Global Market Comments

February 26, 2021

Fiat Lux

Featured Trade:

(REVISITING THE GREAT DEPRESSION)

(EXPLORING MY NEW YORK ROOTS)

Global Market Comments

February 26, 2021

Fiat Lux

Featured Trade:

(REVISITING THE GREAT DEPRESSION)

(EXPLORING MY NEW YORK ROOTS)

Global Market Comments

February 25, 2021

Fiat Lux

Featured Trade:

(TAKING A LOOK AT THE ROM)

(ROM)

(BRING BACK THE UPTICK RULE!)

Global Market Comments

February 24, 2021

Fiat Lux

Featured Trade:

(LONG TERM ECONOMIC EFFECTS OF THE CORONA VIRUS),

(ZM), (LOGM), (AMZN), (PYPL), (SQ), CNK), (AMC), (IMAX), (CCL), (RCL), (NCLH), (CVS), (RAD), (WMT)

The world will never be the same again.

Not only is the old world rapidly disappearing before our eyes, the new one is breaking down the front door with alarming speed. In short: the future is happening fast, very fast.

To a large extent, long-term economic trends already in place have been given a turbocharger. Quite simply, you just take out the people. Human contact of any kind will be minimized. I’ll tick off some of the more obvious changes.

All San Francisco Bay Area counties are still living under a “shelter in place” order. All schools have now been closed for a year. In March 2020 the local high school managed to get the first weekend of their annual musical “Titanic” done, but not the second.

All travel is banned except to gain essential necessities. Most bars and restaurants have been closed indefinitely, except for takeout. Some cities are issuing $1,000 fines for failure to wear a mask. The kids have turned into white, pasty zombies after staring at laptops for 12 months.

To say that we are merely fatigued from a yearlong quarantine would be a vast understatement. Climbing the walls is more like it.

As I write this, US Covid-19 deaths have topped a half million and cases have surpassed 28 million. China peaked at 4,000 deaths with four times our population. The difference was leadership issue. China welded the doors of Covid carriers shut. Here said it was a big nothing and would “magically” go away.

The magic didn’t work.

In the meantime, you better get used to your new life. You know that home office of yours you’ve been living in? It is now a permanent affair, as your employer figured out that they can make more money and earn a high stock multiple with you at home.

Besides, they didn’t like you anyway.

Many employees are never coming back, preferring to avoid horrendous commutes, lower costs, and yes, future pandemic viruses. GoToMeeting (LOGM) and Zoom (ZM) are now a permanent aspect of your life.

Commerce will change beyond all recognition. Did you do a lot of shopping on Amazon (AMZN) like I do? Now, you’re really going to pour it on.

Amazon hired a staggering 500,000 new distribution and delivery people in 2020 to handle the surge in business, the most by any organization since WWII. I can’t believe the stock is only at $3,200. It is worth double that, especially if they break up the company.

The epidemic really hammered the mall, where a fatal disease is only a sneeze away. Mall REITs are only just starting to crawl off the floor and may never again reach their old highs, no matter how much they promise to pay you in yield.

And how are you going to pay for that transaction? Guess what one of the most efficient transmitters of disease is? That would be US dollar bills. Something like 50% of all US paper money already tests positive for drugs, according to one Fed study.

Take paper money in change and you are not only getting contact from the salesclerk, but the last dozen people who handled the money. You are crazy now to take change and then not go swimming in Purell afterwards. Personally, I leave it all as a tip.

Contactless payments deal with this nicely (PYPL), (SQ), two of the top-performing stocks since April. People pay by swiping their iPhone wallet, or are simply scanned when they walk in the store, as with some Whole Foods shops owned by Amazon.

Conferences? A thing of the past. All of my public speaking events around the world have been cancelled. Webinars now rule. They offer lower conversion rates but include vastly cheaper costs as well. I can reach more viewers for $1,000 on Zoom than the Money Show could ever attract to the Las Vegas Mandalay Bay for $1 million.

At least I won’t have 18 hours of jet lag to deal with anymore. I’m sure Qantas will miss those first-class ticket purchases and I’ll miss the Champaign.

Entertainment is also morphing beyond all recognition. Streaming is now the order of the day. Disney+ (DIS) was probably the best-timed launch in business history, earning enough to cancel out most of the losses from the closure of the theme parks. Again, this has been a long time coming and the other major movie producers will soon follow suit.

Movie theaters, which have been closed for a year, may also never see their peak business again (CNK), (AMC), (IMAX). The theaters that survive will do so by only accumulating so much debt that they won’t be attractive investments for a decade.

The same is true for cruise lines (CCL), (RCL), (NCLH). But that won’t forestall dead cat bounces that are worth a double in the meantime, as they are coming off of such low levels. No vaccination, no cruise.

Exercise is changing overnight. All gyms and health clubs are now closed, so working out will become a solo exercise far away on a high mountain. I have already been doing this for 30 years, so a piece of cake here.

Friends with yoga classes are now doing them in the living room, streaming their instructors online. The economics of online yoga classes are so compelling, with hundreds attending online classes, that the old model may never come back.

If you are having trouble getting your kids to comply with social distancing requirements, have a family movie night and watch Gwyneth Paltrow and Cate Winslet die in Contagion. It has been applauded by scientists as the most accurate presentation of the kind of out-of-control pandemic which we may now be facing.

It is bone-chilling.

As for me, I have my stockpile of food and will be self-quarantining for the foreseeable future. I am at the top of five lists to get vaccinations, but so far all I have received is a ton of special offers from CVS (CVS), Rite Aid (RAD), and Walmart (WMT)

Stay healthy.

Global Market Comments

February 23, 2021

Fiat Lux

Featured Trade:

(THE UNITED STATES OF DEBT),

(TLT), (TBT), ($TNX)

Global Market Comments

February 22, 2021

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TIME FOR A BREAK)

(GME), (TLT), (FB), (AMZN), (AAPL), (XME), (FCX), (MS), (GS), (BLX), (KO), (AMD)

I know you’re not going to want to hear this. I might as well be trying to pull your teeth, lead you down a garden path, or sell you a high-priced annuity.

But there is nothing to do in the market right now. Nada, diddly squat, bupkis, and for all you Limey’s out there, bugger all.

For during the first six weeks of 2021, we have pretty much squeezed all there is out of the market.

Not only did we nail the timing and the direction, we also got the lead sectors, financials, brokers, chips, and short bonds (MS), (GS), (BLK), (AMD). We also chased the Volatility Index (VIX) down from $38 to a lowly $20, baying and protesting all the way.

That enabled us to extract a 28.29% profit so far in 2021, the best return in the 13-year history of the Mad Hedge Fund Trader. The only other time you see numbers this high is when Ponzi schemes get busted. And not a dollar of this was earned from the really marginal plays like Bitcoin, SPAC’s, GameStop (GME), or pot stocks.

If I feel like I did a year’s worth of work during the first seven weeks of 2021, it’s because I have, issuing 60 trade alerts since January 1.

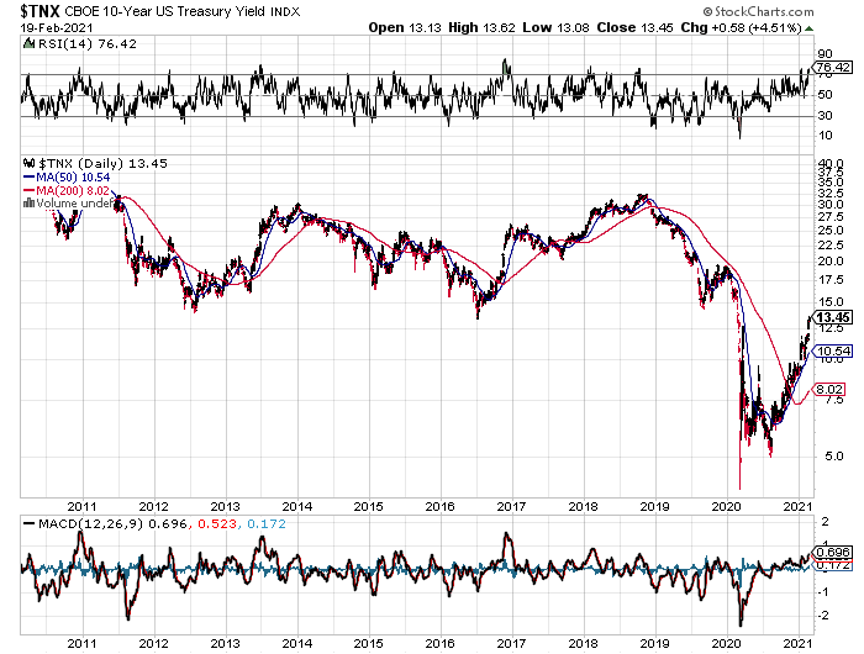

However, bonds (TLT) are reaching the end of their current leg down. The 1.34% yield we saw on Friday is suspiciously close to the 1.36% yields we saw during the 2012 and 2017 market double bottom.

So, there may be some wood to chop around these, levels, possibly for weeks or months.

This is important because a collapsing bond market has been the principal driver of the winning trades of 2021, such as in banks, brokers, money managers, and other domestic recovery plays.

And when one side of the barbell goes dead, what do you do? You buy the other side. FANGs are just completing a six-month “time” correction where they have gone absolutely nowhere. So, Facebook (FB), Amazon (AMZN), and Apple (AAPL) may be getting ready for a roll.

One other sector that might keep running is the SPDR Mining & Metals ETF (XME), and Freeport McMoRan (FCX). That’s because it's not just us buying metals to front-run a recovery, it’s the entire world. What do you think a $2 trillion infrastructure budget will do to this area?

New lows for bonds, as the ten-year US Treasury yield hits 1.26%, up 38 basis points since January 1 and a one-year high. 1.50% here we come! Ever hear the expression “Don’t fight the Fed”? All financials are off to the races, where we were 60% long. Biden’s $1.9 trillion rescue package will be 100% borrowed and take total US borrowing to a back-breaking 55% of GDP. I hate to sound like a broken record but keep selling rallies in the (TLT), buy (JPM), (BAC), (GS), (MS), and (BRK/B) on dips.

Volatility index hit a one-year Low, which is what you’d expect at the dawn of a decade-long bull market in stocks. The (VIX) may flat line here for a while before the next out-of-the-blue spike.

The Nikkei Stock Average topped 30,000, for the first time in 31 years, Yes, it’s been a long haul. I was heavily short in the initial 1990 meltdown from 39,000 to 20,000 and many fortunes were made. The top marked the end of the Japanese company’s ability to copy their way into leadership. After that, rapidly advancing technology made copying too slow to compete in a global economy.

A midwest storm upended energy markets, with oil popping $8 to $67 and gas deliveries spiking from $4 to $999. It would have gone higher, but the software only provided for three digits. Electricity prices are all over the map. Some 4 million Texas customers are without power. Fracking has ground to a halt. Windfarms are frozen solid. If you are a net producer (as I am), you are in heaven. The turmoil is expected to be gone by the weekend. It’s another high price paid for ignoring global warming.

Weekly Jobless Claims soared, to 861,000, casting a dark cloud over the economic recovery. The news took a 300-point bite out of the Dow. Illinois and California saw the biggest gains. We are not out of the woods yet.

SpaceX was valued at $74 Billion, according to an $850 billion venture capital fundraising round this week. However, Elon Musk’s rocket company won’t go public until men are landed on Mars. The company is also the launching pad for its Starlink global WIFI project, which will cost at least $10 billion to build out. Blowing up rockets is not a good backdrop for an IPO.

Cash is still pouring off the sidelines, with equity mutual funds attracting some $7.8 billion last week. As long as this is the case, which could be for years, any market corrections will be limited. Strangely, bond funds are still pulling in money too, some $5.7 billion. It’s called a liquidity-driven market, silly!

When we come out the other side of pandemic, we will be perfectly poised to launch into my new American Golden Age, or the next Roaring Twenties. With interest rates still at zero, oil cheap, there will be no reason not to. The Dow Average will rise by 400% to 120,000 or more in the coming decade. The American coming out the other side of the pandemic will be far more efficient and profitable than the old. Dow 120,000 here we come!

My Mad Hedge Global Trading Dispatch earned an amazing 17.27% so far in February after a blockbuster 10.21% in January. The Dow Average is up a trifling 2.92% so far in 2021.

This is my fourth double-digit month in a row. My 2021 year-to-date performance soared to 27.28%. After the February 19 option expiration, I am now 80% in cash, with a single long in Tesla (TSLA) left.

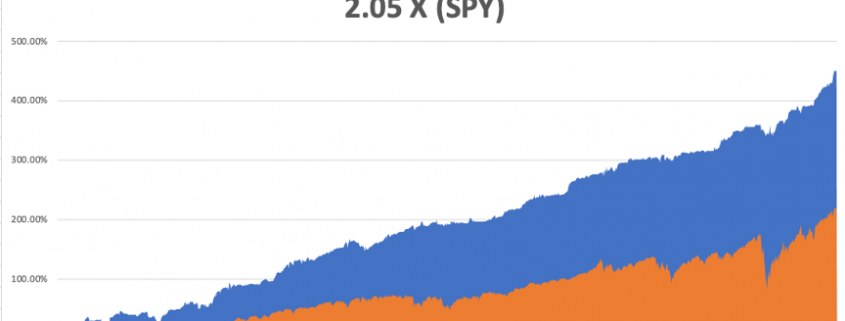

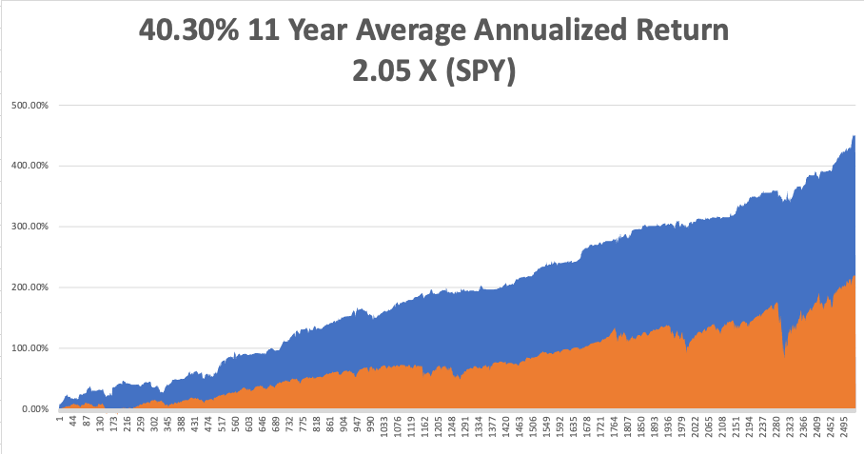

That brings my 11-year total return to 450.03%, some 2.05 times the S&P 500 (SPX) over the same period. My 11-year average annualized return now stands at an Everest-like new high of 40.30%.

My trailing one-year return exploded to 94.09%, the highest in the 13-year history of the Mad Hedge Fund Trader. We have earned 109.00% since the March 20, 2020 low.

We need to keep an eye on the number of US Coronavirus cases at 28 million and deaths approaching 500,000, which you can find here. We are now running at a heart breaking 3,000 deaths a day. But that is down 35% from the recent high.

The coming week will be a boring one on the data front.

On Monday, February 22, at 8:30 AM EST, the Chicago Fed National Activity Index is out. Zoon (ZM) reports.

On Tuesday, February 23 at 9:00 AM, the S&P Case-Shiller National Home Price Index for December is announced. Square (SQ) and Intuit (INTU) report.

On Wednesday, February 24 at 8:30 AM, New Home Sales for January are printed. NVIDIA (NVDA) reports.

On Thursday, February 25 at 9:30 AM, Weekly Jobless Claims are printed. US Durable Goods for January and Q4 GDP are out. Salesforce (CRM), (Moderna (MRNA), and Airbnb (ABNB) report.

On Friday, February 26 at 8:30 AM, US Personal Income and Spending are published. DraftKings (DKNG) reports. At 2:00 PM, we learn the Baker-Hughes Rig Count.

As for me, if you want to see what it is like to work at Amazon, watch the movie Nomadland. It’s an artsy Francis McDormand film made with a $4 million budget about the end of life, which I caught over the weekend on Hulu.

It covers a contemporary trend in US society where retirees with no savings move into RVs and live off the grid, working occasionally to earn gas money. They raved about it in Europe.

If I don’t keep those trade alerts coming, that could be me in a couple of years.

Stay healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 19, 2021

Fiat Lux

Featured Trade:

(FEBRUARY 17 BIWEEKLY STRATEGY WEBINAR Q&A),

(USO), (XLE), (AMZN), (SPY), (RIOT), (T), (ZM), (ROKU), (TSLA), (NVDA) (TMQ) (TLRY), (ACB), (KO), (XLF), (AAPL) (REMX), (GLD), (SLV), (CPER)

Below please find subscribers’ Q&A for the February 17 Mad Hedge Fund Trader Global Strategy Webinar broadcast from frozen Incline Village, NV.

Q: Are we buying gold on dips?

A: Not yet. As long as you have a ballistic move in bitcoin going on, you don't want to touch gold. Eventually gold does get dragged up by the global bull market in commodities, but silver is more preferable since it moves up at twice the rate of gold in bull markets.

Q: Is it time to buy Amazon (AMZN) LEAPS?

A: Yes, I am looking for a move to $5,000 a share in Amazon with the onset of enormous GDP figures. Exploding consumer spending may be what breaks Amazon out of its current six-month range. I would do something like a two-year LEAP with the $3,600-$3,700 in Amazon. Be cautious and stay near the money. You should get like a 400% or 500% return on that LEAP at expiration, or sooner.

Q: What's your view on Tesla (TSLA)?

A: It looks tired—lower lows, lower highs. We’re in a short-term downtrend that could last several months. I’m holding off on buying Tesla until we find a bottom. I just have one $150 out-of-the-money call spread that expires in 20 days, and that’s it. We paired our position way back on Tesla. Wait for the market to come to you, if you can get Tesla under $700, that's a great time to buy LEAPS on Tesla.

Q: Are you still bearish on energy (XLE)?

A: Short term no, long term yes. You’re trying to catch a rally in a long-term bear market. Some people can do that, some people can’t. It’s the next buggy whip industry, the next American Leather, which completely vaporized.

Q: What about the calls for $100 oil (USO)?

A: Yes, after the markets went up $10 dollars in a day you always see calls for $100 oil. If the energy crisis in Texas shows us anything, it’s that we have to move away from oil as an energy source much faster than we thought because its distribution and production system freeze.

Q: Are you expecting a short-term correction (SPY)?

A: Yes but no more than 4%; there is still too much cash on the sidelines.

Q: Have airline leisure stocks run too far?

A: No, they are coming off of much lower lows so they can go to much higher highs. Almost all restrictions should be gone in six months—I’m trying to time my Australia trips and I think in six months may get to the point where, if you show proof of vaccination and submit to a 3 day test, they will let you into the country. But in six months you won’t be able to get an airline or hotel reservation.

Q: What about the AT&T (T) yield play and 5G play?

A: Yes, I still like AT&T and you should probably buy it about here. All these legacy telecom companies are going to have big moves once 5G accelerates allowing a vast expansion of streaming and other high-end services.

Q: Is CRISPR (CRSP) a good LEAP candidate?

A: Yes, and you can do something like the $200-$210 two years out because it’ll almost certainly get taken over before then.

Q: What’s a good LEAP for Tesla?

A: Wait for it to drop to $700 first and then buy something like the $900-$1000 two years out.

Q: What do you think of Apple?

A: Apple (AAPL) is taking a rest waiting for the 5G rollout to reaccelerate. Our target for Apple this year is $200.

Q: Do we sell in May and go away?

A: I would just go away and keep all your longs. The trouble is, trying to be ultra-smart and time all this stuff in a runaway bull market, you find it a lot harder to get in when you come back; you go “oh my gosh these things are up so much,” you don’t buy anything, and then it doubles. I’ve seen that a lot in the past, New York in 1971, Tokyo in 1987, Dotcom stocks in 1985, add US stocks in 2015.

Q: What do you think of Riot (RIOT) stock?

A: Wouldn't touch it with a ten-foot pole. If I didn’t want to buy bitcoin at $1, I'm not going to want to buy it at $51,000. Go elsewhere for your bitcoin advice, except you’ll hear the same thing: it will go up because it’s gone up. You should use it as a risk indicator. That’s essentially what all bitcoin analysts will tell you because there's nothing to analyze. There are no earnings, there's not even any physical presence anywhere to analyze, no customer support. If you can get seven 10 baggers like we did last year, with Zoom (ZM), Roku (ROKU), Tesla (TSLA), and Nvidia (NVDA) —why bother with cryptocurrencies?

Q: What are your thoughts on travel?

A: My take is that leisure travel is returning in mass but that the business travelers will shy away; and that will be true for this year but probably not next year. I think business travel will come back once it’s 100% safe and once all the companies are making money again and can afford travel.

Q: Is Trilogy Metals Inc. (TMQ) a good buy? It has Copper, Zinc, and some exposure to Gold and Silver.

A: Yes, it is a buy. Most commodity prices should double from these levels; and probably the smartest ones to buy are the ones that haven't moved yet—gold and silver, but silver especially. The world will come roaring back and it needs every possible metal it can get its hands on.

Q: What do you think of the cannabis stocks (TLRY), (ACB)?

A: That is one of several small bubbles in the markets that I don't want to touch at all. How hard is it to grow a weed? Barriers to entry are zero. Massive competition from the black market, as about 30% of the cannabis demand is still going to your local drug dealer who doesn’t have to pay taxes, whereas you get double taxed with a pot company—35% retail sales taxes and then taxes on the profits on top of that. So no thank you, Mary Jane.

Q: Do you think Warren Buffet is still the leading thought contributor to personal finance, or is he outdated?

A: Berkshire Hathaway is up 10% this year, and the Dow is up only 2.8%, so I would say he’s still pretty well in touch with the markets; and he has very heavy weightings in Coca Cola (KO), Financials (XLF), and Apple (AAPL), as well as some energy stocks. Good discipline and good strategy never go out of style.

Q: Is the Texas energy disaster going to set the US’ way on renewable energy faster?

A: Yes, it does force people to consider the move into alternative energy sources much faster, especially when the old energy sources go to zero and then have whole states lose their power sources. Look how the governor of Texas is blaming frozen windmills, which only account for 7% of the Texas energy supply. What a joke! I’ll lend him my hairdryer and they’ll work. Notice the propensity to immediately blame others for their own mistakes. That is terrible leadership. Texas is going to turn blue.

Q: Is climate change overhyped in the US stock market?

A: Absolutely yes, that’s why I haven’t been buying any of these. They tend to be smaller companies, and ever since Biden got the lead in the primaries and the polls last spring this whole sector, and ESG investing in general, has been on an absolute tear and is wildly expensive. I call these feel-good stocks; people buy them because they make them feel good but very few of these actually make real money. I prefer to stick to the real money plays of which there are more than enough around.

Q: Do you like rare earth such as the Van Eck Vectors Rare Earth/Strategic Metals ETF (REMX)?

A: I do like rare earths. You need them for practically anything electronic. China's been withholding supplies again, which they like to do from time to time just to rattle our cage because we need them for all our weapons systems. But this is also prone to bubbles, so be careful when you buy it that you’re not paying up too much. By the way, the (REMX) ETF was brought out at the absolute peak of the last rare earth bubble, which we covered extensively 11 years ago. We got people in at the very bottom of rare earth, and things went up ten times. Then we got everybody out and people said I was being bearish too soon, so I never got invited to conferences again. After that, it went down for eight straight years.

Q: Don’t you think frozen windmills and solar speak for more reliance on oil than less? Biden administration limits on oil will drive up prices.

A: You’re right on the second part; creating shortage of supply will cause price increases. But frozen windmills are a result of lack of capital investment and planning. It turns out all of the windmills in the northern part of the US have electric heaters, so they don’t freeze because it gets colder up there. They didn’t do that in Texas to save money, and now they have lost about 7% of the total Texas energy supply. So bad management was the issue there. Penny-wise and pound-foolish.

Q: Are commodities in general in play? What is the best ETF for commodities?

A: The trouble with commodities is there is no one big catch all commodity ETF. However, you can expect one soon; as things peak or have big runs, they tend to generate new ETFs like new children because the demand is there. In the commodities world, there are lots of individual 1x and 2x ETFs like the gold ETF (GLD), the silver (SLV), the copper (CPER), and so on. But there isn’t one good basket I’ve found. You can always create your own by buying small amounts of each of the leading companies, which is probably the best thing to do.

Q: What is the best property value right now?

A: That would be Mississippi; they have the lowest housing prices in the United States. Unfortunately, low cost of living, low tax states also have the worst education systems, which doesn’t matter of course if you don't have kids. In the end, you get what you pay for. It’s OK if you don’t mind dealing with stupid people every day, which I do. I can always tell when I’m dealing with customer support in the deep south because literacy falls off a cliff.

Q: Should we get a 10% correction soon?

A: Probably not; the last 10% correction needed a presidential election to scare the daylights out of you, and there's nothing like that on the horizon now. Maybe we’ll get another 5% correction on a game stop type incident, but there's just too many people trying to get into the stock market now. People who were selling last March/April are the same people who are buying now.

Q: Is there a bright future for hydrogen?

A: No, electricity is infinitely scalable, and hydrogen isn’t. It’s about as scalable as gasoline because you have to move it around in big tankers, keep it at 434.5 degrees Fahrenheit below zero, which is very expensive and has an unfortunate tendency to blow up. So, I never bought into the hydrogen thesis, except for local use of fleets where everyone gets all their hydrogen from a central facility.

Q: What will be the best performing sector in the next 1-3 months?

A: Your bond short and your financials. It’s the same trade. And it’s the one sector that no one asked about today.

Q: Do you think bitcoin is a bubble poised to pop at some point?

A: Yes, but who knows where that is; bubble tops are impossible to predict, especially when there are no valuation metrics. Bottoms can be measured with valuation metrics, but tops can’t because greed is an immeasurable quantity. However, it will certainly pop when they suddenly decide to increase the total outstanding number of bitcoins, which may seem unlikely now but is inevitable.

Good Luck and Stay Healthy.

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

Global Market Comments

February 18, 2021

Fiat Lux

Featured Trade:

(A NOTE ON ASSIGNED OPTIONS OR OPTIONS CALLED AWAY),

(BAC)