Global Market Comments

September 11, 2024

Fiat Lux

Featured Trade:

(TESTIMONIAL)

(WHY DOCTORS, PILOTS, AND ENGINEERS MAKE TERRIBLE TRADERS)

Global Market Comments

September 10, 2024

Fiat Lux

Featured Trade:

(IF YOU SELL IN MAY AND GO AWAY, WHAT TO DO IN SEPTEMBER?)

(ONSHORING: THE NEW GLOBAL TREND)

That is the conundrum facing traders, investors, and individuals as we enter the home stretch for the year. For some hedge fund managers, Q3 2024 is clearly turning into the quarter from hell.

I have been in the market for almost six decades, long enough to collect an encyclopedia's worth of words of wisdom. One of my favorites has always been “Sell in May and Go Away.” On close inspection, you’ll find there is more than a modicum of truth in this time-worn expression.

Refer to your handy Stock Traders Almanac and you’ll find that for the last 50 years, the index yielded a paltry 1% return annually from May to October. From November to April, it brought in a far healthier 7% return.

This explains why you find me with my shoulder to the grindstone during the winter, and jetting about from Baden-Baden to Monte Carlo and Zermatt in the summers. Take away the holidays and this is really a four-month-a-year job.

My friends at StockCharts.com put together the data from the last ten years, and the conclusions on the chart below are pretty undeniable. They have marked every May with a red arrow and Novembers with green arrows.

What is unusual this year is that we went into September with markets at all-time highs and on top of a prodigious 11% gain in the S&P 500 (SPY), one of the sturdiest moves in history. History also shows that the bigger the move going into such a peak, the more savage the correction that follows. From my other profession the term “Bombs away” comes to mind.

Being a long-time student of the American, and indeed, the world economy, I have long had a theory behind the regularity of this cycle. It’s enough to base a pagan religion around, like the once-practicing Druids at Stonehenge.

Up until the 1920’s, we had an overwhelmingly agricultural economy which accounted for 50% of our GDP. Farmers were always in maximum financial distress in the fall, when their outlays for seed, fertilizer, and labor were at a peak, but they had yet to earn any income from the sale of their crops. They had to all borrow at once, placing a large call on the financial system as a whole. This is why we have seen so many stock market crashes in October. Once the system swallows this lump, it's nothing but green lights for six months.

Once the cycle was set and easily identifiable by low-end computer algorithms, the trend became a self-fulfilling prophecy, even though only 2% of our economy comes from agriculture. Yes, it may be disturbing to learn that we ardent stock market practitioners may in fact be the high priests of a strange set of beliefs. But hey, some people will do anything to outperform the market.

Bombs Away?

By now, we have all become experts in offshoring, the practice whereby American companies relocate manufacturing jobs overseas to take advantage of low wages, missing unions, the lack of regulation, and the paucity of environmental controls. The strategy has been by far the largest source of new profits enjoyed by big companies for the past two decades. It has also been blamed for losses of US jobs, with some estimates reaching as high as 25 million.

When offshoring first started 50 years ago, it was a total no-brainer. Wages were sometimes 95% cheaper than those at home. The cost savings were so great that you could amortize your total capital costs in as little as two years. So American electronics makers began filing overseas to Singapore, Thailand, Hong Kong, Taiwan, South Korea, and the Philippines. After the US normalized relations with China 50 years ago, the action moved there and found that labor was even cheaper.

Then, a funny thing happens. After 40 years of falling real American wages and soaring Chinese wages, offshoring isn’t such a great deal anymore. The average Chinese laborer earned $100 a year in 1977. Today, it is $6,563, and $24,000 for trained technicians, with total compensation rising 20% a year. At this rate, US and Chinese wages will reach parity in about 10 years.

But wages won’t have to reach parity for onshoring to accelerate in a meaningful way. Investing in China is still not without risks. Managing a global supply chain is no piece of cake on a good day. Asian countries still lack much of the infrastructure that we take for granted here. Natural disasters like earthquakes, fires, and tidal waves can have a hugely disruptive impact on a manufacturing system that is in effect a highly tuned, incredibly complex watch.

There are also far larger political risks in keeping a large chunk of our manufacturing base in the Middle Kingdom than most Americans realize. With the US fleet and the Chinese military playing an endless game of chicken off the Tawan coast, we are one mid-air collision away from a major diplomatic incident. Protectionism constantly threatens to boil over in the US, whether it is over the dumping of chicken feet, tires, or the latest, solar cells.

This is what the visits to the Foxconn factory by Apple’s CEO, Tim Cook, are all about. Be nice to the workers there, let them work only 8 hours a day instead of 16, let them unionize, and guess what? Work will come back to the US all the faster. This week, the Chinese press was ripe with speculation that Apple-induced reforms might spread to the rest of the country like wildfire.

The impact of a real onshoring move on the US economy would be huge. Some economists estimate that as many as 10%-30% of the jobs lost to offshoring could return. At the high end, this could amount to 8 million jobs. That would cut our unemployment rate down by half, at least. It added $20-$60 billion in GDP per year, or up to 0.4% in economic growth per year. It would also lead to a much stronger dollar, rising stocks, and lower bond prices. Is this what the stock market is trying to tell us, rising by 34% off the October lows?

Who would be the biggest beneficiaries of an onshoring trend? Si! Ole! Mexico, which took the biggest hit when China started soaking up all the low-wage jobs in the world. After that, the industrial Midwest has to figure pretty large, especially in gutted Michigan. With real estate prices there below their 1992 lows, if there is a market at all, you know that doing business there costs a fraction of what it did 20 years ago.

I Hear They're Offering $2 an Hour Across the Street

“The only surprise to me is that so many people were surprised,” said Nobel Prize winning economist Joseph Stiglitz, about the financial crisis he predicted.

Global Market Comments

September 9, 2024

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or SEPTEMBER LIVES UP TO ITS REPUTATION)

(COPX), (USO), (ARE), (UUP), (TLT), (JNK), (GLD), (SPY), (NASD), ($VIX)

One of my Concierge clients holds a weekly staff meeting. Each employee is told his family is being held hostage and can only be rescued if they recommend the top-performing stock for the coming week. Then everyone throws in their two cents worth.

Last week, for the first time in the company’s history, no one could come up with a single name, even if it meant sacrificing their family (nobody was really sacrificed).

That speaks volumes.

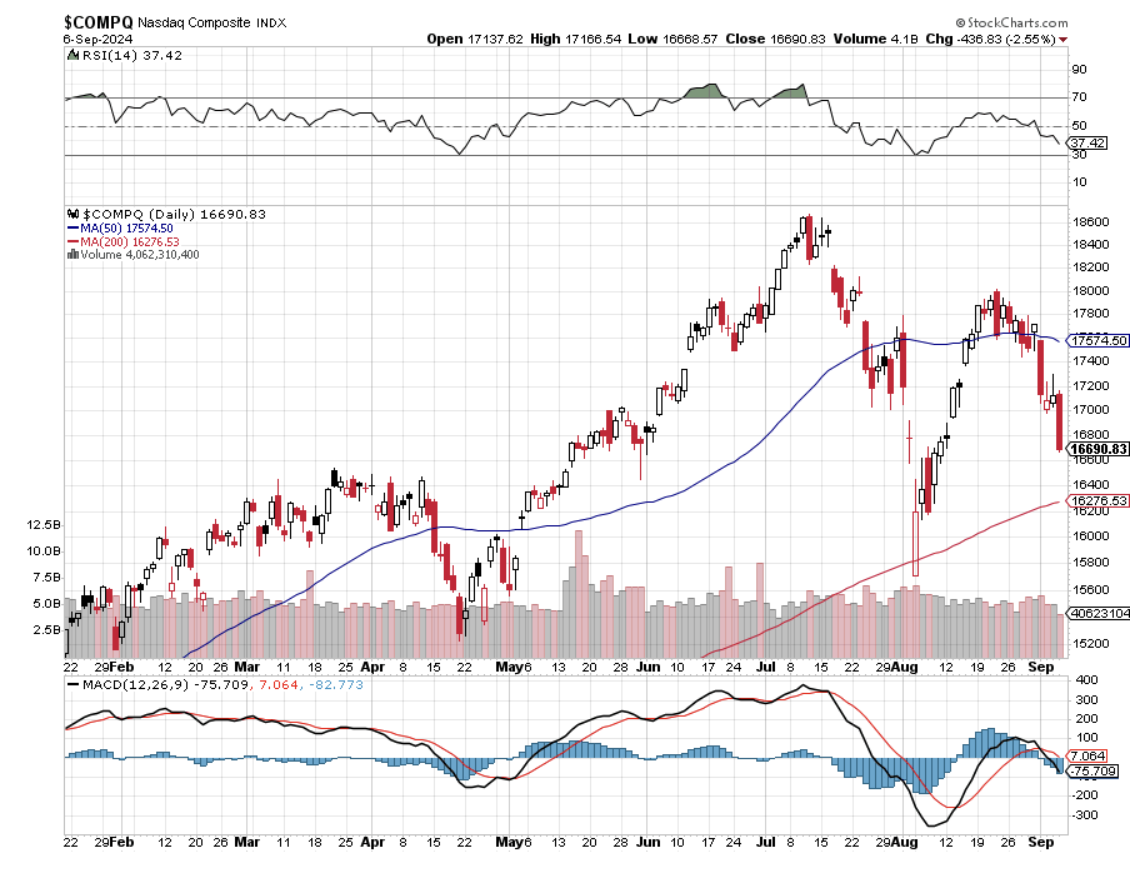

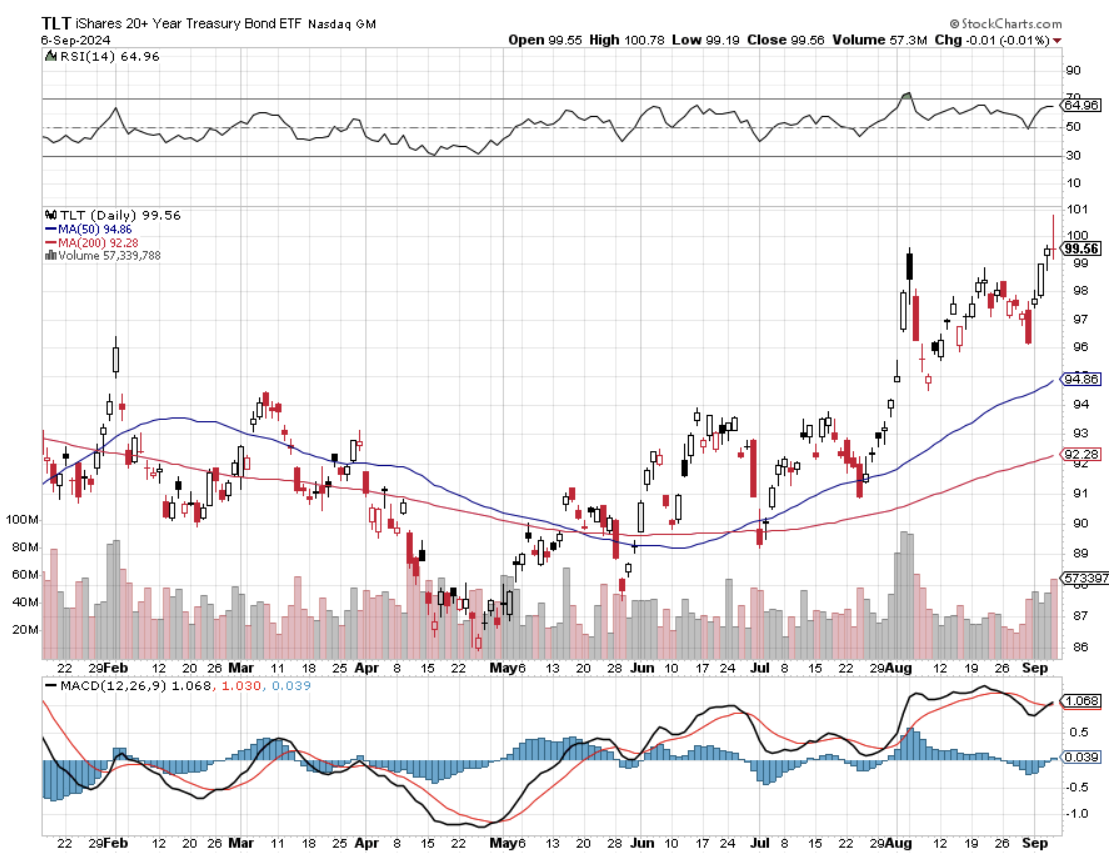

In fact, until last week, every asset class in the market was discounting an imminent recession: Commodities (COPX), energy (USO), real estate (ARE), and the US dollar (UUP). Reliable recession hideouts like bonds (TLT), fixed income (JNK), and gold (GLD) caught an endless bid. Only the stock market (SPY), (NASD) wasn’t reading from the same music sheet.

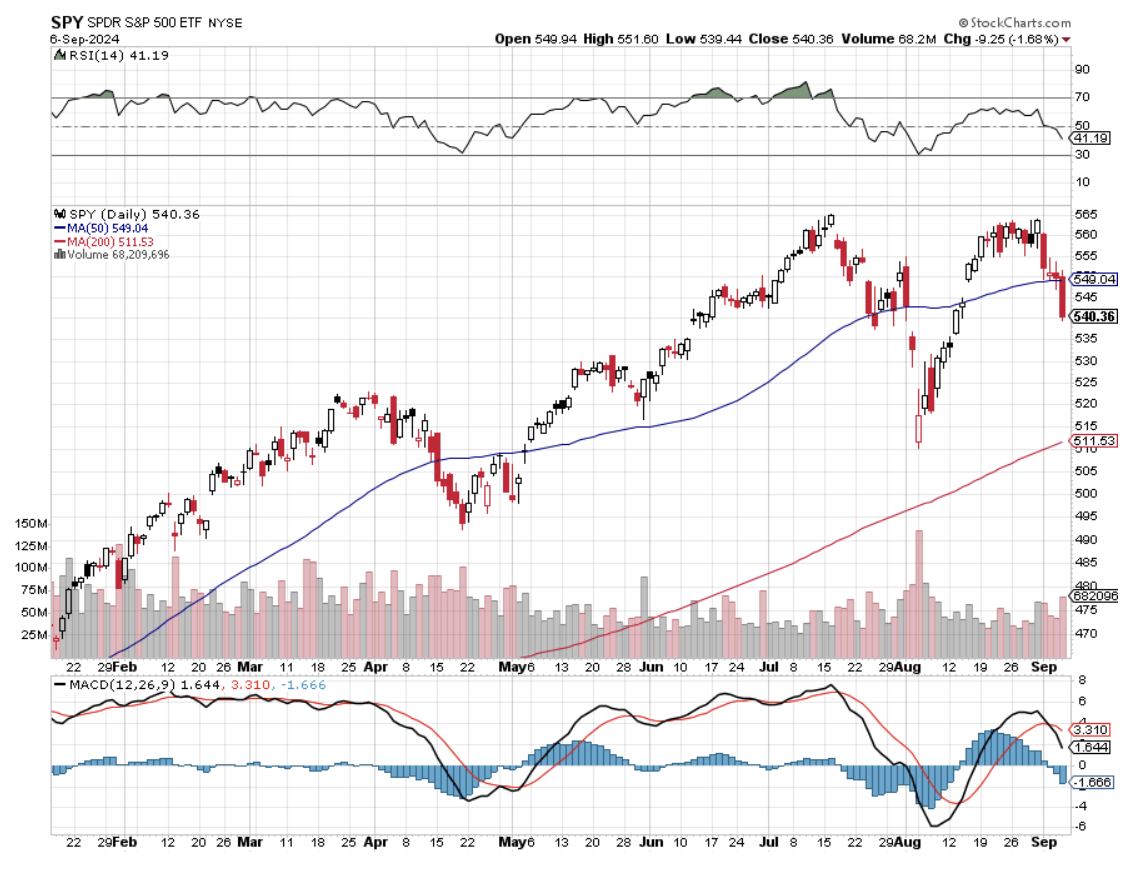

Well, stocks finally got the memo, delivering the worst week in 2 ½ years. Suddenly, the glass has gone from half full to half empty. Permabears have suddenly morphed from complete idiots to maybe having something to say. Here it is only September 9 and the Month from Hell is already living up to its awful reputation. Is the stock market the slow learner in the bunch?

I came back from Europe in August rested, refreshed, invigorated, and in a near state of panic. The last 11% rally in the (SPY) made absolutely no sense to me whatsoever. Either the September jobs data would come in hot, canceling the Fed’s expected interest rate cut. Or, the data would come in cold, proving that the Fed waited too long to cut rates and inviting a recession, causing stocks to tank.

It would have been one of the worst self-inflicted wounds and own goals of all time.

What was especially dangerous was that we were going into the worth trading month of the year, September, with the (SPY) showing a crystal-clear double top on the charts.

It was a perfect lose/lose situation.

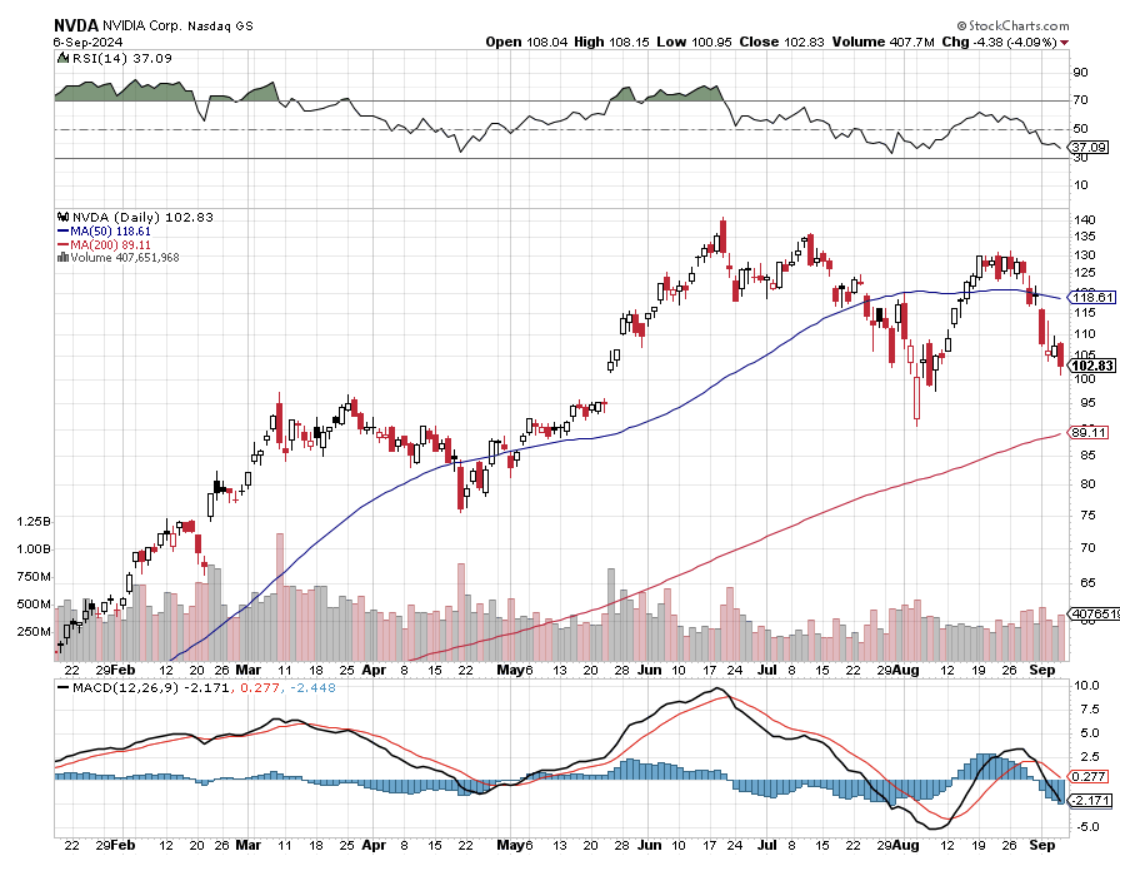

Seasonals are important, especially this month. This is because most mutual funds run an annual year that ends on September 30. To window dress their books and those glossy marketing brochures, they sell all their losers (think energy) in September and use the cash to buy more of their winners in October. (NVDA) yes, (XOM) not so much. This creates a swing in the indexes every year of 10%-20%.

To learn more about the seasonals, read tomorrow’s letter in detail, IF YOU SELL IN MAY AND GO AWAY, WHAT TO DO IN SEPTEMBER?

So I did what I usually do when the market refuses to give me marching orders. I let all my positions expire with the August 16 options expiration, took back the cash, and then sat on my hands. Suddenly, a 100% cash position was looking like a stroke of genius. It cleared the cobwebs, moved the fog away from my eyes, and took the monkey off my back all in one fell swoop.

And you know what? After surveying my big hedge fund clients, I learned they were doing exactly the same thing.

Let me pass on another piece of interesting intel. All of the many algorithms the hedge fund industry follows are bunching up around two specific bottoms for the stock market in coming months: September 18, the Fed rate cut day, and October 22, two weeks before the presidential election.

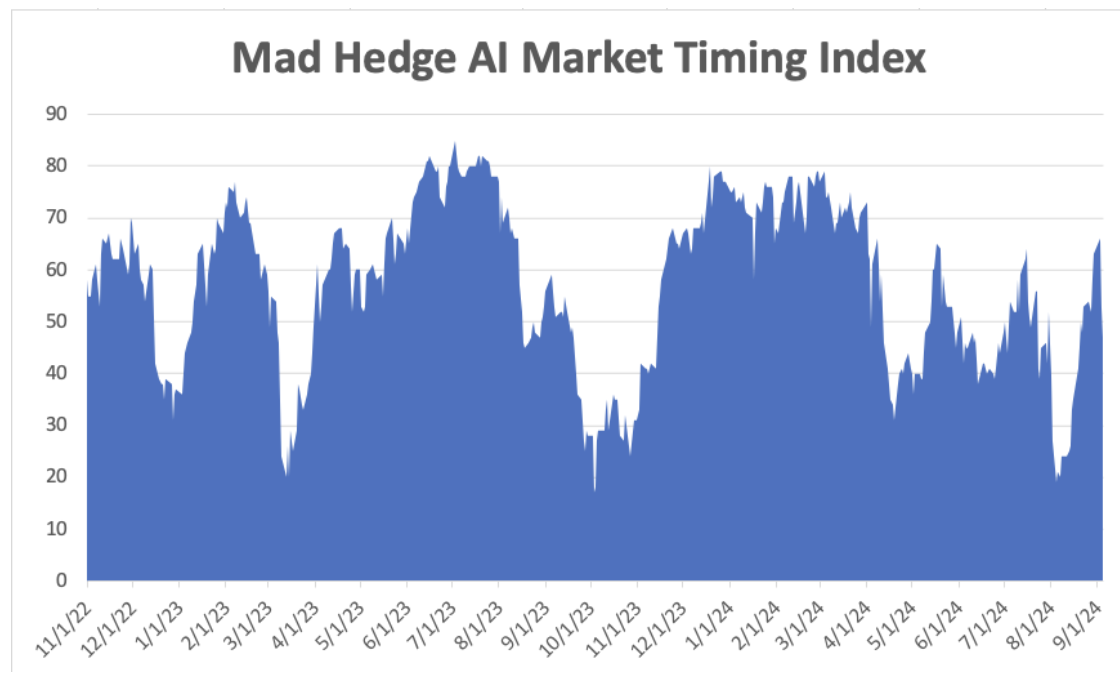

With any luck, other classic “BUY” signals will kick in at the same time with the Mad Hedge Market Timing Index below 20 by then and the Volatility Index ($VIX) over $30. It could be the best entry point of the year.

What has been fascinating is how much money has been pouring into the interest rate plays I have been banging the table about for the last six months. When was the last time the stock market has been led by AT&T (T), Altria (MO), and Crown Castle International (CCI)? You might have to look behind the radiator to find some old, dusty research on these names.

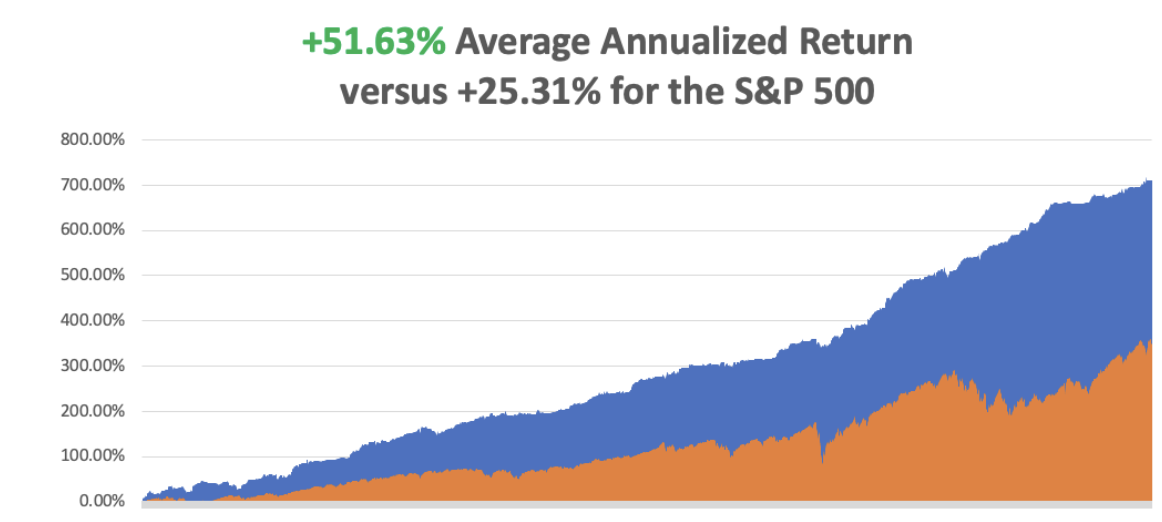

So far in September, we are down by -1.21%. My 2024 year-to-date performance is at +33.49%. The S&P 500 (SPY) is up +13% so far in 2024. My trailing one-year return reached +51.89. That brings my 16-year total return to +710.12. My average annualized return has recovered to +51.63%.

I executed only one trade last week, covering a short in Tesla at cost. I am now maintaining a 100% cash position. I’ll text you next time I see a bargain in any market. Now there is none. There is no law dictating that you have to have a position every day of the year. Only your broker wants you to trade every day.

Some 63 of my 70 round trips, or 90%, were profitable in 2023. Some 47 of 66 trades have been profitable so far in 2024, and several of those losses were really break-even. That is a success rate of +72.24%.

Try beating that anywhere.

Nonfarm Payroll Report Fades at 142,000, but the Headline Unemployment Rate stays at 4.2%. More shocking is that the previous two months saw substantial downward revisions. The BLS cut July’s total by 25,000, while June fell to 118,000, a downward revision of 61,000. If the Fed doesn’t cut by 0.50% on September 18, the stock market will crash.

Broadcom Beats and Stock Tanks driven by strong sales of its AI products and VMware software. But management’s guidance for the current quarter disappointed investors, sending shares of the chipmaker down nearly 7% in the after-market. This is too harsh of a reaction to an otherwise solid print. Buy (AVGO) on dips.

ADP Employment Change Report Hits 3 ½-Year Low, up only 99,000 in August. Economists polled had forecast private employment would advance by 145,000 positions after a previously reported gain of 122,000.

Biden Blocks Nippon Steel Takeover of US Steel, no doubt to save the jobs these deals usually destroy. Good thing we got out of the (X) LEAPS a year ago at max profit. (X) dropped 20% on the news. Not a good time to concentrate on industry.

No Subpoenas Here Says NVIDIA, refuting rumors that it was the target of an antitrust action. Don’t believe everything you read on the internet.

The Yield Curve has De-Inverted, meaning that short-term interest rates have fallen below long-term ones. Two-year interest rates at 3.72% are now 0.03% lower than ten-year ones at 3.75%. It’s a clear signal to the Fed that rates must be cut soon.

Weekly Jobless Claims Drop 5,000 to 227,000. The weekly jobless claims report from the Labor Department on Thursday, the most timely data on the economy's health, also showed unemployment rolls shrinking to levels last seen in mid-June. It reduces the urgency for the Federal Reserve to deliver a 50-basis points interest rate cut this month.

US Oil Production Hits All-Time High. In August 2024, U.S. oil production hit a record 13.4 million barrels per day according to the U.S. Energy Information Administration. Big Oil has become more productive as horizontal drilling and hydraulic fracturing, which is also known as fracking, have seen technological breakthroughs. The fossil fuel industry benefits from tax incentives, such as the intangible drilling costs tax credit, that are built into the tax code. The intangible drilling costs tax break is expected to benefit oil and gas companies by $1.7 billion in 2025 and $9.7 billion through 2034

Crude Oil Now Down on the Year, after a precipitous weekend selloff. Blame a weak China, lost OPEC discipline, and overproduction by Iraq. The bearish Goldman Sachs commodities report was also a factor. Avoid the worst-performing asset class in the market.

Eli Lilly is now a trillion-dollar stock, the first Biotech to do so. The drug giant is riding the wave of Mounjaro and Zepbound, its blockbuster injectable GLP-1 medications for weight loss. The drugs are also used to treat diabetes and cardiovascular disease. Eli Lilly’s shares have soared 65% this year.

Goldman Goes Big on Gold. Central banks in emerging market countries are continuing to buy gold — with purchases tripling since the middle of 2022 amid fears of U.S. financial sanctions and a mountain of sovereign debt. Goldman is taking a more selective approach to commodity investing as soft demand in China weighs on crude oil and copper prices. The investment bank has slashed its Brent oil outlook by $5 to a range of $70 to $85 per barrel and delayed its copper target of $12,000 per metric ton until after 2025.

My Ten-Year View

When we come out the other side of the recession, we will be perfectly poised to launch into my new American Golden Age or the next Roaring Twenties. The economy decarbonizing and technology hyper accelerating, creating enormous investment opportunities. The Dow Average will rise by 600% to 240,000 or more in the coming decade. The new America will be far more efficient and profitable than the old.

Dow 240,000 here we come!

On Monday, September 9 at 3:00 PM EST, Consumer Inflation Expectations are out

On Tuesday, September 10 at 6:00 AM, the NFIB Business Optimism Index is released.

On Wednesday, September 11 at 7:30 AM, the Core CPI is printed.

On Thursday, September 12 at 8:30 AM, the Weekly Jobless Claims are announced. We also get the Producer Price Index.

On Friday, September 13 at 8:30 AM, the University of Michigan Consumer Sentiment. At 2:00 PM the Baker Hughes Rig Count is printed.

As for me, I was having lunch at the Paris France casino in Las Vegas at Mon Ami Gabi, one of the top ten-grossing restaurants in the United States. My usual waiter, Pierre from Bordeaux, took care of me with his typical ebullient way, graciously letting me practice my rusty French.

As I finished an excellent, but calorie packed breakfast (eggs Benedict, caramelized bacon, hash browns, and a café au lait), I noticed an elderly couple sitting at the table next to me. Easily in their 80s, they were dressed to the nines and out on the town.

I told them I wanted to be like them when I grew up.

Then I asked when they first went to Paris, expecting a date sometime after WWII. The gentleman responded, “Seven years ago.”

And what brought them to France?

“My father is buried there. He’s at the American Military Cemetery at Colleville-sur-Mer along with 9,386 other Americans. He died on Omaha Beach on D-Day. I went for the D-Day 70th anniversary.” He also mentioned that he never met his dad, as he was killed in action weeks after he was born.

I reeled with the possibilities. First, I mentioned that I participated in the 40-year D-Day anniversary with my uncle, Medal of Honor winner Mitchell Paige, and met with President Ronald Reagan.

We joined the RAF fly-past in my own private plane and flew low over the invasion beaches at 200 feet, spotting the remaining bunkers and the rusted-out remains of the once floating pier. Pont du Hoc is a sight to behold from above, pockmarked with shell craters like the moon. When we landed at a nearby airport, I taxied over railroad tracks that were the launch site for the German V1 “buzzbomb” rockets.

D-Day was a close-run thing and was nearly lost. Only the determination of individual American soldiers saved the day. The US Navy helped too, bringing destroyers right to the shoreline to pummel the German defenses with their five-inch guns. Eventually, battleships working in concert with very lightweight Stinson L5 spotter planes made sure that anything the Germans brought to within 20 miles of the coast was destroyed.

Then the gentleman noticed the gold Marine Corps pin on my lapel and volunteered that he had been with the Third Marine Division in Vietnam. I replied that my father had been with the Third Marine Division during WWII at Bougainville and Guadalcanal and that I had been with the Third Marine Air Wing during Desert Storm.

I also informed him that I had led an expedition to Guadalcanal two years ago looking for some of the 400 Marines still missing in action. We found 30 dog tags and sent them to the Marine Historical Division at Quantico, Virginia for tracing. I proudly showed them my pictures.

When the stories came back it, turned out that many survivors were children now in their 80s who had never met their fathers because they were killed in action on Guadalcanal.

Small world.

I didn’t want to infringe any further on their fine morning out, so I excused myself. He said Semper Fi, the Marine Corps motto, thanked me for my service, and gave me a fist pump and a smile. I responded in kind and made my way home.

Oh and say “Hi” when you visit Mon Ami Gabi. Tell Pierre that John Thomas sent you and give him a big tip. It’s not easy for a Frenchman to cater to all these loud Americans.

Third Marine Air Wing

The D-Day Couple

The American Military Cemetery at Colleville-sur-Mer

Stay Healthy,

John Thomas

CEO & Publisher

The Diary of a Mad Hedge Fund Trader

“Over the long term, all of the fiat currencies of the world are involved in a competitive devaluation. The structural stresses in most of the western economies are such that central banks will attempt to continue to substitute liquidity for solvency,” said Rick Rule, director, president and CEO of Sprott U.S. Holdings, a precious metals specialist.

Global Market Comments

September 6, 2024

Fiat Lux

Featured Trade:

(ANOTHER CRYPTO VICTIM BITES THE DUST)

Global Market Comments

September 5, 2024

Fiat Lux

Featured Trade:

(COFFEE WITH RAY KURZWEIL)

(GOOG)