I know all of this may sound confusing at first. But once you get the hang of it, this is the greatest way to make money since sliced bread.

I still have six positions left in my model trading portfolio, they are all deep in-the-money, and about to expire in six trading days. That opens up a set of risks unique to these positions.

I call it the “Screw up risk.”

As long as the markets maintain current levels, ALL of these positions will expire at their maximum profit values.

They include:

Risk On (World is Getting Better)

(TLT) 8/$157-$160 put spread 10.00%

(TLT) 8/$156-$159 put spread. 10.00%

(JPM) 8/$300-$320 call spread 10.00%

(V) 8/$220-$225 call spread 10.00%

(GS) $355-$365 call spread 10.00%

Risk Off (World is Getting Worse)

(SPY) 8/$445-$450 put spread -10.00%

Total Net Position 40.00%

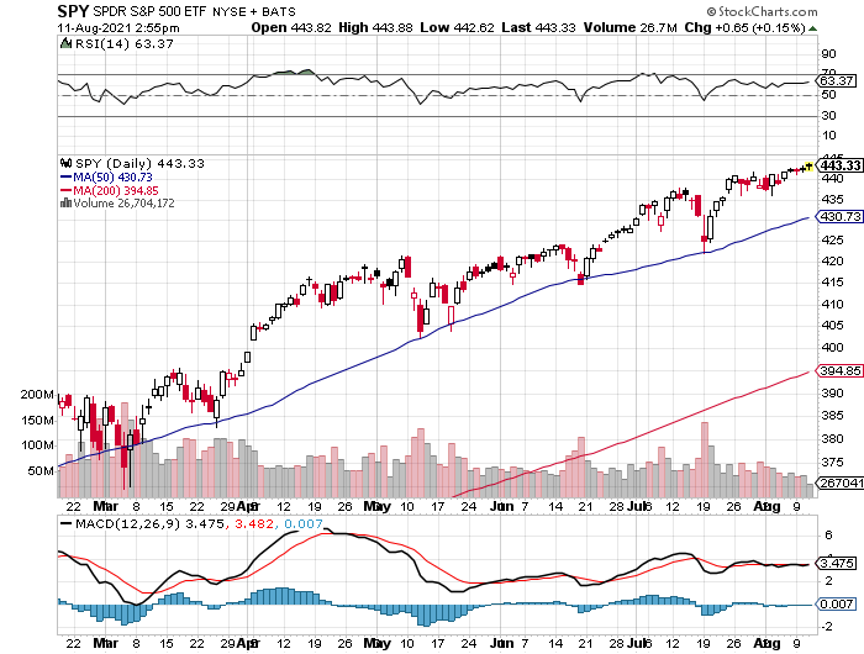

With the August 20 options expiration upon us, there is a heightened probability that your short position in the options may get called away.

If it happens, there is only one thing to do: fall down on your knees and thank your lucky stars. You have just made the maximum possible profit for your position instantly.

Most of you have short option positions, although you may not realize it. For when you buy an in-the-money vertical option spread, it contains two elements: a long option and a short option.

The short options can get “assigned,” or “called away” at any time, as it is owned by a third party, the one you initially sold the put option to when you initiated the position.

You have to be careful here because the inexperienced can blow their newfound windfall if they take the wrong action, so here’s how to handle it correctly.

Let’s say you get an email from your broker telling you that your call options have been assigned away.

I’ll use the example of the Goldman Sachs (GS) call spread.

For what the broker had done in effect is allow you to get out of your call spread position at the maximum profit point days before the August 20 expiration date. In other words, what you bought for $8.60 on August 4 is now worth $10.00, giving you a near-instant profit of 16.27%!

In the case of the Goldman Sachs (GS) August 20 $200-$210 in-the-money vertical Bull Call spread, all you have to do is call your broker and instruct them to “exercise your long position in your (GS) August 20 $355 calls to close out your short position in the (GS) August 20 $365 calls.”

You must do this in person. Brokers are not allowed to exercise options automatically, on their own, without your expressed permission.

This is a perfectly hedged position, with both options having the same name and the same expiration date, so there is no risk. The name, number of shares, and number of contracts are all identical, so you have no exposure at all.

Calls are a right to buy shares at a fixed price before a fixed date, and one options contract is exercisable into 100 shares.

Short positions usually only get called away for dividend-paying stocks or interest-paying ETFs like the (TLT). There are strategies out there that try to capture dividends the day before they are payable. Exercising an option is one way to do that.

Weird stuff like this happens in the run-up to options expiration like we have coming.

A call owner may need to buy a long (GS) position after the close, and exercising his long (GS) $365 call is the only way to execute it.

Adequate shares may not be available in the market, or maybe a limit order didn’t get done by the market close.

There are thousands of algorithms out there which may arrive at some twisted logic that the puts need to be exercised.

Many require a rebalancing of hedges at the close every day which can be achieved through option exercises.

And yes, options even get exercised by accident. There are still a few humans left in this market to blow it by writing shoddy algorithms.

And here’s another possible outcome in this process.

Your broker will call you to notify you of an option called away, and then give you the wrong advice on what to do about it.

This generates tons of commissions for the broker but is a terrible thing for the trader to do from a risk point of view, such as generating a loss by the time everything is closed and netted out.

There may not even be an evil motive behind the bad advice. Brokers are not investing a lot in training staff these days. In fact, I think I’m the last one they really did train.

Avarice could have been an explanation here but I think stupidity and poor training and low wages are much more likely.

Brokers have so many ways to steal money legally that they don’t need to resort to the illegal kind.

This exercise process is now fully automated at most brokers but it never hurts to follow up with a phone call if you get an exercise notice. Mistakes do happen.

Some may also send you a link to a video of what to do about all this.

If any of you are the slightest bit worried or confused by all of this, come out of your position RIGHT NOW at a small profit! You should never be worried or confused about any position tying up YOUR money.

Professionals do these things all day long and exercises become second nature, just another cost of doing business.

If you do this long enough, eventually you get hit. I bet you don’t.