something for nothing, but it looks like this time I will. That is, as long as the damn car works, and my kids don't run the battery down playing rap music all night. For a glimpse at the future and further insights into this amazing technology, please visit Nissan's Leaf website at https://www.drivenissanleaf.com/ .

-

-

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-08 01:40:462011-02-08 01:40:46February 8, 2011 - Getting Something for Nothing

1) Years of Pain to Come in Residential Real Estate. Regular readers of this letter are familiar with my antipathy towards real estate of every flavor, with the exceptions of multi-unit dwellings (apartment buildings) and farmland .

So my interest was piqued when Ron Peltier spoke the other day, the CEO of? Home Services America, a national brokerage firm in the Berkshire Hathaway (BRK/A) fold. What better way to get a hands on, from the trenches read on this troubled market than Oracle of Omaha, Warren Buffet's personal agent?

He said that we may see the number of existing homes on the market climb from the current 4 million units to 5 million, versus a ten year annual trailing average sales of 2.5 million units. Record foreclosures are forcing reasonable sellers moving for demographic reasons (larger families, job changes, divorces, etc.) to compete against distressed sellers, driving prices down. Those suffering the indignity of losing their homes are seeing realizations at 25% to 50% below fair value.

At least 25% of American homeowners, or some 35 million dwellings, have negative equity.? While prices on average have fallen back to 2002 levels, Peltier doesn't expect further declines because of the huge support provided by mortgage interest rates at 50 year lows. So he sees a best case scenario of flat prices until this record excess inventory of 2.5 million homes is worked off, which can't occur until 2012 at the earliest.

Personally, I think Peltier is being optimistic because he doesn't address the hurricane force headwinds of the retirement and downsizing of 80 million baby boomers, the parsimonious attitude of banks towards new borrowers, and the harsh reality of continued falling standards of living in the US. Continue to rent, not buy, and let the landlord worry about the rats in the attic.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-07 02:00:562011-02-07 02:00:56February 7, 2011 - Years of Pain to Come in Residential Real Estate

2) Who Says Hedge Funds Aren't Adding Value? According to my old friend, Rick Sopher, chairman of LCH Investments in London, the top ten hedge funds have earned $153 billion for their investors since inception. John Paulson's fund alone, which made an absolute killing by shorting subprime mortgage debt instruments going into the housing crisis, came in tops with $26.4 billion in profits.

Rick, who runs his business from an elegant flat on posh Eaton Square, compiled the list after a comprehensive survey of the still operating 7,000 hedge funds worldwide. It is dominated by marquee names like Steve Cohen's SAC Capital, Bruce Kovner's Caxton, and Louise Bacon's Moore Capital. Of the 100 largest funds, 95% have returned much of their investors' original capital, and are using the remaining profits to trade on.

Of course, the numbers show a huge survivor bias. They don't include the hundreds of billions of dollars lost by now shuttered 'wanabee' managers during the financial crash, largely with highly leveraged fixed income, spread oriented, 'low risk' strategies. Many of these are still in liquidation, peddling illiquid assets for pennies on the dollar through online auctions and elsewhere.

The numbers highlight the increasing barbell nature of the hedge fund industry. The biggest funds continue to attract the big bucks, and a steady wave of defections from Wall Street, are funding hundreds of new startups. But many mid-tier firms are getting nothing and are struggling to stay in business.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-07 01:50:182011-02-07 01:50:18February 7, 2011 - Who Says Hedge Funds Aren't Adding Value?

'I'm sure there are gobs and gobs of money to be made in emerging markets,' said legendary hedge fund manager Bill Fleckenstein on Hedge Fund Radio.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-07 01:00:132011-02-07 01:00:13February 7, 2011 - Quote of the Day

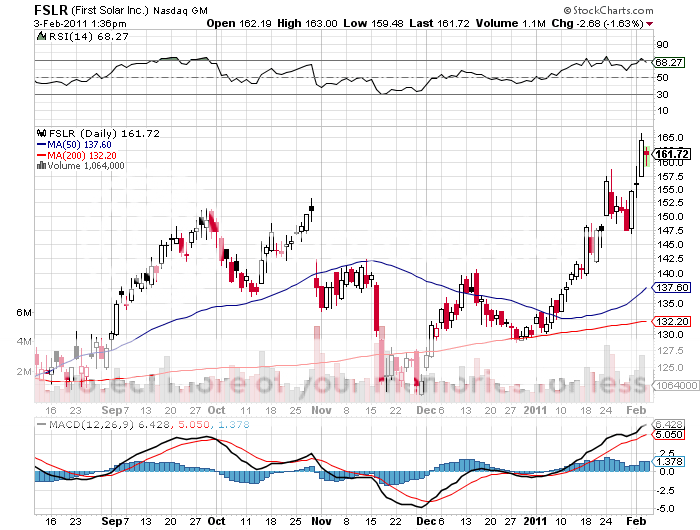

3) Solar Energy is Poised to Achieve Cost Parity. After two years of relentless cost, the solar industry is about to reach the Holy Grail of parity with the cost of conventional power sources at around 10 cents per kilowatt hour, paving the way for and exponential growth in profitability.

For those of us who have been cheerleading this industry from the sidelines since the 1973 oil shock, it has been a long and tedious wait. We have traveled the long and winding road from primitive roof mounted water pre heaters to advanced thin film technology, with endless political battles along the way against frequently hostile and tight fisted administrations in Washington.

You can thank Germany, a country that ironically often lacks sunlight, where individuals and local utilities alike are putting the pedal to the metal to cash in on generous government subsidies. The goal is to push the Fatherland's alternative energy supplies from the current 12.5% of total generation to 20% by 2020. Local sources tell me that installed rooftop solar panels are expected to double this year.

Several US states have similar mandates. California, which has the lofty goal of 30% for alternative power, has just approved the building of a massive solar facility in the Mohave Desert just North of Los Angeles.

The net net is higher volumes and prices than the solar industry was expecting only six months ago. This will enable the big players in this space to wean themselves off of subsidies, stand on their own feet, attract more private capital, and shrink costs further through economies of scale.

Part of the economization story for American companies involved the offshoring of a substantial part of its manufacturing to China. It didn't hurt that the Middle Kingdom signed a contract with First Solar (FSLR) to build an enormous one square mile plant in the Western part of their country, which looks an awful lot like our Southwestern desert, to gain advanced technology. They no doubt also sought to defuse the threat of anti-dumping actions in the US against their own manufacturers.

I think the earnings leverage in this industry is now huge, and any upturn in oil prices, which I expect over the long term, will act on profitability like a shot of steroids. Equity investors have recently figured this out and have broken (FSLR) out of its recent range to the upside. Buy (FSLR), which has lived in my long term model portfolio for some time, on any serious dip.

-

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-04 01:40:192011-02-04 01:40:19February 4, 2011 - Solar Energy is Poised to Achieve Cost Parity

Featured Trades: (THE YEAR OF THE RABBIT), (FXI), (SSEC), (CYB)

1) Ringing in the Year of the Rabbit. An invitation to the Chinese consulate for their New Year's party is always one of the most sought after invitations in the Lilliputan diplomatic community of San Francisco. Welcoming the Year of the Rabbit were true Mandarins bedecked in elegant silk brocade, rubbing shoulders with true proletarians wearing blue jeans and running shoes. The elite of the city's Chinese business community were there, celebrating a trade surplus with the US that exceeded $200 billion last year, taking out generous margins along the way.

Out of 500 guests, I was one of a handful on non-Chinese visitors. I have long been accorded VIP status here, being one of the few Americans still living who survived the Cultural Revolution, and having interviewed such luminaries as Deng Xiaoping and Zhou Enlai. It's like attending a Tea Party rally and telling people you used to pall around with Thomas Jefferson and Alexander Hamilton.

There was enough food to feed the entire Chinese army, which vaporized in minutes. After covering the country on the ground for 40 years, I still can only identify half of what I am eating. The trick is to never ask what it is because you might find out that it is disgusting (Chicken feet? Cock's comb?). One mysterious purple jellyfish like substance my hosts could only describe as 'fungus', which they scarfed down in great quantities.

The bar went mostly ignored, there being few takers of Great Wall merlot, attendees maintaining their allegiance to nearby Napa Valley. So I quaffed a couple of bottles of my favorite Tsing Tao beer. It was always healthier than the local water, both ours and theirs, although the benzene blended in to assure longevity during hot, humid summers, always gave me a headache.

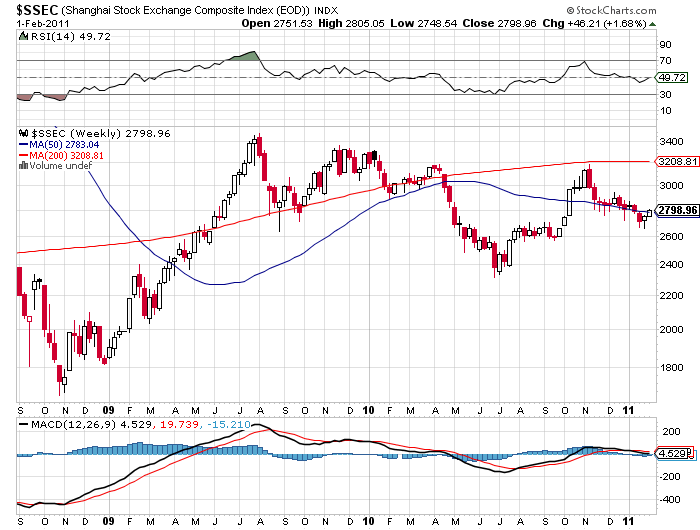

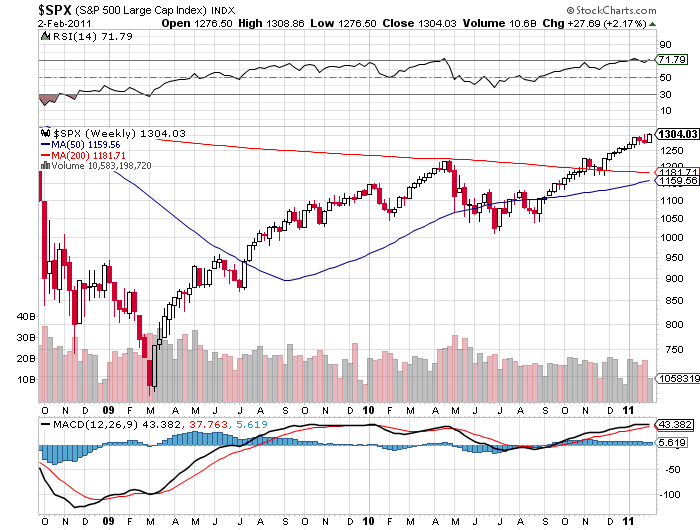

I managed to buttonhole a visiting senior official from the Ministry of Finance and asked him what gives with the Chinese stock market (FXI)? With GDP up 9.9% in the latest quarter, and a global bull market in full flower, how come the Shanghai Index ($SSEC) was down by 13% in 2010? Even the enfeebled dying capitalist nation of America saw its market up 9%, despite an enormous budget deficit, ballooning national debt, bankrupt states and cities, and a hopelessly incurable unemployment problem.

He said things were a little complicated. Inflation is getting to be a real problem in the Middle Kingdom. The challenge for the government is to cool of the inflationary parts of the economy, predominantly real estate, without killing off the rest. So far measures taken by the People's Bank of China have been targeted at speculative land purchases, to the extent that is possible. This is why the focus has been on increasing bank reserve requirements, which have been tightened seven times in the past year. Soon China's banking system will be as deleveraged as Canada's (5:1).

I told him that was nice, but that this would do nothing to address imported commodity inflation from abroad. The price of oil, coal, food, copper, and other essential raw materials were about to head up a lot more. I argued that the only means of dealing with this problem was to let the Yuan float (CYB), thus cutting the cost of imports in local currency terms. I was about to get into China's nationalization of several rare earth exporting firms when the Consul General motioned for him to join him on the other side of the room.

As I was explaining to my plumber the other day, if China is growing at 10% and we're growing at 2%, where do you want to own stock for the long term? You don't get a divergence like a stock market falling 13% while the economy is growing 10%, lasting forever, so it appears like there is a screaming 'BUY' setting up here. But given what I heard at the party, it is clear that the answer is an overwhelming 'Not Yet!' Jim Chanos, you may be right about a China crash, but you're early by a decade!

And what is the Chinese element for the New Year? Metal. Good thing I covered my short in gold.

Where's My Bull Market?

-

-

-

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-03 02:00:172011-02-03 02:00:17February 3, 2011 - Ringing in the Year of the Rabbit

3) An Insider's Review of Wall Street: Money Never Sleeps. One of the great things about flying first class is that you often get to meet some pretty interesting people. During the early eighties, I found myself on a flight from Los Angles to New York sitting next to an unknown aspiring young director named Oliver Stone, who was on his way to pitch a new film idea to potential investors.

Over six hours I enjoyed one of the most interesting conversations of my career, covering jungle combat in Vietnam, the ins and outs of movie making, and the harsh realities of Hollywood style accounting. The movie he was pitching turned out to be the 1987 industry cult classic, Wall Street.

The film sparked one of the greatest guessing games of all time, with everyone attempting to identify the real people behind the fictional characters. The villain, Gordon Gekko, was easy. That was Ivan Boesky, a risk arbitrageur who became the target of one of the first high profile insider trading case. Other links with reality were more obscure, and many real life traders on the floor of the NYSE simply played themselves as extras.

In the sequel, it is much easier to play who's who, thanks to the financial crash that seems like was happening only yesterday. Gordon Gekko, released from federal prison, this time turns into legendary hedge fund manager John Paulson, whose character turns $100 million into $1.2 billion in a matter of months through buying up cheap credit default swaps on subprime debt. Hank Paulson and Tim Geithner are easy to pick out in a crucial meeting at the New York Fed. The chairman of 'Keller Zabel' (Bear Stearns), one 'Louis Zabel' (Ace Greenberg), throws himself in front of a train on the Lexington line. Well, this is fiction, after all. The $2 dollar/share sale price gave it all away.

Many people played themselves. The whole CNBC crowd was there, their descriptions of the crash so realistic that I thought it might be archival footage. So were Warren Buffet, Nouriel Roubini, Jim Chanos, and other notables. In fact, Chanos managed to get Stone to change the original script, switching the bad guy role from a hedge fund to Goldman Sachs (GS), as it should be, referred to in the film as 'Churchill Schwartz.'. They are easily identified as the Wall Street firm that took out a big short in housing debt just before the crash.

Shia Labeouf does an outstanding job playing Jake Moore, an aggressive, razor sharp, earnest young investment banker. I have known so many like him over the years, both working for me and at competitors, that his performance really rung true. Michael Douglas, who has aged dramatically, seemed to be simply replaying the same role that he has in countless earlier films. To understand their characters, several actors opened up online trading accounts and did quite well in the market, with Shia alone reportedly booking some $20,000 in profits.

There are a few minor flaws in the film. It could have used more editing. There is a mention of '50% leverage' of subprime debt, when the correct figure was 50 times. The Chinese government investor doesn't act like a real person from the People's Republic, but as an American with a bad accent. However, these are trivial complaints. If you want to have a hoot, rent the DVD, but expect to provide a simultaneous translation about all of the different instruments and strategies if you bring any non-financial types with you. And thanks to Oliver's advice, I never got involved in financially backing a film project, despite countless invitations to do. It was the best trade I never did.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-03 01:40:282011-02-03 01:40:28February 3, 2011 - An Insider's Review of Wall Street: Money Never Sleeps

3) More Insights on Egypt. I had dinner with Neil MacFarquhar, UN Bureau Chief and former Cairo Bureau Chief for the New York Times, to get the latest view of what is happening on the Arab 'street.' MacFarquhar grew up in Libya around the time I tried to visit the country in the sixties (I was turned away at the Tunisian border), speaks and writes fluent Arabic, and has lived in Egypt, Kuwait, Israel, Cyprus, and Saudi Arabia, so he should know.

Until now, the US has tried to turn everyone into Americans, which is why Bush's policies were doomed to failure. As a result, our form of government has a bad name, which Iraqis now equate with violence and bloodshed. The political process in the Middle East is dead, with most countries run by dictatorships backed by secret police. Many have used the war on terrorism simply to lock up their own pro- democracy dissidents, and of course, our outsourcing of torture there is well known.

However, the bombings in Riyadh and Casablanca have clearly moved sentiment against Al Qaida. Ironically, the Arab cable TV network, Al Jazeera, has become a tremendous force for change by giving air to debate and alternative views, even though it has been opposed by the US for years. With 25% inflation and 30% unemployment, the mullahs have to eventually lose control in Iran, with the demographics running strongly against them.

Obama was right to launch new initiatives the first week of his administration in the region, where leaders have learned they can resist foreign peace efforts by waiting them out. I covered the Middle East myself as a journalist in the seventies and as an investment banker during the eighties, and what Neil says makes a lot of sense.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-02 01:40:592011-02-02 01:40:59February 2, 2011 - More Insights on Egypt

1) Thoughts on Egypt. When I first visited Egypt in 1977, they tried to kill me. I was accompanying US Secretary of State Henry Kissinger on an Air Force jet as part of his shuttle diplomacy between Tel Aviv and Cairo. Every Arab terrorist organization had vowed to shoot our plane down. When we hit the runway I looked out the window and saw a dozen armored cars and personnel carriers? chasing us just down the runway;? all on board suddenly got that gut churning feeling. When the plane stopped, they surrounded us, then turned around, pointing their guns outward. They were there to protect us. The sighs of relief were audible. In a lifetime of heart rending landings, this was certainly one of the most interesting ones. Those State Department people are such wimps! Henry was nonplussed, as usual.

When I traveled to Tel Aviv, El Al security made sure my luggage got lost. So the Israeli airline gave me $50 to buy clothes. On that budget, all I could afford were the surplus Israeli army fatigues at the Jerusalem flea market. A week later, my clothes still had not caught up with me when I boarded the plane with Henry. That meant walking the streets of Cairo in my Israeli army clothes. It would be an understatement to say that I attracted attention.

I was besieged with offers to buy my clothes. Egypt had lost four wars against Israel in the previous 30 years, and military souvenirs were definitely in short supply. By the time I left the country, I was stripped bare of all Israeli artifacts, down to my towels from the Tel Aviv Hilton, and boarded the British Airways flight to London wearing a cheap pair of Russian blue jeans. Levi Strauss never had a thing to worry about.

Virtually every research and intelligence organization seemed surprised at the sudden riots in Egypt that dinged the market on Friday. Every one, except this one, that is (click here for 'It's just a matter of time before the food riots resume'). For some time now, I have been warning that high food prices would lead to political instability in emerging markets. If you had to pick one place where this would happen first, it would be Egypt.

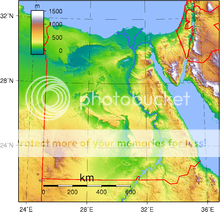

The bewitching North African country is a prisoner of a medieval religion that has left its people stranded in the Middle Ages. While its GDP has doubled in the last 60 years, so has its population, to 83 million, meaning there has been no improvement per capital income. Islamic fundamentalism can be traced back to the mid-19th century as an extreme reaction to British colonialism. Egypt responded by? inventing the concept of the sovereign debt default, which is how Britain ended up with the Suez Canal. Later, a young Winston Churchill cut his teeth as a journalist covering a major battle, the first where machine guns were successfully employed, and 10,000 of the faithful were mowed down. During the sixties, Gamel Abdel Nasser's efforts to form an Arab United States failed. As a journalist, I covered Kissinger's negotiations for peace with Nasser's successor, Anwar Sadat, who was? assassinated by his own bodyguard for his efforts shortly afterwards. Hosni Mubarek inherited the throne in 1981, and has been ruling the country with somewhat of an iron fist ever since.

I know that whenever the CIA kidnapped a suspected terrorist, but didn't want to deal with the legal consequences of bringing them home, they happily handed them over to Egypt, where the shadow of Amnesty International is unseen. Today, the advent of cell phones, cable TV, the Internet, Twitter, and even Facebook, enable revolutions to unfold at lightning speed. Cut these off, and everyone pours into the streets. The tourism industry, the big earner for this impoverished country, has been shattered and will take years to recover. The Egyptian stock market gave up $12 billion in stock market capitalization in two days, but who cares.

Events like this tend to have implications far beyond our initial understanding. In 1979, when the Shah of Iran fell to a movement led by an unknown radical mullah named Ayatollah Khomeini, we thought no big deal, it's a local problem. The Shah was no Boy Scout, and corruption in Iran was then endemic. Yet the fall out eventually led to our wars in Afghanistan and Iraq that has cost us trillions of dollars.

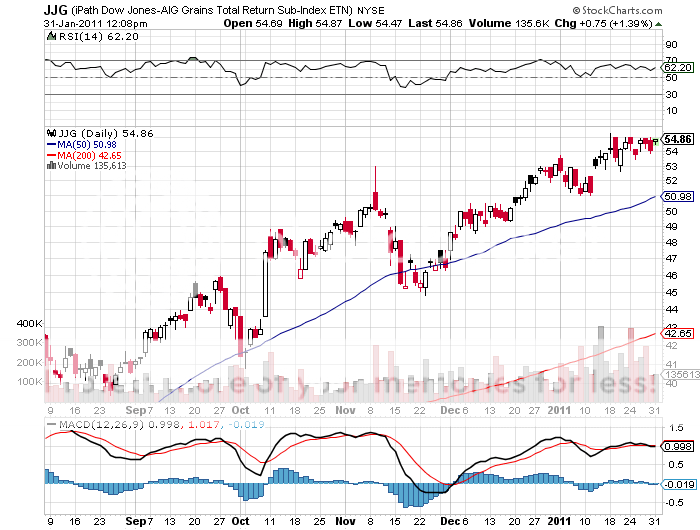

Of course, the final question has to be how all of this affects you and I and the financial markets. The positive impact on food prices has to be obvious. But as long as the world is in 'RISK OFF' mode, we aren't going to see dramatic moves in my favorite ETF in the area, the (JJG). The selloff in stocks was going to happen anyway, so don't pin the correction on the Middle East. Egypt was just the match to a market pyre that had been drenched with gasoline.

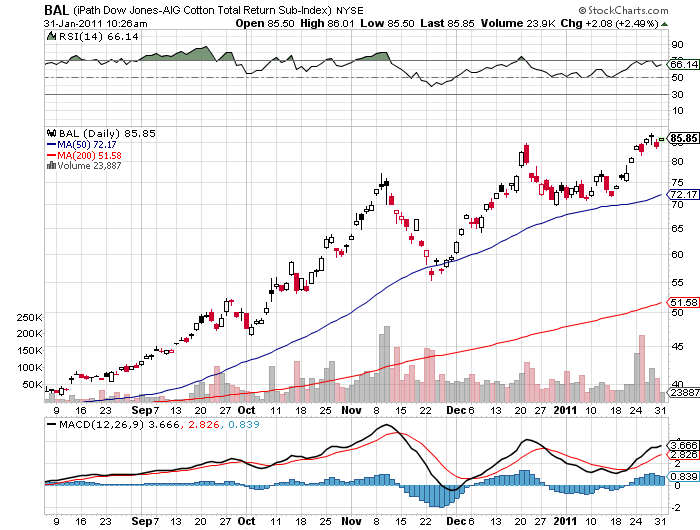

Today, Egypt is far and away the world's largest importer of wheat. It is also a major supplier of food to the rest of Africa, as it always has been. At first sight of the troubles, surrounding countries rushed to increase stockpiles to head off shortages, and are a major force driving prices higher. Egypt is also a leading supplier of cotton to the world market, and there is no other commodity less able to handle a supply cut off right now. Its price has already doubled in the past four months.

-

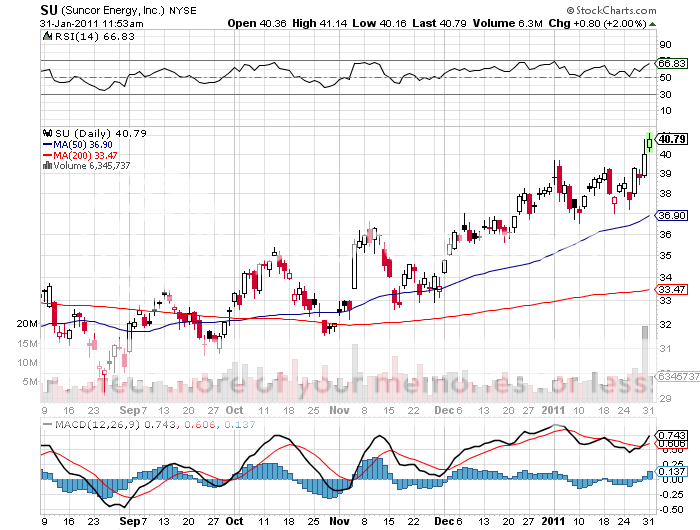

There has been much talk about the oil situation. While Egypt produces 600,000 barrels a day, that is a drop in the bucket in today's 84 million barrel/day global production. That is barely enough to meet domestic needs. A cut off of the Suez Canal would be problematic, but only for the short term. This explains why there has been a huge run up in Brent crude, to a record $9 a barrel premium over West Texas intermediate. But that is Europe's problem, not ours. All of America's crude from the Middle East comes around Cape Horn because the tankers are so large. If anything, this places a greater premium on Canadian tar sands producers like Suncor (SU), which are already rapidly replacing imports from other unstable sources.

The net net of all of this is a lot of short term angst, but little long term impact. This is great for volatility owners (VIX), (VXX), but of little consequence to the rest of us.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-02-01 02:00:032011-02-01 02:00:03February 1, 2011 - Thoughts on Egypt

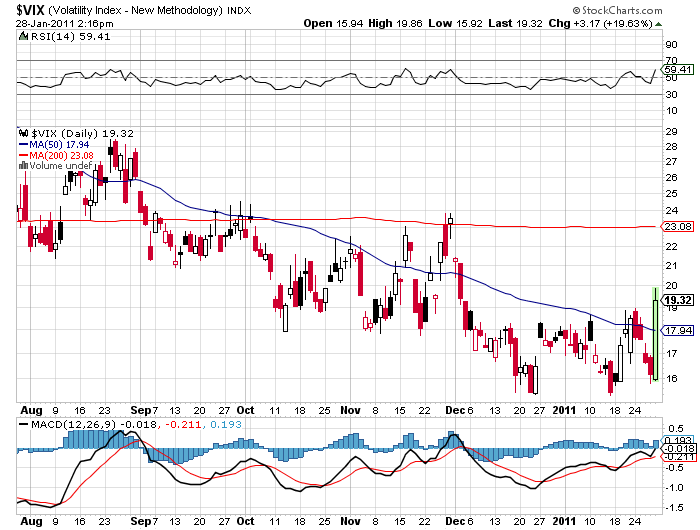

1) Learning About VIX the Hard Way. We certainly received a highly instructive lesson on how the volatility index (VIX) works on Friday. All it took was a ten point drop in the S&P 500 to trigger a stampede to buy insurance against further declines, taking the closely watched barometer from $15.90 to $20 in hours. It was only three days ago that I urged readers to buy flood insurance while the sun was shining. Good luck getting it now with a torrential thunderstorm overhead.

There were more potential culprits for the washout than found in an Agatha Christie murder mystery. You knew it was going to be a tough day when Amazon (AMZN) came in with a big earnings disappointment. Then Ford Motors (F) followed with its own huge shortfall.? The riots in Egypt threatened a cut off of the Suez Canal, sending oil prices soaring. A much ballyhooed Q4 US GDP, expected to run as hot as 4%, came in at a still robust 3.2%, disappointing many bulls. Given that corporations have been reporting earnings at a torrid pace, some 70% beating analysts' forecasts, even I was taken aback when I first heard the number. Spending on government stimulus efforts seems to be bleeding off faster than expected.

Once the selling started, virtually every technician out there started setting off emergency flares. The lead bellwether stocks for the market, like Apple (AAPL), Caterpillar (CAT), and Goldman Sachs (GS) started hitting the floor like a prom dress. The glass has suddenly gone from half full to half empty. The cat was set amongst the pigeons when NASDAQ's automated order system for options briefly broke down because of an imbalance of sell orders.

My friend, technical analyst to the stars, Charles Nenner, warned you on January 10 that the markets would peak on January 26 (click here for the interview on HedgeFund Radio). Really, Charles! You're slipping in your old age. You were two days early this time!

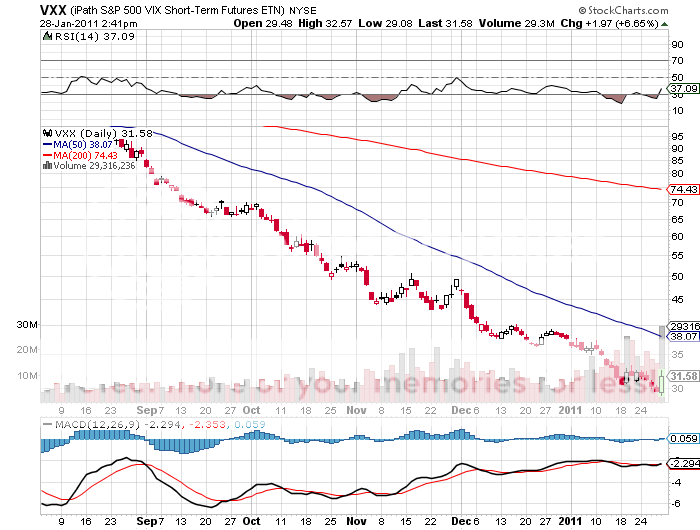

For those who are unable to engage in the long (VIX) options strategies that I have been recommending, and prefer an instrument that can be easily traded in a simple online equities trading account, you might take a look at the IPath S&P 500 VIX Short Term Futures exchange traded note (VXX) (click here for the prospectus). The (VXX) gives investors a slightly different, non-leveraged volatility play on the (VIX), as it is concentrated in S&P 500 options for only the front two months. You will, therefore, see divergences between the two, especially when short term volatility gaps against long term volatility. On Friday, the (VXX) popped 7% during the carnage.

-

-

-

Do You Understand the VIX Now?

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2011-01-31 02:00:222011-01-31 02:00:22January 31, 2011 - Learning About VIX the Hard Way

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.