SOCIALISM -You have 2 cows. You give one to your neighbor.

COMMUNISM -You have 2 cows. The State takes both and gives you some milk.

FASCISM -You have 2 cows. The State takes both and sells you some milk.

NAZISM -You have 2 cows. The State takes both and shoots you.

BUREAUCRATISM -You have 2 cows. The State takes both, shoots one, milks the other, and then throws the milk away.

TRADITIONAL CAPITALISM -You have two cows. You sell one and buy a bull. Your herd multiplies, and the economy grows. You sell them and retire on the income.

ROYAL BANK OF SCOTLAND (VENTURE) CAPITALISM -You have two cows. You sell three of them to your publicly listed company, using letters of credit opened by your brother-in-law at the bank, then execute a debt/equity swap with an associated general offer so that you get all four cows back, with a tax exemption for five cows. The milk rights of the six cows are transferred via an intermediary to a Cayman Island Company secretly owned by the majority shareholder who sells the rights to all seven cows back to your listed company. The annual report says the company owns eight cows, with an option on one more. You sell one cow to buy a new president of the United States, leaving you with nine cows. No balance sheet provided with the release. The public then buys your bull.

SURREALISM -You have two giraffes. The government requires you to take harmonica lessons.

AN AMERICAN CORPORATION -You have two cows. You sell one, and force the other to produce the milk of four cows. Later, you hire a consultant to analyze why the cow has dropped dead.

A FRENCH CORPORATION -You have two cows. You go on strike, organize a riot, and block the roads, because you want three cows.

A JAPANESE CORPORATION -You have two cows. You redesign them so they are one-tenth the size of an ordinary cow and produce twenty times the milk. You then create a clever cow cartoon image called a Cowkimona and market it worldwide.

AN ITALIAN CORPORATION -You have two cows, but you don?t know where they are. You decide to have lunch.

A SWISS CORPORATION -You have 5000 cows. None of them belong to you. You charge the owners for storing them.

A CHINESE CORPORATION -You have two cows. You have 300 people milking them. You claim that you have full employment, and high bovine productivity. You arrest the newsman who reported the real situation.

AN INDIAN CORPORATION -You have two cows. You worship them.

A BRITISH CORPORATION -You have two cows. Both are mad.

AN IRAQI CORPORATION -Everyone thinks you have lots of cows. You tell them that you have none. No-one believes you, so they bomb the ** out of you and invade your?country. You still have no cows, but at least you are now a Democracy.

AN AUSTRALIAN CORPORATION -You have two cows. Business seems pretty good. You close the office and go for a few beers to celebrate.

A NEW ZEALAND CORPORATION -You have two cows. The one on the left looks very attractive. The one on the right is very nervous.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/02/HappyCow.jpg394400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-09-04 01:04:552013-09-04 01:04:55A Cow Based Economics Lesson

Will the person who bought Tesla shares (TSLA) on my recommendation last year at $30 please email me? I was traveling in Europe over the summer and lost your email address. I would like to get a testimonial from you. The stock hit $173.70 today, and is up 580% from your cost, making it the top performing US stock this year.

With the money you?ve made you can probably buy a Tesla now. I recommend the high performance Model S-1 with the upgraded sound system and the 270-mile range. I have one, and they are to die for. It?s the only car I ever bought where the specifications keep improving every month with each automatic software update. Or you can wait until next year and by the four-wheel drive SUV Model X. I am on the waiting list for that one.

You owe me.

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/JT-with-Tesla-e1427723768460.jpg227400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-09-04 01:03:492013-09-04 01:03:49On That Tesla Recommendation

Long-term readers of this letter are well aware of my antipathy towards General Motors (GM). For decades, the company turned a deaf ear to customer complaints about shoddy, uncompetitive products, arcane management practices, entitled dealers, and a totally inward looking view of the world that was rapidly globalizing. It was like watching a close friend kill himself through chronic alcoholism.

During this time, Japan?s share of the US car market rose from 1% to 42%. The only surprise when the inevitable bankruptcy came was that it took so long. This was traumatic for me personally, since for the first 30 years of my life General Motors was the largest company in the world. Their elegant headquarters building in Detroit was widely viewed as the high temple of capitalism. I was raised to believe that what was good for GM was good for the country. Oops!

I opposed the bailout because it interfered with creative destruction, something America does better than anyone else, and gives us a huge competitive advantage in the international marketplace. Probably 10% of the listed companies in Japan are zombies that should have been killed off 20 years ago. Without GM a large part of the US car industry would have moved to California and gone hybrid or electric.

When an opportunity arose to spend a few hours with the new CEO, Dan Akerson, I gratefully accepted. After all, he wasn?t responsible for past sins, and I thought I might gain some insights into the new GM. Besides, he was a native of the Golden State and a graduate in nuclear engineering from the Naval Academy at Annapolis and the London School of Economics. How bad could he be?

When I shook hands, I remarked that his lapel pin looked like the hood ornament on my dad?s old car, a Buick Oldsmobile. He noticeably winced. So to give the guy a break, I asked him about the company?s outlook.

Last year was the best in the 104-year history of the company. It is now the world?s largest car company, with the biggest market share. The 40-mpg Chevy Cruze is the number one selling sub compact in the US. GM competed in no less than 117 countries, and was a leader in the fastest growing emerging market, China.

I asked how a private equity guy from the Carlyle Group was fitting in on the GM board. He responded that all of the Big Three Detroit automakers were being run by ?non-car guys? now, and they generated profits for the first time in 20 years. However, it was not without its culture clashes. When he publicly admitted that he believed in global warming, he was severely chastised by other board members. He wasn?t following the official playbook.

When I started carping about the bailout, he cut me right off at the knees. Liquidation would have been a deathblow for the Midwestern economy, killing 1 million jobs, and saddling the government with $23 billion in pension fund obligations. It also would have deprived the Treasury Department of $135 billion in annual tax revenues. It was inevitable that in the last election year the company became a political punching bag. Akerson said that he was still a Republican, but just.

GM?s Chevy Volt is so efficient, running off a 16kWh lithium ion battery charge for the first 25-50 miles, that many are still driving around with the original tank of gas they were delivered with a year ago. Extreme crash testing by the government and the bad press that followed forced a relaunch of the brand. Despite this, I often get emails from readers saying they love the car.

The summer production halt says more about GM?s more efficient inventory management than it does about the hybrid car. GM?s recent investment in California based Envia Systems should succeed in increasing battery energy densities threefold.

However the Volt is just a bridge technology to the Holy Grail, hydrogen fuel cell powered cars, which will start to go mainstream in four years. These cars burn hydrogen, emit water, and cost about $300,000 a unit to produce now. By 2017, GM hopes to make it available as a $30,000 option for the Chevy Aveo.

Another bridge technology will be natural gas powered conventional piston engines. These take advantage of the new glut of this simple molecule and its 80% price discount per BTU compared to gasoline. The company announced a dual gas tank pickup truck that can use either gasoline or compressed gas. Cheap compressors that enable home gas refueling are also on the horizon. Fleet sales will be the initial target.

Massive overcapacity in Europe will continue to be a huge headache for the global industry. There are just too many carmakers there, with Germany, England, Italy, France, and Sweden each carrying multiple manufacturers. Governments would rather bail them out to save jobs and protect entrenched unions than allow market forces to work their magic. GM lost $700 million on its European operations last year, and Akerson doesn?t see that improving now that the continent is clearly moving into recession.

I asked if GM stock was cheap, given the dismal performance since the IPO. It is still just above the $33/share launch price. Now that the government has unloaded its shareholding the way for further appreciation should be clear. Also, the old bondholders still owned substantial numbers of shares and were selling into every rally. That is hardly a ringing endorsement.

Akerson said that a cultural change had been crucial in the revival of the new GM. Last year, the Feds announced an increase in mileage standards from 25 to 55 mpg by 2025. Instead of lawyering up for a prolonged fight to dilute or eliminate the new rules, as it might have done in the past, it is working with the appropriate agencies to meet these targets.

Finally, I asked Akerson what went through his head when the top job at GM was offered him at the height of the crisis. Were they crazy, insane, delusional, or all the above? He confessed that it offered him the management challenge of a generation and that he had to rise to it.

Spoken like a true Annapolis man.

Shifting GM from This?.

To This?.

And This

https://www.madhedgefundtrader.com/wp-content/uploads/2012/03/GM-CEO-Dan-Akerson-1.jpg307399Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-09-03 01:04:542013-09-03 01:04:54An Evening With ?Government Motors?

I don?t just think he hates me. He truly despises me. In fact, he does everything he can to put me out of business.

Take the taper, for example. If I am right and he doesn?t end quantitative easing, then my model-trading portfolio goes through the roof. If he does, it will crater. Many other independent analysts agree with me, including several Fed governors. But is he giving me any hints? Not any chance. I might as well flip a coin.

He could have let me off easy by announcing some minor back door easing, like ceasing interest rate payments on deposits from private banks, or even a token taper of $10 billion or so.

It?s not that I am not an all right guy. I am kind to children and small animals. I donate generously to many charities. I just sent my mother a card for her birthday, even though she is 85 and not expected to last much longer. I even occasionally escort little old ladies across the street, although this is a holdover from my days as an Eagle Scout.

It?s just that Ben Bernanke and I don?t see eye-to-eye on a lot of important issues. He wants stocks to go up. As a hedge fund manager who plays from the short side more often than not when the economy is growing at a paltry 2% rate, I want them to go down.

He wants bonds to go up too, as he clearly elicited with his recent announcement. I, on the other hand, want bonds to sell off because I know that when the bill comes due for all of this monetary easing, the crash will be momentous.

These are not the only matters we differ on. He wants to create jobs. He can wish this until the cows come home, but he?s not going to get them because of the gale force demographic headwinds the country is now facing and the massive deleveraging by the public and private sector. The 6 million jobs we exported to China are never coming back.

However, all he has to do is make a mere mention of his desires, or even just mention the letter ?Q?, and asset prices skyrocket, forcing me to stop out of my shorts at losses. This is why I was in such a foul, acrimonious, and detestable mood over the weekend, after stocks started to rally again for the umpteenth time.

My problem is that Ben Bernanke isn?t the only person who dislikes me. President Obama doesn?t think much of me either. And it?s not because I refuse to buy a cold chicken dinner at his St. Francis Hotel fundraisers for $35,000 or $70,000 if I bring a date. He talks about jobs too. He frequently speaks about the need to improve our education system, even though I know he is poised to slash the budget for the Department of Education as part of some deal with the Republicans. Ditto for Social Security and defense.

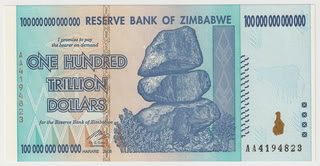

Fortunately for me, I wrote off any prospect of getting a retirement check a long time ago and have made other arrangements, like becoming a hedge fund manager. Either the payments will be too small for me to live on, subject to a means test that excludes fat cats like myself, or they will be made in worthless Zimbabwean dollars.

I got along with former Treasury Secretary, Timothy Geithner, OK, who keeps me on his ?must see? list whenever he stops in San Francisco. But we go way back. There are not a lot of people around who read my first book on the Japanese financial system when it was published 30 years ago. There are only four people in US history who can discuss Japanese monetary policy of the 1920?s in depth, and do it in Japanese just for laughs (it was clearly too easy, but they had to reflate after the 1923 Great Kanto Earthquake. Some things never change).

Two of them, Senator Mike Mansfield of Montana and Harvard professor, John K. Fairbank, died ages ago. So he is kind of limited in his choices. Besides, there are not a lot of people out there who can give him a 40-year view on the global economy, and I am one of them.

There are plenty of others who don?t think I am so hot. Try making a fortune in a market crash when everyone else is losing their shirt. While others in the locker room at my country club are slamming doors, tearing their hair out, and breaking golf clubs in half when they see the price feed on CNBC, I am chirping happily away about selling short at the top. I might as well be letting out a loud fart in Sunday church service. This explains why I stopped getting invitations to social dinners ages ago.

It?s not that my relationship with Ben Bernanke is totally hopeless. When the demographic picture turns from a headwind to a tailwind and individuals and corporations cease de-leveraging and return to re-leveraging, we?ll probably be reading from the same page of music. But according to the US Census Bureau, the earliest this can happen is 2023. By then, he probably won?t be the Fed governor anymore and I won?t care if he likes me or not.

There are other Fed governors who are not in the least bit interested in all this quantitative easing malarkey. They are much more similar in philosophy to Herbert Hoover?s Treasury Secretary, Andrew Mellon, who popularized the ?let the chips fall where they may? approach to economic policy. ?Liquidate, liquidate, liquidate?, he said. Kick the props out from under this market and all of a sudden Dow 3,000 is on the table, as argued by Global strategist and demographics maven, Harry Dent.

They might even go as far as unwinding the Fed?s hefty $3.5 trillion balance sheet. That would give the Chinese, who hold $1 trillion of these bonds, a heart attack. But who cares? It would create the mother of all trading windfalls for me. Hell, they might not even care if I torture small animals, beat children with a switch, and strand little old ladies in the middle of onrushing traffic. I think we would get along just great.

Screw Social Security, and Ben Bernanke too.

The Great Kanto Earthquake of 1923

https://www.madhedgefundtrader.com/wp-content/uploads/2012/06/zimbabwe-1.jpg166320Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-09-03 01:03:552013-09-03 01:03:55Why Ben Bernanke Hates Me

I believe that the global economy is setting up for a new golden age reminiscent of the one the United States enjoyed during the 1950?s, and which I still remember fondly. This is not some pie in the sky prediction. It simply assumes a continuation of existing trends in demographics, technology, politics, and economics. The implications for your investment portfolio will be huge.

What I call ?intergenerational arbitrage? will be the principal impetus. The main reason that we are now enduring two ?lost decades? is that 80 million baby boomers are retiring to be followed by only 65 million ?Gen Xer?s?. When the majority of the population is in retirement mode, it means that there are fewer buyers of real estate, home appliances, and ?RISK ON? assets like equities, and more buyers of assisted living facilities, health care, and ?RISK OFF? assets like bonds.

The net result of this is slower economic growth, higher budget deficits, a weak currency, and registered investment advisors who have distilled their practices down to only municipal bond sales.

Fast forward ten years when the reverse happens and the baby boomers are out of the economy, worried about whether their diapers get changed on time or if their favorite flavor of Ensure is in stock at the nursing home. That is when you have 65 million Gen Xer?s being chased by 85 million of the ?millennial? generation trying to buy their assets.

By then we will not have built new homes in appreciable numbers for 20 years and a severe scarcity of housing hits. Residential real estate prices will soar. Labor shortages will force wage hikes. The middle class standard of living will reverse a then 40-year decline. Annual GDP growth will return from the current subdued 2% rate to near the torrid 4% seen during the 1990?s.

The stock market rockets in this scenario. Share prices may rise very gradually for the rest of the teens as long as tepid 2% growth persists. A 5% annual gain takes the Dow to 20,000 by 2020. After that, we could see the same fourfold return we saw during the Clinton administration, taking the Dow to 80,000 by 2030. Emerging stock markets (EEM) with much higher growth rates do far better.

This is not just a demographic story. The next 20 years should bring a fundamental restructuring of our energy infrastructure as well. The 100-year supply of natural gas (UNG) we have recently discovered through the new ?fracking? technology will finally make it to end users, replacing coal (KOL) and oil (USO). Fracking applied to oilfields is also unlocking vast new supplies.

Since 1995, the US Geological Survey estimate of recoverable reserves has ballooned from 150 million barrels to 8 billion. OPEC?s share of global reserves is collapsing. This is all happening while automobile efficiencies are rapidly improving and the use of public transportation soars.? Mileage for the average US car has jumped from 23 to 24.7 miles per gallon in the last couple of years. Total gasoline consumption is now at a five year low.

Alternative energy technologies will also contribute in an important way in states like California, accounting for 30% of total electric power generation. I now have an all-electric garage, with a Nissan Leaf (NSANY) for local errands and a Tesla Model S-1 (TSLA) for longer trips, allowing me to disappear from the gasoline market completely. Millions will follow. The net result of all of this is lower energy prices for everyone.

It will also flip the US from a net importer to an exporter of energy, with hugely positive implications for America?s balance of payments. Eliminating our largest import and adding an important export is very dollar bullish for the long term. That sets up a multiyear short for the world?s big energy consuming currencies, especially the Japanese yen (FXY) and the Euro (FXE). A strong greenback further reinforces the bull case for stocks.

Accelerating technology will bring another continuing positive. Of course, it?s great to have new toys to play with on the weekends, send out Facebook photos to the family, and edit your own home videos. But at the enterprise level this is enabling speedy improvements in productivity that is filtering down to every business in the US, lower costs everywhere.

This is why corporate earnings have been outperforming the economy as a whole by a large margin. Profit margins are at an all time high. Living near booming Silicon Valley, I can tell you that there are thousands of new technologies and business models that you have never heard of under development. When the winners emerge they will have a big cross-leveraged effect on economy.

New health care breakthroughs will make serious disease a thing of the past, which are also being spearheaded in the San Francisco Bay area. This is because the Golden State thumbed its nose at the federal government ten years ago when the stem cell research ban was implemented. It raised $3 billion through a bond issue to fund its own research, even though it couldn?t afford it.

I tell my kids they will never be afflicted by my maladies. When they get cancer in 40 years they will just go down to Wal-Mart and buy a bottle of cancer pills for $5, and it will be gone by Friday. What is this worth to the global economy? Oh, about $2 trillion a year, or 4% of GDP. Who is overwhelmingly in the driver?s seat on these innovations? The USA.

There is a political element to the new Golden Age as well. Gridlock in Washington can?t last forever. Eventually, one side or another will prevail with a clear majority. Conservatives may grind their teeth, but if Hillary Clinton wins in 2016, the Democrats will control the White House until 2025. Right now, she is leading by a 60% margin with Republican women.

This will allow the government to push through needed long-term structural reforms, the solution of which everyone agrees on now, but nobody wants to be blamed for. That means raising the retirement age from 66 to 70 where it belongs, and means-testing recipients. Billionaires don?t need the $30,156 annual supplement. Nor do I.

The ending of our foreign wars and the elimination of extravagant unneeded weapons systems cuts defense spending from $800 billion a year to $400 billion, or back to the 2000, pre-9/11 level. Guess what happens when we cut defense spending? So does everyone else.

I can tell you from personal experience that staying friendly with someone is far cheaper than blowing them up. A Pax Americana would ensue. That means China will have to defend its own oil supply, instead of relying on us to do it for them. That?s why they have recently bought a second used aircraft carrier.

Medicare also needs to be reformed. How is it that the world?s most efficient economy has the least efficient health care system, with the worst outcomes? This is going to be a decade long workout and I can?t guess how it will end. Raise the growth rate and trim back the government?s participation in the credit markets, and you make the numerous miracles above more likely.

The national debt comes under control, and we don?t end up like Greece. The long awaited Treasury bond (TLT) crash never happens. Ben Bernanke has already told us as much by indicating that the Federal Reserve may never unwind its massive $3.5 trillion in bond holdings.

Sure, this is all very long-term, over the horizon stuff. You can expect the financial markets to start discounting a few years hence, even though the main drivers won?t kick in for another decade. But some individual industries and companies will start to discount this rosy scenario now. Perhaps this is what the nonstop rally in stocks since November has been trying to tell us.

Dow Average 1970-2012

Another American Golden Age is Coming

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/57-T-Bird.jpg237305Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-30 09:28:162013-08-30 09:28:16Get Ready for the Next Golden Age

Featured Trade: (BATTLE TESTING YOUR PORTFOLIO), (SPY), (USO), (FXE), (FXY), (YCS), (GLD), (SLV), (TLT), (THE COST OF CLEAN COAL), (KOL), (WHO IS BEN BERNANKE?)

SPDR S&P 500 (SPY)

United States Oil (USO)

CurrencyShares Euro Trust (FXE)

CurrencyShares Japanese Yen Trust (FXY)

ProShares UltraShort Yen (YCS)

SPDR Gold Shares (GLD)

iShares Silver Trust (SLV)

iShares Barclays 20+ Year Treas Bond (TLT)

Market Vectors Coal ETF (KOL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-29 09:13:302013-08-29 09:13:30August 29, 2013

I wanted to get the low down on clean coal (KOL) to see how clean it really is, so I visited some friends at Lawrence Livermore National Laboratory. The modern day descendent of the Atomic Energy Commission, where I had a student job in the seventies, the leading researcher on laser induced nuclear fission, and the administrator of our atomic weapons stockpile, I figured they?d know.

Dirty coal currently supplies us with 35% of our electricity, and total electricity demand is expected to go up 30% by 2030. The industry is spewing out 32 billion tons of carbon dioxide (CO2) a year and the great majority of independent scientists out there believe that the global warming it is causing will lead us to an environmental disaster within decades.

Carbon Capture and Storage technology (CCS) locks up these emissions deep underground forever. The problem is that there is only one of these plants in operation in North Dakota, a legacy of the Carter administration, and new ones would cost $4 billion each. The low estimate to replace the 250 existing coal plants in the US is $1 trillion, and this will produce electricity that costs 50% more than we now pay. In a gridlocked constrained congress, this is a big ticket that is highly unlikely to get picked up.

While we can build a wall to keep out illegal immigrants from Latin America, it won?t keep out CO2. This is a big problem as China is currently completing one new coal fired plant a week. In fact, the Middle Kingdom is rushing to perfect cheaper CCS technologies, not only for their own use, but also to sell to us. The bottom line is coal can be cleaned, but at a frightful price.

Coal?s Popularity is Fading Fast

00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-29 09:08:442013-08-29 09:08:44The Price Tag for Clean Coal

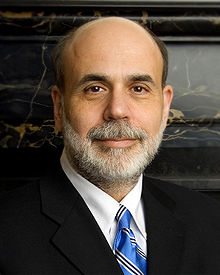

Since nothing less than the fate of the free world depends on the judgment of Ben Bernanke these days, I thought I?d touch base with David Wessel, the Wall Street Journal economics editor, who has just published In Fed We Trust: Ben Bernanke?s War on the Great Panic.

I doubted David could tell me anything more about the former Princeton professor I didn?t already know. I couldn?t have been more wrong, as David gave me some fascinating insights into the inner soul of our much-vaunted Chairman of the Federal Reserve.

Bernanke was the smartest kid in rural Dillon, South Carolina, who, through a series of improbable accidents, and intervention by a local black civil rights leader, ended up at Harvard. He built his career on studying the Great Depression, then the closest thing to paleontology economics had to offer, a field focused so distantly on the past that it was irrelevant. Bernanke took over the Fed when Greenspan was considered a rock star, inhaling his libertarian, free-market, Ayn Rand inspired philosophy in great giant gulps.

Within a year, the economy suddenly transported itself back to the Jurassic Age, and the landscape was overrun with T-Rex?s and Brontosaurs. He tried to stop the panic 150 different ways, 125 of which were terrible ideas, the remaining 25 saving us from the Great Depression II. This is why unemployment is now only 9.1%, instead of 25%.

The Fed governor is naturally a very shy and withdrawn person, and would have been quite happy limiting his political career to the Princeton, NJ school board. To rebuild confidence, he took his campaign to the masses, attending town hall meetings and pressing the flesh like a campaigning first term congressman.

The price tag for Ben?s success has been large, with the Fed balance sheet exploding from $800 million to $2.7 trillion, solely on his signature. The true cost of the financial crisis won?t be known for a decade or more. The biggest risk is that we grow complacent, having pulled back from the brink, and let desperately needed reforms of the financial system and the rebuilding of Fannie Mae and Freddie Mac slide. This is already starting to happen.

How Bernanke unwinds this bubble will define his legacy. Too soon, and we go back into a real depression. Too late, and hyperinflation hits. That?s when we find out who Ben Bernanke really is.

https://www.madhedgefundtrader.com/wp-content/uploads/2012/07/220px-Ben_Bernanke_official_portrait.jpg275220Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2013-08-29 09:06:082013-08-29 09:06:08Who is Ben Bernanke?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.