I am getting tired of the endless procession of perma bulls who keep insisting that, at a 14 times multiple, the S&P 500 is cheap. The last time I heard this was in 2000, when NASDAQ multiples went from 100 to 50, on their way to 10. Before that, it was in Japan in 1990, when multiples went from, guess what, 100 to 50 on their way to 10. Some 20 years later, Japanese multiples are still at a lowly 15.

When I first entered the stock business in the seventies, typical equity earnings multiples were in the seven to eight neighborhood. If you performed exhaustive stock screens, which then involved paging through endless reams of 10-k's, newsletters, and tip sheets printed in impossibly small type, you could occasionally find something at a two multiple, the kind Graham and Dodd wrote about. Anything over ten was considered outrageously overpriced, fit only to be sold on to retail investors. This is when the prime rate was at 6%.

The weakness we saw this week is consistent with my long term view that we are permanently downshifting from a 3.9% to a 2%-2.5% growth rate, and the lower multiples this deserves. I'm convinced that if the circuit breakers had not been installed, we would have been visited by another flash crash last week. If you look at a 30 year range of market multiples, it ranges from 10-22. Given our flaccid growth prospects going forward, I think the new range will be 10-16. It doesn?t make today's 14 multiple look like such a bargain.

Still missing in action from this economic recovery has been the residential real estate market. Everyone who is in the business of selling me a new home assures me that we have hit bottom and things are getting better, including the home builders, real estate agents, and countless local chambers of commerce. Look no further than home builder Lennar (LEN), which had more than doubled since the October low, and Pulte Homes (PHM), which has tripled.

Much of the improvement in bank shares, which saw Bank of America (BAC) double in three months, was based on the improving fortunes of homeowners. Is there something wrong with this picture? Should I be relying on these ?belief based? sources of information?

The hard data say otherwise. This morning, the January S&P 500 Case Shiller Real Estate Index put in a new seven year low, dropping 0.8% from the previous month. San Francisco showed the biggest loss (-2.5%), followed by Atlanta (-2.1%), Portland (-2.1%), Cleveland (-2.0%), and Chicago (-1.9%). Some 47% of transactions nationally are from short sales and foreclosures. This figure exceeds 60% in some troubled markets in the West. There is a foreclosure tidal wave of Biblical proportions now sweeping the South.

The cancellation rate for new purchases is still a stunningly high 30%. First time buyers have virtually ceased to exist, a key component of this market, as few young couples can qualify for bank loans under the new credit regime. They were once 40% of the market.

Who is buying all of these houses? Hedge funds, which are setting up partnerships to buy distressed homes at discounts of 25% or more, remodeling and modernizing them, and flipping them out as fast as they can. This presages a new institutionalization of the market that was once the refuge of the individual homeowners. I have heard of aggregations of as many as 1,000 units, which are individually bought at bankruptcy auctions on the courthouse steps, and moved as quickly as possible on an assembly line to the market.

While this may bring a welcome increase in turnover in a once moribund market, it will also cap any future price appreciation. These guys are not long term investors by any means. They are in for the quick buck, and will happily walk away with a net profit of only 5%. The money is made on the turnover. These resellers are successfully front running retail owners desperately trying to unload holdings from the vast shadow inventory where negative equity is more often the rule than the exception.

They say all real estate is local, and that has never been more true than now. Where you do find real end buyers is at the absolute top end, with prices listed at over $2 million. The players here often pay with cash to avoid the higher interest rates that usually come with jumbo loans. I am seeing this across the entire expanse of the economy, from American Express (AXP) to Coach (COH) to Tiffany (TIF).

I even see this at my local ski resort of Incline Village in Nevada, where homes over $10 million are moving nicely, but there is a constipated glut of hundreds of dwellings priced under $800,000. Right now, business is great for anyone selling to rich people. This is why we are seeing bidding wars in the San Francisco Bay area for any homes within commuting distance of Google (GOOG), Facebook, and Apple (AAPL) headquarters, while market for homes in the rest of the region is dead in the water.

I write all of this with the usual provisos. Case Shiller lags the real market by 3-5 months. There is no doubt that this year?s unusually warm winter has pulled forward a lot of real estate investment. Even still, the monthly data is taking a turn for the worse. March signed contracts are down -0.5%, while February housing starts were down -1.1%.

Why do I care about any of this, since I have been renting for the past seven years? It is hard to see the broader economy growing faster than 2% a year without serious real estate participation, which in the past has accounted for up to half of our total growth. It is the missing 2% that used to take us to 4% growth. That harsh reality affects all markets everywhere, whether you are renting or not.

The Fire Isn?t Out Yet

Since I am in the long term forecasting business, it was with some fascination that I caught the Associated Press report that minority children born this year may exceed Caucasian children for the first time. Whites lost their majority in San Francisco many years ago, and will do so in California as a whole in the near future.

The report said that the US will have a ?minority? majority by 2050. Whites now account for 2/3 of the population. While minorities now dominate only 10% of counties, they account for 40% of new births.

Demographers say the trend will be reinforced by a large number of Hispanic women entering their prime child bearing years, who historically have more children than other races. More white women are delaying childbearing, reducing fertility.

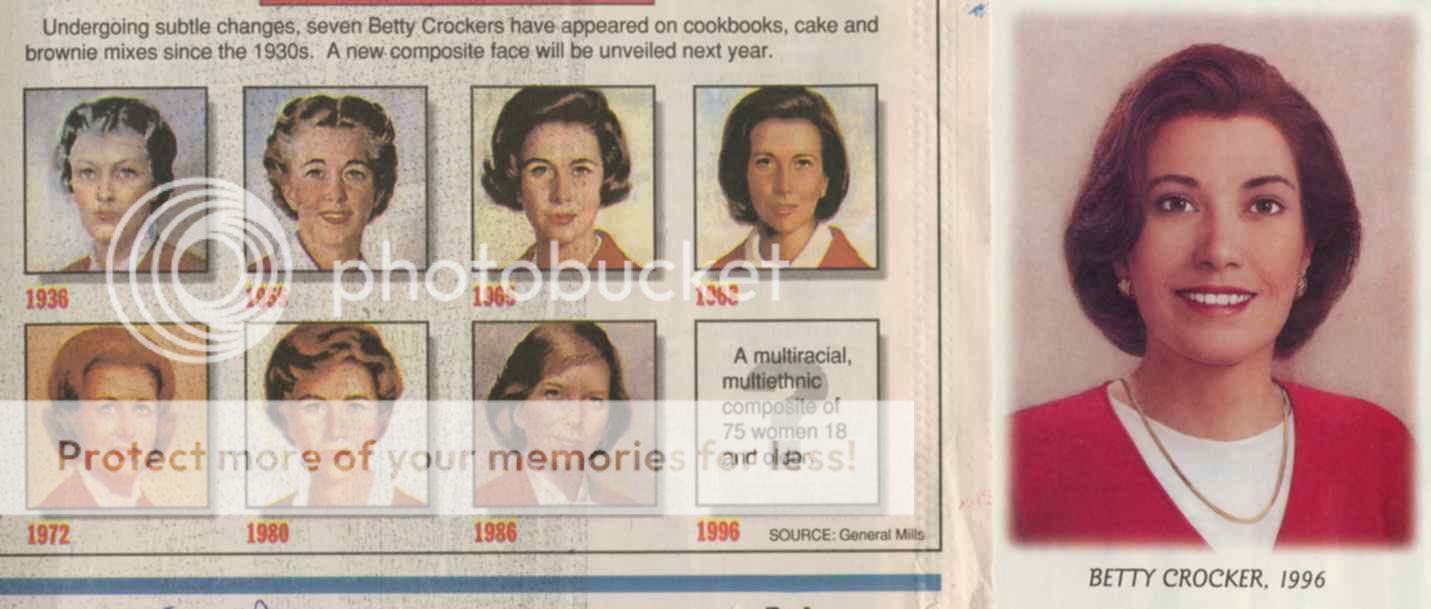

As demographics is destiny, this is bound to have huge political and economic ramifications for the country going forward. It is also going to influence the marketing priorities of corporations. 16 years ago, Betty Crocker anticipated this trend by using shorter, darker skinned models on the boxes of its cake mix boxes.

Companies that target specific ethnic groups are going to gain a competitive advantage. Furthermore, the rate of interracial mixing is accelerating at a tremendous rate. In California, 50% of all Chinese woman and 60% of Japanese women marry whites. This is amazing given that this was illegal until the Civil Rights Act was passed as recently as 1962.The young millennial generation are virtually color blind. Talk to them and you?ll see what I mean.

Genetically recessive blonde haired, blue-eyed people, who sprang out of a mutation in the Caucuses 7,000 years ago, may completely disappear in 200 years. Pure Caucasians themselves may eventually go too, as they only account for 15% of the world?s population, and that number is falling.

If you want to impress your friends with your vast knowledge of financial matters, then here are the Latin translations of the script on the backside of a US dollar bill.

?ANNUIT COEPTIS? means ?God has favored our undertaking.? ?NOVUS ORDO SECLORUM? translates into ?A new order has begun.? The Roman numerals at the base of the pyramid are ?1776.? The better known ?E PLURIBUS UNUM? is ?One nation from many people.?

The basic design for the cotton and linen currency with red and blue silk fibers, which has been in circulation since 1957, carries enough symbolism to drive conspiracy theorists to distraction. An all seeing eye? The darkened Western face of the pyramid? And of course, the number ?13? abounds.

Thank freemason Benjamin Franklin for these cryptic symbols, and watch Nicholas Cage?s historical adventure movie ?National Treasure.? The balanced scales in the seal are certainly wishful thinking and a bit quaint if they refer to the Federal budget. Study the buck closely, because there are soon going to be a lot more of them around.

What Did You Really Mean, Ben?

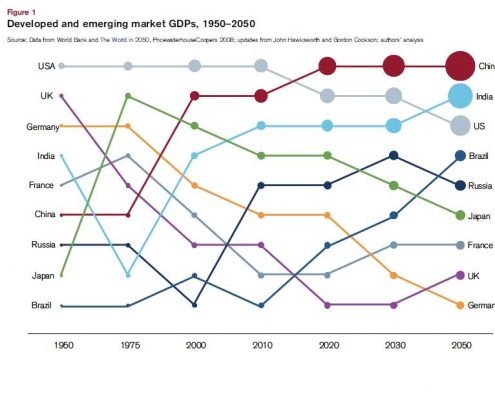

I love making very long term forecasts, because they give tremendous insights into the future of the global economy, and because at my advanced age, I won?t live long enough to see if I am right or wrong.

Check out the chart below which shows predicted GDP growth rates for a 100 year period from 1950 to 2050. It shows why you should be infatuated with emerging markets (EEM) like Brazil (EWZ), China (FXI), and India (PIN), lukewarm about the US (SPX), and avoiding Europe and Japan (EWJ) like the plague. It also gives the underlying argument behind my long term currency calls to stay short the yen.

The basic trade is to be long countries and currencies with high growth rates, and be short, or at least stay out of, countries and currencies with low growth rates. As exciting as this chart is, I really don?t see myself living another 38 years to 2050. But who knows? Isn?t 100 the new 80?

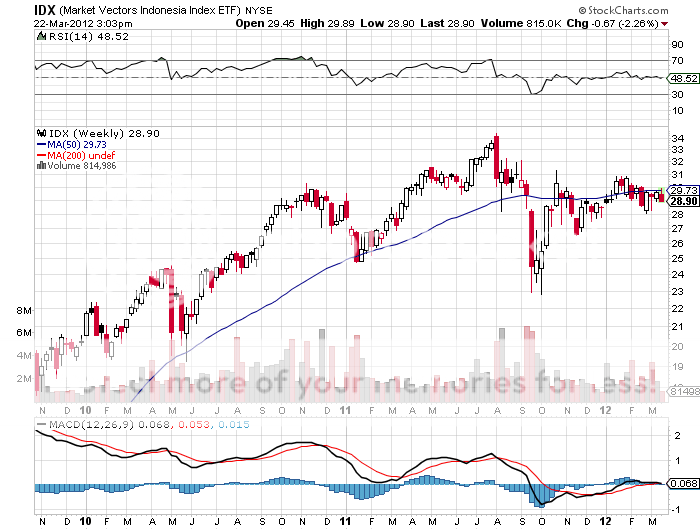

If you are looking for another emerging market to add to your list of things to buy on big dips, then take a look at Indonesia.

The world?s largest Muslim country offers a combination that I love, a population with great demographics that is also a major energy and commodities exporter. The archipelago is the biggest country in Southeast Asia and a huge exporter of oil and LPG to Japan on long term contracts. (An old friend of mine torched their Borneo fields at the beginning of WWII, and spent four years in a Japanese prison camp for his troubles.)

Other big exports include marvelous textiles, rubber, and increasingly rare tropical hardwoods. The global financial crisis only knocked their growth rate from 6.1% to 4.5%, and now it is back above 6%. No doubt, $63 billion of direct foreign investment into the country last year helped.

A series of tax reforms promise to keep the train moving, cutting the top corporate rate from 30% in 2008 to 28% in 2009, and 25% in 2010.? Wisdom Tree had the ?wisdom? to launch the country?s first ETF (IDX) close to a market bottom, a rare event indeed (what timing!), which became one of the best performers of 2009, rocketing over 300% from the lows to $60.

Islamic inspired terrorism is still a lingering concern. I keep Indonesia in the category of highly volatile, high risk, high return frontier markets that you only want to buy on a big dip. Keep it on your radar.

Expect to hear a lot about ignition in the next year. No, I don?t mean the rebuilt ignition for the beat up ?68 Cadillac El Dorado up on blocks in your front yard. I?m referring to the inauguration of the National Ignition Facility next door to me at Lawrence Livermore National Labs in Livermore, California.

Mention California to most people, and images of love beads, tie died T-shirts, and Birkenstocks come to mind. But it is also the home of the hydrogen bomb, which was originally designed amid the vineyards and cow pastures of this bucolic suburb. The thinking at the time was that if someone accidentally flipped the wrong switch, it wouldn?t blow up San Francisco, or more importantly, Berkeley.

The $5 billion project aims 192 lasers at a BB sized piece of frozen hydrogen, using fusion to convert it to helium and unlimited amounts of clean energy. The heat released by this process reaches 100 million degrees, hotter than the core of the sun, and will be used to fuel conventional steam electric power plants. There is no need for a four foot thick reinforced concrete containment structure that accounts for half the construction cost of conventional nuclear plants. The entire facility is housed in a large warehouse.

The raw material is seawater, and a byproduct is liquid hydrogen, which can be used to fuel cars, trucks, and aircraft. If this all sounds like it is out of Star Trek, you?d be right. I worked with these guys in the early seventies, back when math was used to make things, and before it was used to game financial markets, and I can tell you, there is not a smarter and more dedicated bunch of people on the planet.

If it works, we will get unlimited amounts of clean energy for low cost in about 20 years. Oil will only be used to make plastics and fertilizer, taking the price down to $10 for domestic production only. The crude left in the Middle East will become worthless. Lumps of coal will only be found in museums, or in jewelry, its original use. If it doesn?t work, it will melt the adjacent Mt. Diablo and take me with it. If you don?t get your newsletter tomorrow, you?ll know what happened. Now what is this switch for?

Until now, the country?s power grid has been divided into three unconnected chunks, making transnational transmission impossible, leading to huge regional mispricing. While California and New York suffered from brown outs and sky high prices, electricity was given away virtually for free in Texas.

A group of power companies is now proposing to build the $1 billion Tres Amigas superstation in Clovis, New Mexico that would connect all three grids. The plant would use advanced superconducting technology that will send five gigawatts of power down cables cooled at 300 degrees below zero. Construction is expected to begin this year and reach completion in 2014.

The facility would solve a major headache of alternative energy planners, and will no doubt accelerate development. It would allow the enormous wind farms on the drawing board in the Midwest to ship energy to the power hungry coasts. Ditto for the mega solar projects proposed in the Southwest deserts, and the big geothermal plants being built in Nevada.

With the Department of Energy having already sent tidal waves of government cash towards the sector, the timing couldn?t be better. With gasoline prices rapidly approaching $5 a gallon, some of these projects might now actually make some sense.

?We have 3,500 nuclear weapons left over from the cold war we don?t need, they take 20 seconds to re-aim, we?re not afraid to use them. And by the way, they?re already aimed at you.? That is the approach James Baker III thinks America should take with Iran, Ronald Reagan?s Chief of Staff and Secretary of the Treasury and George H.W. Bush?s Secretary of State.

At the same time we should be talking to the regime in Tehran, while doing everything we can to support the reformers, tighten sanctions, and enlist Europe?s help. Baker does not see a military solution in Iran, even though their potential to create instability in the region is enormous. This was one of dozens of amazing insights I gained chatting with the wily Texas lawyer during an evening in San Francisco.

Baker is happy to take on the ?America Bashers?, pointing out that the US still plays a dominant role in the UN, NATO, the IMF, and the World Bank. It accounts for 25% of global GDP, and its military is unmatched. The US spread globalization, and the spectacular growth of China and India is largely the result of open American trade policies, raising standards of living globally.

But the US can?t take its leadership role for granted. The biggest threats to American dominance are the runaway borrowing and entitlements. US debt to GDP will soar to over 100% in the near future, the highest level since WWII. This is unsustainable, is certain to bring a return of inflation, and unless dealt with, will lead to a long term American decline on the world stage.

Massive trade and capital flow imbalances also have to be addressed. The 82 year old ex-Marine, who confesses to being the only Treasury Secretary in history who never took an economics class, believes that the advantageous rates that the government now borrows at are not set in stone.

Baker is the man who engineered an end to the cold war with a whimper, and not a bang. He thinks that ?even our power has its limits,? and that there is a risk of strategic overreach.? With the US politically evenly divided, Congress has degenerated from debating teams into execution squads, and consensus is impossible. The media are partly to blame, especially bloggers who propagate wild conspiracy theories, as confrontation sells better than accommodation.

Regarding the financial crisis, we need to end ?too big to fail? and embark on re-regulation, not strangulation. All in all, it was a fascinating few hours spent with a piece of living history who still maintains his excellent contacts in the diplomatic and intelligence communities.