Featured Trade: (A NOTE ON THE FRIDAY OPTIONS EXPIRATION), (FXY), (GILD), (SPY), (VIX), (TLT), (IWM), (QQQ), (SCTY), (USO), (GLD), ?(AN EVENING WITH TEXAS GOVERNOR RICK PERRY), ?(LNG), (UNG), (TSLA)

CurrencyShares Japanese Yen ETF (FXY) Gilead Sciences Inc. (GILD) SPDR S&P 500 ETF (SPY) VOLATILITY S&P 500 (^VIX) iShares 20+ Year Treasury Bond (TLT) iShares Russell 2000 (IWM) PowerShares QQQ Trust, Series 1 (QQQ) SolarCity Corporation (SCTY) United States Oil ETF (USO) SPDR Gold Shares (GLD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-20 01:05:312015-02-20 01:05:31February 20, 2015

We have several options positions that expire on Friday, and I just want to explain to the newbies how to best maximize their profits.

These include:

The Currency Shares Japanese Yen Trust (FXY) February $84-$87 vertical bear put spread

The Gilead Sciences (GILD) February $87.50-$92.50 vertical bull call spread

The S&P 500 (SPY) February $199-$202 vertical bull call spread

My bets that (GILD) and the (SPY) would rise, and that the (FXY) would fall during January and February proved dead on accurate. We got a further kicker with the two stock positions in that we captured a dramatic plunge in volatility (VIX).

Provided that some 9/11 type event doesn?t occur today, all three positions should expire at their maximum profit point. In that case, your profits on these positions will amount to 13% for the (FXY), 19% for (GILD) and 20% for the (SPY).

This will bring us a fabulous 5.58% profit so far for February, and a market beating 6.11% for year-to-date 2015.

Many of you have already emailed me asking what to do with these winning positions. The answer is very simple. You take your left hand, grab your right wrist, pull it behind your neck and pat yourself on the back for a job well done. You don?t have to do anything.

Your broker (are they still called that?) will automatically use your long put position to cover the short put position, cancelling out the total holding. Ditto for the call spreads. The profit will be credited to your account on Monday morning, and he margin freed up.

If you don?t see the cash show up in you account on Monday, get on the blower immediately. Although the expiration process is now supposed to be fully automated, occasionally mistakes do occur. Better to sort out any confusion before losses ensue.

I don?t usually run positions into expiration like this, preferring to take profits two weeks ahead of time, as the risk reward is no longer that favorable.

But we have a ton of cash right now, and I don?t see any other great entry points for the moment. Better to keep the cash working and duck the double commissions. This time being a pig paid off handsomely.

If you want to wimp out and close the position before the expiration, it may be expensive to do so. Keep in mind that the liquidity in the options market disappears, and the spreads substantially widen, when a security has only hours, or minutes until expiration. This is known in the trade as the ?expiration risk.?

One way or the other, I?m sure you?ll do OK, as long as I am looking over your shoulder, as I will be.

This expiration will leave me with a very rare 100% cash position. I am going to hang back and wait for good entry points before jumping back in. It?s all about getting that ?buy low, sell high? thing going again.

There are already interesting trades setting up in bonds (TLT), the (SPY), the Russell 2000 (IWM), NASDAQ (QQQ), solar stocks (SCTY), oil (USO), and gold (GLD).

The currencies seem to have gone dead for the time being, so I?ll stay away.

Well done, and on to the next trade.

Pat Yourself on the Back

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Pat-on-the-back-e1424375419249.jpg259400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-20 01:04:322015-02-20 01:04:32A Note on the Friday Options Expiration

For the last few months, I have leapt off my biweekly global strategy webinars to check the weekly crude inventories announced minutes before. This week?s figures absolutely blew me away.

The American Petroleum Institute reported that crude stocks rose a staggering 14.3 million barrels over the past week. This is the biggest weekly build that I can remember after covering the industry for 45 years.

This comes on the heels of a breathtaking build of 6.1 million barrels the previous week.

Will someone please text me when the numbers come out during my next webinar? I hate being in the dark, even when it is just for 20 minutes.

Needless to say, crude prices (USO) fell like a stone, giving up 5.5% in hours. Prices are still plunging as I write this. It confirms my suspicion, voiced assiduously in the earlier webinar, that Texas tea has another run to the downside in store.

The 500,000 barrels a day of new production coming on line over the next four months make this a virtual certainty.

The implications for your investment portfolio are legion.

It means that a new leg down in the oil collapse is now unfolding. We may be in the process of taking another shot at the $43 low in January. Best case, this sets up the double bottom where you should buy the entire energy and commodity sectors. Worse case, we break to a new low in the $30?s.

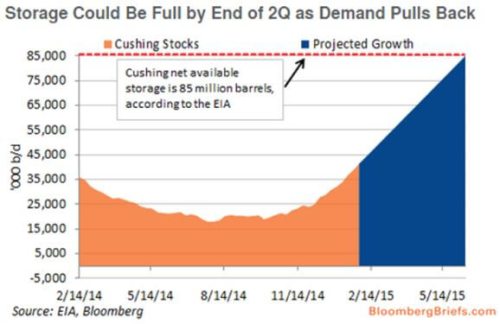

Industry experts are keeping a laser like focus on the storage facilities at Cushing, Oklahoma. They are rapidly filling up, and will be full at 85 million barrels by June. Today?s numbers bring that day dramatically forward.

Once topped up, the industry could be facing a price Armageddon, and newly produced crude will have nowhere to go.

That will bring widespread capping of producing wells, which are never able to recover production when restored. This will be a terrible outcome for the producing companies and oil lease investors.

Consumers aren?t the only ones who are celebrating.

Oil traders are enjoying their best year since 2009, cashing in on the sky high volatility. Front month volatility is gyrating around the 55% levels. This compares to only 15.45% for the S&P 500.

Traders, eat your hearts out.

Big players like Glencore, Gunvor and Mercuria are cashing in with lower prices vastly offset by much greater turnover. Specialized energy hedge funds are also doing well.

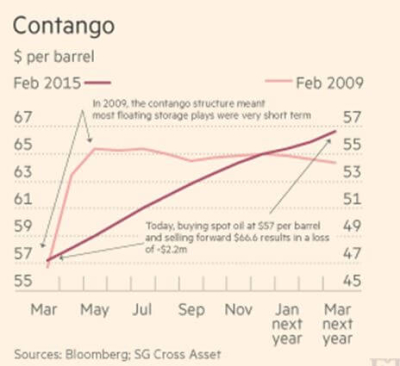

The contango, whereby futures contracts for far month delivery are trading at huge premiums to front month ones, is also generating enormous trading opportunities.

The last time I checked, oil one-year out was trading at a 25% premium. This means you can buy a few hundred thousand barrels, charter a rusted out old tanker, and store it for future sale.

Ultra low interest rates to finance the position provide an additional kicker. Hedge funds with the right credit lines are pouring into the field.

OK, so you?re not set up to borrow billions, charter ships, and swing around huge amounts of crude. Nor am I, for that matter. However, the next best thing is also setting up.

When oil completes its next swan dive, there will be great opportunities in the options market.

One year dated calls on oil majors like Exxon (XOM), Conoco Phillips (COP) and Occidental Petroleum (OXY) and the oil ETF (USO) should rise tenfold in the next recovery if you are able to buy anywhere close to the bottom.

I?ll send out a Trade Alert when I see it.

I Think I See a Spot Over There

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Oil-Storage-e1424354835281.jpg249400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-19 09:20:352015-02-19 09:20:35The Best is yet to Come in Crude

?I want staffers who are so loyal that they will kiss my ass in Macy?s front window and tell everyone it smells like roses,? said the late president, Lyndon Baines Johnson, the model for the character, Francis Underwood, in the hit cable TV series House of Cards.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Kevin-Spacey-e1424355019892.jpg200300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-19 09:12:442015-02-19 09:12:44February 19, 2015 - Quote of the Day

Long-term readers of this letter have prospered mightily from my addiction to biotech stocks in recent years, one of the most reliably top performing sectors in the stock market.

But have we visited the well one time too many times? Is biotech turning into a bubble that will eventually deliver the same grievous outcome of other past bubbles?

Not yet.

Still, one has to ask the question. No less a figure than Federal Reserve governor Janet Yellen has indicated that she thought valuations in the biotech sector were getting ?substantially stretched.? The Fed doesn?t single out stocks for commentary very often.

Biotech certainly has been a money-spinner for followers of my top performing Trade Alert service, which delivered a 30.5% profit in 2014.

Readers made three round trips in hepatitis C drug developer Gilead Sciences (GILD) in the past four months, adding 5.77% to the value of their portfolios. I believe the company?s blockbuster drug will become the most profitable in history. So do a lot of others.

Longer-term investors bought the Biotech iShares ETF (IBB) on my advice, which gained an impressive 45% last year, and is still rising.

However, biotech has long been a hedge fund favorite.

That means many shareholders are only dating these stocks and are not married to them. The hot money regularly flows in and out, giving the sector more than double the volatility of the main market. A 10% correction in any other stock is worth at least 25% in biotech.

This also makes biotech stocks great to buy on a dip. My last foray into (GILD) occurred after cautious guidance took the shares down a heart stopping 10% in a single day.

This is a great example of how unusually sensitive biotech stocks are to headline risk. I?ve ridden stocks to tremendous heights, watching them pour billions into a single treatment, only to see them crash and burn on failed stage three trials.

That is just the nature of their business. It?s all about all or nothing bets.

It?s just a matter of time before one of the major companies gets stuck with a hickey like this, flushing billions down the drain. That could herald a generalized sector selloff that could last months, or even years.

Biotech is a high-risk sector that should only be held within a well diversified portfolio. You may notice that in the Mad Hedge Fund Trader?s model trading portfolio I never have more than 10% in biotech at any given time. I figure I could handle a total blow up and lose the whole 10% and still stay in business.

When I speak at conferences, strategy luncheons and on TV, I tell listeners of my lazy man?s guide to long-term investment. Only follow three sectors, technology, biotech and energy, and ignore the other 97. You?ll save yourself a lot of time reading pointless research.

Biotech currently accounts for a mere 1% of US GDP. It is on its way to 20%, about where technology is today. That means that a disproportionately large share of earnings growth will spring from biotech over the coming decades.

One way to protect yourself is to stick with the big caps, which are undervalued relative to the sector, and are expected to haul in 20% earnings growth this year.

Many smaller companies prices are assuming a total certainty of the success of their drugs. The reality is that this only happens about half the time.

If you do go with small caps, I would take a venture capital approach. Buy a dozen with the expectation that many will go under, a couple do OK, and one goes through the roof. Never put all your eggs in one basket.

It also helps that you have someone with a scientific background making your picks, like me. Because drug companies promise such amazing results, like curing cancer, the sector has always been prone to hype and over promotion. I never met I biotech CEO who didn?t believe his company was about to deliver the next panacea, taking his shares up tenfold.

One plus for biotech is that it has unusually strong patent protection, which usually extends out 20 years for new products. There are not a lot of Chinese companies that can imitate their drugs.

That means earnings can be predicted far into the future, and are largely immune from the economic cycle. If you?re sick, you want to get cured regardless of whether the GDP is growing or shrinking, or whether interest rates are low or high.

Make sure that your investments have plenty of new developments in the pipeline. Expiring patents on past winners with no replacements can spell certain death for a stock price.

Publicly listed drug companies are now venturing into research fields that were only science fiction when I was in the lab 45 years go. ?Gene editing? whereby genes can be repaired, edited and then turned on and off at will, is now becoming a burgeoning new science.

It promises to cure the whole range of human maladies, including heart disease, cancer, obesity and a whole range of degenerative diseases (including some of mine).

Expect to hear a lot more about TALENs (transcription activator-like effector nucleases) and CRISPR (clustered regular interspaced short palindromic repeats). You heard it here first.

What is truly fascinating is that hybrid computer science/biochemical scientists are now taking algorithms developed y the National Security Agency hackers and using them to decode human DNA. (I hope I?m not speaking too much out of school here.)

Gene editing is the natural outcome of the discovery of recombinant DNA technology developed during the 1970?s by Paul Berg, Herbert Boyer, and Stanley Cohen, all early heroes of mine.

Since none were the equity participants of private companies, the initial rewards for the breakthrough were minimal. I remember that one received a new surfboard for his efforts.

Berg went on to found Genentech (GENE) in 1977 and got rich. If I hadn?t gone into the stock market, that is almost certainly where I would have ended up.

How things have changed.

The short answer here is that biotech does have further to run. A lot further.

The rate of innovation of biotechnology is accelerating so fast that it will continue to spew out fantastic investment opportunities for the rest of your lives. So expect to receive many more Trade Alerts in this area in the years to come.

But it is definitely an ?E? ticket ride. So fasten your seatbelt on your path to riches.

As for me, I?m thrilled that I got to live so long to see this stuff happen. At times, it was a close run race.

This One Looks Like a Winner

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Scientist-Bio-Lab-e1424187891662.jpg265400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-17 10:52:212015-02-17 10:52:21How Far Will Biotech Run?

?We need to have more faith in the central bank?s ability to print money?, said Scott Minerd, of Guggenheim Partners.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/02/Foreign-Currency.jpg215289Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-17 10:49:232015-02-17 10:49:23February 17, 2015 - Quote of the Day

Featured Trade: (FEBRUARY 18 GLOBAL STRATEGY WEBINAR), (WHY ARE BOND YIELDS SO LOW?) (TLT), (TBT), (LQD), (MUB), (LINE), (ELD), (QQQ), (UUP), (EEM), (DBA) (BRING BACK THE UPTICK RULE!)

iShares 20+ Year Treasury Bond (TLT) ProShares UltraShort 20+ Year Treasury (TBT) iShares iBoxx $ Invst Grade Crp Bond (LQD) iShares National AMT-Free Muni Bond (MUB) Linn Energy, LLC (LINE) WisdomTree Emerging Markets Lcl Dbt ETF (ELD) PowerShares QQQ Trust, Series 1 (QQQ) PowerShares DB US Dollar Bullish ETF (UUP) iShares MSCI Emerging Markets (EEM) PowerShares DB Agriculture ETF (DBA)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-02-16 01:06:232015-02-16 01:06:23February 16, 2015

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.