Featured Trade: (LUCKY FIND SPARKS NEW CALIFORNIA GOLD RUSH), (GLD), (THE DIFFERENCE BETWEEN MAD HEDGE FUND TRADER AND MAD DAY FUND TRADER), (THE NEW CALIFORNIA GOLD RUSH)

?SPDR Gold Shares (GLD)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-20 10:02:072014-11-20 10:02:07November 20, 2014

On my way back from Lake Tahoe last weekend I saw that every bend of the American river was dotted with hopeful miners, looking to make a windfall fortune.

Weekend hobbyists were there panning away from the banks, while the hardcore pros stood in hip waders balancing portable pumps on truck inner tubes, pouring sand into sluice boxes. Welcome to the new California gold rush.

A sharp-eyed veteran can take in $2,000 worth of gold dust a day. The new 2013'ers were driven by a price of gold at $1,180 and the attendant headlines, but also by unemployment, and heavy rains that flushed new quantities of the yellow metal out of the Sierras.

They were no doubt inspired by the chance discovery of an 8.7 ounce nugget in May near Bakersfield, worth an impressive $10,266.

Local folklore says that The Sierra's have given up only 20% of their gold, and the remaining 80% is still up there awaiting discovery. Out of work construction workers are taking their heavy equipment up to the mountains and using it to reopen mines that have been abandoned since the 19th century.

The US Bureau of Land Management says that mining permits in the Golden State this year have shot up from 15,606 to 23,974. Unfortunately, the big money here is being made by the sellers of supplies and services to the new miners, much as Levi Strauss and Wells Fargo did in the original 1849 gold rush.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Panning-for-Gold.jpg165504Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-20 09:37:122014-11-20 09:37:12The New California Gold Rush

Featured Trade: (WHY WATER WILL SOON BE WORTH MORE THAN OIL), (CGW), (PHO), (FIW), (VE), (TTEK), (PNR), (TESTIMONIAL) (REPORT FROM NEW ZEALAND), (ENZL)

Guggenheim S&P Global Water ETF (CGW) PowerShares Water Resources ETF (PHO) First Trust ISE Water ETF (FIW) Veolia Environnement S.A. (VE) Tetra Tech Inc. (TTEK) Pentair plc (PNR) iShares MSCI New Zealand Capped (ENZL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-19 09:42:592014-11-19 09:42:59November 19, 2014

35 degrees South latitude, 174 degrees East longitude.

I am writing this report from the Duke of Marlborough Hotel and Pub in remote Russell, off the east coast of New Zealand?s North Island. Once known as ?The Hell Hole of the Pacific? in 1835, no less an authority than Charles Darwin, claimed this 19th century whaling port was populated with ?the refuse of humanity.?

It has since been cleaned up, gentrified, and turned into a gentrifying tourist Mecca. It is much like Lahaina on Maui, Hawaii was in the early seventies, before the blighting high rise hotels and condos went up.

The Residents of Russell were Most Welcoming

Others Had Different Opinions

The bar was packed to the gunwales with drunken and riotous rugby fans screaming their lungs out in support of their team in the Super Rugby League game. When South Africa won, I bought a round of drinks for the house, but first had to arm-wrestle a deeply tanned and craggy faced Welshman for the right to do so. I hope my credit card doesn?t get cancelled when the bill comes through for NZ$1,046.29. ?Thomas? is a Welsh name, isn?t it?

The trip started auspiciously at SFO when I found myself checking in behind a group of heavily tattooed, bulked up, but amiable Maoris. A few days later, I found myself at a Maori tribal dinner, where I feasted on a meal of feral pig and sweet potatoes cooked deep in the earth, and was instructed on the finer points of the Haka dance.

Let me tell you that there is a reason why there is not a national chain of Maori fast food restaurants offering their primitive cuisine on every street corner. No offense intended to my hosts, but you would only want to eat it if you were starving to death.

One of My Many High Level Contacts

The rental company was out of cars, thanks to the games, but managed to come up with a battered old Toyota Camry with bald tires, breaks well past their prime, and leaking fluids from every orifice. In other words, it was a lot like me. I was OK with the left hand drive, having lived for 20 years in Japan and England.

But the stick shift certainly made things interesting. I can?t tell you how many times I turned on the windshield wipers instead of the right turn signal, as the controls are reversed. I headed north from Auckland hoping to find better weather, picking up hitchhikers along the way to absorb the local lore.

My dad was here 70 years ago with the Marine Corps, training for the invasion of Guadalcanal, and always remarked how friendly approachable the women were. I found them friendly, yes, but not so approachable. Maybe this is because dad was a combat ready 19 year old, and I am a combat ready, but aging 62 year old fart.

The countryside was incredibly lush and green, mountainous, and covered with massive cycad ferns and kauri trees ensnarled by choking vines. Cleared grazing lands were dotted with sheep. The Maori are ever present, accounting for a substantial part of the rural population. Every town name seems to start with the letter ?W?, as in Whangaparaoa, Whangarei, and Waipu.

The Largest Tree in New Zealand

One of the most interesting conversations that I have had this year was with an aged Maori historian and Shaman at the Waitangi Treaty Grounds. When I told her I was part Cherokee, Sioux, and Delaware Indian, she opened right up and let loose for two hours.

It turns out that tribal groups around the world are cooperating and coordinating legal attacks on establishment land ownership around the world. Everyone from the Maoris to Hawaiians, Navajo?s, Australian, Aborigines, and Finnish Laps are involved, and are getting legal aid from the United Nations to fund this.

Perhaps a Distant Kiwi Cousin?

The Maoris have been especially successful, scoring a $170 million payoff from their own government. The money went into community centers and education in the most Maori dominated parts of the country.

It isn?t often that I get to discuss global economics with a Neolithic tribal representative, and I relished the opportunity. I am always looking for the new view, and I?m sure there is much we can learn from 8,000 BC.

When I checked into the Pahia Beach Hotel and Spa, I did what I always do when I visit the Southern hemisphere. I flush the toilet, watching with satisfaction as the water disappears in a counterclockwise fashion, thanks to the Coriolis force (check your physics textbook). In the Northern hemisphere is goes down clockwise. If you don?t believe me, go try it. That night I found the Southern Cross, the only one of 88 constellations not visible at home.

We all thought New Zealand was toast when Great Britain cut the economic umbilical cord by joining the European Community in 1973, leaving the land of the kiwis out in the cold. A radical series of reforms saved the country in 1984. The financial system was deregulated and exchange rates were freed. Agricultural subsidies were cut, forcing farmers to become more efficient and globally price competitive.

Through a series of fortunate historical accidents, it then entered the sweet spot of the global economy. It was too small to have its own car industry, so it had nothing to lose when Japan took over that business. The same occurred with manufacturing, which China swallowed whole in the past decade.

Today, services and tourism account for 70% of GDP. With a per capita GDP of $27,130, New Zealand ranks 33rd in the world, behind the US at $46.810 (7th), but well ahead of China at $7,544 (94th).

Kiwis Will Sell You Anything

Today, the World Bank ranks New Zealand as the most business friendly country on the planet. It has the lowest taxes in the developed world, and an unemployment rate at an enviable 6.6%. People are happy and the cities bustle. Recently, the economy has been booming because of the baby formula tainting scandal in China. New Zealand supplies one third of the world?s milk powder, and Chinese mothers who can afford it are now feeding only imported foreign brands to their kids.

This makes all of the country?s assets long term buys, including both the New Zealand dollar and the iShares MSCI New Zealand Investable Index Fund ETF (ENZL). The Chinese certainly think so, who have emerged as far and away the largest buyers of the country?s real estate. Use the big dips to take positions.

And Never Throw Anything Out

Well, I have to go now, or I?ll miss the last ferry back to Pahia on the mainland. Besides, that waitress across the room is starting to wink at me.

To watch a video of my giving thanks for your support from New Zealand?s Mount Maunganui, a long dead volcano, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/02/John-Thomas-New-Zeland-Maori.jpg474356Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-19 09:33:172014-11-19 09:33:17Report from New Zealand

Traders in Japan suffered a rude awakening yesterday morning when the Ministry of International Trade and Industry announced that the troubled country?s GDP shrunk by -1.6% during the third quarter. Analysts had been expecting a gain of 2.2%.

What?s worse, this is the second consecutive quarter of negative GDP, meaning that the Land of the Rising Sun is now solidly in recession, the fourth since 2008, and the umpteenth since the country fell off a demographic cliff 25 years ago.

The Nikkei Average took it on the kisser, plunging some 3% from its high for the year. The Wisdom Tree Japan Hedged Equity ETF (DXJ) declined by half as much.

Half of the gain since the Bank of Japan?s ?shock and awe? monetization measures on October 15 went up in smoke. Now we know why the central bank had been so aggressive and preemptive.

There are immediate implications from the dismal numbers. Prime Minister Shinzo Abe is almost certain to delay a hike in Japan?s VAT sales tax from 8% to 10% scheduled for the new fiscal year starting April 1.

This year?s rise, from 5% to 8%, is viewed as the chief culprit responsible for the shocking slowdown.

It turns out that clever consumers rushed to beat the tax, pulled their spending forward, creating an artificial boost to economic growth in the first quarter. This lulled the government and Japanese retailers, into thinking their recovery strategy was working.

After the tax increase took effect, the spending boom ground to a complete halt, and the economy came to a juddering stop. The end result was a huge inventory build that was the most destructive aspect of the terrible GDP numbers, as higher prices caused consumers to stay away from the stores in droves.

The conservative Abe was behind the government?s grab for more revenues to head off the country?s runaway budget deficit, which is now seen by many economists as reaching catastrophic proportions, some 160% of total GDP.

The problem is that governments should balance budgets when they can, not when they want to. I have lost count of how many Japanese recoveries have been smothered in the cradle by premature tax increases over the last two decades.

Thank goodness the US government had the sense not to try that here, or we?d all be standing in breadlines by now.

The global implications of a new Japanese recession are, fortunately, not as dire. It?s not like many analysts had built in a Japanese economic miracle into their long-term growth forecasts. Japan only accounts for 7% of world GDP these days, and losing a couple percent of that annualized doesn?t move the needle much.

The fall of the Japanese yen this year has been so rapid and dramatic that there hasn?t nearly been enough time for it to have a positive impact on the economy. It will going forward. That alone should pull the country back out of recession in the current quarter.

Remember too that since Japan is far more dependent than America on imported energy, it will benefit greater from the ongoing collapse in the price of oil.

The disastrous GDP numbers should also encourage the BOJ to become even more aggressive in its own reflationary efforts. Think more growth of the money supply, more quantitative easing, and faster. Buy Japanese printing press stocks!

Fortunately, all of these global, multi market cross currents distill down into a single trade for you and I: sell more yen.

A substantially weaker Japanese currency seems to be the one stop solution for all of Japan?s many intractable problems.

You already saw this in action in the foreign currency markets on Monday after the GDP numbers came out. Normally, a downside surprise of this magnitude on the economic data front generates a big ?flight to safety? move across all asset classes. That would have caused the Japanese yen to rise sharply against the buck.

Not this time. In fact, it barely moved. Japan and yen bears weren?t waiting a nanosecond to sell short more of the beleaguered currency, offsetting whatever profit taking there was from pre existing shorts the GDP figures might have incited.

So the set up here is to sell short the Currency Shares Japanese Yen Trust ETF (FXE), or to buy the 2X ProShares Ultra Short Yen ETF (YCS), two positions I have been recommending non stop for the past three years.

It looks like we have only just gotten started with out big down move in the yen.

Back in Recession Again

https://www.madhedgefundtrader.com/wp-content/uploads/2013/11/Woman-Hari-Kari.jpg280396Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-18 09:38:312014-11-18 09:38:31Japan?s Rude Awakening

By now, the reasons behind this year?s bear market are pretty well known. Even my cleaning lady, Cecelia, can site them chapter and verse.

Quantitative easing went global. Inflation fell, with the prices of almost all business input costs, like commodities, energy, interest rates, collapsing. Labor costs remained muted, so corporate profits rocketed.

Voila! Stocks rose, probably by 17% in the S&P 500 by the end of 2014, and 19% with dividends. Not bad for the fifth year of a bull market.

So is this it? Should we now be taking profits in a topping market and running for the hills to avoid a rollover in 2015?

Is it game over?

Let us think again. We need a new set of reasons to keep this bull alive. The good news is that if we delve down to our inner most thoughts, those reasons are out there. What we are really looking for is a bull market 2.0.

It goes something like this. The rally in bonds almost certainly ended on October 15. It is now ?Sell the rallies? for the next 20 years. The mere fact that they are no longer going up will scare away momentum based investors and ignite some institutional selling in the New Year asset reallocations.

Given the gargantuan size of the global bond market, some $100 trillion, this development is potentially more important for stock prices than five years of QE from the Federal Reserve.

That Herculean effort created $4.5 trillion in new cash. Moving 10% out of bonds into stocks and other risk assets would generate double that amount of firepower, or some $10 trillion.

Mind you, bond prices aren?t going to collapse. They will engage in long, tedious range trading, with an eventual slow grind down. Continued disinflation assures that. Bond traders will die from boredom, and not a heart attack. This is a key element of the bull case for stocks.

In other words, you ain?t seen nothing yet, baby!

It gets better.

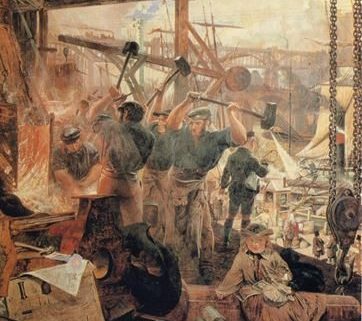

After the first industrial revolution started during the 1820?s, when we saw the transition to modern manufacturing processes that started with textiles, we witnessed a century of rising profits, falling inflation, and booming stock markets, subject to the occasional 50% correction (there was no Fed then).

Sound familiar?

The really interesting thing now is that we are seeing at least five, if not more, new industrial revolutions get underway, which are collapsing business costs at a prodigious rate.

Count the transition from silicon to DNA based computing, biotechnology, health care, alternative energy sources, and transportation. These are all century long trends which are only just getting started.

This is happening against a backdrop of perennially low interest rates and energy costs. Companies can?t help but make more money, and by implication, share prices can?t help but go higher. Think of Goldilocks on steroids.

This leads to self-sustaining economic growth that keeps the major indexes appreciating for years. The Fed understands this, which is why their gentle exit from quantitative easing in recent months had absolutely no effect on asset prices. If anything, it accelerated their upturn.

So how much juice can we count on for next year? Add 10% to company profits, maintain a 2% dividend rate, and that gets us up 12%. Use 2,100 as a launching pad, and that gets us up to 2,350 by the end of 2015.

When did investors realize that an industrial revolution started in the 1820?s? Oh, sometime in the 1850?s. Similarly, investors today may not understand how rosy the current investment environment is for another couple of decades. Then they?ll be kicking themselves for not loading the boat with shares now.

Just thought you?d like to know.

Think it?s Time to Buy Stocks?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/11/Industrial-Revolution.jpg359362Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-17 01:04:112014-11-17 01:04:11Bull Market 2.0

Featured Trade: (NOVEMBER 19 GLOBAL STRATEGY WEBINAR), (THE 120/120 BATTLE), (FXY), (YCS), (FXE), (EUO), (UUP), (GET READY FOR YOUR NEXT BIG TAX HIT)

CurrencyShares Japanese Yen ETF (FXY) ProShares UltraShort Yen (YCS) CurrencyShares Euro ETF (FXE) ProShares UltraShort Euro (EUO) PowerShares DB US Dollar Bullish ETF (UUP)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-14 01:06:372014-11-14 01:06:37November 14, 2014

Foreign exchange traders are an odd lot. They tend to maintain a laser like focus on specific numbers that are utterly meaningless to us mere mortals, but which have momentous importance to themselves.

Right now, one is hearing the battle cry over the 120/120 targets. Specifically, traders want to take the yen down to Y120 to the US dollar, and the Euro down to $1.20 by the last trading day of 2014.

They may well get their wishes.

Powering the moves is the biggest policy divergence between central banks in a decade. The US Federal is threatening to take interest rates up every other day.

In the meantime, lower interest rates beckon in Europe and Japan as their economies lurch from one disaster to the next, dragging their own currencies down.

Accelerating the move is the gasoline that has been thrown on the economic fires caused by? You guessed it, plunging gasoline prices in the US, which is quickly turning into a massive stimulus program.

Wonder why Wal-Mart (WMT) has suddenly taken off to the races? It?s because their impoverished, gap toothed customers have suddenly received big cash bonuses, thanks to the war for market share among the members of OPEC.

Even a penny drop in the price of petrol adds $1 billion a year in consumer spending. Gas is so cheap that we might even break the $3 level here in high tax California.

Higher interest rates are great for the greenback because they prompt foreign investors to send more money here faster to chase higher returns than available at home.

The sharpest bond market move in history, taking ten year Treasury yields from 1.86% all the way up to 2.38% in four weeks, makes this view even more convincing.

Followers of this letter already know that the currencies have been in deep doo doo all year. That?s why I have been aggressively pushing out Trade Alerts to buy the dollar (UUP) and sell short the Euro (FXE), (EUO) and the Japanese yen (FXY), (YCS) for the past six months.

Readers have been laughing all the way to the bank.

The really thrilling part here is that this is only the beginning of a decade long move. My final target for the yen is Y150 and $1.00 for the Euro. This could be the trade that keeps on giving.

There are also important spillover implications for the stock market. It means more money for stocks at higher prices. The S&P 500 at 2,100 by yearend now looks like a chip shot, and we may probe even higher.

So why am I currently lacking any current positions in the currencies in my model trading portfolio? We are now at the end of extreme moves in all asset classes over the past month.

So, while everything looks hunky dory (a street in Yokohama where the cheap geishas used to hang out) in the markets, risk is, in fact, rising.

I have to admit that, being up 42.5% year to date, I have gotten spoiled. I am holding back for the low risk, high return type of entry points for new trades that my readers have become addicted to.

When I see one, you?ll be the first to know. Watch this space.

Gosh, I love this job.

See the Connection?

The Best Stimulus Program Ever

Wal-Mart Customer

https://www.madhedgefundtrader.com/wp-content/uploads/2014/11/Wacky-Guy.jpg288387Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2014-11-14 01:04:342014-11-14 01:04:34The 120/120 Battle

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.