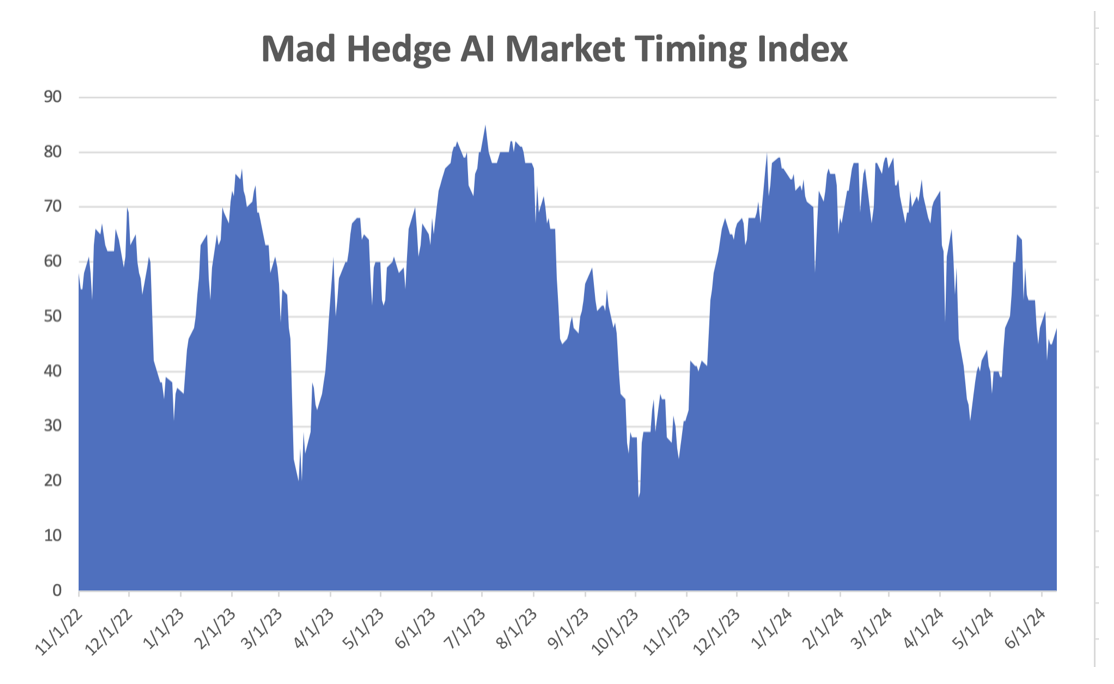

Since we have just taken in a large number of new subscribers from around the world, I will go through the basics of my Mad Hedge AI Market Timing Index one more time.

I have tried to make this as easy to use as possible, even devoid of the thought process.

When the index is reading 20 or below, you only consider “BUY” ideas. When it reads over 80, it’s time to “SELL.” Everything in between is a varying shade of grey. Most of the time, the index fluctuates between 20-80, which means there is absolutely nothing to do.

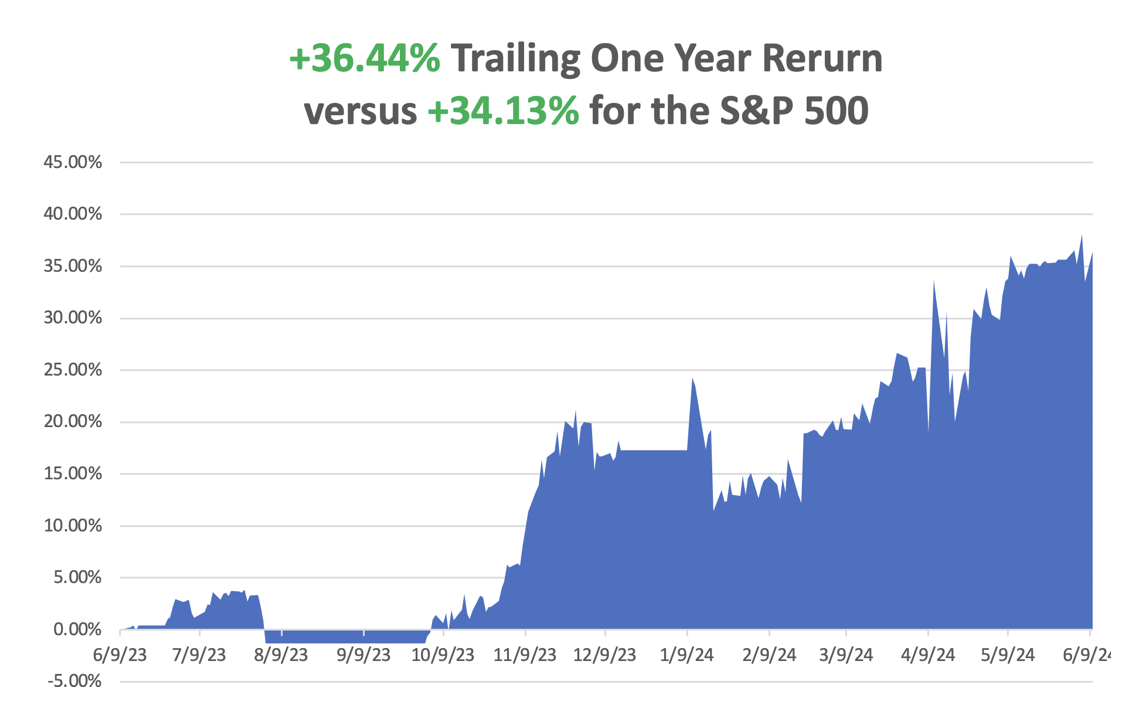

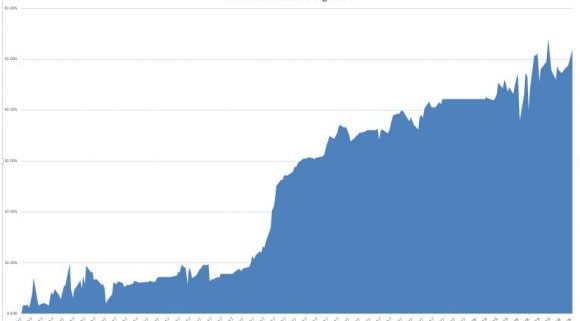

To identify a coming market reversal, it’s good to see the index chop around for at least a few weeks at an extreme reading. Look at the three-year chart of the Mad Hedge Market Timing Index.

After three years of battle testing, the algorithm has earned its stripes. I started posting it at the top of every newsletter and Trade Alert several years ago and will continue to do so in the future.

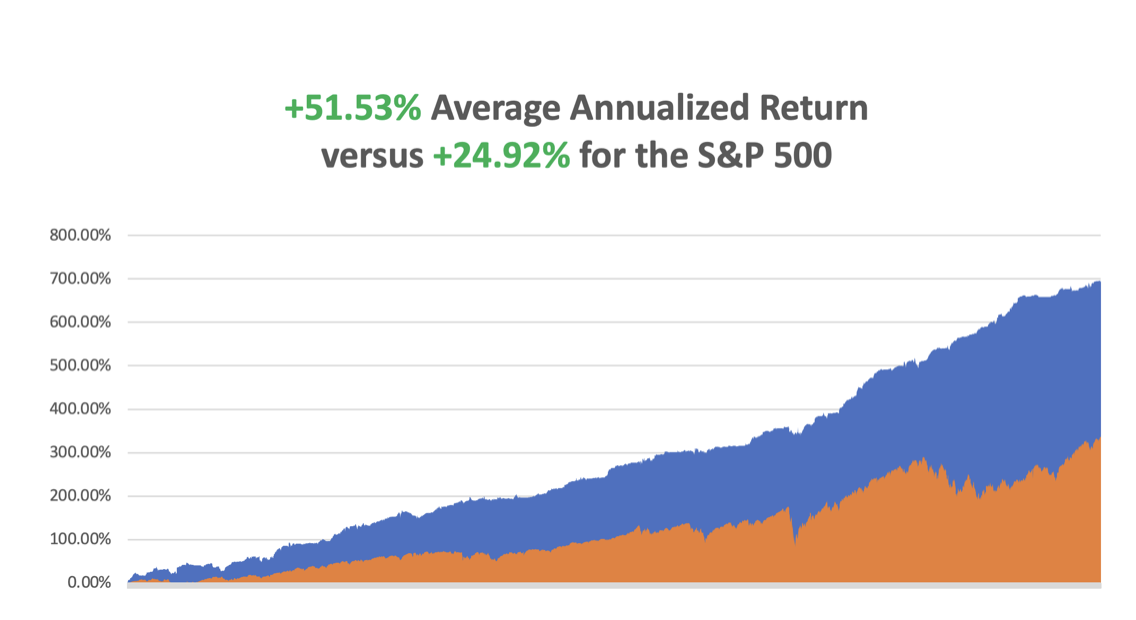

Once I implemented my proprietary Mad Hedge Market Timing Index in October 2016, the average annualized performance of my Trade Alert service soared to an eye-popping 44.54%.

As a result, new subscribers have been beating down the doors trying to get in.

Let me list the high points of having a friendly algorithm looking over your shoulder on every trade.

*Algorithms have become so dominant in the market, accounting for up to 90% of total trading volume, that you should never trade without one

*It does the work of a seasoned 100-man research department in seconds

*It runs in real-time and optimizes returns with the addition of every new data point far faster than any human can. Image a trading strategy that upgrades itself 30 times a day!

*It is artificial intelligence-driven and self-learning.

*Don’t go to a gunfight with a knife. If you are trading against algos alone, you WILL lose!

*Algorithms provide you with a defined systematic trading discipline that will enhance your profits.

And here’s the amazing thing. My Mad Hedge Market Timing Index correctly predicted the outcome of the presidential election, while I got it dead wrong.

You saw this in stocks like US Steel, which took off like a scalded chimp the week before the election.

When my and the Market Timing Index’s views sharply diverge, I go into cash rather than bet against it.

Since then, my Trade Alert performance has been on an absolute tear. In 2017, we earned an eye-popping 57.39%. In 2018, I clocked 23.67% while the Dow Average was down 8%, a beat of 31%. So far in 2024, we are up 20%.

Here are just a handful of some of the elements that the Mad Hedge Market Timing Index analyzes in real-time, 24/7.

50 and 200-day moving averages across all markets and industries

The Volatility Index (VIX)

The junk bond (JNK)/US Treasury bond spread (TLT)

Stocks hitting 52-day highs versus 52-day lows

McClellan Volume Summation Index

20-day stock bond performance spread

5-day put/call ratio

Stocks with rising versus falling volume

Relative Strength Indicator

12-month US GDP Trend

Case Shiller S&P 500 National Home Price Index

Of course, the Trade Alert service is not entirely algorithm-driven. It is just one tool to use among many others.

Yes, 50 years of experience trading the markets is still worth quite a lot.

I plan to constantly revise and upgrade the algorithm that drives the Mad Hedge Market Timing Index continuously as new data sets become available.

It Seems I’m Not the Only One Using Algorithms

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/algorithm.png768575Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-07-02 09:02:242024-07-02 10:11:09How the Mad Hedge Market Timing Algorithm Works

I have been watching with some amusement the trading of the Trump Media & Technology Group (DJT).

After the IPO was issued in 2023, it soared to $130, then collapsed to $15. It has just completed another round trip, plunging 50% over the last month. This is for a company that posted a horrific $58 million loss in 2023. In no way can that support a $5 billion market cap at the current $22 share price unless it’s the next AI stock we don’t know about. (DJT) has become the latest meme stock.

So many hedge funds have lined up to sell that the borrowing costs have skyrocketed to an incredible 550%. (DJT) has become the latest meme stock. The former president owns 60% of the shares. Accusations of insider trading and fraud are rife. If the former president loses the election, goes to jail, or dies as a result of his unhealthy lifestyle (he’s 50 pounds overweight) the shares become worthless. In other words, it’s a stock that no professional investor would touch with a ten-foot pole.

Every investment bubble creates its special instruments of self-destruction and this one is no different.

There were highly touted leveraged commodity and gold funds during the seventies, portfolio insurance during the eighties, money-losing tech companies with lots of “eyeballs” in the nineties, and subprime lending in the 2000s.

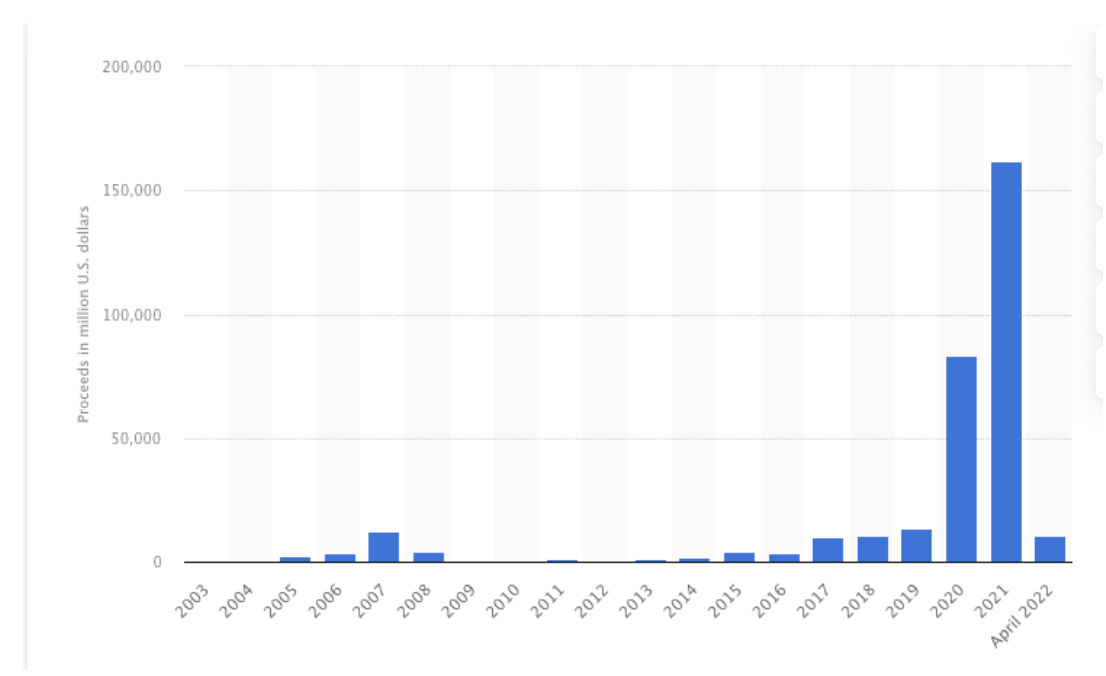

In this cycle, we have the Special Purpose Acquisition Companies, otherwise known as “SPACs.”

The goal of a SPAC is to raise money first on some generalized investment theme, and then merge with a target company to achieve those goals. This allows companies to go public while skipping most disclosure requirements.

SPACs have their advantages for some people. It enables start-up companies with no track record or earnings to go public faster without the costs and regulatory scrutiny of the burdensome public IPO process. Promoters promise to get investors into the next Amazon (AMZN) or Facebook FB) early.

Easier said than done.

Some $162 billion was raised for SPACs in 2021 followed by a much more modest $15 billion in 2022 and $125 million in 2023. The largest has been hedge fund manager Bill Ackman’s Pershing Square Tontine Holdings Ltd. (PSTH) at $4 billion. There is even a SPAC for SPACs, the Defiance Gen SPAC Derived ETF (SPAK).

The performance of SPACs so far has been dismal. There have been 915 SPACs created since 2015. Only 93 managed to invest their funds in a target company and only 29 of those have produced a profit. This was during one of the greatest runaway bull markets of all time.

You would have done better to simply buy the cheapest Vanguard index funds or 90-day T-bills. In the meantime, the issuers of SPACs for the most part became wealthy.

The quality of the management who had stepped forward to run SPACs has been mixed at best, including Ackman himself, who recently ran two gargantuan money-losing years back to back. They include former House Speaker Paul Ryan and NBA Hall of Famer Shaquille O’Neil, not exactly known as financial wizards.

Then there’s Nikola (NKLA), an electric/hydrogen vehicle company that has promised to take on Elon Musk, unfazed by the complete lack of a functioning vehicle. These shares have cratered by 92% since their market peak among multiple fraud allegations aimed at the founder.

The risks and limitations of SPACs are legion. You are essentially betting on the good faith and judgment of a single individual unmoored by any filings with the SEC. There are no guarantees they can achieve anything. These disclosures to the government are there to protect you. Without them, you are swimming without a swimsuit.

The conflicts of interest are enormous. SPAC issuers get to buy the equivalent of call options on their funds at deep discounts prior to the issue. When issuers make fortunes overnight with little money upfront, you want to run a mile.

And here is the big problem with SPACs. They are essentially roach motel investments, easy to check in but impossible to check out. Liquidity going in is unlimited but coming out is nil. You can often only redeem your investment at a huge discount, or if another buyer is willing to take out at any price. That makes marks to market challenging at best.

Investors that buy SPACs are giving up all the protections of SEC protections for much higher risks and lower returns.

Suffice it to say that if PT Barnum were working in the financial markets, he’d be up to his eyeballs with SPAC offerings.

Personally, I’ll give them a pass. You should too.

The Problem is that it’s a Dummy

https://www.madhedgefundtrader.com/wp-content/uploads/2020/10/dummy.png366550Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-04-23 09:02:542024-04-23 10:40:14Why most SPACs are a Scam

You’ve spent vast amounts of time, money, and effort to become options trading experts. You know the difference between bids and offers, puts and calls, exercise prices, and expiration days.

And you still can’t make any money.

Now what?

Where do you apply your newfound expertise? How do you maximize your reward versus your risk?

It is all very simple. Stick to five simple disciplines that I am about to teach you and you will suddenly find that the number of your new trades that are winners takes a quantum leap, and the money will start pouring into your trading account.

It’s really not all that hard to do. So here we go! 1) Know the Macro Picture

If you have a handle on whether the economy is growing or shrinking, you have a major advantage in the options market.

In a growing economy, you only want to employ bullish strategies, such as calls, call spreads, and short volatility plays.

In a shrinking economy, you want to execute bearish plays, such as puts, put spreads, and long volatility plays.

Remember the only thing that is useful is a view on what the economy is going to do NEXT. The government only publishes historical economic data, which is for the most part useless in predicting what is going to happen in the future.

Remember, the options market is all about discounting what is going to happen next.

And how do you find that out? Well, you could hire your own in-house staff economist. Or you could rely on economic research from the largest brokerage houses that all have their own economist.

Even the Federal Reserve puts out its own forecasts for economic growth prospects. However, all of these sources have notoriously poor track records. Listening to them and placing bets on their advice CAN get you into a world of trouble.

For the best possible read on the future of the U.S. and the global economy, there is no better place to go than Global Trading Dispatch, published by me, John Thomas, the Mad Hedge Fund Trader.

This is where the largest hedge funds, brokers, and yes, even the U.S. government go to find out what really is going to happen to the economy.

2) Looking for Great Industry Fundamentals

Do you want to give yourself another edge?

There are more than 100 different industries listed on the U.S. stock markets. However, only about five or 10 are really growing decisively at any particular time. The rest are either going nowhere or are shrinking.

In fact, you can find a handful of sectors that are booming while others are in outright recession.

If you are a major hedge fund, institution, or government, you may want to cover all 100 of those industries. Good luck with that.

If you are a small hedge fund, or an individual working from home, you will want to conserve your time and resources, skip most of the U.S.industry, and only focus on a handful.

Some traders take this a step further and only concentrate on a single high-growing, volatile industry, such as technology or biotech, or a single name, such as Netflix (NFLX), Tesla (TSLA), or Amazon (AMZN).

How do you decide which industry to trade?

Brokerage houses pump out more free research than you could ever read in a lifetime. Government reports tend to be stodgy, boring, and out of date. Big hedge funds keep their in-house research confidential (although some of it leaks out to me).

The Mad Hedge Fund Trader solves this problem for you by limiting its scope to a small number of benchmark, pathfinder industries, such as technology, banks, energy, consumer cyclicals, biotech, and cybersecurity.

In this way, we gain a handle on what is happening in the economy as a whole, while lining up rifle shots on the best options trades out there.

We want to direct you where the action is, and where we have a good handle on future earnings prospects.

It doesn’t hurt that we live on the edge of Silicon Valley and get invited to test out many technologies before they are made public.

3) The Micro Picture is Ideal

Once you have a handle on the economy and the best industries, it’s time to zero in on the best company to trade in, or the “MICRO” selection.

It’s always great to find a good target to trade in because positions in single companies deliver double or triple the returns compared to stock indexes.

That’s because the market will pay a far higher implied volatility for a single company than a large basket of companies.

Remember also that you are taking greater risks in trading individual companies. One single stock is subject to far greater even risk and a basket.

If the earnings come through as expected, everything is hunky-dory. If they don’t, the shares can drop by half in a heartbeat. Large indexes buffer this effect.

Of course, there are gobs of market research out there from brokers about individual companies. Some of it is right, some of it is wrong, but all of it is conflicted. Recommendations are either “BUY” or “HOLD.”

Brokers are loath to issue a “SELL” recommendation for a stock because it will eliminate any chance of that firm obtaining new issue business. Who wants to hire a broker to sell new stock with a “SELL” recommendation on their stock?

And brokerage firms don’t make their bread and butter on those piddling little discount commissions you have been paying them. They make it on new issues business. In fact, a new issue can earn as much as $100 million from a new issue for one firm.

I have been following about 100 companies in the leading market sectors for nearly half a century. Some of the managements of these firms have become close friends over the decades. So, I get some really first-class information.

When markets rotate to sectors and companies that I already know, I have a huge advantage. Needless to say, this gives me a massive head start when selecting individual names for options Trade Alerts.

4) The Technicals Line Up

I have never been a huge fan of technical analysis.

Most technical advice boils down to “If it’s gone up, it will go up more” or “If it’s gone down, it will go down more.”

Over time, the recommendations are accurate 50% of the time or are about equal to a coin toss.

However, the shorter the time frame, the more useful technical analysis becomes. If you analyze intraday trading, almost all very short-term movements can be explained in technical terms. This is entirely how day traders make their livings.

It’s a classic case of if enough people believe something, it becomes true, no matter how dubious the underlying facts may be.

So, it does behoove us to pay some attention to the charts when executing our trades.

Talk to old-time investors and you will find that they use fundamentals for long-term stock selection and technicals for short-term order execution.

Talk to them some more and you find the best fundamentalists sound like technicians, while savvy technicians refer to underlying fundamentals.

Get the technicals right, and you can provide one additional reason for your trade to work.

5) The calendar is favorable There is one more means of assuring your trades turn into winners.

According to the data in the Stock Trader’s Almanac, $10,000 invested at the beginning of May and sold at the end of October every year since 1950 would be showing a loss today.

Amazingly, $10,000 invested on every November 1 and sold at the end of April would today be worth $702,000, giving you a compound annual return of 7.10%.

Of the 62 years under study, the market was down in 25 May-October periods, but negative in only 13 of the November-April periods, and down only three times in the past 20 years!

There have been just three times when the "good six months" have lost more than 10% (1969, 1973 and 2008), but with the "bad six months" time period there have been 11 losing efforts of 10% or more.

Yes, it may be disturbing to learn that we ardent stock market practitioners might in fact be the high priests of a strange set of beliefs. But hey, some people will do anything to outperform the market.

It is important to remember that this cyclicality is not 100% accurate, and you know the one time you bet the ranch, it won’t work.

So, there we have it.

Adopt these five simple disciplines and you will find your success rate on trades jumps from a coin toss to 70%, 80%, or even 90%.

In other words, you convert your trading from an endless series of frustrations to a reliable source of income.

If a potential trade meets only four of these five criteria, please do it with your money and not mine. Your chances of making money have just declined.

And I bet a lot of you poor souls execute trades all the time that meet NONE of these criteria.

Get the tailwinds of the economy, your industrial call, your company picks, the technicals, and the calendar working for you, and all of a sudden you’re a trading genius.

It only took me half a century to pull all this together. Hopefully, you can learn a little bit faster than that.

I hope it all works for you.

This is John Thomas signing off saying good luck and good trading.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/08/John-Thomas-image-e1535492954635.jpg388350MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2024-03-28 09:02:432024-03-28 10:54:52How to Reliably Pick a Winning Options Trade

Malls are dying. Commerce is moving online at a breakneck pace. Investing in retail is a death wish.

No less a figure than Bill Gates, Sr. told me before he died that in a decade, malls would only be inhabited by climbing walls and paintball courses, and that was a decade ago.

Except it didn’t quite work out that way. Lesser quality malls are playing out Mr. Gates’ dire forecast. But others are booming. It turns out that there are malls, and then there are malls.

Let me expand a bit on my thesis.

We are just entering a decade-long decline in interest rates, probably starting in June. Malls are highly leveraged entities that often are financed by Real Estate Investment Trusts) REITS. That makes some mall-based REITS some of the most attractive investments in the market.

Technology is moving forward at an exponential rate. As a result, product performances are improving dramatically, while costs are falling. Commodity and energy prices are also rising, they are but a tiny fraction of the cost of production.

In other words, DEFLATION IS HERE TO STAY!

The nearest hint of real inflation won’t arrive until the late 2020s, when Millennials become big spenders, driving up the cost of everything.

So, let's go back to the REIT thing. Real Estate Investment Trusts are a creation of the Internal Revenue Code, which gives preferential tax treatment for investment in malls and other income-generating properties.

There are 1,100 malls in the United States. Some 464 of these are rated as B+ or better and are concentrated in the biggest spending parts of the country (San Francisco, North New Jersey, Greenwich, CT, etc).

Trading and investing for a half-century, I have noticed that most managers are backward-looking, betting that existing trends will continue forever. As a result, their returns are mediocre at best and terrible at worst.

Truly brilliant managers make big bets on what is going to happen next. They are constantly on the lookout for trend reversals, new technologies, and epochal structural changes to our rapidly evolving modern economy.

I am one of those kinds of managers.

These are not your father’s malls. It turns out the best quality malls are booming, while second and third-tier ones are dying the slow painful death that Mr. Gates outlined.

It is all a reflection of the ongoing American concentration of wealth at the top. If you are selling to the top 1% of wealth owners in the country, business is great. If fact, if you cater even to the top 20%, things are pretty damn fine.

You can see this in the top income-producing tenants in the “class A” malls. In 2000, they comprised J.C. Penney. Sears, and Victoria’s Secret. Now Apple, L Brands, and Foot Locker are sought-after renters. Put an Apple store in a mall, and it is golden.

And what about that online thing?

After 25 years of online commerce, the business has become so cutthroat and competitive that profit margins have been beaten to death. You can bleed yourself white watching Google AdWords empty out your bank account. I know, because I’ve tried it.

Many online-only businesses are now losing money, desperately searching for that perfect algorithm that will bail them out, going head-to-head against the geniuses at Amazon.

I open my email account every morning and find hundreds of solicitations for everything from discount deals on 7 For All Mankind jeans, to the new hot day trading newsletter, to the latest male enhancement vitamins (although why they think I need the latter is beyond me).

Needless to say, it is tough to get noticed in such an environment.

It turns out that the most successful consumer products these days have a very attractive tactile and physical element to them. Look no further than Apple products, which are sleek, smooth, and have an almost sexual attraction to them.

I know Steve Jobs drove his team relentlessly to achieve exactly this effect. No surprise then that Apple is the most successful company in history and can pay astronomical rents for the most prime of prime retail spaces.

It turns out that “Clicks to Bricks” is becoming a dominant business strategy. A combination of the two is presently generating the highest returns on investment in retail today.

People start out by finding a product online and then going to the local mall to try it on, touch it, and feel it. Apple does this.

Research shows that two-thirds of Millennials prefer buying their clothes and shoes at malls. Once there, the probability of a serendipitous purchase is far greater than online, anywhere from 20% to 60% of the time.

This explains why pure online businesses by the hundreds are rushing to get a foothold in the highest-end malls.

Immediate contact with a physical customer gives retailers a big advantage, gaining them the market intelligence they need to stay ahead of the pack. In “fast fashion” retailers like H&M and Uniqlo, which turn over their inventories every two weeks, this is a really big deal.

There’s more to the story. Malls are not just shopping centers they have become entertainment destinations as well. With an ever-increasing share of the population chained to their computers all day, the demand for a full out-of-the-house shopping, dining, and entertainment family experience is rising.

Notice how Merry Go Rounds have started popping up at the best properties? Imax Theaters are spreading like wildfire. And yes, they have climbing walls too. I haven’t seen any paintball courses yet, but the guns and accessories are for sale.

And notice that theaters are now installing first-class adjustable heated seats and will serve you dinner while the movie is playing. (Warning: if you eat in the dark, you will end up wearing half of it home).

This is why all of the highest-rated malls in the country are effectively full. If you want space, there you have to wait in line. REIT managers pray for tenant bankruptcies so that can jack up rents on the next incoming client or pivot their strategy towards the newest retail niche.

Malls are also in the sweet spot in the alternative energy game. Lots of floor space means plenty of roof space. That means they can cash in on the 30% federal investment tax credit for solar roof installations. Some malls in sunny southwestern states are net power generators, effectively turning them into min local power utilities. By the way, the cost of solar has recently crashed.

Fortunately for us investors, we are spoiled for choice in the number of securities we can consider, most which can now be bought for bargain basement prices. Many have a return on investment of 9-11%, a portion of which is passed on to the end investor.

There are now 25 REITs in the S&P 500. The sector has become so important that the ratings firm is about to create a separate REIT subsector within the index.

According to NAREIT.com (click here for the link), these are some of the largest mall-related investment vehicles in the country.

Simon Growth Property (SPG) is the largest REIT in the country, with 241 million square feet in the US and Asia. It is a fully integrated real estate company that operates from five retail real estate platforms: regional malls, Premium Outlet Centers, The Mills, community/lifestyle centers, and international properties. It pays a 4.88% dividend.

Macerich Co. (MAC) is a California-based company that is the third largest REIT operator in the country. It has been growing through acquisitions for the past decade. It pays a 5.31% dividend.

Mind you, REITs are not exactly risk-free investments. To get the high returns you take on more risk. We remember how disastrously the sector did when the credit crunch hit during the 2009 financial crisis. Many went under, while others escaped by the skin of their teeth.

There are a few things that can go wrong with malls. Local economies can die, as it did in Detroit. Populations age, shifting them out of a big spending age group. And tax breaks can be here today and gone tomorrow.

These are all highly leveraged companies, so any prolonged rise in interest rates could be damaging. But as I pointed out below, there is little chance of that in the near future.

The bottom line here is that we are seeing anything but the death of the mall. It just depends on the mall.

All in all, if you are looking for income and yield, which everyone on the planet is currently pursuing, then picking up some REITs could be one of your best calls of the year.

See You At the Mall

https://www.madhedgefundtrader.com/wp-content/uploads/2016/04/Mall-e1461879279977.jpg303400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2024-03-26 09:04:412024-03-26 12:20:27The Death of the Mall

Ignore the lessons of history, and the cost to your portfolio will be great. Especially if you are a bond trader!

Meet deflation, upfront and ugly.

If you look at a chart for data from the United States consumer prices are rising at an annual 3.2% rate. The long-term average is 3.0%.

This is above the Federal Reserve’s own 2.0% annual inflation target, with most of the recent gains coming from housing costs.

We are not just having a deflationary year or decade. We may be having a deflationary century.

If so, it will not be the first one.

The 19th century saw continuously falling prices as well. Read the financial history of the United States, and it is beset with continuous stock market crashes, economic crises, and liquidity shortages.

The union movement sprung largely from the need to put a break on falling wages created by perennial labor oversupply and sub-living wages.

Enjoy riding the New York subway? Workers paid 10 cents an hour built it 125 years ago. It couldn’t be constructed today, as other more modern cities have discovered. The cost would be wildly prohibitive. Look no further than the California Bullet Train, now expected to cost $100 billion. A second transbay tube in San Francisco will cost $29 billion.

The causes of the 19th-century price collapse were easy to discern. A technology boom sparked an industrial revolution that reduced the labor content of end products by ten to a hundredfold.

Instead of employing 100 women for a day to make 100 spools of thread, a single man operating a machine could do the job in an hour.

The dramatic productivity gains swept through the developing economies like a hurricane. The jump from steam to electric power during the last quarter of the century took manufacturing gains a quantum leap forward.

If any of this sounds familiar, it is because we are now seeing a repeat of the exact same impact of accelerating technology. Machines and software are replacing human workers faster than their ability to retrain for new professions. If you want to order a Big Mac at McDonald’s these days, you need a PhD in Computer Science from MIT. The new stores have no humans to take orders.

This is why there has been no net gain in middle-class wages for the past 40 years. That is until the pandemic hit which created labor shortages that are still working their way out. It is the cause of the structurally high U-6 “discouraged workers” employment rate, as well as the millions of millennials still living in their parent’s basements.

To the above add the huge advances now being made in healthcare, biotechnology, genetic engineering, DNA-based computing, and big data solutions to problems. Did anyone say “AI”?

If all the major diseases in the world were wiped out, a probability within 10 years, how many healthcare jobs would that destroy?

Probably tens of millions.

So the deflation that we have been suffering in recent years isn’t likely to end any time soon. In fact, it is just getting started.

Why am I interested in this issue? Of course, I always enjoy analyzing and predicting the far future, using the unfolding of the last half-century as my guide. Then I have to live long enough to see if I’m right.

I did nail the rise of eight-track tapes over six-track ones, the victory of VHS over Betamax, the ascendance of Microsoft (MSFT) operating systems over OS2, and then the conquest of Apple (AAPL) over Motorola. So, I have a pretty good track record on this front.

For bond traders especially, there are far-reaching consequences of a deflationary century. It means that there will be no bond market crash, as many are predicting, just a slow grind up in long-term bond prices instead.

Amazingly, the top in rates in this cycle only reaches the bottom of past cycles at 5.49% for ten-year Treasury bonds (TLT), (TBT).

The soonest that we could possibly see real wage rises will be when a generational demographic labor shortage kicks in during the late2020s.

I say this not as a casual observer, but as a trader who is constantly active in an entire range of debt instruments.

I just thought you’d like to know.

Hey, Have You Heard About John Deere?

https://www.madhedgefundtrader.com/wp-content/uploads/2019/07/john-thomas-08.jpg400400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2024-03-20 09:02:142024-03-20 09:57:37Welcome to the Deflationary Century

With California having cut the amount that PG&E has to pay for third-party home-generated solar energy by 75% this year, the price of solar panels has crashed. That’s why SunPower (SPWR) shares have just cratered from $50 to $3.

As a result, deals of the century are being offered almost everywhere in the US. This is fortuitous as the price of public utility-generated electricity is rocketing everywhere by up to 15% a year.

It’s just a question of how long it takes Moore’s law-type efficiencies to reach exponential growth in the solar industry.

Solar electricity accounts for 4.75% of total US power generation, up from 3.96% in 2022, and compared to 27.3% in California. That means we are only five doublings away from 100% when energy essentially becomes free.

The next question beyond the immediate trading implications is, “What’s in it for you?”

I should caution you that after listening to more than 20 pitches, almost all of the information you get from fly-by-night solar installation salesmen is inaccurate. Most don’t know the difference when it comes to a watt, an ohm, or a volt.

I think they were mostly psychology or philosophy majors if they went to college at all.

The promised 25-year guarantees are only as good as long as the firms stay in business, which for many poorly run operations will not be long.

Talking to these guys reminded me of the aluminum siding salesman of yore. It was all high pressure, exaggerated benefits, and relentless emailing.

I come to this issue with some qualifications of my own, as I have been designing and building my own solar systems for the past 60 years.

During the early 1960s, when solar cells first became available to the public through Radio Shack (RIP), I used to create my own simple sun-powered devices from scratch. But when I measured the output, I would cry, finding barely enough power to illuminate a flashlight bulb.

We have come a long way since then. For years, I watched my organic bean-sprout-eating, Birkenstock-wearing neighbors install expensive, inefficient arrays because it was good for the environment, politically correct, and saved the whales.

However, when I worked out the breakeven point compared to conventional power sources, it stretched out into decades. So, I held off.

It wasn’t until 2015 when solar price/performance hit the breakeven sweet spot acceptable for me, about six years. I actually earned my money back in only four years, thanks to PG&E’s rapid price increases. Thanks to global warming my solar system is also becoming more efficient, not less. Why, I can’t imagine although higher heat might be bringing greater output.

Then I launched into overdrive, attempting to get the best value for money and game the many financing alternatives.

The numbers are now so compelling, that even a number-crunching, blue state-hating Texas oilman should be installing silicon on his roof.

A lot are.

My effort was the father of the many solar research pieces and profitable Trade Alerts you have received since.

Here are my conclusions up front: Learn about “tier shaving” from your local utility, and buy, don’t lease. All electrical utility plans are local.

First, about the former.

Every utility has a tiered system of charging customers on a prorated basis. A minimal amount of power for a low-income family of four living in a home with less than 1,500 square feet, about 20% of the U.S. population, costs about 10 cents a kilowatt hour.

This is a function of the high level of public power utility regulation in the U.S., where companies are granted local monopolies. There are a lot of trade-offs, local politics, and quid pro quos that are involved in setting electric power rates.

My local supplier, PG&E (PGE) has five graduated billing tiers, with the top rate at 55 cents a kWh for mansion-dwelling energy hogs like me (one Tesla in the garage and a Cybertruck on the way).

In order to minimize your up-front capital cost, you want to buy all the power you can at the poor person rate, and then eliminate the top four tiers entirely. Do this, and you can cut the cost of your new solar system by half.

Your solar provider will ask for your recent power bills and will help you design a system of the right size.

Warning! They will try to sell you more than you need. After all, they are in the solar panel-selling business, not the customer-value-for-money delivery business.

On the other hand, if you are a scientist or engineer, you can simply calculate these figures yourself. In my case, I use 18,000 kWh a year, but by installing only a 9,000 kWh/year system, my monthly power bill dropped from $500 to $50 a month.

This system cost me $32,000, or $22,400 net of the 30% alternative energy investment tax credit, giving me a breakeven point of four years and eight months.

Don’t focus too much on the panels themselves, as they are only 25% of a system’s costs. The big installers constantly play a myriad of panel manufacturers off against each other to get the cheapest bulk supplies.

The majority of the expense is for labor, the inverter needed to convert DC solar power to AC wall plug power, and permitting.

As for me, Mr. First Class All the Way, I specified only 19 of the best American-made, most efficient 335 kWh SunPower (SPWR) panels.

If I had settled for lower-cost 250 kWh imported panels and just bought more of them, I would have saved a few thousand bucks. That’s fine if you have the roof space.

One other frill I ordered was a top-of-the-line SunPower SPR-6000m inverter, which includes two 110-volt AC outlets. Many solar systems won’t work without access to the grid to run the inverter and software.

This will enable me to operate independently of the grid in case it is knocked out by an earthquake or storm, and power a few select appliances, such as my refrigerator, cell phones, laptop, and, of course, my car.

Once you get your connection notice from your utility, you enter electricity Nirvana, selling power at a premium during the day, and buying it back at a discount at night.

You are, in effect, using the grid as a giant storage device, or battery.

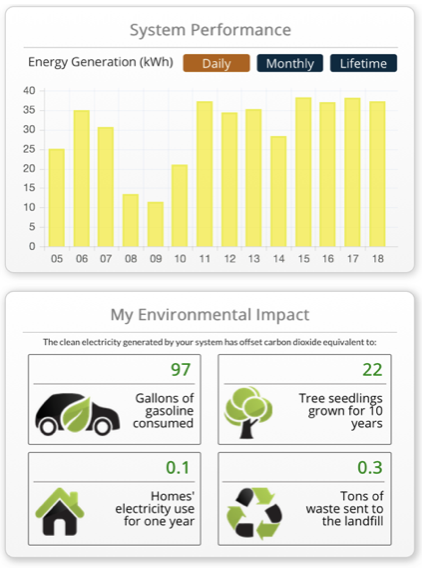

You can then log into your account online and measure how much your solar panels are generating in San Francisco, even from places as remote as Africa, as I did last summer.

My statement is posted below, showing my roof is happily generating about 38 kW a day, or one full Tesla 100kW battery recharge every 2 1/2 days.

Since my system is in California, it also expresses the solar energy produced in terms of gallons of gasoline equivalent, tree seedlings grown over 10 years, an average home’s power consumption for one year, or the number of tons of waste sent to a landfill.

Call this “feel good” with a turbocharger.

At the end of every 12 months, the utility will then perform a “true up” calculation. If you produce more power than you used, the utility owes you a check.

Buzzkill warning!

PG&E has to pay me only its lowest marginal cost of power, or 4 cents/kWh for the excess power I produce. That is why it pays to underbuild your system, which for me costs $2.49/kWh to install, net of the tax credit.

This was the quid pro quo that enabled PG&E to agree to the whole plan in the first place. So, you won’t get rich off your solar system.

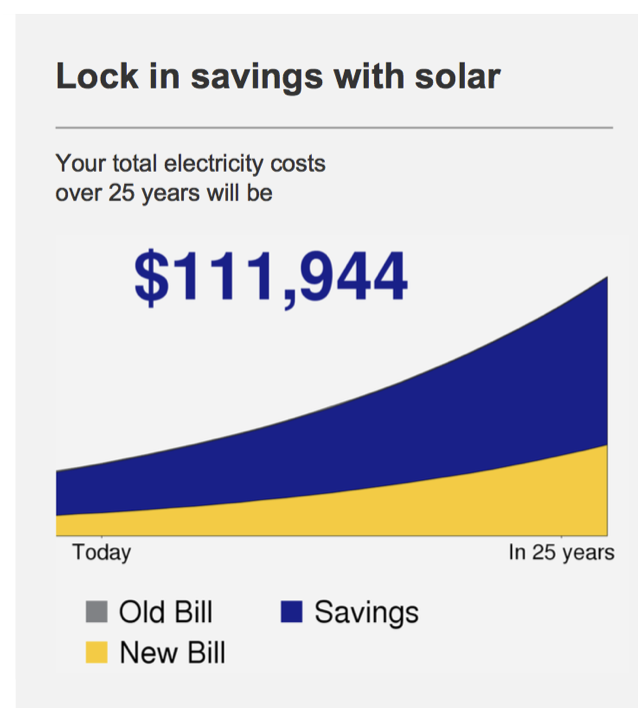

I am now protected against any price increasefor electricity for the next 25 years!

PG&E has already notified me of back-to-back 7.5% annual rate increases for the next two years to pay for the replacement of their aging, dilapidated infrastructure, a problem that is occurring nationally.

Oh, and my $32,000 investment has increased the value of my home by $64,000, according to my real estate friend.

Now for the lease or buy question. If you don’t have $32,000 for a solar installation, (or $16,000 for a normal size house with no Tesla’s), or you want to preserve your capital for your trading account, you may want to lease from a company such as Solar City.

The company will design and install an entire system for you for no money down and lease it to you for 20 years. But after your monthly lease payment, Solar City will end up keeping half the benefit, and raise your cost of electricity annually.

In my case, my monthly power bill will have dropped from $450 to $250. And you don’t get any 30% investment tax credit. However, this is still cheaper than continuing to buy conventional power.

So if you can possibly afford it, buy, don’t rent.

This being Silicon Valley, niche custom financing firms have emerged to let you have your cake and eat it, too.

Dividend Solar (click here for their site) will lend you the money to buy your entire system yourself, thus qualifying you for the investment tax credit.

As long as you use the tax credit to repay 30% of your loan principal within 15 months, the interest rate stays at 6.49% for the 20-year life of the loan. Otherwise, the interest rate then rises to a credit card like 9.99%. A FICO score of only 690 gets you in the door.

There are a few provisos to add.

You can’t install solar panels on clay or mission tile roofs popular in the U.S. Southwest (where the sun is), or tar and gravel roofs, as the breakage or fire risk is too great. The racks that hold the panels down in hurricane-force winds simply won’t fit.

If you want to maintain your aesthetics, you can take the mission tiles off, install a simple composite shingle roof, bolt your solar panels on top, and then put back the clay tiles back around the edges. That way it still looks like you have a mission tile roof.

Also, it is best to install your system in the run-up to the summer solstice, when the days are longest and the sunshine brightest. Solar systems produce 400% more power on the longest day of the year compared to the shortest, because of the lower angle of the sun’s rays hitting the Northern Hemisphere.

Tesla (TSLA) has added a whole new chapter to the solar story.

It offers the PowerWall, a 13.5 kW home storage battery that will cost up to $7,000 (click here for “The Solar Missing Link is Here!”)

The development is made possible by the enormous economies of scale for battery manufacturing made possible by the new Gigafactory near Reno, Nevada.

The Gigafactory will double world lithium-ion battery capacity in one shot. Plans for a second Gigafactory are already in the works.

This will permit homeowners to use their solar panels to charge batteries during the day, and then run off them at night, making them fully energy-independent. Yes, a total American solar energy supply in 15 years sounds outrageous, insane, and even ludicrous (to use some of Elon Musk’s favorite words).

But, so did the idea of a 3-gigahertz laptop microprocessor for a mere $1,000 24 years ago, when Moore’s law first applied.

The graphics for my own solar power supply are below:

SunPower SPR-6000m

https://www.madhedgefundtrader.com/wp-content/uploads/2021/06/solar-pannels.png394342Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2024-03-13 09:02:002024-03-13 10:34:09How to Buy a Solar System

Old Benjamin Franklin, one of the fathers of our country, was a pretty smart guy.

Not only was he a publisher, scientist, postmaster general, ambassador to the court of Louis the XVI, and delegate to the constitutional convention.

He also understood the basic mathematics that underlay modern investment theories centuries ahead of time.

When the United States was first founded, there was widespread belief in Europe that its experimental Republican form of government would soon fail.

After all, democracy hadn’t succeeded since the days of ancient Greece. Why should it now? The fact that the US was chronically broke didn’t help either.

One French mathematician, Charles-Joseph Mathon de la Cour, dared anyone to make a multi-century bet that the country would not survive.

Franklin happily took him up on it.

In 1789, he added to his will a codicil that endowed a trust with the city of Boston, where he was born, and the city of Philadelphia, where he built his career, with £1,000 each.

He specified that half the money be distributed in a century, and the balance in 200 years.

That initial investment equated to $5,000 at the time, or about $100,000 today in inflation-adjusted dollars. The British pound was the preeminent reserve currency of the day, and was good as gold, as it was still exchangeable into the yellow metal on demand.

Franklin died the following year days short of the age of 85.

The trust money was primarily invested in loans at a 5% interest rate in loans to young men under the age of 25 to finance apprenticeships in the trades. Later, it financed home mortgages.

So how did Ben do?

After the first 100 years, the Boston fund was worth $391,000, and half the money was eventually used to establish the Franklin Technical School, a two-year college that is still in operation today (click here for the link).

In 1990, at the end of the second century, the remaining Boston half was worth more than $5 million.

The money was promptly divvied up, with 26% going to the city, and the balance going to the State of Massachusetts. Much of the money went into the endowment of the Franklin Technical School.

Franklin did less well in his adopted hometown of Philadelphia. Corrupt politicians diverted some funds during the 19th century. Still, by 1990, the initial £1,000 had grown to $2 million.

The funds were used to set up a scholarship fund for Philadelphia high school graduates.

Interestingly, the two trusts never came close to their 200-year theoretical maximum value in the hundreds of millions of dollars. That’s because several early borrowers defaulted on their loans.

The Civil War also no doubt took its toll.

This story highlights the value of compounding interest, well known to all savvy money managers.

Every math student knows the fable of the mathematician who invented the game of chess for an ancient potentate. As a reward, he asked for a grain of rice to be doubled with each square on a chessboard. The king agreed.

The servant deserved the entire kingdom well before he reached the 64th square. The final total worked out to 18,446,744,073,709,551,615 grains of rice, or 66 trillion metric tonnes, which is 435,000 times the displacement of the Queen Mary 2.

The fairytale doesn’t tell us if the clever, mathematician ever collected his reward.

Investment legend Warren Buffett is also familiar with the concept of compounding interest. He invests only in companies with great cash flows and dividends and rarely sells.

He entered the market in 1942 when the Dow Average traded around $100, just before the tide was turned for WWII.

Timing is everything in this business.

He entitled his authorized biography “Snowball”, a reference to compounding, and a great read by the way.

Even I have my own two cents to throw in here on the compounding value of investments over the long term.

Before Morgan Stanley (MS) went public in 1986, I was allocated a part ownership of the private partnership at 25 cents a share. That is about one-third of the annualized dividend for today’s shares.

Today, they are worth $300 on a split-adjusted basis, including dividends. And since I never sold them, I never had to pay tax on the gain either.

As for how many shares I got, I’m not telling!

The original £2,000 came from Franklin’s salary for the three years he spent as the governor of Pennsylvania. He believed that the nation’s leaders should work for free and sought to set an example.

Unfortunately, it was an idea that never caught on.

The last amendment to the US Constitution, the 27th, provided for pay increases for members of Congress and was passed in 1992. It only took 203 years to ratify.

Franklin didn’t limit his charity to the Boston and Philadelphia Trusts. He also created an additional fund to award a silver medal to the most creative high school students of the day.

It is now known as the Franklin Legacy Prize Medal and is the oldest continuously funded scholarship in the country, awarded every year since 1793.

As for our friend, Charles-Joseph Mathon de la Cour, he didn’t fare so well. His head was chopped off by a guillotine only four years later during the French Revolution.

Over the 200 years in question, five different republics ruled France, which suffered through several revolutions, civil wars, and invasions.

As Warren Buffett never tires of telling fellow investors, it is a terrible idea to bet against America.

Old Ben Had a Way With Money

Franklin Legacy Prize Medal

https://www.madhedgefundtrader.com/wp-content/uploads/2018/04/Ben-Franklin-story-2-image-1-e1523047087935.jpg222500MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-11-29 09:02:592023-11-29 10:52:21How to "Snowball" Your Fortune with Benjamin Franklin

I’ll do anything to postpone aging, as regular readers of this letter already know.

So when my doctor told me that she could extend the life of my knees by ten years with a stem cell injection, I was all for it.

You better pay attention too.

Stem cells, along with CRISPR gene editing (CRSP), are two hyper-accelerating medical technologies that promise to cure your ills, extend your life, and make you fabulously rich along the way.

Have I got your attention?

When my doc confirmed that she was already getting spectacular results from her other elderly patients, such as the dramatic regrowth of knee cartilage, it was like pushing on an open door.

Yes, these are the famous well-worn 71-year-old knees you have heard so much about over the past 15 years that hike and snowshoe 2,000 miles a year with a 50-pound backpack.

My doc is not lightweight. She is the orthopedic surgeon for the US Ski Team at Lake Tahoe, which is why I sought her out in the first place.

As a UCLA-trained biochemist, I have known about stem cells for most of my life. They only left the realm of science fiction two decades ago.

Early sources of stem cells relied on stillborn human fetuses, creating a religious and political firestorm that led to severe restrictions, a funding drought, or outright bans.

During the 2000’s, California was almost the only state that permitted stem cell research.

Since then, the technology has developed to the point where it can be easily harvested throughout the human body.

Easy, except when the source is the bone marrow in your backbone.

“You may feel a slight twinge,” said my doctor, as she flushed the air out of a gigantic horse needle the width of a straw. “I only have to hammer this needle into your hip bone 20 or 25 times to get the marrow I need.”

This was NOT in the glossy brochure I had been provided.

I said, “Don’t worry, Marines are immune to pain.”

“Does that work?” she asked.

“No, not really,” I replied, grimacing. “But it sounds good.”

I felt every single blow and tried to imagine myself on a faraway tropical island. It turned out to be 55 blows. I counted.

Once she obtained the 10cc she needed, she popped it into a small centrifuge to separate the stem cells (clear) from the red blood cells (red).

She then used an ultrasound machine to inject my stem cells at the exact right spot in both of my knees.

Being the true journalist that I am, I took pictures throughout the entire procedure with my iPhone 15 (see below).

The problem with advanced, experimental treatments is that they are not covered by your health insurance. Still, I thought $2,000 for ten years of extra life for both knees was a bargain.

Stem cells are undifferentiated cells that can transform into specialized cells such as the heart, neurons, liver, lung, skin, and so on, and can also divide to produce more stem cells.

You can think of stem cells as chemical factories generating vital growth factors that can help to reduce inflammation, fight autoimmune diseases, increase muscle mass, repair joints, and even revitalize skin and grow hair.

Goodbye, Rogaine!

When you are young, you have oodles of these cells, which is why kids so rarely die from dread diseases.

However, as you age, your exposure to too much sunlight at the beach, too many chemicals in the food and water you eat and drink, and natural background radiation degrades your DNA and reduces your stem cell supply.

Supplies of stem cells diminish as much as 100 to 10,000-fold in different tissues and organs. Welcome to old age, and eventually death.

The procedure I underwent is called Autologous Adult Stem Cells Treatment.

The great thing about it is that since you are using your cells, the risk of rejection or infection is minimal. And they are free!

This approach has become the must-go treatment for the wealthy seeking to repair aging, sagging parts of their bodies.

They are often sold with vacation packages in exotic third-world countries where regulation and medical malpractice suits are nonexistent.

The fact that the treatments are now becoming widely available in the US testifies to their effectiveness.

Do any search on stem cell treatments, rejuvenation, or life extension and you will find hundreds and hundreds of private clinics offering to do so for high prices.

California leads the nation with 109 clinics (including 18 in Beverly Hills alone), followed by New York and Texas.

Just follow the money.

The market is now on fire and is expected to reach $270 billion by 2025.

As a result, several breakthroughs in longevity are just around the corner.

The industry is now branching out into fields considered unimaginable just a few years ago. I’ll cover some of the highlights.

Imagine using your stem cells to repair not only your knees but any other organ. This is already being done in the lab with animal trials.

In Japan, they are growing human eyes from scratch, including lenses and corneas.

At Stanford, stem cells are bringing dramatic improvements in stroke victims.

At USC they are deployed to bring rapid repairs to those with severe spinal cord injuries.

Several private firms have sprung up to facilitate the banking of your stem cells through cryogenic freezing, such as Lifebank. Just harvest them when you are young for future use.

Better yet, get born to wealthy parents who will pay to have your birth placenta and umbilical cord frozen, the two richest sources of stem cells known.

The key term to search for your investment strategy is Mesenchymal Stem Cells, the major stem cells for cell therapy, or MSCs.

These cells can differentiate into vital cells that can be used to cure autoimmune disease, cardiovascular disease, liver disease, and cancer.

There are now several hundred clinical trials involving these cells underway.

A more adventurous strategy is to buy the stem cells of others and have them injected into yourself, a procedure known as parabiosis.

A company in Monterey, CA named Ambrosia is doing exactly this for $8,000 a patient. The goal here is to reverse aging across every major organ system. Of course, I think there’s got to be a trade here.

Not so fast.

Almost all stem cell efforts are now confined to the research labs of major universities or are buried inside large biotech and drug companies.

A few researchers have spun off to set up their own private companies with substantial venture capital backing.

That said, there are a few peripheral listed plays.

Thermo Fischer Scientific (TMO) provides a range of tools and supplies scientists need to pursue stem cell research (click here for their site at https://www.thermofisher.com/us/en/home.html

Regeneron (REGN) uses stem cells to pursue a broad range of serious medical conditions, including ophthalmology, cancer, rheumatoid arthritis, asthma, atopic dermatitis, pain, and infectious diseases. Visit their site at https://www.regeneron.com

The problem with the entire biotech sector is that it can take a long time to deliver new drugs and procedures to market. So these may be next year's investments, instead of next week's ones.

And how are my knees doing? I knew you would ask.

A little swelling in my knees went away in a day. I sat funny for a few more days, thanks to my bone marrow extraction.

It will take about six months before any real growth in new cartilage in my knees can be measured with an MRI scan, which I have scheduled. So far, the results have been great.

But you know what?

My knees have not hurt an iota, despite my regular tortuous exercise regime. And I think that, right there, is a win.

If it works, my doctor wants to extract fat cells from my middle, known as Adipose Cells, and inject their stem cells, into my knees.

Talk about killing two birds with one stone!

This Won’t Hurt a Bit

https://www.madhedgefundtrader.com/wp-content/uploads/2017/01/Doctor-with-Blood-e1485222275379.jpg396400MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-11-16 09:02:512023-11-16 10:54:28The Stem Cells in Your Investment Future

And if you lose your job to AI in five years you will be one of the lucky ones.

It’s possible that your job is already gone, they just haven’t told you yet.

The shocking conclusion I am getting from dozens of research fronts is that artificial intelligence and automation are accelerating far faster than anyone realizes.

It is all extraordinarily disruptive.

This will cause corporate profits to rocket and share prices to soar but at the price of higher nationwide political instability.

A big leap took place at the beginning of the year when suddenly it appeared that everything got a lot smarter.

My local Safeway has started using self-checkout scanners to enable customers to avoid the long lines still operated by humans.

I hate them because I can never get them to scan pineapples correctly.

Soon, Amazon (AMZN) opened a supermarket in Seattle where there is no checkout stand at all. You simply just pick up whatever products you want, and it will scan them all on the way out to the parking lot.

Once the software is perfected (it is self-learning), and the consumers are educated, 5 million checkout clerks will be joining the unemployment lines.

Uber has been testing self-driving taxis in Phoenix, AZ, with sometimes humorous results. It seems that other human-driven cars like crashing into them. There has been one fatality so far when the human safety driver was caught texting.

When they figure this out, probably in two years, 180,000 taxi drivers and 600,000 Uber and Lyft drivers will have to hit the road.

Some 3 million truck drivers will be right behind them.

Notice that I am only a couple of paragraphs into this peace and already 8,780,000 jobs are about to imminently disappear out of a total of 150 million in the US.

Two decades from now, only vintage car collectors or the very poor will be driving their cars if Tesla (TSLA) has anything to do with it.

I let my Model X drive me around most of the time. It has reaction time, night vision, and a 360-degree radar system that are far better than my 71-year-old senses.

However, all new Teslas now come equipped with the hardware to use it. They are all only one surprise overnight software upgrade away from the future.

And it's not just the low-end high school dropout jobs that are being thrown in the dustbin of history.

Automation is now rapidly moving up the value chain.

A rising share of online news is machine-generated and is targeting you based on your browsing history. You just didn’t know it.

It was a major influence in the last election.

Blackrock (BLK), the largest fund manager in the country, has announced that it is laying off dozens of stock analysts and turning to algorithms to manage its vast $8.6 trillion in assets under management.

As the April 15 tax deadline relentlessly approaches, you are probably totally unaware that an algorithm prepared your return, particularly if you use a low-end service like H & R Block (HRB) or Intuit’s (INTU) TurboTax.

Because of the simultaneous convergence of multiple technologies, half of all current jobs will likely disappear over the next 20 years.

If this sounds alarming, don’t worry.

We’ve been through all of this before.

From 1900 to 1950 farmers fell from 40% to 2% of the labor force. The food output of that 2% has tripled over the last 60 years, thanks to improved seed varieties and farming methods.

The remaining 38% didn’t starve.

They retrained for the emerging growth industries of the day, automobiles, aircraft, and radio.

But there had to be a lot of pain along the way.

More recently, some 30% of all job descriptions listed on the Department of Labor website today didn’t exist 20 years ago.

Yes, disruption happens fast.

And here’s where it gets personal.

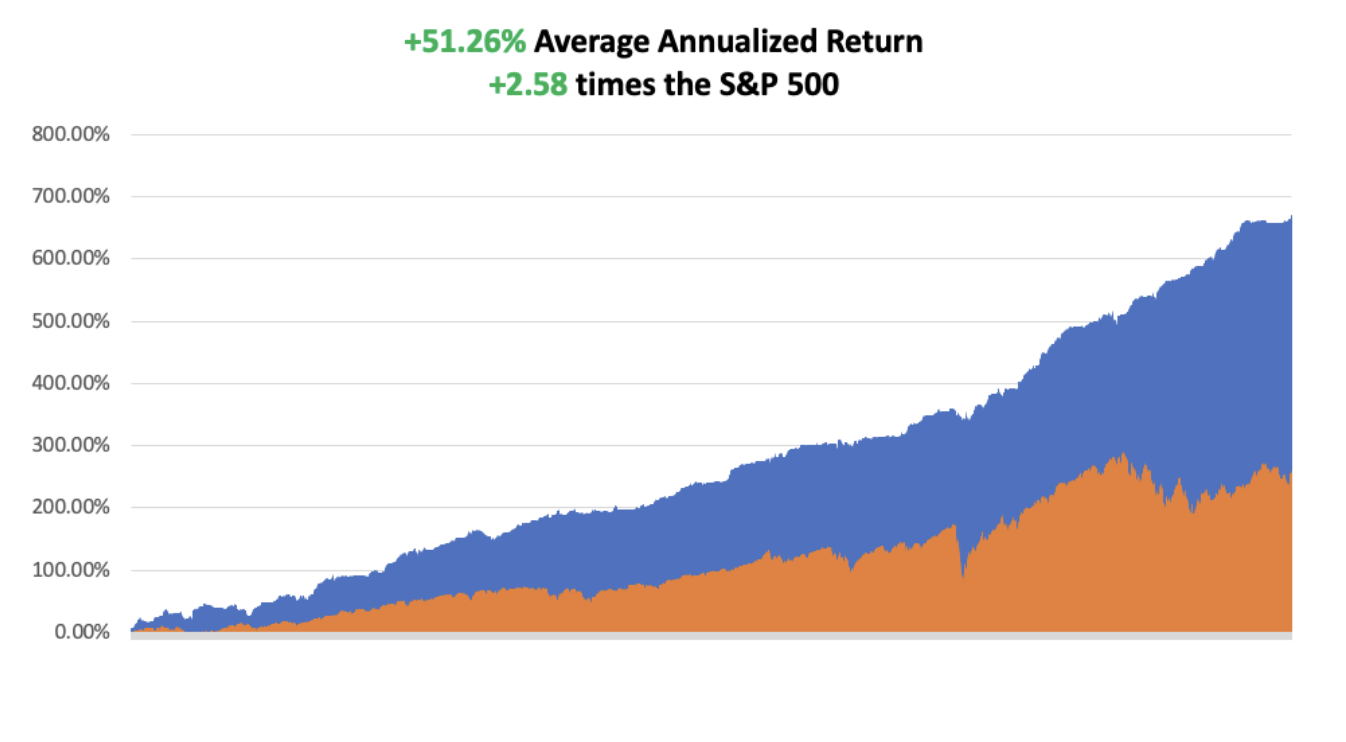

Since I implemented an AI-driven, self-learning Mad Hedge Market Timing algorithm to assist me in my own Trade Alert service six months ago, MY PERFORMANCE HAS ROCKETED, FROM A 21% ANNUAL RATE TO 51%!

As a result, YOU have been crying all the way to the bank!

The proof is all in the numbers (see chart below).

Those trading without the tailwind of algorithms today suddenly find the world a very surprising and confusing place.

They lose money too.

The investment implications of all of this are nothing less than mind-boggling.

Wages are almost always the largest cost for any business, especially the labor-intensive ones like retailing, fast food, and restaurants.

Reduce your largest expense by 90% or more, and the drop through to the bottom line will be enormous.

Stock markets have already noticed.

Maybe this is why price-earnings multiples are trading at a multi-decade high of 19.5X.

Perhaps, the markets know something that we mere humans don’t?

It also is the largest budgetary item in any government-supplied service.

I bet that half of the country’s 7 million teaching jobs will be gone in a decade, taken over by much cheaper online programs.

Today, my kids do their homework on their iPhones, complete class projects on Google Docs, and get a report card that is updated and emailed to me daily.

They’re probably to last generation to ever go to a physical school.

(That’s life. Just as the cost of driving them to school every day becomes free, they don’t have to go anymore).

You can always adopt a “King Canute” strategy and order the tide not to rise.

Or, you can rapidly adapt, as I did.

The choice is yours.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/03/12-month-story-2-1-e1521668829556.jpg349580MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2023-11-14 09:02:152023-11-14 12:13:57Why You Will Lose Your Job in the Next Five Years, and What to do About it

With interest rates and inflation topic number one of the day, everyone has their favorite inflation indicator. The Fed has its, you have yours, and well, I have mine.

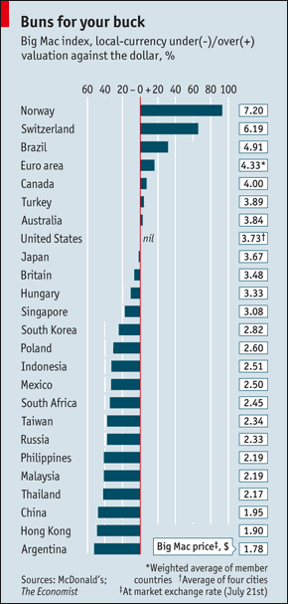

My former employer, The Economist, once the ever-tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its “Big Mac” index of international currency valuations.

Although initially launched as a joke four decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success. The index counts the cost of McDonald’s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn’t agree more with many of these conclusions. It’s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my hip. Better to use it as an economic forecasting tool, than a speedy lunch.

https://www.madhedgefundtrader.com/wp-content/uploads/2023/11/big-mac-yen.jpg312416Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2023-11-01 09:04:142023-11-01 15:31:16Where The Economist “Big Mac” Index Finds Currency Value

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.