What would happen if I recommended a stock that had no profits, was losing billions of dollars a year and had a net worth of negative $44 trillion?

Chances are, you would cancel your subscription to the Mad Hedge Fund Trader, demand a refund, unfriend me from your Facebook account, and unfollow me on Twitter.

Yet, that is precisely what my former colleague at Morgan Stanley did a few years ago, technology guru Mary Meeker.

Now a partner at venture capital giant Kleiner Perkins, Mary has brought her formidable analytical talents to bear on analyzing the United States of America as a stand-alone corporation.

The bottom line: the challenges are so great they would daunt the best turnaround expert. The good news is that our problems are not hopeless or unsolvable.

The US government was a miniscule affair until the Great Depression and WWII when it exploded in size. Since 1965 when Lyndon Johnson’s “Great Society” began, GDP rose by 2.7 times, while entitlement spending leapt by 11.1 times.

If current trends continue, the Congressional Budget Office says that entitlements and interest payments will exceed all federal revenues by 2025.

Of course, the biggest problem is with health care spending, which will see no solution until health care costs are somehow capped. Despite spending more than any other nation, we get one of the worst results, with lagging quality of life, life spans, and infant mortality.

Some 28% of Medicare spending is devoted to a recipient’s final four months of life. Somewhere, there are emergency room cardiologists making a fortune off of this. A night in an American hospital costs 500% more than in any other country.

Social Security is an easier fix. Since it started in 1935, life expectancy has risen by 26% to 78, while the retirement age is up only 3% to 66. Any reforms have to involve raising the retirement age to at least 70 and means testing recipients.

The solutions to our other problems are simple but require political suicide for those making the case.

For example, you could eliminate all tax deductions, including those for home mortgage deductions, charitable contributions, IRA contributions, dependents, and medical expenses, and raise $1 trillion a year. That would more than wipe out the current budget deficit in one fell swoop.

Mary reminds us that government spending on technology laid the foundations of our modern economy. If the old DARPANET had not been funded during the sixties, Google, Yahoo, eBay, Facebook, Cisco, and Oracle would be missing today. Tech generates about 50% of all the profits in the US today.

Global Positioning Systems (GPS) were also invented by and is still run by the government and has been another great wellspring of profits. I got to use it during the 1980s while flying across Greenland when it was still top secret. The Air Force base that ran it was called “Sob Story.”

There are a few gaping holes in Mary’s “thought experiment.” I doubt she knows that the Treasury Department carries the value of America’s gold reserves, the world’s largest at 8,965 tons worth $576 billion, at only $34 an ounce, versus an actual current market price of $1,288.

Nor is she aware that our ten aircraft carriers are valued at $1 each, against an actual cost of $10 billion each in today’s dollars. And what is Yosemite worth on the open market, or Yellowstone, or the Grand Canyon? These all render her net worth calculations meaningless.

Mary expounds at length on her analysis which you can buy in a book entitled USA Inc. at Amazon by clicking here.

Worth More Than a Dollar?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/01/naval-fleet.png387516Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-11-27 04:04:272019-11-26 07:00:55Is USA Inc. a Short?

Followers of the Mad Hedge Technology Letter have the good fortune to own a deep in-the-money options position that expires on Friday, November 15, and I just want to explain to the newbies how to best maximize their profits.

This involves the:

the Boeing (BA) November 2019 $300-$310 in-the-money vertical BULL CALL spread

The total profit on this position will increase the value of our $100,000 model trading portfolio by an impressive 1.35%, or $1,375. Provided that we don’t have a monster “RISK OFF” move in the market this week (more failure of the China trade talks? War with Iran? A massacre in Hong Kong?) which causes stocks to collapse and volatility to rocket, this position should expire at its maximum profit points. So far, so good.

I’ll do the math for you on the (BA) position. Your profit can be calculated as follows:

Profit: $10.00 - $8.75 = $1.25

(11 contracts X 100 contracts per option X $1.25 profit per options)

= $1,375 or 14.28% in 18 trading days.

Many of you have already emailed me asking what to do with these winning positions.

The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck, and pat yourself on the back for a job well done.

You don’t have to do anything.

Your broker (are they still called that?) will automatically use your long position to cover your short position, canceling out the total holdings.

The entire profit will be credited to your account on Monday morning November 18 and the margin freed up.

Some firms charge you a modest $10 or $15 fee for performing this service.

If you don’t see the cash show up in your account on Monday, get on the blower immediately and find it.

Although the expiration process is now supposed to be fully automated, occasionally mistakes do occur. Better to sort out any confusion before losses ensue.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. You can probably unload them pennies below their maximum expiration value.

Keep in mind that the liquidity in the options market disappears and the spreads substantially widen when a security has only hours or minutes until expiration on Friday. So, if you plan to exit, do so well before the final expiration at the Friday market close.

This is known in the trade as the “expiration risk.”

One way or the other, I’m sure you’ll do OK as long as I am looking over your shoulder as I will be, always. Think of me as your trading guardian angel.

I am going to hang back and wait for good entry points before jumping back in. It’s all about keeping that “Buy low, sell high” thing going.

I’m looking to cherry-pick my new positions going into the next quarter end.

Take your winnings and go out and buy yourself a well-earned dinner. Or use it to put a down payment on a long cruise.

Well done, and on to the next trade.

Markets are Especially Tricky Right Now

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/JT-story-2-image-e1523656976555.jpg237300MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-11-13 08:06:382019-11-13 08:50:56How to Handle the Friday November 15 Options Expiration

It is the sort of development that most Biotech investors only dream about. It also shows what’s possible in biotech investing, which is occurring with increasing frequency.

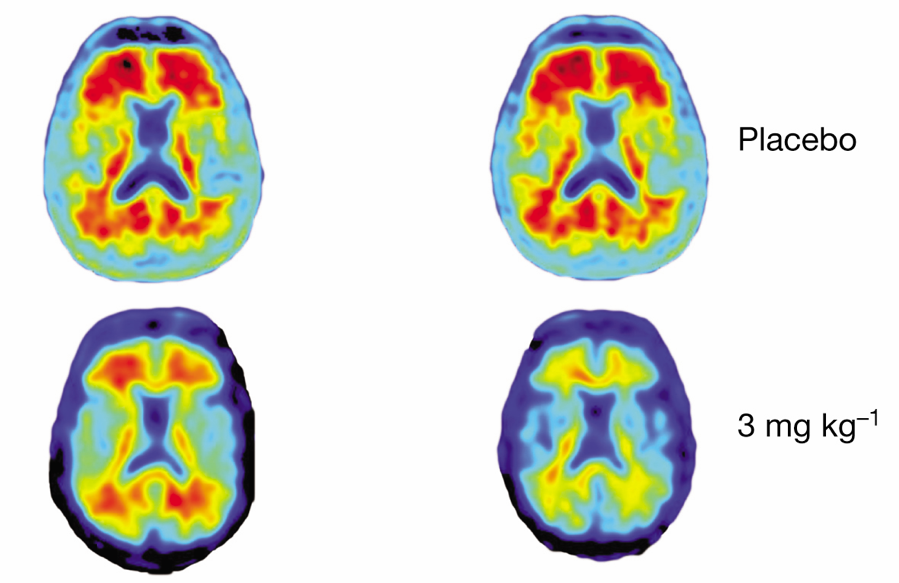

Biogen shares (BIIB) have exploded to the upside on its FDA application for its new Alzheimer’s drug. Written off for dead six months ago, the company secretly kept working on Aducanumab until today’s blockbuster announcement.

The drug reverses amyloid plaques thought responsible for Alzheimer’s. This could eventually cure tens of millions of Alzheimer’s sufferers and maybe even myself someday. The stock is up an incredible 40% today and has even dragged up the biotech ETF (IBB) an impressive 3%.

Way back in March, we saw a huge flop for Biogen (BIIB) as the biotech company supposedly shut down research for Alzheimer's treatment: aducanumab (BIIB037) on the failure of a stage 3 trial. This announcement was a curveball for its shareholders as the drug was touted as a potential groundbreaking miracle treatment with sales pegged at the tens of billions.

Biogen has for some time made Alzheimer's experiments the epicenter of their new drug pipeline. It also offers a multiple sclerosis treatment called Tecfidera.

Generic competition has been hot on its heels and shareholders can expect a number of patent challenges in the next few years. This would undoubtedly lead to a fall in sales soon especially with the recent crackdown on the skyrocketing prices of meds.

To combat these looming challenges, Biogen has shifted its focus on Spinraza which has been beating expectations since its release three years ago. Set to exceed the $2 billion in sales mark, this spinal muscular atrophy drug has been dominating the rare disease market for quite some time.

This reign might not last long though as Novartis AG (NOVN) and Roche Holding AG (ROG) are gunning to release their own version of the drug by 2020 or 2021. This means Biogen would once again see another blockbuster drug go flat.

How does Biogen plan to deal with the backlash?

If history is any indication, then investors can expect Biogen to start looking into acquiring medium-size biopharma firms as soon as possible. Since the company closed 2018 with $3.5 billion in cash along with $5.3 billion in its free cash flow, a buyout is a viable solution at the moment. However, the biotech giant can only afford one.

The medium-sized biopharma firms speculated to be under consideration include ACADIA Pharmaceuticals, Biohaven Pharmaceutical Holding Company, and Alder Biopharmaceuticals. However, Neurocrania Biosciences and Sage Therapeutics are said to be potential frontrunners for a Biogen takeover.

While a lot of investors would understandably be wary of another risk from Biogen, Neurocrania and Sage could be promising targets for the biopharma giant.

Neurocrania has been raking in huge profits from their blockbuster tardive dyskinesia drug Ingrezza since gaining FDA approval in 2017. In fact, annual sales of this product has reached $410 million in 2018.

Aside from their success with Ingrezza, Neurocrine has taken the first step towards gene therapy via their collaboration with Voyager Therapeutics. Just this month, Neurocrine has invested $165 million to commence the process of coming up with a treatment drug for Parkinson's disease.

Another good option is Sage as the company also focuses on neurology, which means their goals could align with Biogen's. The recent approval of Zulresso makes Sage the first company to provide treatment for severe postpartum depression.

While the Alzheimer's debacle can be overwhelming, Biogen's fundamentals remain attractive. In terms of revenue estimates, the company is anticipated to report a 2.2% increase this year or up to $13.75 billion. Meanwhile, growth for earnings per share is projected to be at 9.4% or up to $28.67 from its current EPS of $21.58.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/10/aducanumab.png597899Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-23 08:04:112019-12-09 13:10:28Biogen’s Huge Discovery

Tickets for the Mad Hedge Lake Tahoe Conference are selling briskly. If you want to obtain a ticket that includes a dinner with John Thomas and Arthur Henry, you better get your order in soon.

The conference date has been set for Friday and Saturday, October 25-26.

Come learn from the greatest trading minds in the markets for a day of discussion about making money in the current challenging conditions.

How much longer can the Fed keep boosting the market?

Will the recession start in 2020, or will we have to wait until 2021, and how soon will the stock market start discounting it?

How will you guarantee your retirement in these tumultuous times?

Will the next bear market be as bad as 2008-2009, or worse? And is it worth selling out everything now?

What will destroy the economy first, rising interest rates, collapsing earnings, a trade war, or all three?

Who will tell you what to buy at the next market bottom?

John Thomas is a 50-year market veteran and is the founder, CEO and publisher of the Diary of a Mad Hedge Fund Trader. John will give you a laser-like focus on the best-performing asset classes, sectors, and individual companies of the coming months, years, and decades. John covers stocks, options, and ETFs. He delivers your one-stop global view.

Arthur Henry is the author of the Mad Hedge Technology Letter. He is a seasoned technology analyst and speaks four Asian languages fluently. He will provide insights into the most important investment sector of our generation.

The event will be held at a five-star resort and casino on the pristine shores of Lake Tahoe in Incline Village, NV, the precise location of which will be emailed to you with your ticket purchase confirmation.

It will include a full breakfast on arrival, a sit-down lunch, coffee break. The wine served will be from the best Napa Valley vineyards.

Come rub shoulders with some of the savviest individual investors in the business, trade investment ideas, and learn the secrets of the trading masters.

Ticket Prices

Copper Ticket - $699: Saturday conference all day on October 26, with buffet breakfast, lunch, and coffee break, with no accommodations provided

Silver Ticket - $1,399: Two nights of double occupancy accommodation for October 25 & 26, Saturday conference all day with buffet breakfast, lunch and coffee break

Gold Ticket - $1,598: Two nights of double occupancy accommodation for October 25 & 26, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 26, 7:00 PM Friday night VIP Dinner with John Thomas

Platinum Ticket - $1,599: Two nights of double occupancy accommodation for October 25 & 26, Saturday conference all day with buffet breakfast, lunch, and coffee break, and an October 27, 7:00 PM Saturday night VIP Dinner with John Thomas

Diamond Ticket - $1,999: Two nights of double occupancy accommodation for October 25 & 26, Saturday conference all day with buffet breakfast, lunch, and coffee break, an October 25, 7:00 PM Friday night VIP Dinner with John Thomas, AND an October 26, 7:00 PM Saturday night VIP Dinner with John Thomas

Schedule of Events

Friday, October 25, 7:00 PM

7:00 PM - Exclusive dinner with John Thomas and Arthur Henry for 12 in a private room at a five-star hotel for gold and diamond ticket holders only

Saturday, October 26, 8:00 AM

8:00 AM - Breakfast for all guests at the Lakeshore Ballroom

9:00 AM - Speaker 1: Arthur Henry –The Mad Hedge Technology Letter -The Next Big Trends in Technology and How to Play Them

10:15 AM – 15-minute coffee break

10:30 AM - Speaker 2: John Thomas – Global Trading Dispatch - The Markets in 2020 – Risks and Rewards

12:00 PM - Lunch

1:30 PM - Speaker 3: Arthur Henry – The Mad Hedge Technology Letter - Pain and Pleasure in the Technology IPO Market

2:45 PM – Coffee Break

3:00 PM - Speaker 4: John Thomas – Global Trading Dispatch – The 2020 Election and the Markets

4:15 PM – Adjourn to Lone Eagle Bar

7:00 PM - Exclusive dinner with John Thomas for Platinum and Diamond ticket holders only in the lakeshore Ballroom

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Lake-Tahoe-image-2-e1523564301168.jpg232350Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-22 04:04:142019-10-21 15:23:55Last Chance to Attend the Mad Hedge Lake Tahoe, Nevada Conference, October 25-26, 2019

It was another dreadful DAY for the banks. All bank shares are now down in 2019 with the sole exception of JP Morgan, which is up a modest 10% since January 1. Although their core business is good, the share price hasn’t even bothered to mail it in.

So, I thought it would be time to take another look at what is disrupting the 200-year-old business model of this sector. And that would be Fintech, shorthand for Financial Technology.

To say that fintech was gobbling up the financial industry’s lunch would be a vast understatement. But here’s the problem. Fintech is taking over the world one transaction at a time in an industry that sees billions of transactions a year. The change is almost invisible. If someone were blowing up bank branches on a large scale this would be a far easier trend to see, but the net effect is the same.

The potential market is enormous. While the world’s physical money totals $5 trillion, actual assets controlled by banks today total a staggering $90 trillion.

Why this is all happening now is due to a confluence of several independent technologies. The number of people on the Internet has soared from 1.8 billion in 2010 to 4 billion today, to 8 billion by 2024.

Smartphone usage is diffusing at a similar rate. The roll out of 5G wireless assures that all communications will occur seamlessly, quickly, including financial transactions. Blockchain is enabling encryption on an industrial scale.

This has enabled the rise of a number of online firms over just the last few years that are rapidly taking over a number of traditional banking functions.

So far, the greatest impact has been overseas. Many countries that lack banking infrastructure are leapfrogging straight to mobile. It makes a ton of sense. Poor countries lack the capital to build expensive branch networks to raise fund, and the expertise on how to invest the deposits once in hand.

Good Money (https://goodmoney.com ) is an example of the new online banks that have burst onto the scene. The company offers depositors a generous 1.8% interest rate on overnight funds. Legacy banks are still paying close to zero, even though the Fed has raised rates seven times in three years.

US banks charge an average of $400 in fees a year for a full-service account. Good Money charges nothing.

You will never know where the money goes when you place it with Citibank (C), Bank of America (BAC) or Wells Fargo (WFC). At Good Money, you can specify that your funds be lent to a certain industry or even a specific company. While this means nothing to you or me, it is important issue to oriented Millennials.

Such efforts are called Crowdlending. It first took off in the US with startups like Prosper and Lending Club in the mid 2000s. We’re not talking small potatoes here, or a market that might develop someday. In 2018, some 22,000 businesses extended $380 billion in such loans.

There are other big markets ripe for disruption. I had to pay a Filipino developer $500 for some work he did on my website. Wells Fargo wanted to charge me $50 and the wire transfer would have taken a week. An outfit called Payoneer, Israel-based, did it for $5 and it took 5 seconds.

Wire transfer fees are in fact a global industry worth billions of dollars a year that is there for the taking. The SWIFT international transfer network alone processes some 24 million transactions per day.

It may not surprise many of you that China already has a huge lead in this area. It’s logical since their established banking system is primitive at best. China has three times more mobile phones than the US, five times more Internet customers, sees 10 times more eat-out orders, and 50 times more mobile transactions. In a future where data is currency, this is huge.

Ant Financial, an affiliate of Alibaba (BABA), is in the forefront, facilitating an eye-popping $8 trillion worth of transactions in 2017. Using artificial intelligence to scour public records for past borrowing, income, education, web surfing preferences, and even political leanings, smart finance can use artificial intelligence to gin up a quickie FICO score and generate a new $200 micro loan in as little as eight seconds.

Bank of America eat your heart out.

What gives the Chinese such an advantage here is their huge market, with some 800 million online participants. The money Ant Financial makes isn’t important now. It’s the digitized data they’re collecting and the way it can be manipulated with artificial intelligence. That gives them immense market power. Remember, in the new world, data is the new currency and the Chinese are creating more than we ever will.

The problem with early, under-the-radar but broad-ranging trends, it can be tough to flesh out pure investment plays. Listed liquid tradable stocks are few and far between. You can simply go out and buy Square (SQ) and PayPal (PYPL) and you’d be half the way there in getting some good exposure.

Here’s the problem with that plan. PayPal has tripled in the last two years, while Square has gone ballistic with a 2,000% gain. I expect further appreciation from here, but those ships have already sailed.

A better way to participate might be the Global X Fintech Thematic ETF (FINX), granted you have all the usual problems with specialized ETFs here such as liquidity, high management fees, and tracking error. But you do get exposure to a number of companies that are either domiciled abroad or are not yet publicly listed.

The five largest holdings of (FINX) include Square (SQ), Wirecard AG (WCAGY), Temenos Group AG, Fiserve Inc (FISV), and Intuit (INTU).

You could also simply buy Alibaba. However, as long as America’s trade war with China continues, all Chinese stocks will perform poorly. Given the stubbornness of both sides, the earliest that can happen is January, 2021.

To learn more about (FINX), please go to the manager’s website by clicking here.

Days Gone By

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-09 02:02:182019-12-09 13:03:40How Fintech is Eating the Banks' Lunch

This weekend, we are closing down our discount offer page to buy the New Mad Hedge Biotech and Healthcare Letter at the Founders Price for only $997.

There are two stock sectors that will most likely deliver 80% of the total market return over the coming decade. You already know one of them. The other is:

Biotechnology and Healthcare

An exciting combination of new technologies is coming together, much like the creation of the PC, Windows, and the Internet launched all at the same time in the early 1990s. The result of that revolution was a 10-fold to 1,000-fold increase in many stock prices.

They are about to replay the same movie again! Except this time, biotech and healthcare shares will be the big beneficiaries.

Long held back as a political punching bag, Biotechnology and Healthcare shares are about to break free of their past restraints. The ten baggers will be a dime a dozen. The drivers are very simple:

*Our understanding of the human genome is growing at an exponential rate

*The development of new supercomputers and big data is answering research questions once considered impossible

*Most major human diseases will be cured over the next decade

*US healthcare, the last 19th-century industry, is about to undergo a major restructuring, delivering immense profits

*Diabetes, arthritis, and dementia will all be treated with simple daily pills

*Artificial intelligence is vastly accelerating all of the above trends

With Your Subscription You Will Get:

1) A twice-weekly research newsletter highlighting the most important developments in biotech and healthcare

2) Immediately actionable text and email Trade Alerts sent out at market sweet spots

3) Same-day answers to emailed questions about specific biotech companies

4) Special reports on the dominant trends and players in biotech and healthcare

5) Access to a biotech and healthcare ten-year database

Gaining an unfair advantage in the most important investment theme of your lifetime will be the best decision you ever made!

The Mad Hedge Biotech and Healthcare Letter is already listed in my store at $1,500 a year. If you subscribe this week only, you can obtain a founder’s price of only $997. Act fast. We’ll be taking down this one-time offer this weekend.

To take advantage of this unique opportunity please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/10/DNA.png466302Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-10-04 07:04:212019-12-09 13:03:09Last Chance to buy the New Mad Hedge Biotech and Healthcare Letter at the Founders Price, or The Newsletter That May Save Your Life!

The first major industry to be fundamentally disrupted by artificial intelligence will be healthcare, America’s last 19th-century industry.

Major diseases are being cured at such a dramatic pace that if you can survive the next decade, chances are you can live forever.

DNA is the software of life and spending $3 billion to decode it by 2003 was the best investment the U.S. government ever made.

These are the opinions expressed by longtime friend Dr. Ray Kurzweil. These ideas may seem like the ravings of a mad lunatic. However, Kurzweil long ago became used to such criticisms. The funny thing is, his very long-term predictions have a nasty habit of coming true.

For Kurzweil is the head of engineering at Google (GOOG), the co-founder of the Singularity University, and an early AI evangelist.

The outer shell of the human brain, the neocortex, is where we do all of our higher thinking, problem-solving and imagining. It first appeared in our pre-mammalian ancestors some 200 million years ago.

The neocortex enjoyed a sudden growth spurt 2 million years ago for reasons no one understands. Maybe that’s when we came out of the trees. This gave homo sapiens a huge advantage over all other life forms on earth.

The next step in our intellectual evolution will be carried out by AI. By connecting our neocortex to the Internet, we will improve our intelligence by a billion-fold. Imagine everyone you come in contact with is a billion times smarter than they are today.

Ironically, such advances in human bionic connections have been greatly advanced by our recent wars in the Middle East, which created large numbers of quadriplegic veterans desperate for contact with the outside world.

Defense research dollars have poured in to meet this need. Last year, I saw a classified video of a disabled soldier operating a computer just by thinking about keystrokes.

Kurzweil calls such a connection the Singularity, where humans and computers become one. He envisions this taking place on a large scale by the mid-2040s.

We already know how this will affect civilization because the billion-fold improvement in intelligence is already available in our hand in the form of a smartphone. All that is missing is the human/machine connection.

Over the past 1,000 years, human life expectancy has improved fourfold, from 19 to 80. As a result, a raft of new diseases has appeared only in the past century that show up late in life, such as cancer, diabetes, arthritis, Parkinson’s disease, and dementia.

The problem with this is that a millennium is but a nanosecond in the course of human evolution. Human T-cells have not had the time to evolve to fend off an attack from a cancer cell, which is why the disease is ravaging the human race today. Cancer rates are up exponentially from the 19th century.

Fortunately, there is a way to speed up the evolutionary process. Microscopic nanobots the size of red blood cells can be designed to go after specific cancers, and then injected in swarms in your bloodstream to attack them.

Such technologies require precise manufacturing at the atomic level and will be available in the early 2030s. I have seen pictures of such nanobots myself under an electron microscope in the scientific literature.

Alternatively, with some diseases, such as diabetes, all we need to do is to reprogram our software (DNA) to produce more insulin. This can be done with monoclonal antibodies, whereby a length of bad DNA is excised and a good one installed.

By the end of 2017, the Food and Drug Administration had approved nearly 100 such molecules to deal with a whole range of genetic diseases. Click here for the list.

Such advances will soon lead to what Kurzweil calls “Longevity Escape Velocity,” where advances in medical research are taking place faster than the natural aging process. Then we will only have to deal with senescence cells, which are internally programmed to turn themselves off at a certain age. Presumably, monoclonal antibodies will be able to turn these back on as well.

Of course, the investment implications of all of this will be prodigious. Perhaps, that’s why the shares of the entire healthcare sector (XLV) and big pharma (XPH) have been on an absolute tear for the past two years.

I believe that technology and healthcare stocks will overwhelmingly be the major outperformers over the next two decades. We are seeing the profits from these revolutionary advances sill into companies such as Pfizer (PFE), Bristol Myers Squibb (BMY), and Merck (MRK).

However, all the healthcare advances in the world are not going to help you if you keep eating cheeseburger for lunch every day. One study I always like to cite took place during WWII when the global food supply shrank dramatically, and everyone was put on a strict mandatory diet. The incidence of every major disease fell by 30%.

At the end of the day, plenty of sleep, healthy eating, and exercise will always remain the greatest life extenders. Kurzweil himself has been an ardent vegetarian for most of his life.

As for me, I rather have a good steak once a month and settle for living only to 120.

Keep renewing those newsletter subscriptions!

The Next Cancer Cure?

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/Cancer-cure-image-6-e1537819934607.jpg300400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-10-03 03:02:052019-12-09 13:02:49AI and the New Healthcare

I’m the guy who eternally marches to a different drummer, not in the next town, but the other hemisphere.

I would never want to join a club that would lower its standards so far that it would invite me as a member. (Groucho Marx told me that just before he died).

On those rare times that I do join the lemmings, I am punished severely.

Like everyone and his brother, his fraternity mate, and his long-lost cousin, I thought bonds would fall this year and interest rates would rise.

After all, this is normally what you get in the eleventh year of an economic recovery. This is usually when corporate America starts to expand capacity and borrow money with both hands, driving rates up.

Of course, looking back with laser-sharp 20/20 hindsight, it is so clear why fixed income securities of every description have refused to crash.

I will give you 10 reasons why bonds won’t crash. In fact, they may not reach a 3% yield for decades.

1) The Federal Reserve is pushing on a string, attempting to force companies to increase hiring, keeping interest rates at artificially low levels.

My theory on why this isn’t working is that companies have become so efficient, thanks to hyper-accelerating technology, that they don’t need humans anymore. They also don’t need to add capacity.

2) The U.S. Treasury wants low rates to finance America’s massive $22.5 trillion and growing national debt. Move rates from 0% to 6% and you have an instant financial crisis, and maybe even a government debt default.

3) Constant tit-for-tat saber-rattling by the leaders of China and the United States has created a strong underlying flight to safety bid for Treasury bonds.

The choices for 10-year government bonds are Japan at -0.25%, Germany at -0.50%, and the U.S. at +1.62%. It all makes our bonds look like a screaming bargain.

4) This recovery has been led by consumer spending, not big-ticket capital spending.

5) The Fed’s policy of using asset price inflation to spur the economy has been wildly successful. But bonds are included in these assets, and they have benefited the most.

6) New rules imposed by Dodd-Frank force institutional investors to hold much larger amounts of bonds than in the past.

7) The concentration of wealth with the top 1% also generates more bond purchases. It seems that once you become a billionaire, you become ultra conservative and only invest in safe fixed-income products. The priority becomes “return of capital” rather than “return on capital.”

This is happening globally. For more on this, click here for “The 1% and the Bond Market.”

8) Inflation? Come again? What’s that? Commodity, energy, precious metal, and food prices are disappearing up their own exhaust pipes. Industrial revolutions produce deflationary centuries, and we have just entered the third one in history (after No. 1, steam, and No. 2, electricity).

9) The psychological effects of the 2008-2009 crash were so frightening that many investors will never recover. That means more bond buying and less buying of all other assets.

10) The daily chaos coming out of Washington and the extreme length of this bull market is forcing investors to hold more than the usual amount of bonds in their portfolios. Believe it or not, many individuals still adhere to the ancient wisdom of owning their age in bonds.

I can’t tell you how many investment advisors I know who have converted their practices to bond-only ones.

Call me an ornery, stubborn, stupid old man.

Hey, even a blind squirrel finds an acorn once a day.

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-6-e1577996576492.png393500MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-10-02 07:04:002019-12-09 13:02:40Ten More Reasons Why Bonds Won’t Crash

“May you live in interesting times.” The question is whether this old Chinese proverb is a blessing or a curse.

Our beleaguered lives have certainly been getting more interesting by the day, if not the hour. Trump has been withholding military aid from foreign leaders to fish for dirt on those who may run against him in 2020. The prospects of the Chinese trade negotiations seem to flip flop by the day.

Prospective IPOs for Saudi ARAMCO and WeWork have been stood up against a wall and shot. The Altria (MO) - Philip Morris (PM) merger went up in smoke. Brexit (FXB) has turned into a runaway roller coaster that has lost its brakes. And that was just last week!

All of this is happening with the major indices (SPY), ($INDU) mere inches away from all-time highs, with valuations at the high end of the decade-old band. A worse risk/reward for initiating new positions I can’t imagine. I think I’ll go take a long nap instead.

There are times to trade and there are times to engage in research and this is definitely time for the latter. That means when it is time to strike, you already have a list of short names on which to execute. The worst time to initiate research is when the Dow is down 1,000 points.

I believe the markets are gridlocked until we get a good look at Q3 corporate earnings. If they are as bad as the macro data is suggesting, markets will tank. If they aren’t, we may see a begrudging slow-motion grind up to new highs.

Our launch of the Mad Hedge Biotech and Healthcare Letter was a huge success. Let me tell you, we have some real blockbusters lined up in our newsletter queue. The Tuesday letter will have a link that will enable you to get in at the $997 a year founders’ price. Otherwise, you can find it in our store now for $1,500 a year. Please click here.

The WeWork IPO is on the Rocks, with the CEO soon to be fired for self-dealing. In any case, the company has minimal added value and will not survive the next recession when the bulk of its tenants walk. Don’t touch this one on pain of death, even down three quarters from its original valuation.

Watch out for October, says Goldman Sachs (GS), which will see a volatility (VIX) spike 25%. Shockingly poor Q3 corporate earnings results could be the trigger with almost every company negatively impacted by the trade war. This could set up our next entry point on the long side.

The Saudi ARAMCO IPO is on the skids in the wake of the mass drone attack. Terrorist attacks on your key infrastructure is not a great selling point for new shareholders. It just underlines the high-risk investing in the area. The world’s largest IPO may get cancelled.

A huge killing was made on the Thomas Cook affair. It looks like short sellers raked in $2.7 billion in profits on the collapse. Some 600,000 mostly British travelers were stranded or had future vacations cancelled.

Thomas Cook never figured out the Internet, were destroyed by the collapse of the pound triggered by Brexit and, horror upon horrors, bought an airline. It’s all great news for surviving European tour operators and discount airlines. Airfares are already rising.

The S&P Case Shiller ticked up in July, showing that the National Home Price Index rising 3.2%. It’s the first positive move in more than a year. It’s got to be super-low interest rates finally kicking in. But the real move up won’t start until SALT deductions come back in 18 months.

That went over like a lead balloon. From the moment Trump started speaking at the United Nations, stocks went into free fall, dropping 450 points from top to bottom. It’s trade war against everyone all the time with his withdrawal from globalization. Oh, and if you want to resist America’s incredible military might, we will crush you. It’s not what traders wanted to hear.

In the meantime, the impeachment moved forward, with younger Democrats forcing Pelosi’s hand. The Ukraine scandal, a Trump effort to have candidate Joe Biden arrested, was the stick that broke the camel’s back. Fortunately, the stock market could care less. Stocks rose 20% during the last impeachment in the 1990s.

US Consumer Confidence dove in September from 133 estimated down to 125.1 as trade war concerns take their toll. It’s one of the first September data points to come out and presages worse to come. News fatigue has to be a factor.

BitcoinCrashed 15% to a new three-month low, hitting $7,944. Other cryptos fell 20%. All of the explanations were technical as they always are with this bogus asset class.

The Vaping Crisis demoed the Altria-Philip Morris merger. Suddenly, the crown jewels are toxic and about to be made illegal. The Juul CEO has resigned and the company may be about to go down the tubes. One of the largest mergers in history that would have created a $200 billion company has been tossed on the dustbin of history.

In a rare positive data point, New Homes Sales soared 7.1% in August to a 713,000 annualized rate. Median sales prices rise by 2.2% YOY to $328,400. Inventories drop from 5.9 to 5.5 months. The big numbers are happening in the south and west. Historically low-interest rates are kicking in big time.

The FTC Slammed Match Group (MTCH), the owner of Tinder and OK Cupid, for security lapses and scamming their own customers. Apparently, that gorgeous six-foot blond who speaks six languages who want to meet me if I only subscribed doesn’t actually exist. Oh well.

Q2 GDP final read came in at 2.0% with no change from the last report. Coming quarters will almost certainly be worse as the chickens come home to roost from a global trade war. We may already be in a recession and not know it. Inventories are building at a tremendous rate. Certainly, Fortune 500 CEOs think so.

Tesla deliveries may hit new high in Q3, topping 100,000, according to last week’s leak. The stock is back in play. It looks like I am going to get a new entertainment package upgrade too.

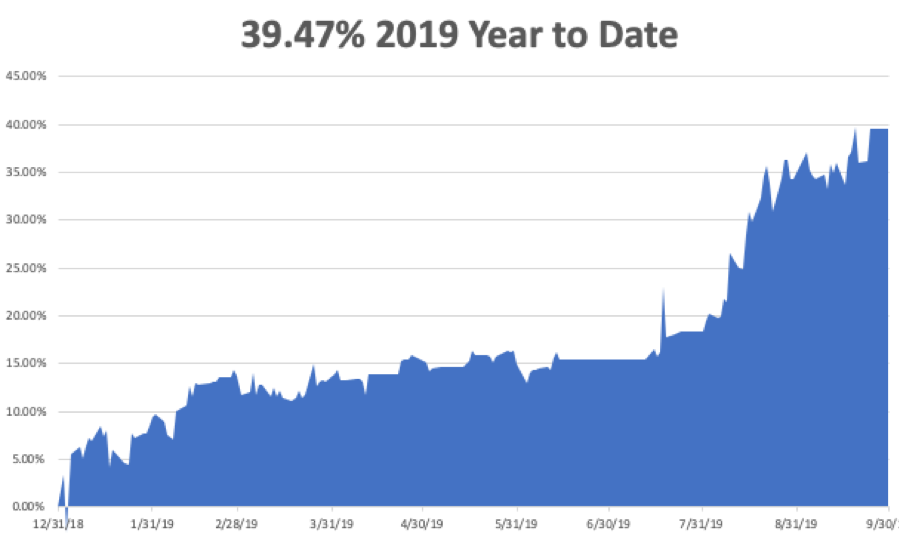

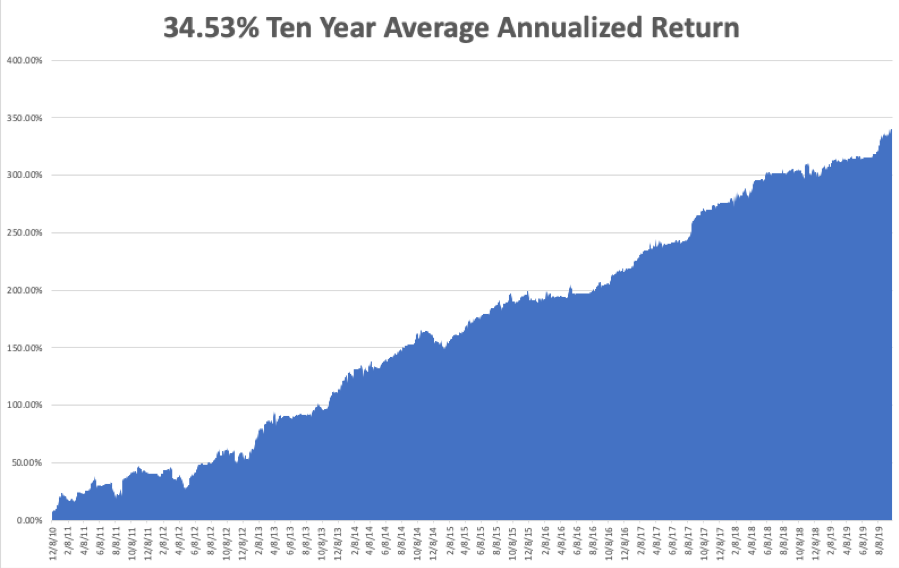

The Mad Hedge Trader Alert Service has blasted through to yet another new all-time high. My Global Trading Dispatch reached new apex of 336.07% and my year-to-date accelerated to +39.47%. The tricky and volatile month of September closed out +3.08%. at My ten-year average annualized profit bobbed up to +34.53%.

Some 25 out of the last 27 trade alerts have made money, a success rate of 92.59%. Under-promise and over-deliver, that's the business I have been in all my life. It works.

I took profits in my short position in oil (USO) earlier in the week, capturing a 12% decline there. That gives me a rare 100% cash position. I’m itching to get back in, but conditions right now are terrible

The coming week is all about the September jobs reports. It seems like we just went through those.

On Monday, September 30 at 9:45 AM, the Chicago Purchasing Managers Index for September is out.

On Tuesday, October 1 at 10:00 AM, the US Construction Spending for August is published

On Wednesday, October 2, at 8:15 AM, we learn the ADP Private Employment Report is out for September.

On Thursday, October 3 at 8:30 AM, the Weekly Jobless Claims are printed. At 3:00 PM, we get US Vehicle Sales for September.

On Friday, October 4 at 8:30 AM, the September Nonfarm Payroll Report is announced. Last month was a big disappointment so this month could set a new trend.

The Baker Hughes Rig Count is released at 2:00 PM.

As for me, I’ll be camping out with 2,500 Boy Scouts at the Solano Fair Grounds to attend Advance Camp. That’s where scouts have the opportunity to earn any of 50 merit badges in a single day.

I will be teaching the Swimming Merit Badge class. The basic idea is that if you throw a scout in the pool and he doesn’t drown, he passes. Personally, I wanted to take the welding class. The bonus is that we get to ride nearby roller coasters at Six Flags for free.

Good luck and good trading.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2019/09/john-thomas-4.png441827Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2019-09-30 05:02:472019-12-09 12:33:17The Market Outlook for the Week Ahead, or Interesting Times are Upon Us

Having been at the inception of the international trading order, first for The Economist magazine and later with Morgan Stanley, I can tell you that the initial reasons for unleashing globalization have long been forgotten.

It’s really very simple.

If someone is making a ton of money off of you, they are less inclined to blow you up. Profits are a great pacifier, and no one wants to destroy the people who have been buttering his bread.

During the 1960s, the US defense establishment went into a panic when China exploded its first atomic bomb.

Some 59 years later, the exponential growth of trade between our two countries have caused the risk of a mutual nuclear war to fall to near zero.

And what country in the world today would love to bomb the US off the face of the earth if it had the remotest ability to do so?

North Korea, which conducts no trade to speak of with the US.

There is another big reason why protectionism fails.

It is counterproductive in its impact on the American economy.

And not in a small way.

There are more than 45 million Americans living in abject poverty, stretching every dollar they have to make ends meet, saving nothing.

The apparel industry employs 135,000 Americans.

Can one really justify tariffs that increase the price of clothing for the 45 million in order to save a few of the 135,000 low-wage jobs?

A three-year 15% tariff enabled domestic producers to raise their prices, thereby increasing the costs of many American manufacturers.

By one estimate, each U.S. job “saved” cost $550,000 as the average bolt-nut-screw worker was earning $23,000 annually.

Ronald Reagan imposed “voluntary restraints” on Japanese automobile exports, thereby creating 44,100 U.S. jobs.

But the cost to consumers was a staggering $8.5 billion in higher auto prices, or $193,000 per job created, six times the average annual pay of a U.S. autoworker.

And there were big job losses in sectors of the economy into which the $8.5 billion of consumer spending could not be spent, like clothing.

In 2012, Barack Obama boasted that “over a thousand Americans are working today because we stopped a surge in Chinese tires.”

But this cost about $900,000 per job, paid by American purchasers of vehicles and tires.

The non-partisan Peterson Institute for International Economics says that this money taken from consumers reduced their spending on other retail goods, bringing the net job loss from the job-saving tire tariffs to around 2,500.

I could go on and on.

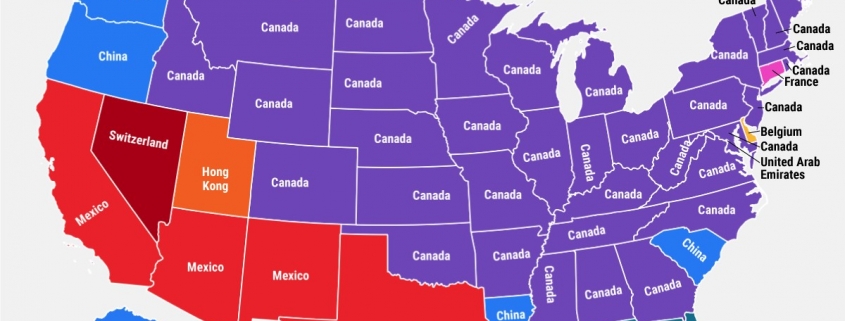

In researching this article, I stumbled across the map below showing the largest trading partner for each individual state.

While most states have Mexico or China as their largest trading partner, you would NOT believe some of the results!

Nevada-Switzerland

South Carolina-China

Delaware- Belgium

Florida-Brazil

Connecticut-France

So the bottom line here is to let free-market capitalism work unrestrained, and let whatever creative destruction taking place proceed full speed ahead.

Creative destruction is something the US does better than anyone else.

It’s why the US still has the largest and strongest economy by a mile, with the best major country long-term growth rate.

Don’t mess with success. You may not like the alternative.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/east-states-biggest-export-trading-partner-story-2-image-2-e1536094264139.jpg435580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2019-09-26 04:04:082019-12-09 12:33:44The High Cost of Trade Tariffs

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.