Five Tech Stocks to Sell Short on the Next Rally

Next year is poised to be a trading year that will bring tech investors an added dimension with the inclusion of Uber and Lyft to the public markets.

It seemed that everything that could have happened in 2018 happened.

Now, it’s time to bring you five companies that I believe could face a weak 2019.

Every rally should be met with a fresh wave of selling and one of these companies even has a good chance of not being around in 2020.

Western Digital (WDC)

I have been bearish on this company from the beginning of the Mad Hedge Technology Letter and this legacy firm is littered with numerous problems.

Western Digital’s structural story is broken at best.

They are in the business of selling hard disk drive products.

These products store data and have been around for a long time. Sure the technology has gotten better, but that does not mean the technology is more useful now.

The underlying issue with their business model is that companies are moving data and operations into cloud-based products like the Microsoft (MSFT) Azure and Amazon Web Services.

Why need a bulky hard drive to store stuff on when a cloud seamlessly connects with all devices and offers access to add-on tools that can boost efficiency and performance?

It’s a no-brainer for most companies and the efficiency effects are ratcheted up for large companies that can cohesively marry up all branches of the company onto one cloud system.

Even worse, (WDC) also manufactures the NAND chips that are placed in the hard drives.

NAND prices have faltered dropping 15% of late. NAND is like the ugly stepsister of DRAM whose large margins and higher demand insulate DRAM players who are dominated by Micron (MU), Samsung, and SK Hynix.

EPS is decelerating at a faster speed and quarterly sales revenue has plateaued.

Add this all up and you can understand why shares have halved this year and this was mainly a positive year for tech shares.

If there is a downtown next year in the broader market, watch out below as this company is first on the chopping block as well as its competitor Seagate Technology (STX).

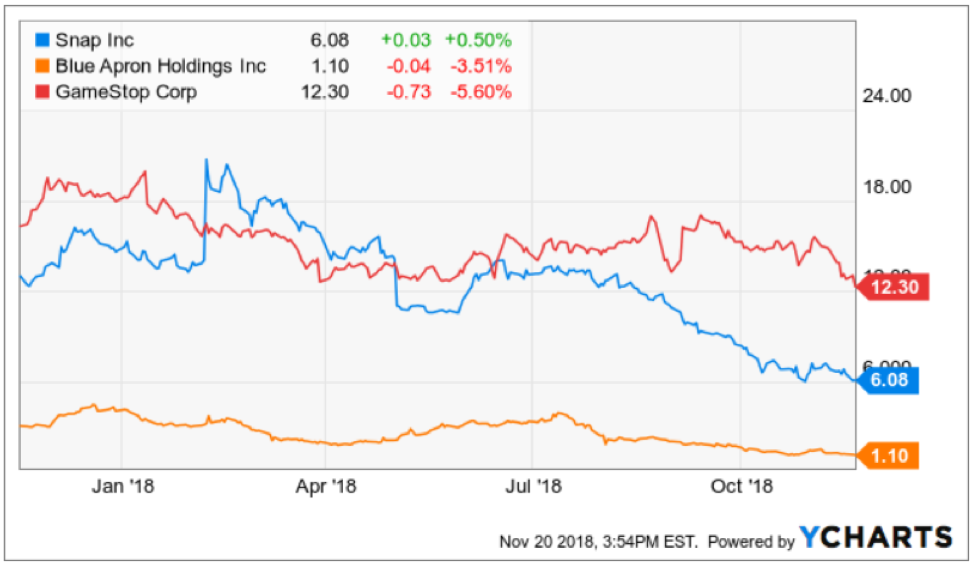

Snapchat (SNAP)

This company must be the tech king of terrible business models out there.

Snapchat is part of an industry the whole western world is attempting to burn down.

Social media has gone for cute and lovable to destroy at all cost. The murky data-collecting antics social media companies deploy have regulators eyeing these companies daily.

More successful and profitable firm Facebook (FB) completely misunderstood the seriousness of regulation by pigeonholing it as a public relation slip-up instead of a full-blown crisis threatening American democracy.

Snapchat is presiding over falling daily active user growth at such an early stage that usership doesn’t even pass 100 million DAUs.

Management also alienated the core user base of adolescent-aged users by botching the redesign that resulted in users bailing out of Snapchat.

Snapchat has been losing high-level executives in spades and fired a good chunk of their software development team tagging them as the scapegoat that messed up the redesign.

Even more imminent, Snapchat is burning cash and could face a cash crunch in the middle of next year.

They just announced a new spectacle product placing two frontal cameras on the glass frame. Smells like desperation and that is because this company needs a miracle to turn things around.

If they hit the lottery, Snap could have an uptick in its prospects.

GameStop (GME)

This part of technology is hot, benefiting from a generational shift to playing video games.

Video games are now seen as a full-blown cash cow industry attracting gaming leagues where professional players taking in annual salaries of over $1 million.

Gaming is not going away but the method of which gaming is consumed is changing.

Gamers no longer venture out to the typical suburban mall to visit the local video games store.

The mushrooming of broad-band accessibility has migrated all games to direct downloads from the game manufacturers or gaming consoles’ official site.

The middleman has effectively been cut out.

That middleman is GameStop who will need to reinvent itself from a video game broker to something that can accrue real value in the video game world.

The long-term story is still intact for gaming manufactures of Activision (ATVI), EA Sports (EA), and Take-Two Interactive (TTWO).

The trio produces the highest quality American video games and has a broad portfolio of games that your kids know about.

GameStop’s annual revenue has been stagnant for the past four years.

It seems GameStop can’t find a way to boost its $9 billion of annual revenue and have been stuck on this number since 2015.

If you do wish to compare GameStop to a competitor, then they are up against Best Buy (BBY) which is a better and more efficiently run company.

Then if you have a yearning to buy video games from Best Buy, then you should ask yourself, why not just buy it from Amazon with 2-day free shipping as a prime member.

The silver lining of this business is that they have a nice niche collectibles division that hopes to deliver over $1 billion in annual sales next year growing at a 25% YOY clip.

But investors need to remember that this is mainly a trade-in used video game company.

Ultimately, the future looks bleak for GameStop in an era where the middleman has a direct path to the graveyard, and they have failed to digitize in an industry where digitization is at the forefront.

Blue Apron

This might be the company that is in most trouble on the list.

Active customers have fallen off a cliff declining by 25% so far in 2018.

Its third quarter earnings were nothing short of dreadful with revenue cratering 28% YOY to $150.6 million, missing estimates by $7 million.

The core business is disappearing like a Houdini act.

Revenue has been decelerating and the shrinking customer base is making the scope of the problem worse for management.

At first, Blue Apron basked in the glory of a first mover advantage and business was operating briskly.

But the lack of barriers to entry really hit the company between the eyes when Amazon (AMZN), Walmart (WMT), and Kroger (KR) rolled out their own version of the innovative meal kit.

Blue Apron recently announced it would lay off 4% of its workforce and its collaboration with big-box retailer Costco (COST) has been shelved indefinitely before the holiday season.

CFO of Blue Apron Tim Bensley forecasts that customers will continue to drop like flies in 2019.

The company has chosen to focus on higher-spending customers, meaning their total addressable market has been slashed and 2019 is shaping up to be a huge loss-making year for the company.

The change, in fact, has flustered investors and is a great explanation of why this stock is trading at $1.

The silver lining is that this stock can hardly trade any lower, but they have a mountain to climb along with strategic imperatives that must be immediately addressed as they descend into an existential crisis.

Intel (INTC)

This company is the best of the five so I am saving it for last.

Intel has fallen behind unable to keep up with upstart Advanced Micro Devices (AMD) led by stellar CEO Dr. Lisa Su.

Advanced Micro Devices is planning to launch a 7-nanometer CPU in the summer while Intel plans to roll out its next-generation 10-nanometer CPUs in early 2020.

The gulf is widening between the two with Advanced Micro Devices with the better technology.

As the new year inches closer, Intel will have a tough time beating last year's comps, and investors will need to reset expectations.

This year has really been a story of missteps for the chip titan.

Intel dealt with the specter security vulnerability that gave hackers access to private data but later fixed it.

Executive management problems haven’t helped at all.

Former CEO of Intel Brian Krzanich was fired soon after having an inappropriate relationship with an employee.

The company has been mired in R&D delays and engineering problems.

Dragging its feet could cause nightmares for its chip development for the long haul as they have lost significant market share to Advanced Micro Devices.

Then there is the general overhang of the trade war and Intel is one of the biggest earners on mainland China.

The tariff risk could hit the stock hard if the two sides get nasty with each other.

Then consider the chip sector is headed for a cyclical downturn which could dent the demand for Intel chip products.

The risks to this stock are endless and even though Intel registered a good earnings report last out, 2019 is set up with landmines galore.

If this stock treads water in 2019, I would call that a victory.