Readers of the Diary of a Mad Hedge Fund Trader down under are welcome to join the online ?Secure the Future? conference which I will be participating in through the miracle of the Internet. My friend, Greg Owen, created this organization to educate investors in the opportunities available in international markets by bringing in industry veterans like myself. I will be making presentations on the current state of and prospects for the global financial markets, to be followed by an extended question and answer session. No doubt I will spend a lot of time expounding on my outlook for Australian stocks, bonds, commodities, precious metals, and real estate. My schedule is below.

Sydney on Saturday, May 12 at 2:00 PM

Brisbane on Tuesday, May 15 at 2:00 PM

Perth on Thursday, May 17 at 2:00 PM

To register for the event, please click here at www.securethefuture.com.au/greg . In order to register, you will need to input your credit card information. However, you can attend as my guest, so there will be no charge made to your credit card. I look forward to hearing from you in the Q & A.

As of this week, Oregon will become the first state to complete a chain of charging stations that will enable electric cars to travel from one end of the state to the other. It completed the last of eight 440 volt fast charging stations that allow travel for the full 310 miles on the beaver state?s Interstate 5, from the Washington to the California border.

A fleet of Tesla Roadsters, Nissan Leafs, Fisker Karmas, and Mitsubishi iMiEVs celebrated the event by traveling in convoy from one end of the state to the other. It is all part of the Electric Highway Project, which has the final goal of building an all-electric corridor from Canada to Mexico.

The development understates how rapidly electric cars are going mainstream. Once the domain of the wealthy who bought Tesla?s $100,000 two seat roadster, prices are now falling to the level of high end luxury cars. Tesla?s own Model S1 Sedan, which carries a 300 mile range, will be available for $58,000. Toyota announced that its electric Rav4 SUV will cost $49,800 and will include a Tesla built drive train. My own 100 mile range Nissan Leaf cost me $38,000, and after a year has delivered me 12,000 miles of pleasant driving with zero fuel and maintenance costs. Also on the drawing board is a Tesla driven Mercedes ?A? class Smart car for even less.

Toyota invested $60 million in founder Elon Musk?s fledgling car company to assure timely deliveries. Elon wisely used the cash to buy the abandoned General Motors Prizm plant in Fremont, California for pennies on the dollar with some generous US government subsidies thrown in, where Model S1 production is underway.

Yesterday, Tesla announced it was moving the delivers up a month to June this year, causing a one day 10% pop in the stock, despite announcing a $98 million quarterly loss the day before. No doubt, the 10,000 on the waiting list for the S1are thrilled. Their $5,000 deposits have provided the company with $50 million in free financing for two years.

When I first bought my Leaf, finding a charging station away from home required some advanced planning and guerrilla tactics. I still feel bad about depriving a parking lot attendant of his coffee maker outlet for three hours while I enjoyed the opera, but he didn?t mind the $20 tip. That was back when there were only 25 charging stations in the entire San Francisco Bay area. Today there are nearly 400, with 20 new ones joining the ranks each week. Soon, every Walgreens, Whole Foods, and Best buy will have one, as will every major hotel in the city. Not a bad deal, given that none of these stations has yet to charge a penny for a single electron.

Tesla is moving ahead to build its own network of 440 volt ?supercharging stations? which can get you an 80% top up in 45 minutes. One is being built at Harris Ranch, half way between San Francisco and Los Angles, with a second in Sacramento, midpoint for a trip to Lake Tahoe. I can foresee a life of plugging in my car, going into Starbucks with an Economist, a Wall Street Journal, and a New York Times, and then zooming away 45 minutes later.

Although the Tesla plug won?t be compatible with my Leaf, the stations will carry adapters for all cars. I won?t need an adapter for my Tesla Model X SUV. I am one of 1,000 on the waiting list for that futuristic, 300 mile range vehicle, which should be parked in my garage in 2 years.

Tesla Model S Sedan

Tesla Model X SUV

My Leaf

I immediately recognized Robert Mueller as the kind of no nonsense, fellow ex-Marine, Vietnam Vet that he was, the kind of officer who used to rip your guts out for disobeying a direct order, which in my case was frequently.

President Obama thought this was the man you want for your Director of the FBI, which is why Mueller survived as one of the few holdovers from the previous Bush administration. Mueller has been following in the tradition of the legendary G-Man J. Edgar Hoover for 11 years now.

Mueller believes that the Internet is not just a conduit for commerce, but also for crime and terrorism, and the bad guys are checking your doorknobs every day. Information is power, and fiber optic cable is a weapon. Terrorists, in particular, love the new Google Earth application.

Recently, Mueller busted an American-Egyptian phishing ring, arresting 50, which looted 5,000 US accounts. We all must take ownership of the cyber security problem through the vigilant use of antivirus software, firewalls, sophisticated and frequently changed passwords, and constant patches. Tracing a 75-cent accounting discrepancy at UC Berkeley led to the smashing of a German industrial espionage ring that was tapping into university computers.

Teenaged kids, like the Canadian who launched the biggest ?denial of service? attack against E-Trade and E-Bay, are to be feared. Be careful what you post on your Facebook page because it may kill a job prospect years down the road.

The FBI is now embedding agents in police departments in Eastern Europe and China to take the fight global. The last time a visited FBI headquarters in Washington, I was amazed to learn that Chinese anti-hacking specialists kept their own office there.

When I got home, I immediately backed up all my files, reset my passwords, and bought my fourth antivirus program. I also installed bars on my windows and set booby traps on the front lawn for good measure. Maybe Apple products, usually immune to these sorts of problems, are not so bad after all?

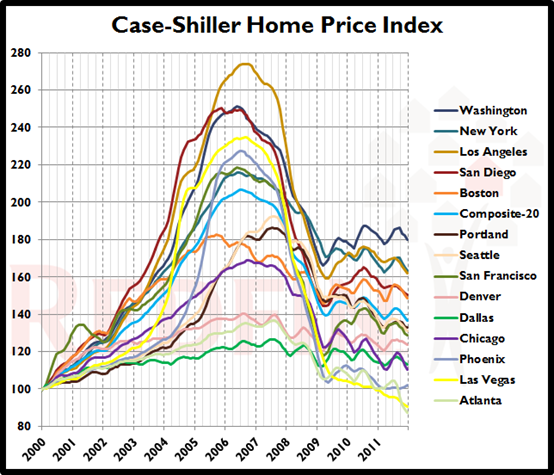

Yale professor, Robert Shiller, is the kind of imp like, peripatetic college professor you might expect to find in a Disney movie. Highly animated and jumping from one radical idea to the next it is hard to keep up with his stream of consciousness torrent of economic innovations. After a two-hour barrage, I was so intellectually exhausted that all I could do when I returned home was to plop down on the sofa with a Jack on the rocks and watch Fox News.

You know Robert Shiller as the creator of the Case Shiller Real Estate Index, which tracks 20 major residential housing markets around the US. His data was originally the domain of a handful of real estate brokers with a theoretical bent or securitizing investment bankers. But when the real estate collapse began to accelerate in 2007, it suddenly became the data point du jour for every property investor, business news network, and hedge fund manager.

Shiller is a devout non believer of the efficient market theory espoused by Eugene Fama of the University of Chicago. He thinks that financial markets are so emotional that they are beyond rational analysis. The systemic vulnerability of financial markets was a major cause of the 2008 crash and is still not well understood. He argues that people should have a 100 year time horizon when making investments, because that?s how long today?s children will live. Does anyone have the trading call for the Spring of 2112? (no typo!).

He says that teaching finance today is about as popular as being the university Reserve Officer Training Corps (ROTC) instructor during the Vietnam War. People are angry at bankers, as the Occupy Wall Street crowd has so amply shown, which Shiller sees as our own ?Arab Spring?. Since 1990, the top 1% of the wealthy have seen their net worth soar by 60%, while it has fallen for the other 99%.

When Occupiers discovered that their movement could cause governments to fall, it rapidly spilled beyond its Madrid, Spain origins. But the financial industry is not all bad. Witness the miracle in emerging markets which has been made possible through new capital provided by western investment bankers.

Robert titillated me with some highly creative innovations which we may see adopted in coming years. I?ll give you the highlights.

*Options on individual real estate markets, now five years old, will go mainstream and finally become liquid as individuals seek to protect their home equity during economic downturns. This will become a major area of new profits for Wall Street.

*?Continuous mortgages? should be created whereby the debt is never paid off, but is assumed from one owner to the next in exchange for a higher interest rate. If you package many of these together and securitize them, it would be a major step towards clearing out the massive inventory of unsold homes.

*The government already issues plenty of bonds and next should sell equity in itself in one trillionth increments. That puts the value of the government?s share price today at about $15.50. If the economy grows, the share price should go up.

*Tax rates for the wealthy should rise with inequality. The more wealth that is concentrated with the 1%, the higher the maximum tax rate should go. Remember, the maximum rate was 90% at the time of the Roosevelt administration during the Great Depression, nearly triple today?s 35% rate.

*The actual impact of high frequency traders, who he refers to as ?millisecond traders?, is vastly exaggerated.

*Although the new ?crowd funding? bill just signed by president Obama has been described as the ?Boiler Room Full Employment Act?, it will provide a valuable source of venture capital for micro startups. Those earning only $40,000 a year are limited to an $800 bet, with the maximum legal investment set at $10,000.

*Some 14% of the total economic activity of the US involves security. Just having people watching people is an enormous waste of resources.

*For profit nonprofits, called benefit corporations, should proliferate to advance specific social goals. These should work well as they pay little in wages and enjoy community support. They are already legal in eight states.

If you would like to attend one of Shiller?s classes for free and expose yourself to more out of the box economic thinking, you can do so through regular offerings of his online courses. To sign up for Open Yale University, which Time magazine lists as one of the top websites, please click here at http://oyc.yale.edu/economics .

And what about real estate? Robert told me that his data show that there is not the slightest sign of any long term recovery in prices. Real estate brokers insisting that the final bottom has been reached are best to be ignored. Rent, don?t buy.

With Treasury Secretary, Tim Geithner, in Beijing last week kowtowing to the largest foreign owner of our national debt, the prospect of the dollar?s demise as a reserve currency has once again reared its ugly head.

Will people pleeease stop incessantly nattering about the possibility of China dropping the dollar as a reserve currency? What else are they going to use? Monopoly money? Taiwanese dollars? Collectable postage stamps?

At $3.6 trillion and rising fast, the Middle Kingdom?s reserves are so enormous that no other currency in the world could accommodate the switch, and no other security offers the necessary depth and liquidity but US Treasuries. China only needs to breathe on any other market for it to skyrocket, we have seen in the relatively Lilliputian commodity markets in recent years.

And really, how likely is it that China embarks on radical new monetary policies that suddenly halves the earnings of its exporters, as well as its 30 year hoard of accumulated savings? The demise of the dollar has been predicted more often than the ditching of Microsoft?s Windows as the global PC operating system, and is just as likely. Hate the greenback as much as you like, but there just isn?t any other alternative.

I have been hearing these arguments ever since the US went off the gold standard in 1971. First there was a perennial Arab threat to price crude in a basket of currencies. Gee, they never seem to complain when the buck is going up. Then there was the speculated emergence of the ?Yen Block?, in the eighties, back when Japan was dominating international trade and the yen was bumping up against ?75 to the dollar. Remember the book ?Japan as Number One? What a laugh.

Next we got all that European whining after the launch of the euro, when the weak dollar was every trader?s free lunch. Let?s face it, Europeans hate using someone else?s currency as their primary reserve instrument. Before the dollar, sterling was the de facto international currency, and was equally despised. So rather than waste time discussing this issue anymore, let?s talk about something more important, like who is going to win the World Series this year. I?m wearing my Yankees hat.

Our New Reserve Currency?

After my entertaining repast with the head of our nation?s intelligence service, I had to ask myself this question.

During the sixties, new dwarf varieties, irrigation, fertilizer, and heavy duty pesticides tripled crop yields, unleashing a green revolution. But guess what? The world population has doubled from 3.5 to 7 billion since then, eating up surpluses, and is expected to rise to 9 billion by 2050.

Now we are running out of water in key areas like the American West and Northern India, droughts are hitting Australia, Africa, and China, soil is exhausted, and global warming is shriveling yields. Water supplies are so polluted with toxic pesticide residues that rural cancer rates are soaring.

Food reserves are now at 20 year lows. Rising emerging market standards of living are consuming more and better food, with Chinese pork demand rising 45% from 1993 to 2005. The problem is that meat is an incredibly inefficient calorie transmission mechanism, creating demand for five times more grain than just eating the grain alone.

To produce one pound of beef, you need 16 pounds of grain and over 2,000 gallons of water! I won?t even mention the strain the politically inspired ethanol and biofuel programs have placed on the food supply. Burning food so you can drive your GM Suburban to Wal-Mart on the weekends while millions are starving never made much sense to me.

It is possible that genetic engineering, sustainable farming, and smart irrigation could lead to a second green revolution, but the burden is on scientists to deliver.

The amount of arable land per person has fallen precipitously since 1960, from 1.1 acres to 0.6 acres, and that could halve again by 2050. Water is about to become even more scarce than land. Productivity gains from new seed types are hitting a wall.

China, especially, is in a pickle because it has 20% of the world?s population, but only 7% of the arable land. It has committed $5 billion to develop agricultural land in Africa. There are now thought to be over one million Chinese agricultural workers on the Dark Continent. Similarly, South Korea has leased half the arable land in Madagascar to insure their own food supplies.

An impending global famine has not escaped the notice of major hedge funds. George Soros has snatched up 650,000 acres of land in Argentina and Brazil on the cheap, an area half the size of Rhode Island, Others are getting into the game, quietly building portfolios of farms in the Midwest and the South.

This year promises to deliver one of the greatest US crop yields in history, brought on by the warmest winter in 100 years. The US Dept. of Agricultural January crop report then predicted huge surpluses, slamming prices once again, and delivering limit down moves in the futures markets. But the weather may not cooperate, as it did last year.

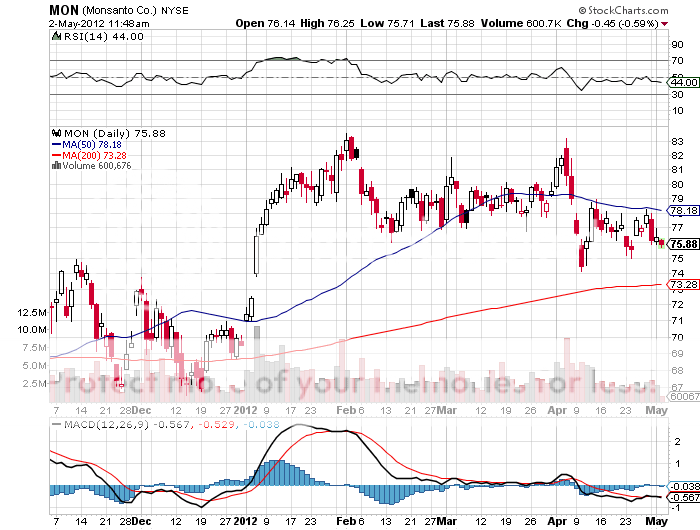

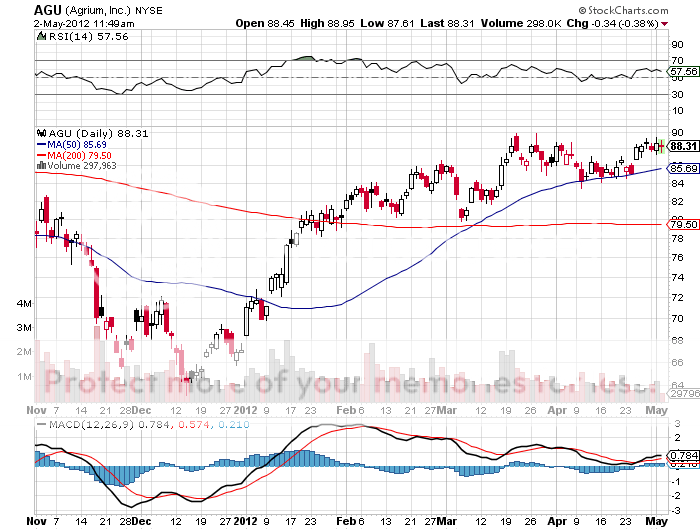

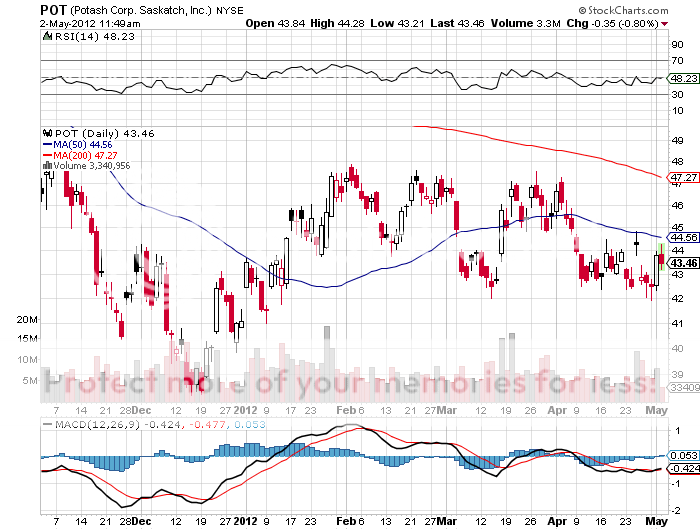

The net net of all of this is that food prices are going up, a lot. Use this year?s expected weakness in prices to build core long positions in corn, wheat, and soybeans, as well as in the second derivative plays like Potash (POT), Agrium (AGU) and Monsanto (MON). You might also look at the PowerShares Multi Sector Agricultural ETF (DBA) and the Market Vectors Agribusiness ETF (MOO).

A ?BUY? SIGNAL?

The original purpose of this letter was to build a database of ideas to draw on in the management of my hedge fund. When a certain trade comes into play, I merely type in the symbol, name, currency, or commodity into the search box, and the entire fundamental argument in favor of that position pops up. With a link chain to older stories.

You can do the same. Just type anything into the search box with the little magnifying glass in the upper right hand corner of my homepage and a cornucopia of data, charts, and opinion will appear. Even the price of camels in India (to find out why they?re going up, click here) As of today, the database goes back to February 2008, and comprises some 2 million words, or triple the length of Tolstoy?s epic novel, War and Peace.

Watching the traffic over time, I can tell you how the database is being used, and the implications are fascinating:

1) Small hedge funds want to see what the large hedge funds are doing.

2) Large hedge funds look to see what they have missed, which is usually nothing.

3) Midwestern advisors to find out what is happening in New York and Chicago.

4) American investors to find out if there are any opportunities overseas (there are lots).

5) Foreign investors wish to find out what the hell is happening in the US (about 1,000 inquiries a day come in through Google?s translation software in a multitude of languages).

6) Specialist traders in stocks, bonds, currencies, commodities, and precious metals are looking for cross market insights which will give them a trading advantage with their own book.

7) High net worth individuals managing their own portfolios so they don?t get screwed on management fees.

8) Low net worth individuals, students, and the military looking to expand their knowledge of financial markets (lots of free online time in the Navy).

9) People at the Treasury and the Fed trying to find out what the private sector is doing.

10) Staff at the SEC and the CFTC to see if there is anything new they should be regulating.

11) More staff at the Congress and the Senate looking for new hot button issues to distort and obfuscate.

12) Yet, even more staff in Obama?s office gauging his popularity and the reception of his policies.

13) As far as I know, no justices at the Supreme Court read my letter. They?re all closet indexers.

14) Potential investors/subscribers attempting to ascertain if I have the slightest idea of what I am talking about.

15) Me trying to remember trades which I recommended, but have forgotten.

16) Me looking for trades that worked so I can say ?I told you so.?

It?s there, it?s free, so please use it.

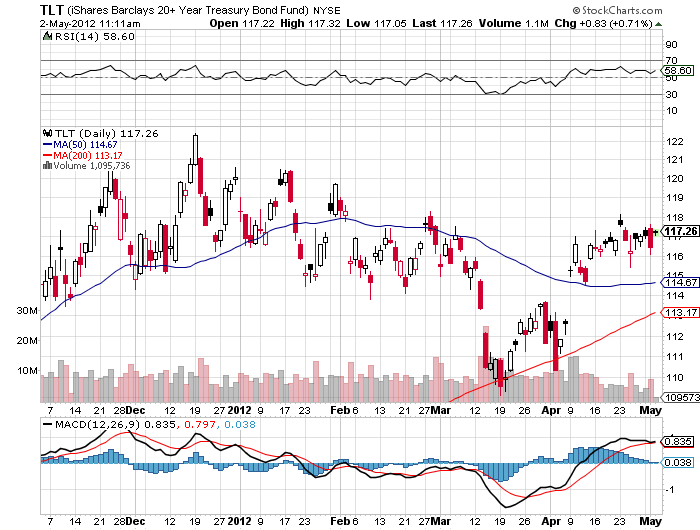

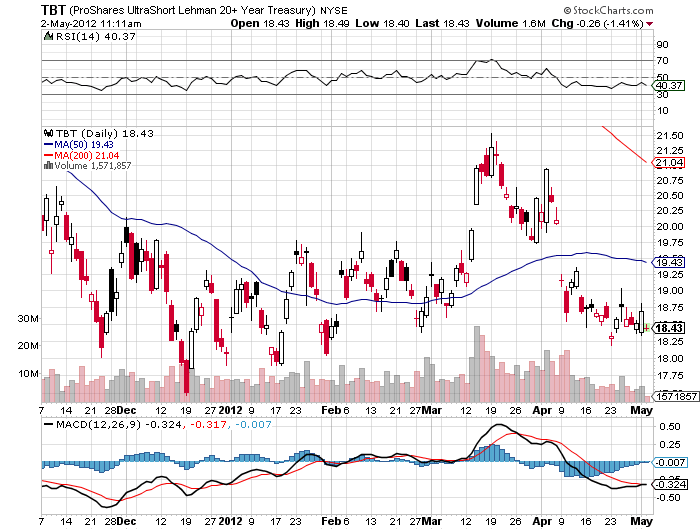

In order to enjoy your coming weekend, I thought you'd like a technical update of your positions, so feast your eyes on the two charts below. They say that a picture is worth a thousand words, so here is 2,000 words worth. If you have been negative on bonds as I have, these charts should enable you to sleep much better.

Virtually every fixed income product is peaking now. Let me draw a simple picture for you laymen out there. That means you should sell every major bond market rally for the next ten years. Whether the final bottom in yields for the ten year Treasury bond is the 1.80% that we have already seen, or 1.60% coming this summer is anyone?s guess. The technical set up is now so dire, that bonds are going to have a really tough time rallying from here. The momentum players will soon smell blood in the water, and they'll be jumping in with both feet at every opportunity. The lost decade for bonds has begun!

Of course, you knew this was coming. It doesn?t help that the budget proposals for both political parties going forward will engineer a dramatic increase in the deficit. The bond market is not laughing. Of course putting in the final top in a 30 year move could be a multiyear process. But it is time to dump that old investment guidline where you own your age in bonds. From here on, the bond/equity ratio should be o% in bonds and 100% in equities, whatever your age.

Is the Lost Decade for Bonds Beginning?

Hey! You there, staring at this monitor. This is your PC talking to you. No, not you over there standing in the background. I?m talking to the guy sitting in front of me poking at my keys. Ouch! That one hurt!

So you thought no one was watching, did you? Let me straighten you out. About a month ago you clicked on a certain website, and I installed myself as a cookie on your computer, which is an innocuous little text file that you can?t see. Since then, I have been tracking your every move, recording websites you clicked on, the pages you visited, and the stuff you ordered. I then used this handy little algorithm to build a profile of exactly who you are. I now know you better than your own mother. In fact, I know you better than you know yourself.

For example, I am aware that you make more than $250,000 a year, live in a posh zip code in San Francisco, belong to a fancy country club, and drive a Mercedes. You donate to Republican political causes, send your kids to a prestigious private school, and bill it all to an American Express Platinum Card. Did I leave anything out?

Because I know every detail of your life, down to your inside leg measurement, I am able to harness the power of this machine to more precisely service your every need. That includes directing advertising to you, which you have a high probability of clicking on. The more you click on my ads, the higher prices I can realize for those ads. The ad campaigns you now see are unique to your own personal computer because they are tied to your IP address. My program, called ?behavioral targeting? is the next ?big thing? in online advertising. It?s all part of the brave new world.

I see you have been shopping for a new car. Check out the new Hyundai at http://www.hyundaiusa.com/ , which offers the same quality as your existing ride, at half the price. Your clicks this morning suggest you?re taking your ?significant other? out to dinner tonight. Might I suggest Gary Danko?s on Bay Street at http://www.garydanko.com/site/bio.html ? The rack of lamb is to die for there. Your visits to http://www.travelocity.com/ and http://www.expedia.com/ tell me you?re planning a vacation. I bet you didn?t know you can find incredible deals in Las Vegas at http://www.visitlasvegas.com/vegas/index.jsp . Thinking about buying a condo there? They?ll even pay for the trip if you promise to check one out while you?re there.

Since we?re chatting here mano a mano, I noticed that that last pair of jeans you ordered from http://us.levi.com/home/index.jsp had a 42-inch waist, up from the 40?s in your last order. Better lay off those cheeseburgers. Pretty soon, they?ll be calling you ?tubby? or ?fatso?. Better visit http://www.weightwatchers.com/Index.aspx soon, or the legs on that chair might buckle out from under you.

Worried about privacy? Privacy, shmivacy. There hasn?t been privacy in this country since the first social security number was handed out in 1936. And don?t expect any relief from Congress. I doubt half those dummies even know how to turn on their own PC?s.

Don?t even think about trying to delete me. I?m a ?flash cookie?, an insidious little piece of code that reinstalls every time you try that. Think of me as a toenail fungus. Once you catch me, I?m almost impossible to get rid of.

I hope you don?t mind, but I?ve been passing your personal details around to some of my buddies at other websites. That?s why when you clicked on http://www.nfl.com/ you got deluged with product offers from your local team, the San Francisco 49ers. I?ve got friends at Google, Facebook, MySpace, and pretty much everywhere. Can I help it if I?m a popular guy? I bet the view from those 50 yard seats is great, isn?t it?

I noticed that your spending habits don?t exactly match with the income you reported on your last tax return. Do you think the IRS would like to know about that? I bet you didn?t know the agency offers a 10% reward for turning in tax cheats.

How did you like those triple X DVD?s you bought last week? Whoa! Hot, hot, hot! I hope your employer never finds out about those. It might not go down too well at your next performance review.

I thought it was lovely that you bought your spouse a two carat, yellow, vvs1, round cut diamond ring for $26,000 from http://www.bluenile.com/ for your 30th wedding anniversary. But who is Lolita, the Argentine firecracker, in Miami Beach? Does the old wifey know you sent her a $2,000 pair of diamond stud earrings? What?s it worth to you for me to keep mum on this? Maybe you should take a quick peak at http://www.divorcelawfirms.com/ and see what you?re in for?

Naw, I?m just pulling your leg. This is all just between friends, right? Think of it as a doctor/patient relationship. I?ll tell you what. See that leaderboard ad at the top of the page? Just click on that and we?ll call it even. Oooh that felt good! Click it again. Oh, baby! Not too many times. You?ll trigger my anti click fraud program.

Now you see that wide skyscraper add over on the right? Click on that too. Oh baby! Click it again! And there?s a little button ad at the bottom of the page. No, not that one. A little lower. What was that little cutie?s name in Miami again? Aaaaah.

Anyone who has any illusions about the Canadian tar sands business should take a look at the picture below. I?m not a fanatic, sandal wearing, organic bean sprout eating environmentalist, but just looking at it tells you that this is an eco-disaster of Biblical proportions.

A $50 billion investment by several firms over the last decade is now producing 750,000 barrels/day, and another $100 billion in capital is headed north. You have to cut down a whole forest, remove two tons of peat, then another two tons of sand, and burn 100 barrels of oil equivalent to heat rivers of water to steam, just to produce a single miserable barrel of oil.

This gives you the world?s highest production cost, thought to be $80-$100/barrel. There are now 50 square miles of sludge ponds in Northern Alberta leaching a witch?s brew of poisons into the water supply, which has caused the local cancer rate to explode tenfold. We?re not just talking about a few sick geese here.

Canada is the largest foreign supplier of oil to the US, accounting for 19% of our total, and half of that is coming from tar sands. The whole industry was built as a hedge against some Third World War, Armageddon type total cut off of all foreign crude supplies that would drive prices to $500/barrel, making all of this hugely profitable someday.

Maybe the owners think they can get away with this because it is in the middle of nowhere. An army of lawyers hitting these projects with a tidal wave of litigation think otherwise. This is the reason why environmentalist opposition to the Keystone pipeline was so acerbic. They view the tar sands as the world?s single largest source of greenhouse gasses. With North Dakota?s production expected to exceed total Canadian tar sands production by next year, and with challenges now arising from the seemingly endless new supply of cheap natural gas, the whole project may become redundant

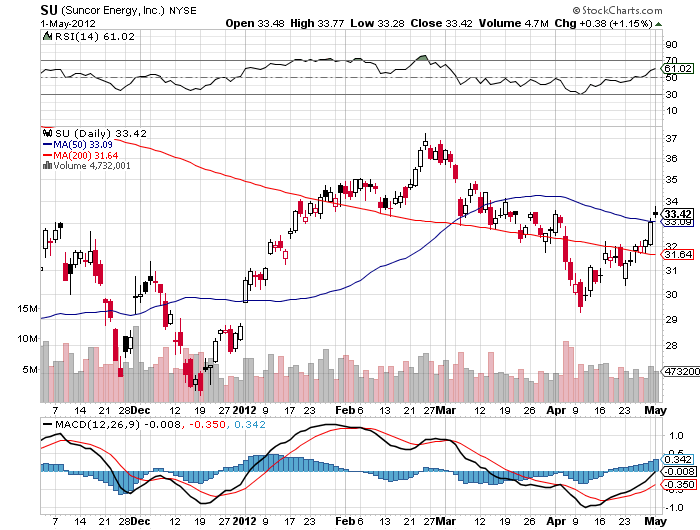

After looking at this picture and analyzing the numbers, you have to ask if it is really worth it, just so you can drive your Hummer to Wal-Mart. It all makes the future performance of major producer, Suncor Energy (SU), very suspect.