I feel obliged to reveal one corner of this bubbling market that might actually make sense.

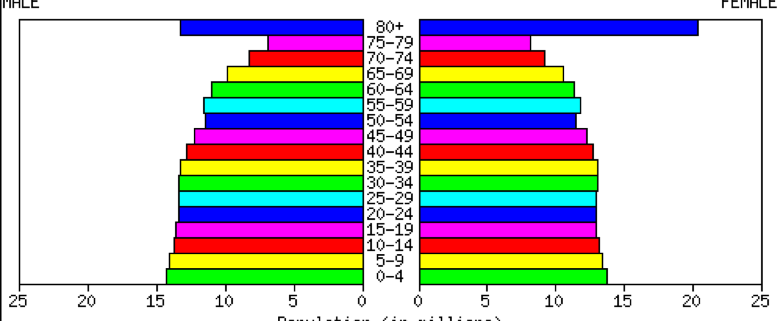

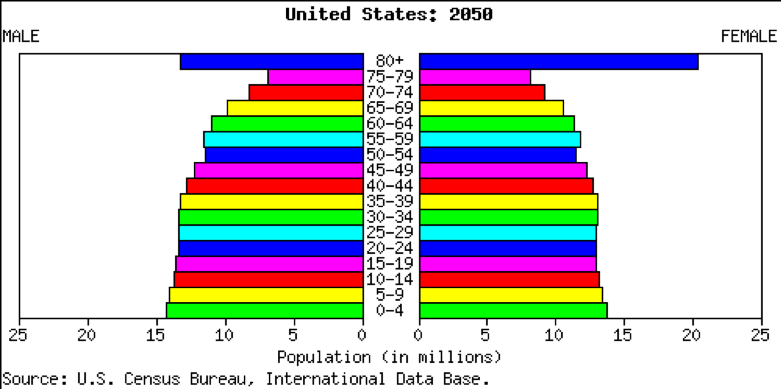

By 2050, the population of California will soar from 39 million to 50 million, and that of the US from 330 million to 400 million, according to data released by the US Census Bureau and the CIA Fact Book (check out the two population pyramids below).

That means enormous demand for the low end of the housing market, apartments in multi-family dwellings.

Many of our new citizens will be cash-short immigrants. They will be joined by generational demand for limited rental housing by 65 million Gen Xers and 85 million Millennials enduring a lower standard of living than their parents and grandparents.

These people aren't going to be living in cardboard boxes under freeway overpasses.

If you have any millennial kids of your own (I have three!), you may have noticed that they are far less acquisitive and materialistic than earlier generations.

They would rather save their money for a new iPhone than a mortgage payment. Car ownership is plunging, as the “sharing” economy takes over.

This explains why the number of first-time homebuyers, only 32% of the current market now, is near the lowest on record.

It’s not like they could buy if they wanted to.

Remember that this generation is almost the most indebted in history, with $1.6 trillion in student loans outstanding.

They don’t care. Coming of age since the financial crisis, to them, homeownership means falling prices, default, and bankruptcy. Bring on the “renter” generation!

The trend towards apartments also fits neatly with the downsizing needs of 85 million retiring Baby Boomers.

As they age, boomers are moving from an average home size of 2,500 sq. ft. down to 1,000 sq ft condos and eventually 100 sq. ft. rooms in assisted living facilities.

The cumulative shrinkage in demand for housing amounts to about 4 billion sq. ft. a year, the equivalent of a city the size of San Francisco.

In the aftermath of the economic collapse, rents are now rising dramatically, and vacancies rates are shrinking, boosting cash flows for apartment building owners.

Fannie Mae and Freddie Mac Financing is still abundantly available at the lowest interest rates on record. Institutions combing the landscape for low volatility cash flows and limited risk are starting to pour money in.

Run the numbers on the multi-dwelling investment opportunities in your town. You’ll find that the net after-tax yields beat almost anything available in the financial markets.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/08/2050-population.png389781Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-07-01 09:02:542021-07-01 11:01:25A Very Bright Spot in Real Estate

"The difference between a Tesla and all of its competitors is the difference between an iPod and a cassette player," said Harvard Law fellow Vivek Wadhwa.

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00MHFTRhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMHFTR2021-07-01 09:00:002021-07-01 10:59:36July 1, 2021 - Quote of the Day

“The last few years have been periods of high returns and relatively low volatility. I think with the yield curve inversion and the economy slowing, PMI is in contraction in much of the world ... we’re entering a period that’s the opposite of that. We’re going to have lower returns and substantially higher volatility,” said Ben Kirby of Thornburg Investment Management.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/09/JohnThomas-Sept20-e1537393647191.png327224Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-29 09:00:572021-06-29 11:46:34June 29, 2021 - Quote of the Day

I received an email from a reader last week that I really had no idea what the stock market was going to do and that I was just guessing.

I answered that I couldn’t agree more. These are unprecedented times for the American economy. There is no playbook for what is going on, we’re just making it up.

“I’m guessing, Jay Powell is guessing, we’re all guessing.” I threw in an afterthought: “guessing and hoping.”

That is why the hottest inflation rate in 13 years sends interest rates into freefall when they should be soaring.

I have been one of the most bullish strategists in the market since the March 2009 low and have been richly rewarded as a result. (Even though being bearish sells more newsletters). You have been too.

I thought the market was overdue for a 7.8% correction. So, even I was flabbergasted when the latest market selloff amounted to only a meager 4.3%. There is still so much money trying to get into the market it is unable to go any lower.

Don’t get fooled again, to quote that eminent market guru, Peter Townsend.

Which raises an issue for investors. That 7.8% correction I thought was overdue is still ahead of us. That demands caution and prudence for shorter term investors. Long term investors can work on their golf swings or take that dreamed of round the world cruise.

What was especially encouraging last week was the leadership maintain by the big five tech stocks. I ran some numbers last week to see if there was more than meets the eye and came up with some eye-popping results.

The rocket fuel last week was provided by progress by an infrastructure bill that could unleash another $579 billion. That could be enough stimulus to keep the recovery on steroids powering well into 2022.

Big tech stocks saw this a month ago when they started discounting robust 2023 earnings reports much farther in advance than usual.

The top five big tech companies, Apple (AAPL), Amazon (AMZN), Alphabet (GOOGL), Facebook (FB), and Microsoft (MSFT), earned a staggering $88 billion in profits in Q1, or an annualized $332 billion.

That amounts to an average 40% YOY growth rate. Some 16.7% of total US profits of $1,984 billion was generated by only 2% of the workforce. These are positively ballistic numbers. Tech was never going to be down for long. That’s why most went to new all-time highs last week.

Don’t get fooled again.

The Infrastructure Deal is done, at $579 billion in new spending, will provide a further boost to the economy. The climate had to be cut to get Republican support. Transportation is the big winner at $312 billion. Grid and broadband upgrades received major funding. I don’t think that Biden expected to get his whole $2 trillion. It was just a negotiating strategy. Still, something is better than nothing. Look for Infrastructure 2.0 after the 2022 midterms with lots of climate spending. NASDAQ Hit New High. Prime day has catapulted Amazon (AMZN). Microsoft (MSFT) became the second $2 trillion company and Alphabet (GOOGL) will probably be next. Apple (AAPL) is bringing up the rear but could hit new highs in the coming months. The big question is whether this is a one-night stand or a long-term relationship with the bull. Me, being the stable guy that I am, vote for the latter. Poof, Inflation is Gone! Almost all commodity prices have given up their 2021 gains after traumatic selloffs over the past weeks. Bad boy lumber has dropped by half, and bitcoin has been slaughtered. That puts interest rate hikes on hold. In the meantime, Tesla (TSLA) and the Ark stocks are recovering. Load the boat with big tech, we are going to new all-time highs across the board. Turns out the Fed was right after all. Weekly Jobless Claims drop to 411,000, down from the pandemic peak of 900,000 in January. We’re headed to 100,000 by yearend.

$1.2 Trillion Poured into Equities in H1, more than double the previous 2007 record. Corporate share buybacks are also approaching new highs. That means the 150-day moving average for the (SPY) should hold well into 2022. As high as we are, equities are still the best game in town. Bitcoin battles at $30,000, for the fourth time in two months, at one point falling to a $24,000 low. China miners, about 70% of the total, are facing a total ban. Many loaded their servers on planes over the weekend and moved to unregulated Maryland or Virginia. The charts are pointing towards a $20,000 bottom. The ultra bulls are targeting $100,000 by yearend. Existing Home Sales down for the fourth month, down 0.9% to an annualized 5.8 million in May. Shortage of supply remains the big problem with inventories at an incredible 2.5 months. Some 89% of the homes sold were on the market for less than a month. Conditions will get a lot worse before they get better.

New Home Sales dive 5.9%, thanks to shortage of supply and high prices. Labor, land, and lumber are through the roof. The median price of a home sold in May is $374,400, up a staggering 18% YOY. Supplies rose to 5.1 months. The cure for high prices is high prices. This trend should last a decade. AmazonPrime Day Sales top $11 billion, including the Havaheart 0754 single door humane rabbit trap I bought for only $27. That made Monday and Tuesday the biggest online sales days of the year. Use the recent profit-taking to load up on (AMZN) shares and LEAPS. It’s headed to $5,000. Oh, and I’ve caught three rabbits so far. Intel to build huge German chip factory,to address the global shortage. Germany’s largest auto industry makes it a natural location. Buy (INTC) on dips. NVIDIA is going ballistic, with Raymond James raising its target to $900 as the best-positioned chip company over the long term. I was early at $1,000. The explosion in crypto has been a big plus. A new generation of high-end gaming is coming where (NVDA) has a complete monopoly and supplies are short. I have bought six of their GeForce and RTX graphics cards in the past month. But artificial intelligence is the big grower over the long term, which is exploding everywhere, and their $5,000 Tesla M10 GPU is dominant. Buy (NVDA) now. We may lose Christmas, as lack of containers and ships makes transport from China problematic. Home Depot (HD) has chartered its own ship to make up for the shortfall, and Target (TGT) is considering the same. Conditions are so bad there is also a fireworks shortage for the Fourth of July where China is a major supplier (they invented them).

My Ten Year View

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch profit reached 0.71% gain so far in June on the heels of a spectacular 8.13% profit in May. That leaves me 100% in cash.

My 2021 year-to-date performance appreciated to 68.60%. The Dow Average is up 12.62% so far in 2021.

I spent the week sitting in 100% cash, waiting for a better entry point on the long side. Up this much this year, there is no reason to reach for the marginal trade, the maybe instead of the certainty. I’ll leave that for the Millennials.

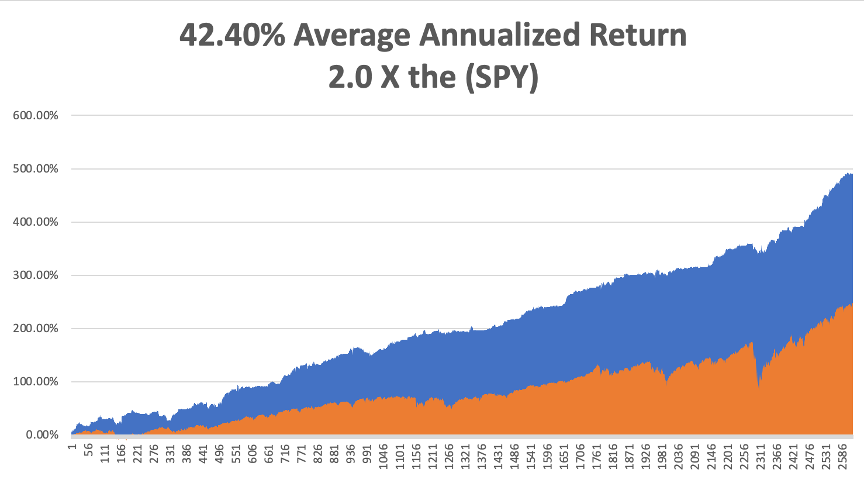

That brings my 11-year total return to 491.15%, some 2.00 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an unbelievable 42.70%, easily the highest in the industry.

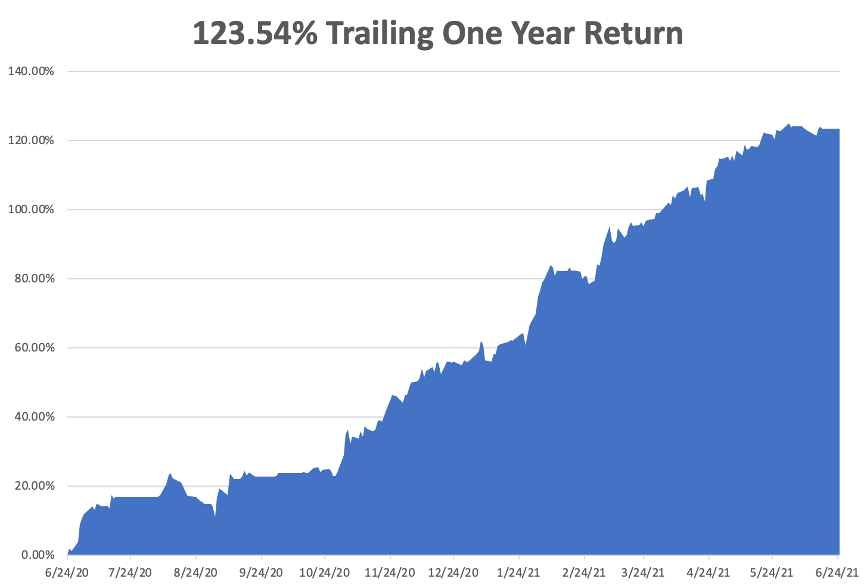

My trailing one-year return exploded to positively eye-popping 123.54%. I truly have to pinch myself when I see numbers like this. I bet many of you are making the biggest money of your long lives.

We need to keep an eye on the number of US Coronavirus cases at 33.1million and deaths topping 600,000, which you can find here. Some 33.1 million Americans have contracted Covid-19.

The coming week will be a weak one on the data front.

On Monday, June 28 at 10:30 AM, the Dallas Fed Manufacturing Index for June is out.

On Tuesday, June 29 at 9:00 AM, the S&P Case Shiller National Home Price Index is published.

On Wednesday, June 30 at 8:15 AM, the ADP Private Employment Report is released.

On Thursday, July 1 at 8:30 AM, the Weekly Jobless Claims are published.

On Friday, July 2 at 8:30 AM, the all-important June Nonfarm Payroll Report is announced. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, I’m in Los Angeles this week visiting old friends, and I am reminded of one of the weirdest chapters of my life.

There were not a lot of jobs in the summer of 1971, but Thomas Noguchi, the LA County Coroner, was hiring. The famed USC student jobs board had delivered! Better yet, the job included free housing at the coroner's department.

I got the graveyard shift, from midnight to 8:00 AM. All I had to do was buy a black suit from Robert Halls for $25.

Noguchi was known as the “coroner to the stars” having famously done the autopsies on Marlin Mansfield and Jane Mansfield. He did not disappoint.

For three months, whenever there was a death from unnatural causes, I was there to pick up the bodies. If there was a suicide, gangland shooting, or horrific car accident, I was your man.

Charles Manson had recently been arrested and I was tasked with digging up the victims. One, cowboy stuntman Shorty Shay, had his head cut off and neatly placed in between his ankles.

The first time I ever saw a full set of women’s underclothing, a girdle and pantyhose, was when I excavated a desert roadside grave that the coyotes had dug up. She was pretty far gone.

Once, I and another driver were sent to pick up a teenaged boy who had committed suicide in Beverly Hills. The father came out and asked us to take the mattress as well. I regretted that we were not allowed to do favors on city time. He then said, “Can you take it for $200”, then an astronomical sum.

A few minutes later found a hearse driving down the Santa Monica freeway on the way to the dump with a double mattress expertly tied on the roof with Boy Scout knots with a giant blood spot in the middle.

Once, I was sent to a cheap motel where a drug deal gone bad had produced several shootings. I found $10,000 in a brown paper bag under the bed. The other driver found another ten grand and a bag of drugs and kept them. He went to jail. Eventually, I figured out that handling dead bodies could be hazardous to your health, so I asked for rubber gloves. I was fired.

Still, I ended up with some of the best summer job stories ever.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

https://www.madhedgefundtrader.com/wp-content/uploads/2020/04/john-gardening.png429308Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-28 09:02:582021-06-28 11:48:21The Market Outlook for the Week Ahead, or Don’t Get Fooled Again

I realized that perhaps I had bitten off too much taking the Boy Scouts on a 50-mile hike one minute into the adventure.

Cutting everything to the bone, I was only able to trim my pack down to 50 pounds. That was with chopping my food ration in half, leaving an extra cell phone battery behind, and bringing only one set of clothes.

However, I had to bring a five-pound first aid kit to care for the 14 scouts, my own tent, and all the maps needed to keep us on course.

Then at the last minute, another five pounds of medical releases, a satellite phone, and an electronic thermometer were dumped on me by worried parents, taking my load up to a bone-breaking 55 pounds.

That’s a lot for a 68-year-old. That’s a lot for anyone.

But then the Desolation Wilderness, the roof of the High Sierras, is one of the most stunningly beautiful places on the planet. All other outdoor trips for the Boy Scouts this year had been cancelled, thanks to the pandemic. And at my age, who knows how many 50-mile hikes I have ahead of me? It was now, or maybe never.

But then the Desolation Wilderness, the roof of the High Sierras, is one of the most stunningly beautiful places on the planet. All other outdoor trips for the Boy Scouts this year had been cancelled thanks to the pandemic. And at my age, who knows how many 50-miles hikes I have ahead of me? It was now, or maybe never.

We took temperatures every morning. All 50 miles were hiked with masks, as did every other group we ran into. Carpooling was banned and every parent had to bring up their own kid to Lake Tahoe. It all worked as no one got sick.

We didn’t do just any 50-mile hike. We attacked one of the toughest in the United States. The first two days demanded a 3,200-vertical climb, from Meeks Bay to Phipps Pass, from 6,200 to 9,400 feet. The kids barely noticed the altitude. The adults did.

The Desolation Wilderness (click here for permits at https://www.recreation.gov/permits/233261 ) is a 50-mile by 30-mile slab of granite left behind by the last ice age. It is graced with 100 brilliant blue lakes. It looks like a giant’s playground, with enormous boulders and huge fallen trees scattered about the landscape.

Black bears were an ever-present danger, as the area was undergoing an unprecedented “bear bloom.” Other hikers reported being harassed all night by the ursine creatures, one even invading a tent in search of food. A Cliff Bar beats clawing termites out of a dead log any day.

However, we observed the strictest of bear practices, bagging our food every night and hanging it from tall trees. It became our nightly entertainment, to see who could do the best bear bag hang. Of course, getting it down the next morning was another story.

The area had changed a lot since my grandfather brought me up to Desolation 60 years ago with a horse, a mule, a Winchester, and all the fishing gear we could carry. Then wilderness survival meant bringing in plenty of canned food and a nice 16-inch iron skillet, not the tasteless freeze-dried versions of today.

You never saw a single soul for a week. You caught your full limit of ten rainbow and brook trout as fast as you could bait the hooks. For fun, we would rummage through old log cabins outfitted with potbellied stoves for 100-year-old supplies left behind by the 19th century California gold rush. Once, we even found a crashed airplane that had been missing since the 1930s.

Nobody ever went up there.

This time around, we passed other hikers once an hour. Every lake was completely fished out. In fact, the park saw record crowds with people flocking to the safety of the great outdoors to flee the epidemic at home. Inexperienced with the outdoors, they attracted even more hungry bears.

The scouts developed a daily routine of cooking breakfast, breaking camp, hiking ten miles, searching for the ideal camping spot, setting up tents, and cooking dinner. In the process, they learned organization, self-sufficiency, responsibility, and survival skills. They don’t teach these in schools anymore.

Free time was spent playing cards for food. Winners accumulated highly sought-after beef stroganoff. The losers ended up with the despised chicken tetrazzini. I stuck to my granola bars.

On the last day, we straggled back to Meeks Bay worn, bleeding, exhausted, but exhilarated. Every morning, we woke up to a Christmas calendar view. The parents couldn’t believe we finished the entire challenging 50 miles without a major injury.

I was especially proud of my own 15- and 16-year old daughters, who are probably the first girls to ever complete a 50 miler in a Boy Scout event. The apples don’t fall far from the tree.

Everyone became eligible for the elite Boy Scout 50-Mile Patch, which few in the scouting movement ever achieve.

During much of the week, scouts were carping about the difficulty of the trail, the mosquitoes, and the sparse offerings of food. They fantasized about the first thing they would eat on return to civilization (banana split, pancakes with whipped cream, a Big Mac, or all three).

By the end of the week, they were talking about the next 50-mile hike. With their 2021 spring break trip to the Boy Scout Florida Sea Base cancelled, suddenly California’s Lost Coast looks very inviting.

That is, providing we can deal with the bears and the mosquitoes.

https://www.madhedgefundtrader.com/wp-content/uploads/2020/08/John-napping.png350408Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-25 09:02:252021-06-25 11:17:01Back From My 50-Mile Hike

(WHY DOCTORS, PILOTS, AND ENGINEERS MAKE TERRIBLE TRADERS)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2021-06-24 10:04:482021-06-24 11:00:39June 24, 2021

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.