Featured Trade: (FAREWELL TO QUANTITATIVE EASING), (SPY), (TLT), (TBT), (FXE), (EUO), (FXY), (YCS), (LNG), (BIDU), (TSLA), (BAC), (MS), (GS), (AXP), (AN EVENING WITH JAMES BAKER III), (CONNECTING UP AMERICA)

SPDR S&P 500 ETF (SPY) iShares 20+ Year Treasury Bond (TLT) ProShares UltraShort 20+ Year Treasury (TBT) CurrencyShares Euro ETF (FXE) ProShares UltraShort Euro (EUO) CurrencyShares Japanese Yen ETF (FXY) ProShares UltraShort Yen (YCS) Cheniere Energy, Inc. (LNG) Baidu, Inc. (BIDU) Tesla Motors, Inc. (TSLA) Bank of America Corporation (BAC) Morgan Stanley (MS) The Goldman Sachs Group, Inc. (GS) American Express Company (AXP)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-30 01:06:402014-10-30 01:06:40October 30, 2014

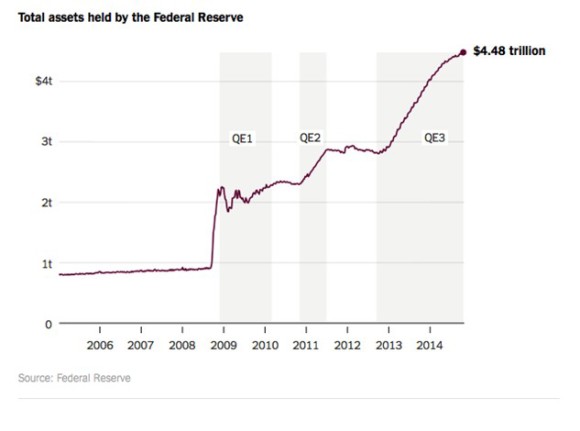

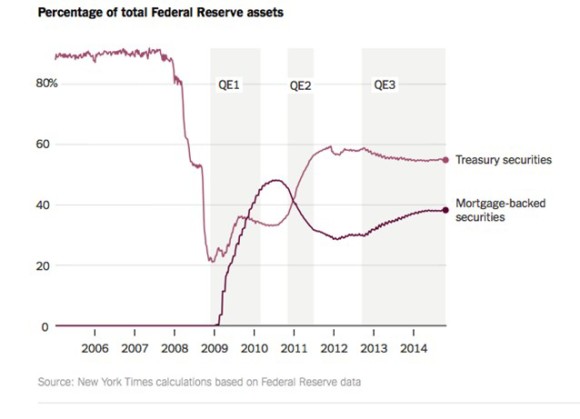

Finally, at long last, after infinite amounts of speculation and false starts, the Federal Reserve has decided to end quantitative easing.

After five years of soaking up both public and private debt in the marketplace, some $4.5 trillion worth, America?s central bank will quit picking up paper sometime next month. The printing presses are getting turned off and put into cold storage, job well done.

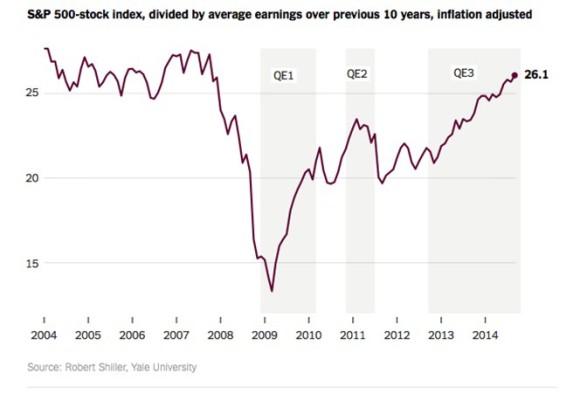

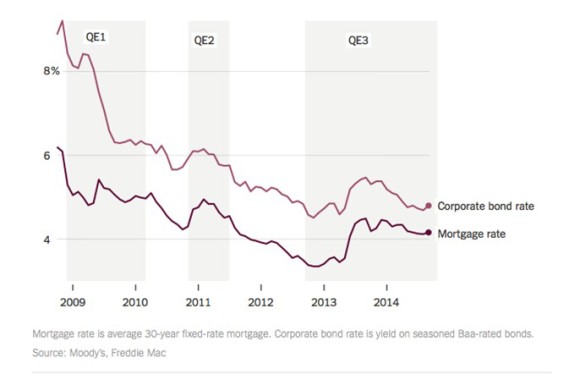

Boy, that was one hell of a monetary stimulus program, the likes of which has not been seen since the Great Depression. So much money flooded into the economy that homes values doubled on the bottom, stock indexes tripled, enriching quite a few traders along the way, including many followers of the Mad Hedge Fund Trader.

Who ended up making most of the money? Risk takers, equity owners, and the 1%. Everyone else was left in the dust, still waiting for the economic recovery to begin.

Since the controversial program was dreamed up and implemented by the former Fed governor, Ben Bernanke, five years ago, some $12 trillion was added to the value of equities alone. Some of my picks, like Cheniere Energy (LNG), Baidu (BIDU), ad Tesla (TSLA) soared by nearly 20 times.

Conservatives hated QE, fearing that such easy money would lead to hyperinflation and the collapse of the US dollar. The only problem is that the Consumer Price Index didn?t get the memo, with deflation now the country?s greatest economic threat. As I write this, the greenback is tickling new multiyear highs.

What QE did do was pull the US away from the brink of complete economic collapse. As far as the Fed is concerned, mission accomplished.

The other message that emanated from the Fed today is that it may raise interest rates sooner than expected. That trashed the bond market, taking Treasury bond yields to 2.35%, off an amazing 40 basis points from the low only two weeks ago.

There are some important points to take here for our trading strategy going forward.

First of all, the final top in bonds is looking more convincing by the day.

Second, the top in bonds, and slightly hawkish tone taken by the Fed today are extremely positive for the banks. I have already loaded up followers with Bank of America (BAC), which just pierced $17 on the upside and appears poised to claim new highs for the year.

I am inclined to add to this position on dips, and expand to my exposure to other names. On the menu are Morgan Stanley (MS), Golden Sachs (GS), JP Morgan (JPM), Wells Fargo (WFC), and American Express (AXP).

The dollar rocketed. Those who followed my recent Trade Alerts to aggressively sell short the Euro (FXE), (EUO) and the yen (FXY), (YCS) were sent laughing all the way to the bank.

I spoke to my colleague after the close today, ace Mad Day Trader, Jim Parker. We concluded that if the market doesn?t show any weakness Thursday morning, we could continue a straight line run up into the month end book closing on Friday, and then on to new all time highs.

I know it?s not gentlemanly to say ?I told you so,? but I told you so.

If you are bemoaning the loss of quantitative easing, don?t worry, it may not be gone for long.

When the economy goes into the tank in two or three years, it may well return from the dead in all its glory, especially if the inflation rate peaks in this cycle at an Appalachian 2.5% and then heads for negative numbers.

Will Quantitative Easing Return From the Dead?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Dracula-e1414680764804.jpg235400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-30 01:05:532014-10-30 01:05:53Farewell to Quantitative Easing

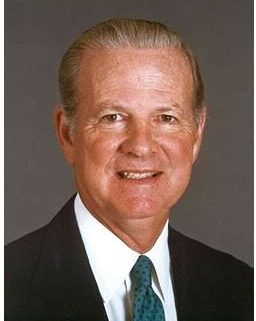

?We have 3,500 nuclear weapons left over from the cold war we don?t need, they take 20 seconds to re-aim, we?re not afraid to use them. And by the way, they?re already aimed at you.? That is the approach James Baker III thinks America should take with Iran, Ronald Reagan?s Chief of Staff and Secretary of the Treasury and George H.W. Bush?s Secretary of State.

At the same time we should be talking to the regime in Tehran, while doing everything we can to support the reformers, tighten sanctions, and enlist Europe?s help. Baker does not see a military solution in Iran, even though their potential to create instability in the region is enormous. This was one of dozens of amazing insights I gained chatting with the wily Texas lawyer during an evening in San Francisco.

Baker is happy to take on the ?America Bashers?, pointing out that the US still plays a dominant role in the UN, NATO, the IMF, and the World Bank. It accounts for 25% of global GDP, and its military is unmatched. The US spread globalization, and the spectacular growth of China and India is largely the result of open American trade policies, raising standards of living globally.

But the US can?t take its leadership role for granted. The biggest threats to American dominance are the runaway borrowing and entitlements. US debt to GDP will soar to over 100% in the near future, the highest level since WWII. This is unsustainable, is certain to bring a return of inflation, and unless dealt with, will lead to a long term American decline on the world stage.

Massive trade and capital flow imbalances also have to be addressed. The 84-year-old ex-Marine, who confesses to being the only Treasury Secretary in history who never took an economics class, believes that the advantageous rates that the government now borrows at are not set in stone.

Baker is the man who engineered an end to the cold war with a whimper, and not a bang. He thinks that ?even our power has its limits,? and that there is a risk of strategic overreach.? With the US politically evenly divided, Congress has degenerated from debating teams into execution squads, and consensus is impossible. The media are partly to blame, especially bloggers who propagate wild conspiracy theories, as confrontation sells better than accommodation.

Regarding the financial crisis, we need to end ?too big to fail? and embark on re-regulation, not strangulation. All in all, it was a fascinating few hours spent with a piece of living history who still maintains his excellent contacts in the diplomatic and intelligence communities.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/James-Baker.jpg335256Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-30 01:04:482014-10-30 01:04:48An Evening With James Baker III

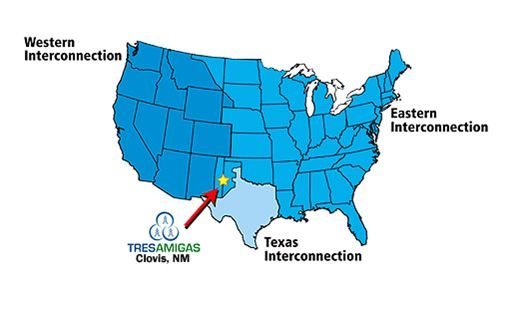

Until now, the country?s power grid has been divided into three unconnected, noncompetitive kingdoms (in the spirit of Game of Thrones), making transnational transmission impossible, leading to huge regional mispricing. While California and New York suffered from periodic brown outs and sky-high prices, electricity was given away virtually for free in Texas.

A group of power companies is now building the $1 billion Tres Amigas superstation in Clovis, New Mexico that would connect all three grids. The plant would use advanced superconducting technology that will send five gigawatts of power down cables cooled at 300 degrees below zero. Construction is expected to reach completion in 2014.

The facility would solve a major headache of alternative energy planners, and will no doubt accelerate development. It would allow the enormous wind farms in the Lone Star State to ship energy to the power hungry coasts. Ditto for the mega solar projects proposed in the Southwest deserts, and the big geothermal plants being built in Nevada. With the Department of Energy having already sent tidal waves of government cash towards the sector, the timing couldn?t be better.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Tres-Amigas.jpg311526Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-30 01:03:422014-10-30 01:03:42Connecting Up America

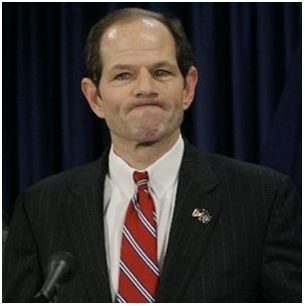

I couldn?t for the life of me figure out why New York?s former governor and federal prosecutor, Eliot Spitzer, wanted to invite me to dinner. He wasn?t flogging a book or promoting a movie, and he certainly wasn?t running for office again. But I went anyway, thinking perhaps the notorious ?Client No.9? might let me peek at his famous black book.

Eliot, who showed up wearing a classic New York blue pin stripped suit that seems oddly out of place in San Francisco, is currently running his family?s commercial real estate business.

He told me that the advantages that the US enjoyed over the rest of the world in 1945, such as a monopoly in skilled labor, are now long gone. The driver of the world economy has switched from America to Asia in the nineties.

As a result, income distribution here has morphed from a bell shaped curve to a barbell, with both the wealthy and the poor increasing in numbers, squeezing the middle class. The financial crisis compressed 30 years of change into two, taking us from libertarian Ayn Rand to pay Czar Ken Feinberg in one giant leap.

Having cut his teeth prosecuting the Gambino crime family in the eighties, Eliot had some views on the need for more regulation. We only need to enforce the laws on the books, not pass new ones. The ?white collarization? of organized crime has been a secular trend since the sixties.

He said the ethical lapses in the run up to the crash were best characterized by a quote from Merrill Lynch?s Jack Robins; ?What used to be a conflict of interest is now a synergy.?

AIG getting 100 cents on the dollar from the federal government was the greatest scam in history. The US did not extract a high enough price from top paid executives and shareholders of financial institutions for failure, and should have let more firms go under.

As for his own scandal, Eliot admitted that he failed, that his flaws were made publicly apparent, and that other politicians should be smarter than he was.

Although Eliot had some good ideas, I was still puzzled over what this was all about as I ploughed through my cr?me brulee. Perhaps the governor has a pathological need to be in front of the spotlight, even at the risk of flaming out.

And no luck with the black book.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/04/Eliot-Spitzer.jpg306305Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-29 01:05:572014-10-29 01:05:57Dinner With Eliot Spitzer

Her red Tesla is parked in the driveway, her potted plants are back on the balcony, and the closet is once again filled with designer shoes.

Goldilocks is back!

It?s not like she was ever going to be gone for long. Once a woman of a certain maturity gets accustomed to the lifestyle of the rich and famous, it?s hard to give up the better things in life.

However, there were some doubts.

When the Dow Average opened down 400 points on October 15, a gigantic capitulation move saw $70 billion worth of stock sold at market at the absolute low of 15,850, and a spectacular 315 million shares of the S&P 500 ETF (SPY) were unloaded.

One might have thought that Goldilocks had changed her name and moved into a nunnery for good.

It was not to be.

The rally that ensued off of that print was one of the most ferocious in history. After having cleaned out hedge fund trader longs on the downside, the market then ripped their faces off on the upside.

It has not been a good year for hedge funds. It has been a fantastic year for high frequency traders, with September the most profitable month in the history of this arcane, computer trading strategy.

As for me, I never had any doubt that Goldilocks was coming back. As I miraculously pound into my followers on a daily basis, it?s all about the numbers. It?s always about the numbers.

The strength of the economy is such that the sudden 10% swoon we witnessed was in no way justified. All that was really required was that an extreme overbought condition in stocks we say six weeks ago be remedied. Now that is done, it is up, up, and away.

Corporate earnings obliged, with an eye-popping 80% delivering upside surprises. Corporate earnings are now growing at a robust year on year 11% annual rate.

Instead of focusing in on Ebola, Russia and ISIS, traders are now looking at improving Purchasing Managers Indexes in both Europe and China. The Middle East has gone quiet. There were even rumors, later quashed, of an extended quantitative easing for the US.

The European Central Bank announced the results of its bank stress test, and guess what? Almost everyone passed! Only 12 banks need to raise $12 billion in new capital.

Of course, this was never more than a window dressing exercise designed to make us all feel warm and fuzzy about the beleaguered continent.

It worked!

Capital spending also remains robust for the first time in eight years. But I think most analysts are missing the reason why this is happening. It is too late for companies to add capacity for this economic cycle.

They are instead building factories now to accommodate demand for the next economic and financial boom in the early 2020?s, when the stiff demographic headwind created by the baby boomers flips to a brisk tailwind provided by the Gen Xer?s.

The true 800-pound gorilla on the trading landscape these days is the price of oil, which broke the $80 handle yesterday morning. As with every move by every financial instrument everywhere, the more it goes down, the more dire the forecasts become. The savings in energy costs at this level amount to $12,000 per family per year. Do the math.

$10 a barrel? Really?

I think it is safe to say, like interest rates, energy prices will stay lower for longer than anyone imagines possible. So add another 1% to US GDP growth this year, next year and the one after that.

When the stock market figures this out, new highs will follow, probably before year end.

Has Goldilocks Moved Back in For Good?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Goldilocks.jpg337131Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-28 09:12:302014-10-28 09:12:30Goldilocks is Back!

Now we learn that the Ebola virus has been riding New York?s ?A? train subway line since October 21!

That is what we have learned from the physician from Doctors Without Borders, now locked up in the Ebola Ward at Manhattan?s Bellevue Hospital, just returned from treating victims in the West African country of Guinea. His girlfriend and some close friends have been rounded up and are now undergoing 21 day isolation treatment.

As for the 100,000 people who have ridden the ?A? train since, we?ll just have to wait and see. And the Uber drive involved, who knows?

The doctor also went bowling in Brooklyn before he checked himself into the hospital. That will almost certainly signal the death of this much-loved recreation. Who knows where those fingers have been that used that 16 pound ball last?

Looks like I?ll never top my lifetime best of a 200 score.

As a long in the tooth trader of most of the world?s major markets, I can tell you to use every Ebola induced market swoon as a buying opportunity. To explain why, I have to delve into my dark and murky past.

Back in the early 1970?s, the well-connected head of the Biology Department at the University of Southern California got me a summer job at the Nuclear Test Site in Nevada.

Some 60 miles north of Las Vegas on lonely US Highway 95, I found four recreational vehicles parked on the right side of the road in the middle of nowhere, the place of business, one of the world?s oldest profession.

But where were the customers? From there, a dirt road headed east and disappeared over a distant mountain range. The road was not on the map.

An hour latter I found myself in Mercury, Nevada, then inside Nellis Air Force base, the mythical ?Area 51.? Baking in 120-degree heat and filled with hundreds of WWII era Quonset huts, Mercury Nevada was one of the most forlorn parts of the world. The sole recreational facility was the swimming pool, which was particularly popular with the coed graduate students after midnight.

My heavy math background got me a job to work on the ultra top secret Neutron Bomb project, although I didn?t find out that?s what is was for another decade. This is where ?yield? didn?t mean interest paid, but ?millions killed.?

Because I came from a biology department I was particularly popular with the biowarfare guys, who were also there in force. My area of expertise was tropical diseases.

I was often invited to lunch at the commissary so they could pick my brain for potential new vectors. Yes, the subject of Ebola came up, as the kill rate was an attractively high 50%. But it was dismissed because the transmissibility is so poor. You can?t rely on a bioweapon that requires you to hug your enemy.

In the end, the flu virus was settled on as the most effective agent. It is airborne, and the virus reproduces every hour. It has also been field-tested. During the great 1918-1919 Spanish Flu pandemic, 100 million died around the world, mostly those in their teens and twenties, including a couple of great aunts of mine.

Best of all, it naturally originates in China, where contact between humans and pigs is the greatest on the planet. That?s where our viruses combine to form new organisms. You?d never be able to tell the difference between a bioattack and the real thing.

Since then, the US has created hundreds of synthetic viruses and stockpiled their vaccines. The Chinese have created thousands. For more depth on this, click here for ?Will SynBio Save or Destroy the World?.

Which brings us all to where we are today. Why do we have a fixation, not only with Ebola, but ISIL, Russia, China, and the Ukraine as well?

I blame it all on the 24 hour news cycle, a monster with a voracious appetite that has to be constantly fed. Never mind that much of what they pump out is speculation, or is just plain untrue.

The financial media are the worst of all. On market down days they parade out their collection of perma bears. On the up days the perma pulls get the spotlight. Listen to all the advice and you end up buying the up days and selling the down days.

It is a perfect money destruction machine. Too many individual investors run through entire 401k?s and IRA?s before they figure this out, if ever.

I know when many readers see a news flash, they wonder ?Gee, should I sell?? I know people in New York who have become so nervous about Ebola, they have quit shaking hands with people.

I?m a little different.

One moron actually predicted that there would be 300,000 Ebola cases in Liberia by the end of the year. One of the purposes of this newsletter is to separate out fact from fiction, the wheat from the chaff. I take great pleasure in using an Ebola induced market dump to get you to load up on S&P 500 (SPY) calls spreads, as I have done.

I?ll tell you what the stock market thinks about Ebola. The two who caught the disease after the initial fatality are cured. The 48 who came into contact with him are also out of their 21 days quarantine period. So far the US has suffered one fatality from the dread virus, but boasts 330 million survivors.

There was a time in our history when we were flooded with thousands of disease carrying immigrants. They carried everything from black plague to smallpox, cholera, dengue fever, malaria, and tuberculosis.

What the government did then was quarantine all suspected carriers to Angle Island in San Francisco Bay and Ellis Island in New York harbor, until the doctors gave them the all clear. The new quarantine procedures hark back to that day.

You are not going to get the Ebola Virus. Earnings are the primary market focus here, not an African virus. Keep your eye on the ball, and don?t get distracted.

No Ebola Here

Is This A ?BUY? Signal?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Ebola-Virus-e1414246615403.jpg266400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-10-27 01:05:582014-10-27 01:05:58The Truth about Ebola

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.