When things can’t be better, they really can’t get any better, and there is no upside left.

As I expected, big tech companies announced earnings for the ages, the top four totaling a staggering $56.6 billion in profits in Q2, or $226.4 billion annualized. That compares to total US Q1 profits of $2.347 trillion. Then their stocks fell apart, with Amazon leading the charge to the downside.

To say tech earnings were impressive would be a vast understatement, with Apple (AAPL) coming in at $21.7 billion, Amazon (AMZN) at $7.8 billion, Facebook (FB) at $10.4 billion, and Microsoft (MSFT) at $16.7 billion.

However, since we are in the “What have you done for me lately” business, what do we have to look forward in August?

Covid cases are soaring nationally tripling off the 15,000 a day lows of a month ago. The delta variant is twice as contagious and twice as fatal as earlier ones. Mask mandates are back in the big cities, pushing back economic growth and a jobs recovery out into 2022. The least vaccinated stated are seeing hospital systems overwhelmed once again. School reopenings are now an unknown, and if they do, it will be with masks.

I sent my kids to a Boy Scout camp this week. On the second day, two unvaccinated staff members tested positive for delta and the county immediately shut the place down, sending home 500 disappointed scouts and parents. Dreams of long sought merit badges went up in smoke. The same thing is happening across the entire economy.

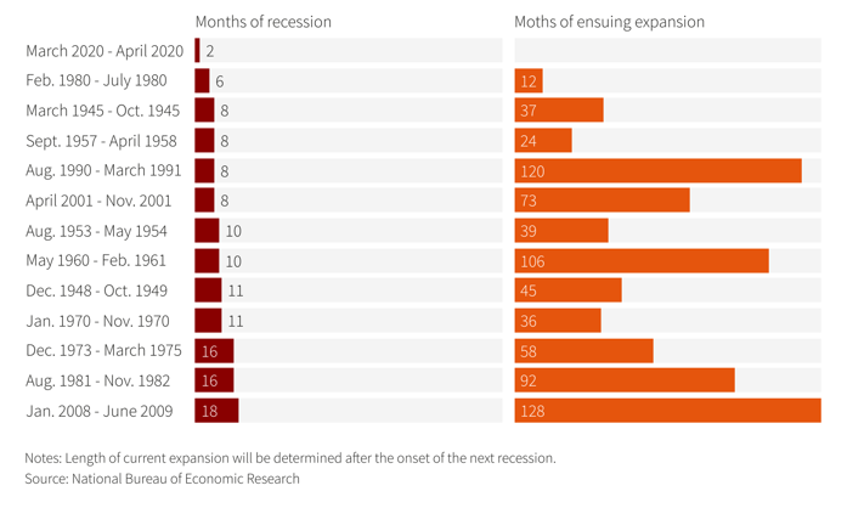

The next three months are historically the worst performing of the year, generating an average 0.03% over the last 100 years. Inflation reports are going to remain high for the rest of the year. The Fed has a new reason to keep interest rates a zero for longer, bad for banks, brokers, commodities, and industrials.

Oh, and the next round of spectacular tech earnings are three months away.

There is another factor in play. Investors have made the most money in their lives over the last 16 months, including me. The temptation to take the money and run is strong and irresistible. Traders have visions of Ferraris dancing in their eyes. This alone would bring on an overdue 5%-10% pull back.

So what is the smart thing to do here? Sell all your short-term positions but keep all your long-term positions and LEAPS. The market isn’t going down enough to justify the round-trip expenses and capital gains taxes.

If you have new cash flows keep it in money market funds. People will be shocked by the speed and viciousness of the coming selloff. But when it occurs, the best buying opportunity in a year will be on its knees begging for your attention.

It may feel cataclysmic, another Armageddon, and like the end of the world, but it won’t be. After all, we have seen no less than 36 10% corrections in my lifetime. The investors who hung in made the most money every single time.

I’ll tell you when we hit bottom with a raft of new LEAPS recommendations, provided I can get them out fast enough.

The Fed stands pat, keeping overnight rates at 0%-0.25%. The delta variant has pushed the taper off three months, but Jay Powell gave the barest of hints that it is the next step to take. We have 9 million unemployed and 9 million job openings but there is a massive skills gap, with jobless waitresses and retails in over supply and coders and artificial intelligence specialist sought after. It’s all the result of 40 years of under investment in our education system.

US Q2 GDP comes in at 6.5%, one of the strongest in economic history, but less than forecasts that were as high as 10%. Supply chain restraints we the main explanation for the shortfall. All that does is push growth into 2022, when people CAN get parts and labor. In the meantime, personal consumption soared by 11.8%, the hottest report since 1952, proving the demand is there.

Covid Cases triple from recent lows to 43,700 a day. Blame the delta variant, which originated in India, and now accounts for 86% of new cases. Twice as contiguous, with a greater fatality rate and more long-term effect, delta is prompting the return of mask mandates in several cities. Only the unvaccinated are affected. This could be the trigger for the next correction.

Smart phones will deliver the next big chip shortage, even if the chip shortage for cars abates. The bad news? There are 22 times more phones produced each year than cars, 1.4 billion versus only 64 million in 2020. Out of the frying pan and into the fire.

S&P Case Shiller smashes all records, up 17% YOY for national home prices. Phoenix (25.9%), San Diego (24.7%), and Seattle (23.4%) lead. These numbers are past “extraordinary.” Expect it to continue.

New Homes Sales plunge to 676,000, down 6.6% on a signed contract basis, but prices are up 6%. Inventories are up from 5 months to a still low 6.5 months. Shortages of land, labor, and materials are still the big issue.

Pending Home Sales drop 1.9% in June on a signed contract bases. High prices are curing high prices, with the Case-Shiller National Home Price Index up 17% YOY. The south and west posted the biggest declines. Single family homes have dropped for three months in a row to a one year low.

China meltdown continues, with the Beijing government apparently withdrawing from western capital markets. It’s all about showing the world who is in charge and punishing the billionaires by destroying their stocks. They are wiping out $1 trillion in equity per day and don’t care if you get hit as well. Cathy Wood’s Ark Innovation ETF (ARKK) is dumping everything they have. Avoid China at all cost.

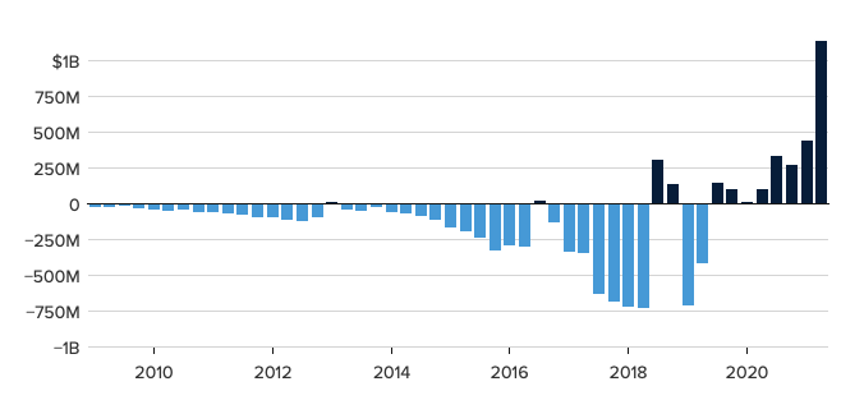

Tesla announces first $1 billion profit in Q2, despite losing $23 million in Bitcoin. That is 10X the year ago report. They could have made a lot more if they had more chip supplies. The energy business brought in a rapidly growing $800 million in revenues. The Austin and Berlin Gigafactory’s are coming online at the end of the year, allowing them to scale globally. The Cybertruck is on hold and production of Powerwall’s cut back until they can get more chip supplies, creating extreme shortages. Buy (TSLA) on dips. There’s a 10X from here.

Tesla claims No.2 auto sales spot in Europe in June, just behind Volkswagen’s Golf, and beathing Daimler Benz, Audi, Fiat, and Renault. The company shipped 25,697 Model 3’s, which is perfect for the continent’s tight spaces, short distances, and green preferences. Big government subsidies to switch from internal combustion engines helped too.

Tesla Profits

Bitcoin tops $40,000 in a massive short covering rally. Tesla may start taking the crypto currency as payment for new vehicles and Amazon (AMZN) may get into the game as well. While China is studying way to make a digital yuan (CYB) and Europe a digital Euro (FXE), the US congress sees such a move as pointless.

Robinhood IPO (HOOD) Bombs, trading down as much as 12% from its $38.00 IPO price. That leaves it with a still impressive $29 billion market capitalization, a fifth the size of Morgan Stanley. What happens when individuals get their allocations? No “diamond hands” here. It looks like a “BUY” after it drops by half opportunity, just like Tesla after its IPO. The facilitator of meme stock frenzies has best ever year is behind it, or until we get another pandemic. The company has already paid $127 million in fines and almost went under in January. Avoid (HOOD) for now.

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 800% to 240,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 240,000 here we come!

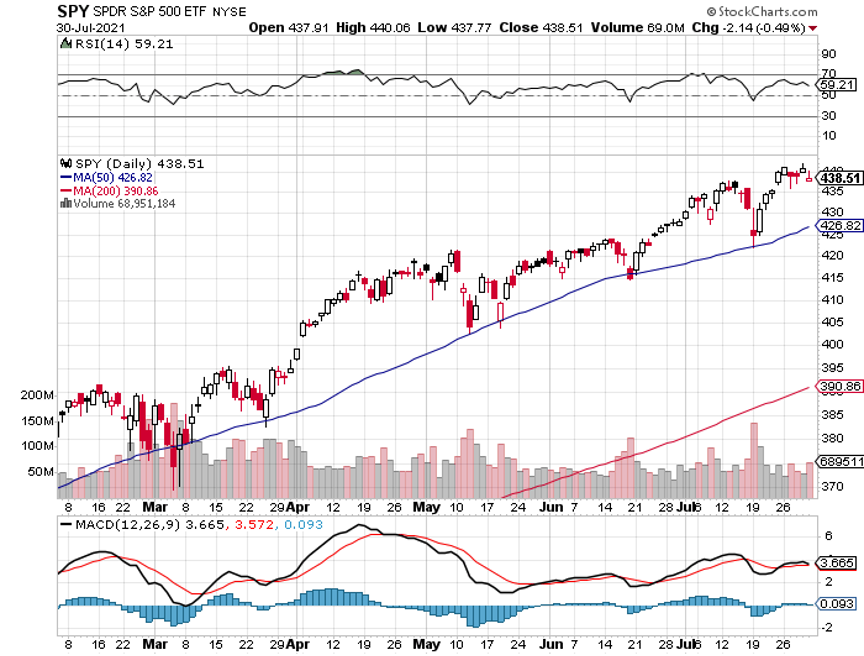

My Mad Hedge Global Trading Dispatch saw a modest +0.61% in July. My 2021 year-to-date performance appreciated to 69.21%. The Dow Average was up 14.16% so far in 2021.

I stuck with my four positions, a long in (JPM) and a short in the (TLT) and a double short in the (SPY). I bled all the way until Friday, when big hits to tech stocks took the (SPY) down and edging me up to a positive return for July. That leaves me 60% in cash. I’m keeping positions small as long as we are at extreme overbought conditions.

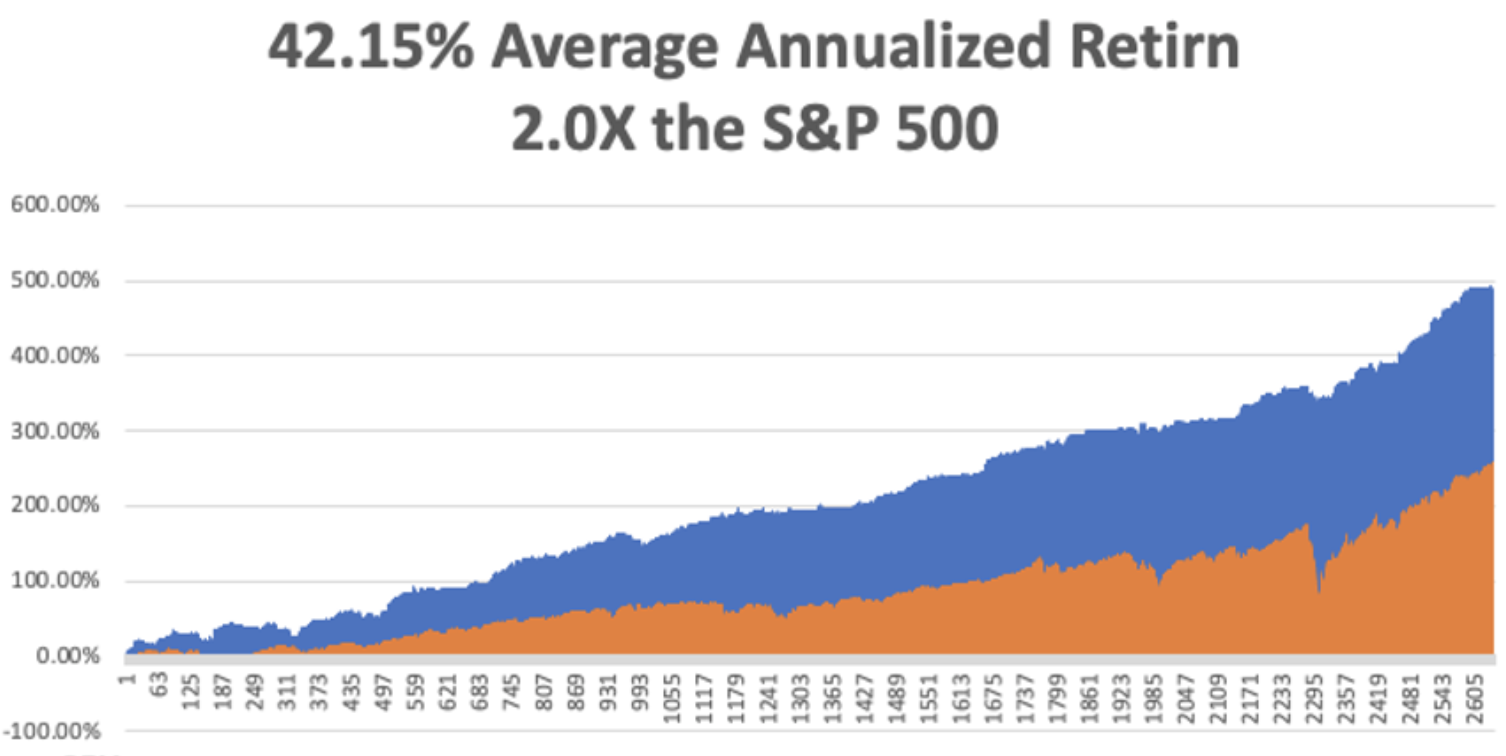

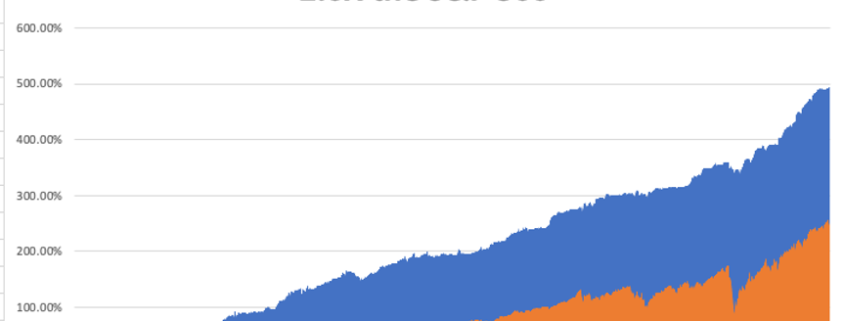

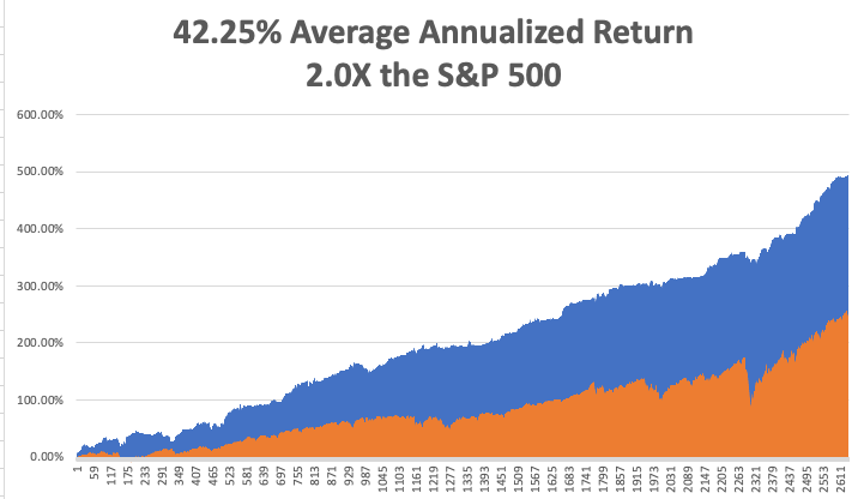

That brings my 11-year total return to 491.76%, some 2.00 times the S&P 500 (SPX) over the same period. My 12-year average annualized return now stands at an unbelievable 12.15%, easily the highest in the industry.

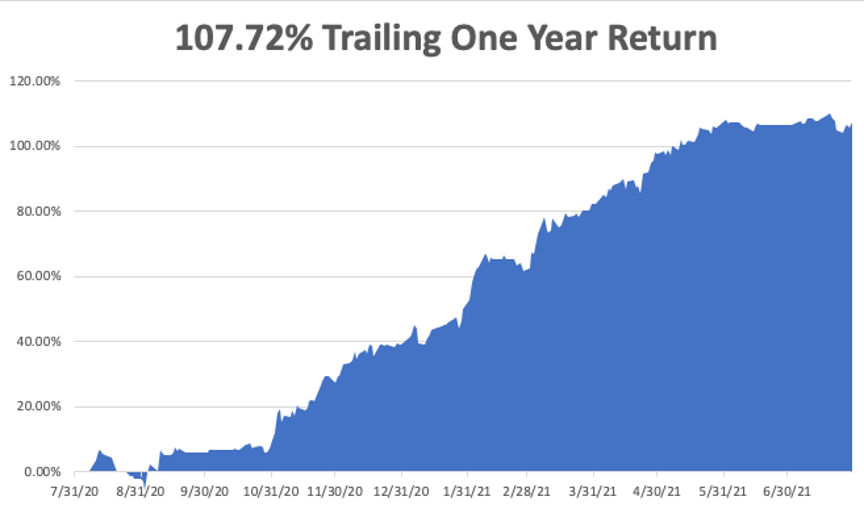

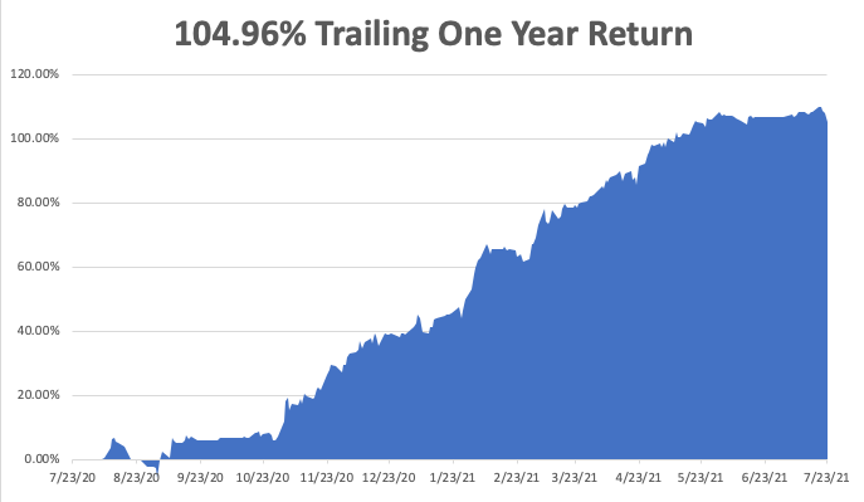

My trailing one-year return retreated to positively eye-popping 107.72%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Corona virus cases at 34.9 million and rising quickly and deaths topping 613,000, which you can find here.

The coming week will bring our monthly blockbuster jobs reports on the data front.

On Monday, August 2 at 7:00 AM, the Manufacturing PMI for July is published. NXP Semiconductor (NXP) reports.

On Tuesday, August 3, at 7:30 AM, Factory Orders for June are released. Amgen (AMGN), Eli Lily (LLY), and Alibaba (BABA) report.

On Wednesday, August 4 at 5:30 AM, the ADP Private Employment Report is published. Uber (UBER) and General Motors (GM) report.

On Thursday, August 5 at 8:30 AM, Weekly Jobless Claims are announced. Square (SQ) reports.

On Friday, August 6 at 8:30 AM, we get the Nonfarm Payroll Report for July. Berkshire Hathaway (BRKB) reports.

As for me, I am reminded of my own summer of 1967, back when I was 15, which may be the subject of a future book and movie.

My family summer vacation that year was on the slopes of Mount Rainier in Washington state. Since it was raining every day, the other kids wanted to go home early. So my parents left me and my younger brother in the hands of Mount Everest veteran Jim Whitaker to summit the 14,411 peak (click here for his story). The deal was for us to hitch hike back to Los Angeles when we got off the mountain.

In those days, it wasn’t such an unreasonable plan. The Vietnam war was on, and a lot of soldiers were thumbing their way to report to duty. My parents figured that since I was an Eagle Scout, I could take care of myself.

When we got off the mountain, I looked at the map and saw there was this fascinating country called “Canada” just to the north. So, it was off to Vancouver. Once there, I learned there was a world’s fair going on in Montreal some 2,843 away, so we hit the TransCanada Highway going east.

We ran out of money in Alberta, so we took jobs as ranch hands. There we learned the joys of running down lost cattle on horseback, working all day at a buzz saw, inseminating cows, and eating steak three times a day. I made friends with the cowboys by reading them their mail, which they were unable to do. There were lots of bills due, child support owed, and alimony demands.

In Saskatchewan, the roads ran out of cars, so we hopped a freight train in Manitoba, narrowly missing getting mugged in the rail yard. We camped out in a box car occupied by other rough sorts for three days. There’s nothing like opening the doors and watching the scenery go by with no billboards ad, the wind blowing through your hair!

When the engineer spotted us on a curve, he stopped the train and invited us to up the engine. There, we slept on the floor, and he even let us take turns driving! That’s how we made it to Ontario, the most mosquito-infested place on the face of the earth.

Our last ride into Montreal offered to let us stay in his boat house as long as we wanted so there we stayed. Thank you, WWII RAF bomber pilot Group Captain John Chenier!

Broke again, we landed jobs at a hamburger stand at Expo 67 in front of the imposing Russian pavilion. The pay was $1 an hour and all we could eat. At the end of the month, Madame Desjardin couldn’t balance her inventory, so she asked how many burgers I was eating a day. I answer 20, and my brother answered 21. “Well, there’s my inventory problem” she replied.

And then there was Suzanne Baribeau, the love of my life. I wonder whatever happened to her?

I had to allow two weeks to hitch hike home in time for school. When we crossed the border at Niagara Falls, we were arrested as draft dodgers as we were too young to have driver’s licenses. It took a long conversation between US Immigration and my dad to convince them we weren’t.

We developed a system where my parents could keep track of us. Long distance calls were then enormously expensive. So, I called home collect and when my dad answered he asked what city the call was coming from. When the operator gave him the answer, he said he would not accept the call. I remember lots of surprised operators. But the calls were free, and dad always knew where we were.

We had to divert around Detroit to avoid the race riots there. We got robbed in North Dakota, where we were in the only car for 50 miles. We made it as far has Seattle with only three days left until school started.

Finally, my parents had a nervous breakdown. They bought us our first air tickets ever to get back to LA, then quite an investment.

I haven’t stopped traveling since, my tally now topping all 50 states and 135 countries.

And I learned an amazing thing about the United States. Almost everyone in the country is honest, kind, and generous. Virtually every night, our last ride of the day took us home and provided us with an extra bedroom or a garage to sleep in. The next morning, they fed us a big breakfast and dropped us off at a good spot to catch the next ride.

It was the adventure of a lifetime and am a better man for it.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Summit of Mt. Rainier 1967

McKinnon Ranch Bassano Alberta 1967

American Pavilion Expo 67

Hamburger Stand at Expo 67

Picking Cherries in Michigan 1967