Copenhagen's Cash Cow

The first time I visited Denmark, my taxi driver had an unusual conversation starter.

"You know what's our biggest company?" he asked, navigating Copenhagen's rain-slicked streets. "Not LEGO, not Maersk. It's the diabetes people." He was right.

Novo Nordisk (NVO), which began in the 1920s with a borrowed insulin recipe and a dream of treating diabetes, has morphed into Denmark's crown jewel of pharmaceuticals.

The company that once extracted insulin from cow pancreases (collected by the truckload from local slaughterhouses) is now making the kind of money that would make a Viking raid look like pocket change.

In the third quarter of 2024 alone, Novo Nordisk reported a 21% profit surge to 27.3 billion Danish kroner (that's $2.45 billion for those of us who don't speak currency converter).

The star of this financial show? A drug called Wegovy, whose sales have skyrocketed to 17.3 billion kroner in Q3, leaving analysts' predictions in the dust like a marathoner who's found an extra gear.

But before we pop the champagne (or the sugar-free sparkling water, given the company's focus), let's peek behind the Danish curtain.

The story of Novo Nordisk is like watching a high-wire act at the circus - thrilling, precisely executed, but with plenty of observers holding their breath about what could go wrong.

But, it's now a far cry from the days when company founders Harald and Thorvald Pedersen would personally deliver insulin to local pharmacies by bicycle.

The company has carved out its empire in the rather unglamorous-sounding GLP-1 receptor agonist market.

Don't let the clunky name fool you - this market was worth a hefty $36.79 billion in 2023 and is growing faster than bacteria in a petri dish, with projections showing a 21.65% annual growth rate from 2024 to 2030.

By 2031, we're looking at a potential $150 billion market, with obesity treatments accounting for $90 billion of that pie.

Novo Nordisk's triple threat - Wegovy, Ozempic, and Rybelsus - have been dominating this space like a scientific dream team.

Not bad for a company that once had to import porcine intestines from China to keep up with insulin production in the 1960s.

But success attracts competition like moths to a flame, and the flames are getting crowded.

Enter Eli Lilly (LLY), strutting into the party with Mounjaro, which raked in $1.5 billion in Q2 2024 sales alone - a 71% quarterly growth that probably caused some sleepless nights in Denmark.

Meanwhile, Amgen (AMGN) and Viking Therapeutics (VKTX) are cooking up their own weight-loss concoctions in their respective labs.

Viking's oral GLP-1 drug is particularly interesting - imagine taking a pill instead of giving yourself a shot. For needle-phobic patients, that's like choosing between a day at the spa and a day at the dentist.

Speaking of setbacks, Novo Nordisk recently had to wave the white flag on ocedurenone, their hoped-for kidney disease drug.

After spending $1.3 billion to acquire it from KBP Biosciences (ouch), the phase 3 trial results came back with all the excitement of a flat sofa.

The company had to write off $816.5 million - the kind of number that makes accountants reach for the antacids.

Now they're left with just one CKD program based on semaglutide, the same ingredient that makes Wegovy, Ozempic, and Rybelsus tick. It's a reminder that even in the age of sophisticated molecular modeling and AI-driven drug discovery, pharmaceutical development can still be as unpredictable as Danish weather.

As if that weren't enough to keep executives up at night, Hims & Hers Health (HIMS) is preparing to crash the party with a generic version of liraglutide (the secret sauce in Novo's older drugs Victoza and Saxenda) as soon as 2025.

While these older medications contribute less than 10% to Novo's revenue, it's like watching the first raindrops of what could become a storm.

The ghosts of those early insulin-producing pancreases might be chuckling at how history repeats itself - from fighting for insulin patents in the 1920s to defending weight loss drug territory today.

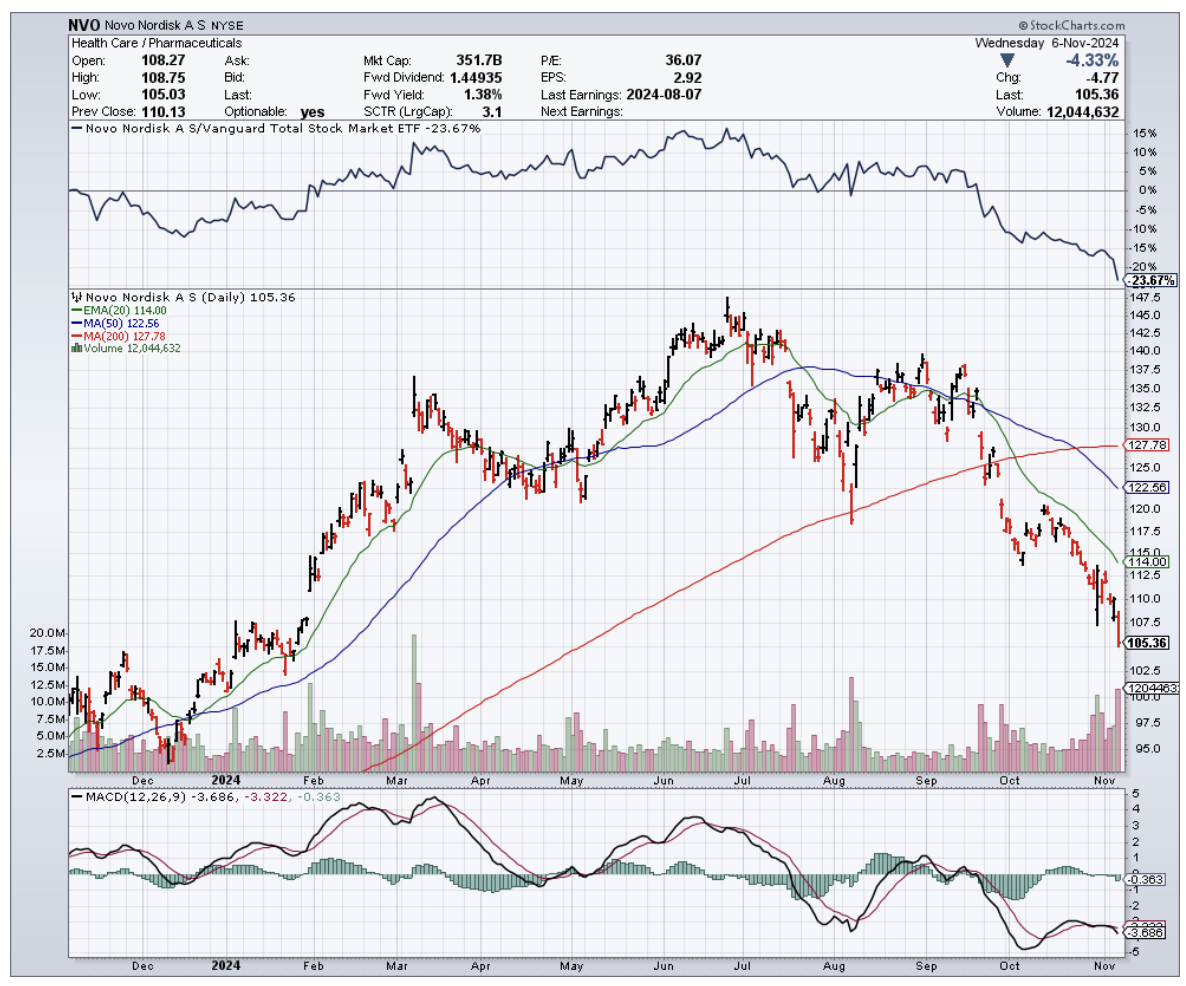

The company's stock currently trades at a forward P/E ratio of 33.2x, with analysts expecting a 22.4% annual earnings growth through 2025.

That's the kind of valuation that makes value investors break out in hives - 37 times trailing earnings and 12.95 times trailing sales means this stock is priced like a luxury handbag, where any scuff could send the price tumbling.

For those eyeing Novo Nordisk like a dessert cart at a weight-loss clinic, the decision isn't simple.

The company's dominance in the GLP-1 market is impressive, but with competitors like Eli Lilly, Amgen, and Pfizer (PFE) circling like hungry sharks, and Roche's (RHHBY) recent acquisition of Carmot Therapeutics adding another player to the mix, the waters are getting choppy.

The prudent move? Current shareholders might want to hold onto their tickets for this roller coaster ride while keeping a white-knuckled grip on the safety bar.

New investors might want to wait in line until the price becomes more reasonable - like waiting for the post-holiday sale at a luxury boutique.

And for those looking to spread their bets, Eli Lilly, Amgen, and Roche offer alternative ways to play in this space, each with their own mix of risk and potential reward.

Anyway, going back to that taxi driver in Copenhagen? He had one more thing to say: "Those Novo people, they started with dead cows and now they're making drugs from bacteria in giant steel tanks. Who knows what they'll do next?"

Indeed, from slaughterhouse pancreases to billion-dollar weight loss drugs, Novo Nordisk's story reads like a scientific fairy tale. But in the world of biotech investing, even fairy tales need solid earnings reports.

For now, this Danish giant continues to prove that sometimes the best investment stories start with someone asking, "What if we could do this better?" - even if "this" means figuring out how to get insulin from a cow pancreas.