“No one wins in a trade war, and manufacturing workers are hopeful the administration's approach will quickly yield results,” said National Association of Manufacturers (NAM) president and CEO Jay Timmons.

“No one wins in a trade war, and manufacturing workers are hopeful the administration's approach will quickly yield results,” said National Association of Manufacturers (NAM) president and CEO Jay Timmons.

Mad Hedge Technology Letter

September 20, 2018

Fiat Lux

Featured Trade:

(THE BULL CASE FOR NETFLIX),

(NFLX), (AAPL), (GOOGL), (FB)

Last quarter’s earnings report sent Netflix shares nosediving to the depths of the ocean floor, and the wreckage saw Netflix’s stock down 24% in 5 weeks.

The short-term weakness in shares was justified after Netflix miscalculated on their quarterly subscriber numbers.

Netflix is still a buy because the wreckage can be salvaged.

In fact, it was never a wreckage to begin with because Netflix boasts the highest grade online streaming product in the industry.

An industry that is benefitting from massive secular tailwinds at its back, from cord cutters and the widespread pivot to mobile platforms.

Netflix has the best product on the market because they have the best strategy – throw $8 billion on content alone and hire the best production team money can buy to churn out content.

The method to their madness has worked and the haul of 23 Emmy’s was a result of this winning formula.

The 23 Emmy’s tied HBO, whose premier series Game of Thrones is still captivating audiences with its mix of graphic sexual exploits and violent tropes.

Several of Netflix’s award winners saluted Netflix’s hands-off approach, who allow these highly paid production specialists the creative freedom to inspire audiences.

For all of Hollywood’s razzmatazz, director’s and actor’s number one major gripe has been that the leash is tight with minimal wiggle room.

It’s not straightforward to change a culture that has developed over a century.

Cross-pollinating Silicon Valley’s lean business model with Hollywood top-grade content was the trick that removed the shackles from the director’s ankles.

The end-product has been the main beneficiary.

Scoping out Netflix’s end of year lineup has viewers drooling.

The tail end of the year sees Netflix reintroduce some hard-hitting content from Orange Is The New Black, Ozark, Daredevil, Narcos, and Making a Murderer, side by side with fresh content involving Simpsons creator Matt Groening and blockbuster names like Jonah Hill and Emma Stone.

As well as shelling out $8 billion for original content, Netflix upped its marketing budget from $1.28 billion to $2 billion in 2018.

The $2 billion budget is a classy touch but at this point, this product more or less sells itself.

The brand awareness is that far-reaching.

The platform is optimized by tweaking Netflix’s proprietary recommendation algorithm herding the audience into viewing more content that the algorithm deems likely viewable.

The man who is in charge of this is Greg Peters - Netflix chief product officer.

Kelly Bennett, Netflix chief marketing officer, will work with Peters to wield the massive $2 billion marketing budget in the most effective way possible.

To insulate the company from any potential Facebook-like data slipups, Netflix poached Rachel Whetstone from Facebook to head up the public relations division.

Who said there were no winners from Facebook’s PR disaster?

Whetstone’s professional year of hell offers valuable insight into how not to pull another Facebook (FB) stinker.

She previously worked for Google and Uber and is a veteran PR spinner.

Earlier this year CEO Reed Hastings detailed the possibility of using ads in Netflix’s ad-less platform by saying this about why Netflix has no ads:

“It is a core differentiator and again we're having great success on the commercial-free path. That's what our brand is about. So we're going to continue to expand the relevance of a commercial free service around the world and make that so popular that consumers are very used to it and appreciate Netflix.”

The relevancy of his statement is more meaningful now after a recently released report confirming that Netflix is testing the usage of ads to promote its content.

This would be a huge shift in the company’s ethos, and if the algorithms give Hastings the green light, this could alienate a big chunk of their subscriber base.

In a survey conducted about the implementation of ads, 23% said they would quit the service if ads are rolled out onto Netflix’s platform.

Only 41% said they would “definitely” or “probably” keep Netflix if ads are introduced.

In the same survey, if Netflix lowers the monthly cost by $3 while integrating ads, the cancellation rate falls from 23% to 16%, and half said they would keep Netflix.

The most important number of the survey was that only 8% would cancel if they increased monthly prices by $2, but if it went up by $5, 23% would say goodbye to the streaming service.

All signs point to an incremental price increase in the near future, partly helping to offset the mind-boggling amount of content spend this year.

Netflix subscribers are still willing to absorb price increases which is a great sign for future profitability.

But it is also worth mentioning that Netflix is a profitable company now, and margins have been slowly creeping up for the past few years.

The tests demonstrate that Hastings is serious about profitability at a time when the premier profit machines in tech are Apple (AAPL) and Alphabet (GOOGL).

These two behemoths blaze the trail for the tech sector and offer important lessons on the potential future profitability of Netflix.

It will take time for Netflix to reach that level of profitability, but the pillars are in place to ramp up the monetization drive.

The treasure trove of data will surely help decision making for the management, but to make their platform more like Facebook (FB) would be a huge error of epic proportions.

It’s proven that digital ads are annoying like a swath of mosquitoes trapped in your bedroom at 2am.

To dilute the quality of their product would fly in the face of what the company represents.

So how on earth will Netflix’s shares go from the mid-$300’s and reach the glorious heights of $400-plus and stay there?

One word – India.

It’s no secret that Netflix has been charging hard to rev up international business.

India is the trump card.

India boasts around 78 million middle class dwellers who can afford Netflix’s service.

In the next two years, it’s feasible that 10% of this socioeconomic class could be tuning into Netflix.

That foothold into India could mushroom, and potentially expand with an audience whose DNA is comprised of a strong film culture.

As broad-brand broadband expansion and smartphone penetration heating up in India, Netflix’s timely arrival could make Netflix look genius.

Their arrival coincides with a slew of American tech companies looking to tap revenue out of the largest democracy in Asia.

The unrealized potential cannot be ignored.

Netflix has primed their strategy by focusing on locally-produced content that will resonate with the Indian viewer.

Netflix’s India strategy started red hot with crime thriller Sacred Games imbued with a level of unfiltered, real filmmaking unseen in India.

The dark crime drama is already facing a legal battle concerning its lusty, foul-mouthed content that presses on the outer limits of what modern Indian society can handle.

The stereotype breaking series directed by Vikramaditya Motwane and Anurag Kashyap is Netflix’s first Indian feather in their cap as Netflix looks to accelerate the momentum.

Netflix has not produced back to back quarters where they failed to meet subscriber growth forecasts since 2012.

I firmly believe Netflix will continue this successful streak and beat subscriber estimates in the third quarter.

Initial indications show that Indians have gravitated towards Netflix’s original content, and with the 2018 Russian World Cup in the history books, the path has opened up for some nice surprises to the upside.

________________________________________________________________________________________________

Quote of the Day

"Health care and education, in my view, are next up for fundamental software-based transformation." – Said Silicon Valley Venture Capitalist Marc Andreessen

Mad Hedge Technology Letter

September 19, 2018

Fiat Lux

Featured Trade:

(IBM’S SELF DESTRUCT),

(IBM), (BIDU), (BABA), (AAPL), (INTC), (AMD), (AMZN), (MSFT), (ORCL)

International Business Machines Corporation (IBM) shares do not need the squeeze of a contentious trade war to dent its share price.

It is doing it all by itself.

Stories have been rife over the past few years of shrinking revenue in China.

And that was during the golden years of China when American tech ran riot on the mainland before the dynamic rise of Baidu (BIDU), Alibaba (BABA), and Tencent, otherwise known as the BATs.

Then the Oracle of Omaha Warren Buffett drove a stake through the heart of IBM shares earlier this year by announcing he was fed up with the company’s direction and dumped a 35-year position.

Buffett unloaded all of his shares in favor of putting down an additional 75 million shares in Apple (AAPL) in the first quarter of 2018.

Topping off his Apple position now sees Buffett owning a mammoth 165.3 million total shares in the resurgent tech company.

Buffett’s shrewd decision has been rewarded, and Apple’s stock has rocketed more than 20% since he jovially declared his purchase in May.

IBM has been a rare misstep for Buffett, who took a moderate loss on his IBM position disclosing an average cost basis of $170 on 64 million shares that Berkshire bought in 2011.

IBM has flatlined since that Buffett interview, and slid around 25% since its peak in mid-2014.

IBM is grappling with the same conundrum most legacy companies deal with – top line contraction.

In 2014, IBM registered a tad under $93 billion in annual revenue, and followed up the next three years with even lower revenue.

A horrible recipe for success to say the least.

In an era of turbo-charged tech companies whose value now comprise over a quarter of the S&P, IBM has really fluffed its lines.

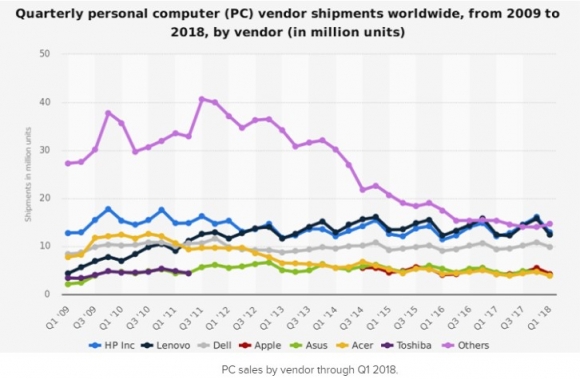

IBM’s prospects have been stapled to the PC market for years.

A recent JP Morgan note revealed the PC market could contract by 5% to 7% in the fourth quarter because of CPU shortages from Intel (INTC).

The report’s timing couldn’t have been worse for IBM.

The PC industry has been tanking for the past six consecutive years unable to shirk shrinking volume.

Intel is another company I have been lukewarm on lately because it is being outmaneuvered by chip competitor Advanced Micro Devices (AMD).

Even worse, this year has been a bad one for Intel’s management, which saw former CEO Brian Krzanich resign for sleeping with a coworker.

The poor management has had a spillover effect with Intel needing to delay new product launches as well.

To read more about my timely recommendation to pile into AMD in mid-August at $19, please click here.

Meanwhile, AMD shares have gone parabolic and surpassed an intraday price of $34 recently.

Investors should ask themselves, why invest in IBM when there are so many other tech companies that are growing, and growing revenue by 20% or more per year?

If IBM does manage to eke out top line growth in 2018, it will be by 1% to 2%, similar to Oracle’s recent performance.

Unsurprisingly, the price action of Oracle (ORCL) for the past year has been flatter than a bicycle ride around Beijing.

Live by the sword and die by the sword.

Thus, the Mad Hedge Technology Letter has been ushering readers into high-performance stocks that will bring technological and societal changes.

If you put a gun to my head and forced me to give sage investment advice, then the answer would be straightforward.

Buy Amazon (AMZN) and Microsoft (MSFT) on the dip and every dip.

This is a way to print money as if you had a rich uncle writing you checks every month.

Legacy tech is another story.

The IBMs and the Oracles of the world are bringing up the tech sector’s rear.

To add insult to injury, the lion’s share of IBM’s revenue is carved out from abroad, and the recent surge in the dollar is not doing IBM any favors.

IBM’s Watson initiative was billed as the savior for Big Blue.

The artificial intelligence initiative would integrate health care data into an actionable app.

The expectations were high hoping this division would drag up IBM from its long period of malaise.

IBM bet big on this division ploughing more than $15 billion into it from 2010-2015, predicting this would be the beginning of a new renaissance for the historic American company.

This game changing move fell on deaf ears and has been a massive bust.

IBM swallowed up three companies to ramp up this shift into the AI world - Phytel, Explorys, and Truven.

The treasure trove of health care data and proprietary analytics systems these companies came with were what this division needed to turn the corner.

These three companies were strong before the buy out and engineers were upbeat hoping Watson would elevate these companies to another level.

Wistfully, IBM Management led by CEO Ginni Rometty grossly mishandled Watson’s execution.

Phytel boasted 160 engineers at the time of IBM’s purchase and confusingly slashed half the workforce earlier this year.

Engineers at the firm even lamented that now, even smaller firms were “eating them alive.”

Unimpressed with the direction of the artificial intelligence division at IBM, many of these three companies’ best and brightest engineers jumped ship.

The inability for IBM to integrate Watson reared its ugly head in plain daylight when MD Anderson Cancer Center in Texas halted its Watson project after draining $62 million.

This was one of many errors that Watson AI accrued.

The failure to quicken clinical decision-making to match patients to clinical trials was an example of how futile IBM had become.

In short, a spectacular breakdown in execution mixed with an abrupt brain drain of AI engineers quickly imploded the prospect of Watson ever succeeding.

In 2013, IBM confidently boasted that Watson would be its “first killer app” in health care.

Internal leaks shined a brighter light on IBM’s subpar management skills.

One engineer described IBM’s management as having “no idea” what they were doing.

Another engineer said they were uncertain of a “road map” and “pivoted many times.”

Phytel, an industry leader at the time focusing on population health management, was bleeding money.

The engineers explained further, chiming in that IBM’s management had zero technical experience that led management wanting to create products that were “simply impossible.”

Not only were these products impossible, but they in no way took advantage of the resources these three companies had at their disposal.

Do you still want to invest in IBM?

Fast forward to today.

IBM is being sued in federal court with the plaintiff’s, former employees at the firm, claiming the company unfairly discriminated against elderly employees, firing them because of their age.

The documents submitted by the plaintiff’s state that “IBM has laid off 20,000 employees who were over the age of 40” since 2012.

This prototypical legacy company has more problems than the eye can see in every nook and cranny of the company.

If you have IBM shares now, dump them as soon as you can and run for cover.

It’s a miracle that IBM shares have eked out a paltry gain this year. And this thesis is constant with one of my overarching themes – stay away from all legacy tech firms with no cutting-edge proprietary technologies and stagnating growth.

________________________________________________________________________________________________

Quote of the Day

“Some say Google is God. Others say Google is Satan. But if they think Google is too powerful, remember that with search engines unlike other companies, all it takes is a single click to go to another search engine,” said Alphabet cofounder Sergey Brin.

My next global strategy webinar will be held on Wednesday, September 19 at 12:00 PM EST, which I will be broadcasting live from Silicon Valley in California.

Mad Day Trader Bill Davis will be my willing co-conspirator.

I’ll be giving you my updated outlook on stocks, bonds, commodities, currencies, precious metals, energy, and real estate.

The goal is to find the cheapest assets in the world to buy, the most expensive to sell short, and the appropriate securities with which to take positions.

I will also be opining on recent political events around the world and the investment implications therein.

I usually include some charts to highlight the most interesting new developments in the capital markets. There will be a live chat window with which you can pose your own questions.

The webinar will last 45 minutes to an hour. International readers and new subscribers who are unable to participate in the webinar live will find it posted on my website within a few hours. I look forward to hearing from you.

To log into the webinar, please click on the link we emailed you entitled, "Next Bi-Weekly Webinar – September 19, 2018" or click here.

Mad Hedge Technology Letter

September 18, 2018

Fiat Lux

Featured Trade:

(THE DANGERS OF PLAYING TECH SMALL FRY),

(FIT), (AAPL), (CRM), (FTNT), (SQ), (SNAP), (BBY)

The No. 1 complaint the Mad Hedge Fund Technology Letter receives is that I focus too much on the tech behemoths, and do not allocate much time for the needle-in-the-haystack inspirations aiming to disrupt the status quo.

Let’s get this straight – both are important.

And when a gem of a company riding the coattails of monstrous secular tailwinds comes to the fore, I do not hesitate to usher readers into the stock at a market sweet spot.

Fortunately, many of the lesser-known companies I have recommended have hit their stride such as Salesforce (CRM), Fortinet (FTNT), and Square (SQ), while I alerted readers to avoid Snap (SNAP) like the plague.

There are a lot of moving parts to say the least.

The most recent annual Apple (AAPL) product release event was emblematic of why I cannot go to the well and recommend the minnows of the tech world on a constant basis.

In 2017, Apple registered more than $229 billion in gross revenue. And under this umbrella of assets is a finely tuned operational empire that stretches like the Mongol empire of yore from best-in-class hardware to innovative software services.

Last year brought Apple a king’s ransom of profits to the tune of more than $48 billion.

Many of these upstart firms are fighting tooth and nail to surpass the $100 million gross sales mark, which is peanuts for the intimidating large tech companies.

In the process of expanding their dominion far and wide, the net they cast extends further by the day.

I hammer home the fact that these cash-rich stalwarts have an insatiable drive to initiate new businesses as a way to position themselves at the heart of each groundbreaking trend and capture fresh markets.

Some decisions are rued and some – brilliant.

At the very least, they can afford a few hits.

Algorithms, which suck up voluminous amounts of data, carry out the best decisions that software can buy.

Managers wield these finely tuned algorithms to make precise bets.

These myriads of algorithms are tweaked every day as the level of tech ingenuity snowballs incrementally with each passing day.

Enter Fitbit (FIT).

This company was first known as Healthy Metrics Research, Inc., a decisively less sexy name than its current name Fitbit.

Healthy Metrics Research, Inc. unglamorously began as did most tech companies - with little fanfare.

Its cofounders James Park and Eric Friedman identified the opportunity to jump into the sensor industry, as they saw a monstrous addressable market for future sensors in wearable smart devices.

They soon caught a bid and $400,000 flew into its coffers. They promptly marketed designs to potential investors with nothing more than a circuit board in a wooden box.

Oh, how the wearable smart device market has advanced since those early days…

All in all, the idea was good enough for some initial seed money.

At the first tech conference marketing their new sensors, they were hoping to eclipse 50 orders.

Fortuitously, the upstart firm received more than 2,000 pre-orders, and a reset upward in expectations.

With momentum at their backs, the cofounders now had the sticky situation of physically delivering the end-product to the end-user.

This involved scouring Asia for reasonable suppliers for three-odd months with “7 near death experiences” mixed in the middle of it.

Highlighting the unglamorous nature of incubation stage firms were the cofounders once quick fix sticking a “piece of foam on a circuit board to correct an antenna problem."

Somehow and some way they debuted their product at the tail end of 2009, delivering 5,000 orders with a backlog of additional orders to boot, offering the company some stress relief.

Fitbit had the best product in an industry that barely existed, and everything was rosy at their headquarters in San Francisco.

Best Buy (BBY) even adopted its products, and Fitbit watches were flying off the shelves like hotcakes.

Margins were gloriously high. The lack of threats around the corner made the company the gold standard for smartwatches.

In short, the company was having its cake and eating it, too.

In 2011, Fitbit was furiously adding to the best smartwatch on the market installing an altimeter, a digital clock and a stopwatch to its premium product.

Then came embedded Bluetooth technology: able to track steps, distance, floors climbed, calories burned, and sleep patterns.

After being embroiled in several law quagmires over big data, momentum was still at their back, and Fitbit still managed to go public.

The IPO was a roaring success and then some.

The share price rocketed to almost $50, and the firm sat pretty in the middle of 2015.

Then the company’s shares fell to pieces in one fell swoop.

Fitbit’s stock cratered more than 50% in 2016. To inject new life into the company, CEO James Park trumpeted Fitbit’s imminent face-lift that would transform the young company from a "consumer electronics company" to a "digital healthcare company."

Bad news for Fitbit. Apple planned to do the same exact thing but do it better than Fitbit.

The readjustment to Fitbit’s grand plan was to combat the original Apple smartwatch that debuted on April 24, 2015 – three years ago.

The Apple smartwatch rapidly became the dominant smartwatch in the wearable industry, selling more than 4.2 million units in just one quarter alone.

Fitbit is now trading just a smidgen over $5 today, and the devastation is far from over.

Fitbit’s shares are down almost 1,000% from its 2015 peak, stressing the dangers that minnow tech companies face getting outgunned by companies that have superior talent, unlimited resources, and top-grade management.

Not only that, Apple can integrate any wearable device linking it with the rest of its ecosystem in a heartbeat.

Even better, it does not need to develop an operating system from scratch because it can use what it already has in place - iOS.

Even if it were to run into development troubles, it would be able to throw around a wad of capital to find someone to solve idiosyncratic issues that pop up.

Yes, Tim Cook has not been the second incarnation of Steve Jobs, but he has demonstrated a natural ability to become a trustworthy steward, advancing the interests of the company, its shareholders, and most importantly its lineup of ultra-premium products.

Fitbit was enjoying its beach promenade stroll and walked into a doozy of a tsunami with little warning.

Spearheading a revival is even more daunting.

For David to outdo Goliath takes an emphatic sum of capital and a master plan to go with it.

Fitbit has neither.

The most recent Apple product launch event introduced a gem of a smartwatch, and Fitbit’s shares once again are on life support.

With each passing Apple smartwatch iteration, Fitbit experiences a new dramatic leg down in the share price.

It is almost curtains for this company.

It will be unceremoniously laid to rest in what is now quite an expansive tech graveyard of futility.

The best-case scenario is possibly salvaging itself by drastic reinvention.

It is easier said than done.

Add this company to your list of small companies obliterated by the phenomenon known as FANG, and this story gives credence to investors trying to be cute with their tech investments.

On paper it looks great until the company becomes steamrolled.

And the paper Fitbit was written on doesn’t even look all that hot with Fitbit poised to lose money until 2021.

It sounds cliché, but the network effect cannot be underestimated.

Without this powerful effect, tech investors are exposed to a demonstrably higher level of risk.

The risk of extinction.

Stay away from Fitbit shares and any dead cat bounces that shortly arise.

The Apple watch series 5 could be the dagger that finishes the walking wounded.

As an endnote, the next potential Fitbit creeping closer to the eye of the FANG storm could be the smart speaker company Sonos (SONO).

Sometimes the calm before the storm can be awfully quiet.

________________________________________________________________________________________________

Quote of the Day

“The best way to predict the future is to create it,” said influential philosopher Peter Drucker.

Mad Hedge Technology Letter

September 17, 2018

Fiat Lux

Featured Trade:

(APPLE RAMPS UP ITS GAME),

(AAPL)

A steady hand on the tiller – that was the key takeaway from the recent Apple release event that saw updated iPhone models poised to hit stores in October.

There was nothing of substance to steal the show or radical revelations awing the patient neutral, but that is how Apple CEO Tim Cook likes it.

iPhone XS, iPhone XS Max and iPhone XR were conveniently named after their predecessor the iPhone X.

These smartphones are of the same ilk but in a refreshed way.

The iPhone XR is the lower-grade version of the three, but shares many of the same specs as the superior versions.

This version could be the model that lures in Apple lovers that avoided upgrading last cycle, because the inner workings are similar enough and the look is premium enough, but hundreds of dollars cheaper than the XS and XS Max models.

Check, check, and check.

I wouldn’t label it an “entry level” smartphone, but it hits all the right notes for iPhone fans that can’t cough up the big bucks for the higher-priced products.

The phone’s price tag has been a lingering concern especially in the emerging world.

Apple smartly widened the range of premium phone prices to the lower and higher range - the net effect will be a moderate bump in the all-critical average selling price (ASP), which is a huge winner in all of this.

At the top end of the range, the iPhone XS Max with 512 GB of memory will command a hefty $1,449.

This is the priciest iPhone ever made.

Larger screen sizes in the 6.5" XS Max and 6.1" XR will appeal to their fan base driving additional incremental business to the company that Steve Jobs left his indelible mark on as well.

The covert winner in all of this is Apple’s share price.

Apple’s share price is notorious for being slashed and burned before their new iPhone release events and the run up to earnings season.

The lack of apocalyptic behavior in its recent share price surely has the bulls rejoicing.

Basically, these new iPhone models aren’t worrying Apple investors even one scintilla.

Apple going forward is not betting the ranch on hardware anymore and investors have approved in spades.

Last quarter’s earnings report highlighted the Teflon nature of Apple’s iPhone demand by proving to investors that Apple could successfully sell smartphones over $1,000.

The seminal shift breaking psychological price barriers is indicative of Apple’s relentless pursuit to produce the best phone in the world.

This perpetual chase has seen the company almost surpass the $1,500 price tag this time around and will smash this price point next time around.

The strength in recent Apple price action wholeheartedly signifies that Apple is a software and service company now and not a hardware company.

Apple was able to make the transformation with grace and elegance and avoiding any damaging blowups.

Apple is on pace to double services revenue to $15 billion per quarter by 2020 creating a $60 billion per year revenue beast of a division.

The software and services are where all the high margin activity is migrating in Apple’s ecosystem.

I have incessantly urged readers to stay with the highest quality tech companies that continue to unlock value at a breathtaking pace, especially amid a precarious backdrop of global trade spats and brutal competition.

Investors are migrating up the value chain storing their hard-earned capital in the best of tech as the weak hands are flushed out by the regulation and global trade police.

Apple is one of these companies with a dazzling portfolio of products.

Their steady march upward in quality is confirmed by products such as the Apple Watch Series 4.

Wearables have become a strength of Apple’s product line after botching the initial debut.

The new watch is redesigned, sleek, and mesmerizingly beautiful.

The display is more than 30% larger than its old design and offers flawless software functionality.

Apple’s shift into health is partly driven by monetizing its watch and other wearables.

Apple hopes its watch can be a natural part of sportsmen and sportswomen’s lives.

If Apple’s watch can be your lovable sports companion going forward, then an entire new avenue of revenue can break ground and be redistributed to shareholders.

The Cupertino company packed a ton of heat into this sensational device. It is a big reason why industry insiders believe that half of the 43.5 million smartwatches expected to be sold in 2018 will come from Apple.

Google's Wear OS lags distantly behind with a forecasted 12% market share, and it will be tough going to compete with Apple in this space.

Not only is the watch’s screen bigger, the speakers are also 50% louder.

The larger screen will allow users up to eight shortcuts on the screen for apps.

Apple also noted that the watch’s battery life will last 18 hours with an outdoor workout time of six hours.

Another groundbreaking feature is the ability to take electrocardiograms (ECG) reaffirming Apple’s pivot into the health sector through their shimmering new watch.

According to Apple, this revolutionary feature is the first time an (ECG) product has been available to retail consumers.

To admire the full beauty of this scintillating watch, click here to watch a video.

Earlier this year, Apple CFO Luca Maestri told the Financial Times that wearables in the past year have experienced a “60% growth in revenue terms. Adding up the last four quarters, wearables revenue now exceeds $10 billion.”

Apple’s wearables are classified under “other products” and include AirPods, Watch, Beats, and the HomePod.

Watch this division to continue its robust performance going forward.

In a nod to the emerging markets, Apple decided to introduce its first dual sim card inside the new iPhone models.

One of the slots will be an “eSIM” slot – a nascent technology that hasn’t been widely adopted yet.

For all the newbies unsure of what an eSIM card is - “Electronic SIM card” removes the hassle of poking a paperclip through your sim tray to switch out your sim card, which is a little smaller than your pinkie finger nail.

Rather, eSIM cards only need a compatible network requiring support, and it bypassed the need for a physical sim card and sim card tray altogether.

This move could syphon off even more revenue for phone network carriers if the eSIM technology mushrooms.

Apple will be the gatekeeper of the eSIM tech since it will have total control over it, even opening up the possibility to rotate between more than two carriers in the future if a physical sim card is not needed.

This could pave the way for Apple to get rid of the sim card slot entirely for the next iPhone iteration and use the space to develop something even better.

Technological innovation requires bold moves, to which Apple is no stranger.

In fact, only 10 countries currently support eSIM technology - Austria, Canada, Croatia, the Czech Republic, Germany, Hungary, India, Spain, the UK, and the U.S.

Demonstrating that dual sim cards are a way of life in the emerging world is data showing that 98% of Indian smartphones come with embedded dual sim card functionality, 92% in the Philippines, 90% in China, 77% in Indonesia, and just 4% in the U.S. in the third quarter of 2017 to the second quarter of 2018.

The ease of swapping in and out contract less sim cards is useful for any digital nomad. Buy a sim card for a few dollars at the airport, activate it, and you’re on your merry way.

In another nod to the Chinese customer, Apple will forgo the eSIM technology entirely and stick with the physical dual tray, allowing mainland Apple fans to physically implant two sim cards at one time.

Whether enhancing the phone, recreating its beloved watch, or rolling out audacious new technologies – Apple is satisfying all the naysayers.

It’s no wonder this company is a buy on the dip and hold to eternity stock.

________________________________________________________________________________________________

Quote of the Day

“Price is rarely the most important thing. A cheap product might sell some units. Somebody gets it home and they feel great when they pay the money, but then they get it home and use it and the joy is gone,” said Apple CEO Tim Cook.