Mad Hedge Technology Letter

April 27, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON)

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON)

Mad Hedge Technology Letter

April 27, 2018

Fiat Lux

Featured Trade:

(WEDNESDAY, JUNE 13, 2018, PHILADELPHIA, PA, GLOBAL STRATEGY LUNCHEON)

(THURSDAY, JUNE 14, 2018, NEW YORK, NY, GLOBAL STRATEGY LUNCHEON)

Come join me for lunch at the Mad Hedge Fund Trader's Global Strategy Update, which I will be conducting in Philadelphia, PA, on Wednesday, June 13, 2018. An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I'll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I'll be throwing a few surprises out there, too. Tickets are available for $238.

I'll be arriving at 11:45 AM, and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive downtown private club. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research.

To purchase a ticket, please click here.

Come join me for lunch at the Mad Hedge Fund Trader's Global Strategy Update, which I will be conducting in New York City on Thursday, June 14, 2018. An excellent meal will be followed by a wide-ranging discussion and an extended question-and-answer period.

I'll be giving you my up-to-date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I'll be throwing a few surprises out there, too. Tickets are available for $278.

I'll be arriving at noon and leaving late in case anyone wants to have a one-on-one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at an exclusive downtown private club. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you and thank you for supporting my research.

To purchase a ticket, please click here.

Mad Hedge Technology Letter

April 26, 2018

Fiat Lux

Featured Trade:

(THE SMALL AI PLAY YOU'VE NEVER HEARD OF),

(BOX), (GOOGL), (MSFT), (AMZN), (IBM)

The cloud segment of technology is hotter than hot, and as this sector starts to trade at a big premium, investors will have to look further down the chain of command to find a reasonable deal.

An up-and-coming cloud service Box (BOX) has gone undiscovered and is in position to seize a larger share of the cloud market moving forward.

The firm is led by CEO Aaron Levie who dropped out of my old alma mater USC in 2005 to start a cloud company with acting CFO and childhood friend Dylan Smith.

Last quarter was record-setting for Box, and it had a number of significant six- and seven-digit deals. Keep in mind Box's revenues are paltry compared to the behemoths that run this industry.

The platform has seen gradual success from all corners of the business world with various businesses from insurance claims processors to wealth advisors who use Box as a back-end platform.

Health care is another industry deploying the Box platform to aid and develop cloud services for patients.

In a general sense, the beauty of the cloud is the propensity to adapt to any company that is willing to go digital.

Even though many legacy companies are not natively digital, the cloud can twist and contort to fit the customers' needs.

Levie raised some compelling arguments for the continued tech momentum stating that imminent regulation in Europe through General Data Protection Regulation (GDPR) will act as a "broader tailwind in compliance and security efforts."

Box also announced a "readiness (GDPR) package" revealing that tech companies have been planning for the regulation overhaul up to 18 months in advance.

Even though mass media sensationalism would lead investors to believe the threat of regulation is about to blindside this whole sector, the unrest has been bubbling up for quite some time allowing tech companies ample time to get their houses in order.

Box actually sees the genesis of GDPR as a critical part of the cloud adoption process.

As dinosaur systems become outdated, a sense of safety reinforced by strong cybersecurity protection, strong privacy rules, and content compliance will nudge companies to head for the cloud like a drunk sailor to a pub.

Legacy platforms are the most susceptible to cyber-criminals and rogue hackers.

The analog defense is no match for sophisticated cyber-espionage, and GDPR will be another "driving force" behind the macro-migration shift to the cloud, just based on the security aspect alone.

Another pearl of wisdom offered by Box is that the bulk of clients requiring cloud products are integrating Microsoft Office 365.

This software acts as a lynchpin to any cloud service.

I must confess that I am writing this story on Microsoft Office 365 now, and most businesses cannot function without the dizzying array of Excel, PowerPoint, and Word.

Box has a strong relationship with Microsoft and has incisive insight into the synergies the cloud industry spins off.

The integration of Office 365 has complemented the Azure cloud with tighter cohesiveness.

The school of thought is the collective cloud industry is a $50 billion per year market and growing, offering smaller firms healthy growth levers to advance at the same time that the Microsofts (MSFT) and Amazons (AMZN) overperform.

At the Sohn Investment Conference in New York, Chamath Palihapitiya, a venture capitalist and former Facebook executive, extolled Box as a great way to play Artificial Intelligence (AI).

The shares spiked almost 13% upon his adulation.

A recent completed survey showed 66% of business leaders feel the pace of digitization must pick up in their own offices.

The speed of innovation is something that keeps most CEOs up at night. Wake up tomorrow and it is possible their core products could be outdated or disrupted by a new Amazon threat.

That is the world we live in now.

Only 42% of CIOs admitted they have a digital strategy. And of those digital strategies, they are mostly digital second or third, not digital first, blueprints.

In the same PricewaterhouseCoopers (PwC) survey, companies conceded that only 40% of IT teams are able to pursue the newest innovations with adopting specific operational needs in mind.

The micro-environment harbors the same bullishness as the macro-factors.

Box is hitting all the right notes.

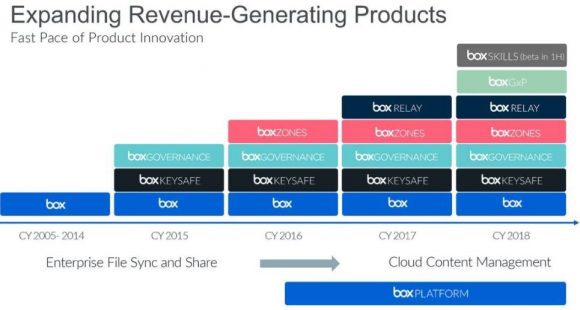

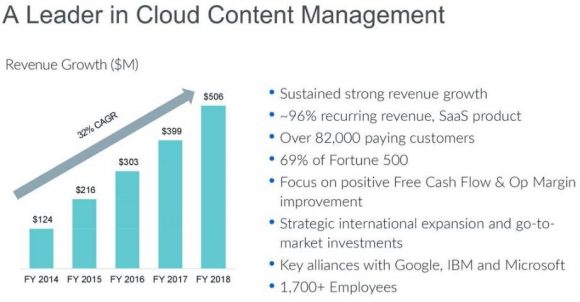

Revenue is advancing at a 24% per year clip, and annual revenue surpassed the half a billion mark.

Box has indicated it expects to cross the $1 billion annual revenue threshold sometime in mid- to late 2021, giving the company more than three years to double revenue.

Recent reports support Box's growth trajectory.

About 60% of revenue derives from firms that employ more than 2,000 workers, highlighting Box's propensity to emphasize enterprise cloud development instead of small individual users.

Working with larger companies gives Box the opportunity to cross-sell more powerful add-ons, delivering a net expansion rate of 14%.

Migrating to a new cloud platform is incredibly sticky boosting retention rates. Box's churn rate is flourishing with a best of breed 4% per year. The key to expediting cloud success is quickening its pace of new product rollout.

Box attempts to give exactly what customers need with a spate of new concoctions.

Box GxP is a new product calibrated around life science companies. The Box GxP compliance is up to date with FDA regulations. And, Box has the ability to retire legacy ECM (Enterprise Content Management) systems.

This new service has experienced solid traction around the world as we head toward a world where legacy software becomes obsolete.

The second new offering is Box Skills, still in beta mode, which is a part of Box's artificial intelligence strategy.

Box is platform neutral allowing in-house architecture to support partnerships with Google, Microsoft, Amazon, and IBM to nail down third-party cloud tools that Box customers need.

Box Skills is a framework that brings the best machine learning innovation to content securely stored in Box.

This is managed through artificial intelligence, which automatically contextualizes images through detection protocols. Text recognition is automated for the benefit of the user, too.

Audio intelligence renders text transcripts and detects topics that can be searched in Box to locate an audio file by words or topic.

Video intelligence offers transcription, topic detection, and facial recognition allowing users to jump around video files in a non-linear fashion.

Palihapitiya effectively gave Box a free commercial to the tech investing world. His bull thesis for Box squarely centers around its AI innovations, specifically Box Skills.

The last new service to market is Box Transform, which is the advanced consulting arm of Box.

The goal of Transform is to arrange a concierge-like Box advisor that can help companies accelerate digital transformation throughout an organization while unlocking efficiencies and productivity for employees.

This service originated from Box's consulting advanced professional services team and will give Box another growth lever. Companies such as Red Hat and Intel have made the consultant- and support-side of the business a robust part of their organizations.

Impeding growth is the cutthroat competition in this space with Amazon, Microsoft, and Google (GOOGL).

However, margins remain strong at 75.5% last quarter, and Box expects margins to slightly dip around 74% this year.

Box has found a warm welcome for its newer products, deriving almost 70% of its new deals from fresh cloud offerings.

Partners are also a big source of new deals comprising more than half the deals over $100,000.

Specifically, IBM (IBM) made up a swath of its larger deals. In a sense, competitors are not really competitors.

They are frenemies. They compete against each other yet innovate and do deals together.

The core growth is supplemented by existing customers that are the best source of extra marginal revenue.

In short, once firms are firmly lodged on a platform, they buy everything on that platform.

Enter a supermarket, and odds are if goods are purchased, the receipt will be from the entered supermarket.

Box is entirely leveraged toward mid-sized and large enterprise business. That is where it makes its money.

The emphasis on large players boosts the ACV (Average Contract Value), which is regarded as a sacrosanct metric for Box.

The amount of data created in 2017 was more data created in the past 5,000 years. In the next five years, data volume with grow by 800%.

Box has continually positioned itself as the firm that can extract a staggering amount of unrealized value locked away in the nooks and crannies of legacy models.

Box is a great long-term hold as these diminutive cloud assets become more valuable by the day.

_________________________________________________________________________________________________

Quote of the Day

"Television won't be able to hold onto any market it captures after the first six months. People will soon get tired of staring at a plywood box every night." - said Darryl F. Zanuck, co-founder of Twentieth Century-Fox Film Corp.

Mad Hedge Technology Letter

April 25, 2018

Fiat Lux

Featured Trade:

(FANGS DELIVER ON EARNINGS, BUT FAIL ON PRICE ACTION),

(GOOGL), (AMZN), (MSFT), (AAPL), (FB),

(DBX), (NFLX), (BOX), (WDC)

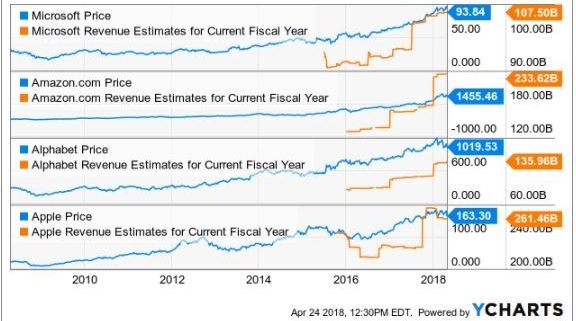

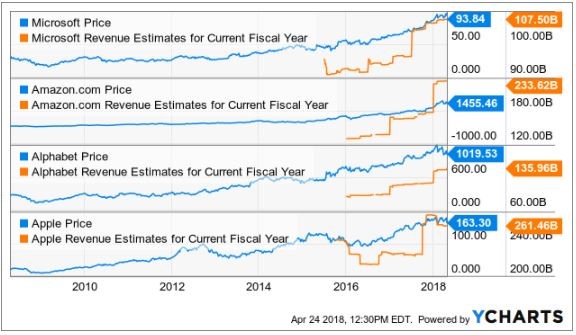

Alphabet (GOOGL) did a great job alleviating fears that large-cap tech would be dragged through the mud and fading earnings would dishearten investors.

The major takeaways from the recent deluge of tech earnings are large-cap tech is getting better at what they do best, and the biggest are getting decisively bigger.

Of the 26% rise to $31.1 billion in Alphabet's quarterly revenue, more than $26 billion was concentrated around its mammoth digital ad revenue business.

Alphabet, even though rebranded to express a diverse portfolio of assets, is still very much reliant on its ad revenue to carry the load made possible by Google search.

Its "other bets" category failed to impact the bottom line with loss-making speculative projects such as Nest Labs in charge of mounting a battle against Amazon's (AMZN) Alexa.

The quandary in this battle is the margins Alphabet will surrender to seize a portion of the future smart home market.

What we are seeing is a case of strength fueling further strength.

Alphabet did a lot to smooth over fears that government regulation would put a dent in its business model, asserting that it has been preparing for the new EU privacy rules for "18 months" and its search ad business will not be materially affected by these new standards.

CFO Ruth Porat emphasized the shift to mobile, as mobile growth is leading the charge due to Internet users' migration to mobile platforms.

Google search remains an unrivaled product that transcends culture, language, and society at optimal levels.

Sure, there are other online search engines out there, but the accuracy of results pale in comparison to the preeminent first-class operation at Google search.

Alphabet does not divulge revenue details about its cloud unit. However, the cloud unit is dropped into the "other revenues" category, which also includes hardware sales and posted close to $4.4 billion, up 36% YOY.

Although the cloud segment will never dwarf its premier digital ad segment, if Alphabet can ameliorate its cloud engine into a $10 billion per quarter segment, investors would dance in the streets with delight.

Another problem with the FANGs is that they are one-trick ponies. And if those ponies ever got locked up in the barn, it would spell imminent disaster.

Apple (AAPL) is trying its best to diversify away from the iconic product with which consumers identify.

The iPhone company is ramping up its services and subscription business to combat waning iPhone demand.

Alphabet is charging hard into the autonomous ride-sharing business seizing a leadership position.

Netflix (NFLX) is doubling down on what it already does great - create top-level original content.

This was after it shed its DVD business in the early stages after CEO Reed Hastings identified its imminent implosion.

Tech companies habitually display flexibility and nimbleness of which big corporations dream.

One of the few negatives in an otherwise solid earnings report was the TAC (traffic acquisition costs) reported at $6.28 billion, which make up 24% of total revenue.

An escalation of TAC as a percentage of revenue is certainly a risk factor for the digital ad business. But nibbling away at margins is not the end of the world, and the digital ad business will remain highly profitable moving forward.

TAC comprised 22% of revenue in Q1 2017, and the rise in costs reflects that mobile ads are priced at a premium.

Google noted that TAC will experience further pricing pressure because of the great leap toward mobile devices, but the pace of price increases will recede.

The increased cost of luring new eyeballs will not diminish FANGs' earnings report buttressed by secular trends that pervade Silicon Valley's platforms.

The year of the cloud has positive implications for Alphabet. It ranks No. 3 in the cloud industry behind Microsoft (MSFT) and Amazon.

Amazon and Microsoft announce earnings later this week. The robust cloud segments should easily reaffirm the bullish sentiment in tech stocks.

Amazon's earnings call could provide clarity on the bizarre backbiting emanating from the White House, even though Jeff Bezos rarely frequents the earnings call.

A thinly veiled or bold response would comfort investors because rumors of tech peaking would add immediate downside pressure to equities.

The wider-reaching short-term problem is the macro headwinds that could knock over tech's position on top of the equity pedestal and bring it back down to reality in a war of diplomatic rhetoric and international tariffs.

Google, Facebook, and Netflix are the least affected FANGs because they have been locked out of the Chinese market for years.

The Amazon Web Services (AWS) cloud arm of Amazon blew past cloud revenue estimates of 42% last quarter by registering a 45% jump in revenue.

Microsoft reiterated that immense cloud growth permeating through the industry, expanding 99% QOQ.

I expect repeat performances from the best cloud plays in the industry.

Any cloud firm growing under 20% is not even worth a look since the bull case for cloud revenue revolves around a minimum of 20% growth QOQ.

Amazon still boasts around 30% market share in the cloud space with Microsoft staking 15% but gaining each quarter.

AWS growth has been stunted for the past nine quarters as competition and cybersecurity costs related to patches erode margins.

Above all else, the one company that investors can pinpoint with margin problems is Amazon, which abandoned margin strength for market share years ago and that investors approved in droves.

AWS is the key driver of profits that allows Amazon to fund its e-commerce business.

Cloud adoption is still in the early stages.

Microsoft Azure and Google have a chance to catch up to AWS. There will be ample opportunity for these players to leverage existing infrastructure and expertise to rival AWS's strength.

As the recent IPO performance suggests, there is nothing hotter than this narrow sliver of tech, and this is all happening with numerous companies losing vast amounts of money such as Dropbox (DBX) and Box (BOX).

Microsoft has been inching toward gross profits of $8 billion per quarter and has been profitable for years.

And now it has a hyper-expanding cloud division to boot.

Any macro sell-off that pulls down Microsoft to around the $90 level or if Alphabet dips below $1,000, these would be great entry points into the core pillars of the equity market.

If tech goes, so will everything else.

If it plays its cards right, Microsoft Azure has the tools in place to overtake AWS.

Shorting cloud companies is a difficult proposition because the leg ups are legendary.

If traders are looking for any tech shorts to pile into, then focus on the legacy companies that lack a cloud growth driver.

Another cue would be a company that has not completed the resuscitation process yet, such as Western Digital (WDC) whose shares have traded sideways for the past year.

But for now, as the 10-year interest rate shoots past 3%, investors should bide their time as cheaper entry points will shortly appear.

_________________________________________________________________________________________________

Quote of the Day

"Technology is a word that describes something that doesn't work yet." - said British author Douglas Adams.

Mad Hedge Technology Letter

April 24, 2018

Fiat Lux

Featured Trade:

(WHAT THE MEDIA REALLY WANTS FROM YOU),

(TRNC), (AMZN), (FB), (GOOGL), (USPS), (SFTBY)

Publishing magnate and self-described populist William Randolph Hearst was a deep admirer of Adolph Hitler and did not shy away from using his newspapers as a de-facto mouthpiece spouting off Der Fuhrer's propaganda.

Hearst created content sympathizing with the Nazi ethos and even mobilized an embedded secret agent from the German government to act as a correspondent that followed hot, daily scoops inside Germany.

Hearst also used his publishing clout to pull the strings in the 1932 presidential election backing candidate John Nance Garner or "Cactus Jack" who later agreed to be Franklin D. Roosevelt's running mate.

The fusion of politics and media has been chiseled into human DNA since antiquity. However, the purpose of newspapers has evolved significantly since it became impossible to break even about 10 years ago.

Print newspapers are a lot like the US Postal Service - they specialize in losing money.

However, the (USPS) was never politicized as was the publishing industry until President Trump managed to commingle the loss-making mail outfit and Amazon as a joint problem roiling society.

The politicization comes at a cost to society.

All the well-intentioned journalists involved in earnest and quality journalism lose out because the new normal for newspapers has evolved into a William Hearst-like blatant tool promoting targeted interests.

Do you ever wonder why the Washington Post hardly ever publishes content harmful to the image of Amazon?

Because it is owned by the same man, Jeff Bezos, who founded Amazon (AMZN) in 1994, as he cruised in his car cross-country from New York to Seattle where he would start his tech empire.

Effectively, Jeff Bezos has the ear of each corner of the political power grid in Washington.

And while the president has been attacking Bezos as a job destroyer on a daily basis, Amazon has in fact been the largest private job CREATOR in the US. It added a staggering 130,000 new jobs in 2017, and an eye-popping 560,000 jobs over the past 10 years.

Last year saw Laurene Powell Jobs, widow to Steve Jobs, acquire the Boston-based American magazine The Atlantic.

The Atlantic earns more than $10 million per year in revenue and lures in over 33 million readers per month.

Billionaire biotech investor Patrick Soon-Shiong reached a deal with Tronc Inc. (TRNC), which possesses a vast array of various legacy media assets, to take over the LA Times and San Diego Union-Tribune for $500 million.

Tronc Inc. is on the verge of catching another bid with SoftBanks' (SFTBY) Masayoshi Son, looking to scoop up parts of the extensive portfolio.

Private equity group Apollo and media firm Gannett Company are also in the mix to acquire Tronc Inc.

Some of Tronc Inc.'s crown assets are the Chicago Tribune, the New York Daily News, and the Baltimore Sun among other regional newspapers with a large audience base.

Tronc's shares spiked almost 10% on whispers of the rumored news.

The courting of these news media assets comes at a time when Google (GOOGL) is funding a project to automate more than 30,000 stories per month for the local media as a cost-effective way to advance the business model.

Quality journalism written by a human is the last thing in which these mega-tech companies are interested.

The first thought that came into my head when I heard about SoftBank's vision fund swooping in for another company was data grab.

We have seen this story time and time again.

Newspapers and how an online subscriber behaves on a digital newspaper platform offer valuable data points that cannot be extracted elsewhere.

The data will reveal the political ideas, topics of interest, and other sensitive information deduced into a comprehensive data profile.

Effectively, a company such as SoftBank will be able to create a functional shadow profile for almost anyone.

The concept of shadow profiling emerged from the acrimony of Mark Zuckerberg's testimony in Washington and could be the next point of heated contention.

What are shadow profiles?

Shadow profiles are digital profiles crafted by data that were not directly handed over to Facebook (FB) by the user.

This data is extracted through fringe third parties, other friends on Facebook if they post content unique to you, and specifically through the "find your friends" function that recommends the uploading of an entire digital address book giving Facebook access to everyone you know.

Scarily, there is no opt-out for shadow profiling, and there probably won't be another congressional testimony about this topic anytime soon.

If Facebook wanted to turn into the FBI, it would be easy.

The treasure trove of data would give insight on the subtle nuances of authentic human behavior.

This artificial profile would seem real.

If you are an Android user like most of the world, Google could fill out the most comprehensive profile with a high degree of accuracy on most people.

The scandalous bit about shadow profiling is that these profiles are whipped up even if a user has never signed up for Facebook.

Shadow profiling, along with other data, becomes more precise as the volume of data piles up. To understand the behavior, trends, and tastes of most of the world's population is incredibly valuable.

Facebook could use this shadow profiling data to understand the wide range of non-Facebook user behavior.

This way of monetizing data would be highly illegal if leaked to an actionable third party and would be significantly worse than the Cambridge Analytica scandal.

This data should be deleted immediately, but Facebook has a backdoor way to keep the data in the system.

If Facebook got slammed for data leakage then others are in danger, too. That's because Facebook is not the only player mining data for money.

It wouldn't be surprising if other large cap tech companies started to create these shadow profiles to get dirt on their competitors as well as other use cases.

Tech is evolving at such a fast pace. It subconsciously encourages the never-give-up mentality that coerces firms to stay one step ahead, which Amazon has been able to do since its inception.

Newspaper companies are next in line to be absorbed by large cap techs continuously expanding web assets that hyper-focus on exponential data generation.

These newspapers will defend tech's interests in the economy similar to how newspapers were used as William Hearst's rallying cry for politics.

Jeff Bezos has chosen silence to react to President Trump's tweet offensive, but he could easily mobilize his newspaper to protect Amazon's interests.

Bezos just shrugs his shoulders and goes about his day because he knows Washington cannot do anything to change Amazon's dominance at the top of the tech food chain.

Better take the high road.

Not only do these big tech companies know who you talk to, what you buy, and where you are, but now they are given deeper access into the identity of users.

Be on the lookout for these assets to get cherry-picked and look forward to reading your future newspaper owned by Google, Facebook and the usual cast of characters.

The recently elevated existential risk that big cap tech is coping with will see meaningful reforms that will implement better defensive tactics, pre-emptive posturing to promote a positive big-picture narrative, and a bulletproof attempt to protect the moats around lucrative business models.

Stay away from these legacy newspaper stocks and only weigh up the media stocks that have already pivoted to the online streaming business model of scaling original premium content.

__________________________________________________________________________________________________

Quote of the Day

"The real danger is not that computers will begin to think like men, but that men will begin to think like computers." - said journalist Sydney Harris.

Mad Hedge Technology Letter

April 23, 2018

Fiat Lux

Featured Trade:

(HOW NETFLIX CAN DOUBLE AGAIN),

(NFLX), (AMZN), (IQ), (ORCL), (MU), (AMAT), (CRUS), (QRVO), (IFNNY), (NVDA), (JD), (BABA), (MSFT)