If you think that an energy shortage was bad, it will pale in comparison to the next water crisis. So investment in fresh water infrastructure is going to be a great recurring long-term investment theme.

One theory about the endless wars in the Middle East since 1918 is that they have really been over water rights.

Although Earth is often referred to as the water planet, only 2.5% is fresh, and three quarters of that is locked up in ice at the North and South poles.

In places like China, with a quarter of the world?s population, up to 90% of the fresh water is already polluted, some irretrievably so.

Some 18% of the world population lacks access to potable water, and demand is expected to rise by 40% in the next 20 years.

Aquifers in the US, which took nature millennia to create, are approaching exhaustion, especially in California?s Central Valley.

While membrane osmosis technologies exist to convert seawater into fresh, they use ten times more energy than current treatment processes, a real problem if you don't have any, and will easily double the end cost of water to consumers.?

While it may take 16 pounds of grain to produce a pound of beef,?it takes a staggering 2,416 gallons of water?to do the same. Beef exports are really a way of shipping water abroad in highly concentrated form.

The UN says that $11 billion a year is needed for water infrastructure investment and $15 billion of the 2008 US stimulus package was similarly spent.

It says a lot that when I went to the University of California at Berkeley's School of Engineering to research this piece, most of the experts in the field had already been retained by major hedge funds!

At the top of the shopping list to participate here would be the Guggenheim S&P Global Water Index ETF (CGW).

You can also check out the PowerShares Water Resources Portfolio (PHO), the First Trust ISE Water Index Fund (FIW), or the individual stocks Veolia Environment (VEOEY), Tetra-Tech (TTEK) and Pentair (PNR).

Bonus Question:? Which country has the world?s greatest water resources? Siberia, which could become a major exporter of H2O to China in the decades to come.

The New Liquid Gold?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/03/Waterfall.jpg283432Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-11-04 01:06:312016-11-04 01:06:31Why Water Will Soon Become More Valuable Than Oil

As a long term observer of America?s demographic picture, I was shocked to hear of a recent report from the US Census Bureau (click here for the website).

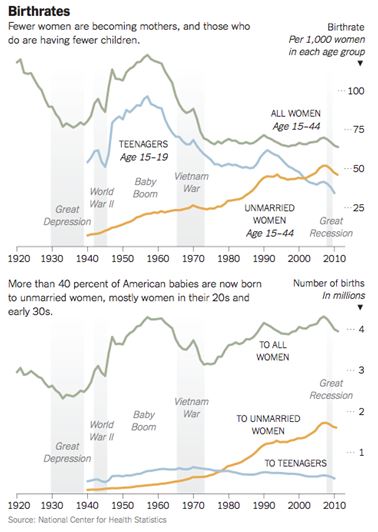

The US population grew by a scant 0.72% in 2012, the lowest since 1942.

You can?t start or expand a family when an essential partner in the process is off fighting WWII, and there were 17 million of them.

This is far below the 2.09% replacement rate that the country was holding on to only a few years ago.

At the end of 2012, there were 316,128,839 Americans. This accounts for 4.4% of the global population of 7,137,577,750, which was up 1.1%. If the growth rate remained the same, there are more than 317 million of us by now.

This places American population growth at the bottom of the international sweepstakes, down with Italy (0.32%), Germany (0.11%), and Poland (0.02%).

According to the World Bank, 22 countries suffered population declines, like Portugal (-0.29%) and Japan (-0.20%) (click here for the website).

The tiny Sultanate of Oman, one of my old stomping grounds as a military pilot, enjoys the planet?s highest growth rate at 9.13%.

The obvious cause here was the weakness of the US economy. There is a high correlation between economic health and fertility a year later.

So we can only hope that the modest improvement in the economy this year will send more to the maternity ward.

If it doesn?t, it could be great news for your investment portfolio. Fewer births today translate into a shortage of workers in 20 years. That brings rising wages, flying inflation, rapid price hikes, and a housing boom.

Corporate profits go through the roof, as does the stock market. It also produces fewer relying on government services in 40 years, which makes it easier for the government to balance the budget.

This Goldilocks scenario is already scheduled for the coming decade of the 2020s, when a 15-year demographic headwind flips to a tailwind, thanks to the coming demise of the ?baby boomer? generation, now a big cost to the economy.

The new data suggests that the next ?roaring twenties? could extend into the 2030?s and beyond.

California was the most populous state, with over 38 million, followed by Texas and New York. Two states saw population declines, Maine and West Virginia, where the collapse of the coal industry is sucking the life out of local businesses.

Parsing through the report, it is clear that prediction of population trends is becoming vastly more complicated, thanks to the increasinglyminestrone-like makeup of the US people.

By 2040 no single group will be a majority. That is already the case in San Francisco, and will be true for the entire State of California by 2020.

America will come to resemble other, much smaller multiethnic societies, like Singapore, South Africa, England, Israel, and Switzerland. This explains much about the current state of politics in the US.

Texas saw the greatest increase in population, with a jump of 387,397, to 26,020,000, as people flock in to take advantage of the big increase in local government hiring there.

Some 80% of new Texans were Hispanic and Black, confirming my belief that the Lone Star State will become the next battleground in presidential elections.

This is why gerrymandering (redistricting) is such a big deal there, with the white establishment battling to hang on to power at any cost.

Further complicating any serious analysis is the rapid decline of the traditional American nuclear family where married parents live with their children.

With a vast concentration of wealth at the top, and a long-term decline of middle class standards of living, this is increasingly becoming a luxury reserved for a prosperous elite.

As a result, the country?s birthrate has declined by half since 1960.

Those who do procreate are having fewer kids, the average family size dropping from three to two. In 1964, the final year of the baby boom, 36% of Americans were under the age of 18.

Today, that figure is just 23.5%, and is expected to fall to 21% by 2050. Only 80% of women have children now, compared to 90% in the 1970s.

One possible explanation is that the cost of child rearing has soared to $241,080 per child now. Rocketing college costs are another barrier, with 70% of high school grads at least starting some higher education.

I was a bargain as a kid, costing my parents only a tenth of that. I went to Boy Scouts and Little League baseball, each of which cost $1 a month. A full scholarship covered by college expenses.

When I look at the checks I have written for my own children for ski lessons, soccer, youth sailing, braces, international travel and assorted masters degrees, I recoil in horror.

Fewer women are following that old adage of ?marriage before carriage.? Some 41% of children are born out of wedlock, up 400% in 40 years.

It is definitely an education and class driven divide. Only 10% of college-educated mothers are still single, compared to 57% for those with a high school education or less.

It is a truism in the science of demographics that educated women have fewer children. It makes possible careers that enable them to bring home paychecks instead of babies.

Blame Roe versus Wade, the Equal Rights Act, and Title Nine, but every social reform benefiting women of the past half century has helped send the birthrate plummeting.

More women wearing the pants in the family hurts the fertility rate as well, as they are unable, or unwilling, to bear the large families of yore. The share of families where women are the primary breadwinners has leapt from 11% to 40% since 1960.

When couples do marry, they are sometimes of the same sex, now that gay marriage is legal in 16 states, further muddying traditional data sources. Some 2 million children are now being raised by gay parents. In fact, there is a gay baby boom underway, which those in the community call the ?gayby? boom.?

All female couples have produced one million children over the last 30 years, 95% of whom select blond haired, blue eyed, Aryan sperm donors who are over six feet tall ($40 a shot for donors if you guys are interested and live walking distance from UC Berkeley. I?m told that water polo players are particularly favored).

The numbers are so large that it is impacting the makeup of the US population.

There was a time when I could usually identify the people standing next to me on San Francisco BART trains. That time has long passed. Now I don?t have a clue.

Whenever we go to war, we become our enemy to a modest degree, both as a people and a culture.

After WWII, 50,000 German and 50,000 Japanese wives were brought home as war brides. Sushi, hot tubs and Volkswagens quickly followed.

The problem is that the US has invaded another 20 countries since 1945, and is now maintaining a military presence in 140. That generates a hell of a lot of green cards.

This has spawned sizable Korean, and later, Iranian communities in Los Angeles, a Vietnamese one in Louisiana, a Somali enclave in Minneapolis, and a large minority of Afghans in San Jose.

The fall of the Soviet Union in 1992 unleashed another dozen Eastern European ethnic groups and languages on the US. Have you noticed the proliferation of Arab fast food restaurants in your neighborhood since we sent 20 divisions to the Middle East?

What all this means is that the grand experiment called the United States is entering a new phase.

Different ethnic, racial, religious, and even political groups are blending with each other to create a population unseen in the history of the world, with untold economic consequences. It is also setting up an example for other countries to follow.

Get

your investment portfolio out in front of it, and you could prosper mightily.

Ignore Demographics at Your Portfolio?s Peril

https://www.madhedgefundtrader.com/wp-content/uploads/2014/10/Children-e1445627473511.jpg266400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-09-21 01:07:012016-09-21 01:07:01America?s Demographic Collapse and Your Stock Portfolio

On the right was my friend?s 1958 Ferrari Testa Rossa Scaglietta. On my left was a 1929 Dusenberg Murphy convertible sedan with a V-12 engine. I just walked past a 1914 Rolls Royce Silver Ghost Portholme Alpine Tourer.

Yes, it?s August in Pebble Beach, California, and that can only mean one thing. It?s time for another Concourse d? Elegance car show.

This is my annual opportunity to mix with my fellow 1%, hobnob with movie stars, and chitchat with the ultra wealthy, fanatically devoted to restoring ancient cars to pristine condition.

Held on the 18th fairway of the famed Pebble Beach golf course, Concourse d? Elegance has been held every year since 1950.

It was a largely local affair until the 1990?s, when wealth started concentrating at the top with a ferocious pace, minting billionaires by the hundreds.

Then the big-ticket sponsors started pouring in, turning it into a luxury global event.

Everywhere you look, you find promotions from Rolex, Flexjet, Davidoff Cigars, Osprey of London, Dom Perignon, and a dozen California vineyards. Every carmaker of note in the world is there in force.

Prices for anything the 1% bought skyrocketed accordingly, especially those for classic cars. Some of the price increases have been astronomical.

Comedian, Jay Leno, once told me that he was bid $10 million for a vehicle he paid $11,000 for during the early nineties. ?What has done better than that in the stock market,? he asked, ?Apple or Google??

Rich Europeans, Asians, and Australians now actually fly their cars to the event in the hope of snagging a much coveted ?Best in Show? prize.

Winners see the value of their ride double overnight as well as? the prestige that goes along with it. Even getting your car into the contest is a big deal. Of the 700 applications, only 200 cars were allowed to compete.

The 2014 prize went to a silver 1954 Ferrari 375MM Scaglietti Coupe, originally built for Italian neorealism filmmaker Roberto Rossellini, husband to the starlet, Igrid Bergman.

The car was owned by Robert Shirley, the former president of Microsoft, who carried out a loving, no expenses spared, ground up restoration after the car had been in pieces for 25 years.

I have to confess a personal weakness for this pastime, given my love of history, technology, and understanding manufacturing processes.

I was a member of the Rolls Royce Club in England for 20 years, and learned a lot about this very expensive hobby. The monthly newsletter used to run pieces on arcane topics, like ?How to Rebuild Your Phantom II Gearbox,? and ?Prewar Hydraulic Systems for Beginners.?

After a two-decade search, I decided not to buy one. Rolls Royce?s don?t appreciate that much, rising in value more or less with the rate of inflation. In other words, they are a lot like bonds.

Because they are so well made, 70% of those ever built are still running. You would have done much better investing in a prewar racing Bentley, or a postwar Ferrari racecar, if capital gains were your priority.

Besides, you don?t dare drive any of these masterpieces on public roads. Your insurance won?t cover it, and heaven help you if you get hit by someone driving while texting.

The other problem is that I am too big to fit into one. Vintage cars were designed when buyers were physically much smaller than today. Adjustable seats were a postwar invention, and I didn?t want to damage a vehicle?s historical integrity by drilling into the chassis to move the seat back.

Every year, the contest opens up special categories of vehicles to highlight certain marquees.

Last year saw classes for the Tatra, a bizarre, prewar Czechoslovakian company, and the Ruxton, a luxury car that disappeared during the Great Depression. Maserati was featured because of its 100-year anniversary.

Turn of the century steam cars were also a focus, a favorite of Jay Leno. The first car owned by a US president was a steam powered White Model M touring car that parked in front of the White House during the administration of William Howard Taft.

The auction house, Bonham?s, takes advantage of the Pebble Beach confab to hold its vintage car auction of the year, where record prices are often set.

Last year?s big earner was a 1962 Ferrari 250 GTO Berlinetta, which sold for $38 million, the highest prices ever paid for a car.

That beats the $30 million a 1954 Mercedes Benz W196 F1 sold for last year, a Grand Prix winner. Buyers? names are usually kept secret, for security reasons, or to avoid embarrassment (he paid what for that car?).

I spent a pleasant morning strolling around the historic links, bumping into old friends, talking technical details with the owners, and taking in the magnificent scenery of the California coast.

Some contestants really get into it, donning period dress to match the ages of their cars. So you?re constantly bumping into women wearing florid Edwardian hats, Art Deco dresses from the Roaring Twenties, or those killer stiletto heels from the fifties.

As for me, I was wearing a blue blazer and Panama hat favored by the judges, which seems to be timeless.

Reading the biographies of the judges was fascinating, and constitutes today?s automotive royalty.? They could be easily spotted with their telltale clipboards looking under hoods and going over every vehicle with a fine tooth comb.

Points are awarded for originality, authenticity and, of course, perfection. Extra kudos are awarded to those who rescue a historically significant vehicle from a barn, a junkyard, a forgotten garage, or an obscure museum. Some cars even had their original tool kits and jacks.

Owners stood back apprehensively.

The design chiefs of every major auto manufacture were there. So were heads of the major auto museums, like the Harrah?s collection in Reno, Nevada; the Mercedes Museum in Stuttgart; and the Petersen Automotive Museum in Los Angeles, created by the founder of Hot Rod and Motor Trend magazines.

A few racing legends were grading entries, including Sir Moss Sterling and Sir Jackie Stewart.

I had a dinner appointment with one judge, Franz von Holzhausen, who designed my Tesla Model S-1. But his wife had a baby that morning, so I dined with the head of production instead (more on that in a future piece).

If all of this appeals to you, the record sale price for a car is expected to be broken again next year. That?s when the actor Steve McQueen?s 1967 Ferrari 275 GTB/4 comes up for sale. Insiders say it should top $50 million.

I once owned McQueen?s home. Do you think it?s too early for me to get a bid in?

? ?Best of Show?

The Next Decade?s Mercedes

Check out This Cool Tatra

The Scenery is Magnificent

So, Which One is the Trophy?

A $38 Million Ride

This One Cost Only $30 Million

Out Of The Traffic Jam at Last!

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Ferrari-375-MM-Scaglietti-Coupe.jpg259428Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-08-22 01:06:322016-08-22 01:06:32Mixing with the 1% at Pebble Beach

While we?re all sitting on our hands waiting for Janet Yellen to make her move, or non move, it is time to reminisce.

My friend was having a hard time finding someone to attend a reception who was knowledgeable about financial markets, White House intrigue, international politics, and nuclear weapons.

I asked who was coming. She said Reagan?s Treasury Secretary George Shultz, Clinton?s Defense Secretary William Perry, and Senate Armed Services Chairman Sam Nunn.

I said I?d be there wearing my darkest suit, cleanest shirt, and would be on my best behavior, to boot.

When I arrived at San Francisco?s Mark Hopkins Hotel, I was expecting the usual mob scene. I was shocked when I saw the three senior statesmen making small talk with their wives and a handful of others.

It was a rare opportunity to grill high level officials on a range of top secret issues that I would have killed for during my days as a journalist for The Economist magazine. I guess arms control is not exactly a hot button issue these days. I moved in for the kill.

I have known George Shultz for decades, back when he was the CEO of the San Francisco based heavy engineering company, Bechtel Corp in the 1970's. I saluted him as ?Captain Schultz?, his WWII Marine Corp rank, which has been our inside joke for years.

Since the Marine Corps didn?t know what to do with a PhD in economics from MIT, they put him in charge of an anti-aircraft unit in the South Pacific, as he already was familiar with ballistics, trajectories, and apogees.

I asked him why Reagan was so obsessed with Nicaragua, and if he really believed that if we didn?t fight them there, we would be fighting them in the streets of Los Angeles.

He replied that the socialist regime had granted the Soviets bases for listening posts that would be used to monitor US West Coast military movements in exchange for free arms supplies. Closing those bases was the true motivation for the entire Nicaragua policy.

To his credit, George was the only senior official to threaten resignation when he learned of the Iran-contra scandal.

I asked his reaction when he met Soviet premier Mikhail Gorbachev in Reykjavik in 1986 when he proposed total nuclear disarmament.

Shultz said he knew the breakthrough was coming because the KGB analyzed a Reagan speech in which he had made just such a proposal.

Reagan had in fact pursued this as a lifetime goal, wanting to return the world to the pre nuclear age he knew in the 1930?s, although he never mentioned this in any election campaign.

As a result of the Reykjavik Treaty, the number of nuclear warheads in the world has dropped from 70,000 to under 10,000. The Soviets then sold their excess plutonium to the US, which today generates 20% of the total US electric power generation.

Shultz argued that nuclear weapons were not all they were cracked up to be. Despite the US being armed to the teeth, they did nothing to stop the invasions of Korea, Hungary, Vietnam, Afghanistan, and Kuwait.

I had not met Bob Perry since the late nineties when I bumped into his delegation at Tokyo?s Okura Hotel during defense negotiations with the Japanese. He told me that the world was far closer to an accidental Armageddon than people realized.

Twice during his term as Defense Secretary he was awoken in the middle of the night by officers at the NORAD early warning system to be told that there were 200 nuclear missiles inbound from the Soviet Union.

He was given five minutes to recommend to the president to launch a counterstrike. Four minutes later, they called back to tell him that there were no missiles, that it was just a computer glitch.

When the US bombed Belgrade in 1999, Russian president, Boris Yeltsin, in a drunken rage, ordered a full-scale nuclear alert, which would have triggered an immediate American counter response. Fortunately, his generals ignored him.

Perry said the only reason that Israel hadn?t attacked Iran yet, was because the US was making aggressive efforts to collapse the economy there with its oil embargo.

Enlisting the aid of Russia and China was key, but difficult since Iran is a major weapons buyer from these two countries.

His argument was that the economic shock that a serious crisis would bring would damage their economies more than any benefits they could hope to gain from their existing Iranian trade.

I told Perry that I doubted Iran had the depth of engineering talent needed to run a full scale nuclear program of any substance.

He said that aid from North Korea and past contributions from the AQ Khan network in Pakistan had helped them address this shortfall.

Ever in search of the profitable trade, I asked Perry if there was an opportunity in nuclear plays, like the Market Vectors Uranium and Nuclear Energy ETF (NLR) and Cameco Corp. (CCR), that have been severely beaten down by the Fukushima nuclear disaster.

He said there definitely was. In fact, he personally was going to lead efforts to restart the moribund US nuclear industry. The key here is to promote 5th generation technology that uses small, modular designs, and alternative low risk fuels like thorium.

I had never met Senator Sam Nunn and had long been an antagonist, as he played a major role in ramping up the Vietnam War. Thanks to his efforts, the Air Force, at great expense, now has more C-130 Hercules transport planes that it could ever fly because they were assembled in his home state of Georgia. Still, I tried to be diplomatic.

Nunn believes that the most likely nuclear war will occur between India and Pakistan. Islamic terrorists are planning another attack on Mumbai. This time India will retaliate by invading Pakistan. The Pakistanis plan on wiping out this army by dropping an atomic bomb on their own territory, not expecting retaliation in kind.

But India will escalate and go nuclear too. Over 100 million would die from the initial exchange. But when you add in unforeseen factors, like the broader environmental effects and crop failures (CORN), (WEAT), (SOYB), (DBA), that number could rise to 1-2 billion. This could happen as early as 2016.

Nunn applauded current administration efforts to cripple the Iranian economy which has caused their currency to fall 50% in the past two years. The strategy should be continued, even if innocents are hurt.

He argued that further arms control talks with the Russians could be tough. They value these weapons more than we do, because that?s all they have left.

Nunn delivered a stunner in telling me that Warren Buffet had contributed $50 million of his own money to enhance security at nuclear power plants in emerging markets.

I hadn?t heard that.

As the event drew to a close, I returned to Secretary Shultz to grill him some more about the details of the Reykjavik conference held some 30 years ago. He responded with incredible detail about names, numbers, and negotiating postures.

I then asked him how old he was. He said he was 94. I responded ?I want to be like you when I grow up?. He answered that I was ?a promising young man?. It was the best 63th birthday gift I could have received.

Oops, Wrong Number

https://www.madhedgefundtrader.com/wp-content/uploads/2013/03/George-Shultz.jpg313411Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-08-09 01:06:212016-08-09 01:06:21The Reception That the Stars Fell Upon

I?ll never forget when my friend, Don Kagin, one of the world?s top dealers in rare coins, walked into the gym one day and announced that he made $1 million that morning.? I enquired ?How is that, pray tell??

He told me that he was an investor and technical consultant to a venture hoping to discover the long lost USS Central America, which sunk in a storm off the Atlantic Coast in 1857, heavily laden with gold from the new state of California.

He just received an excited call that the wreck had been found in deep water off the US east coast.

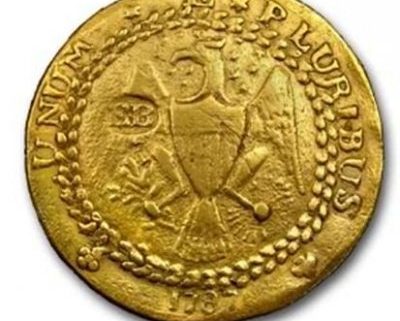

I learned the other day that Don had scored another bonanza in the rare coins business. He had sold his 1787 Brasher Doubloon for $7.4 million. The price was slightly short of the $7.6 million that a 1933 American $20 gold eagle sold for in 2002.

The Brasher $15 doubloon has long been considered the rarest coin in the United States. Ephraim Brasher, a New York City neighbor of George Washington, was hired to mint the first dollar denominated coins issued by the new republic.

Treasury secretary Alexander Hamilton was so impressed with his work that he appointed Brasher as the official American assayer.

The coin is now so famous that it is featured in a Raymond Chandler novel where the tough private detective, Philip Marlowe, attempts to recover the stolen coin.

The book was made into a 1947 movie, ?The Brasher Doubloon,? starring George Montgomery.

This is not the first time that Don has had a profitable experience with this numismatic treasure. He originally bought it in 1989 for under $1 million, and has made several round trips since then.

The real mystery is who bought it last? Don wouldn?t say, only hinting that it was a big New York hedge fund manager who adores the barbarous relic. He hopes the coin will eventually be placed in a public museum.

Who says the rich aren?t getting richer?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/07/Brasher-Doubloon-e1440346073108.jpg379400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-07-13 01:06:442016-07-13 01:06:44The Mystery of the Brasher Doubloon

The San Francisco Bay area?s beleaguered renting class moaned again when the social media giant, Twitter (TWTR) finally went public a couple of years ago.

The deal immediately placed $1.82 billion into the pockets of early shareholders, almost all of whom live near the company?s San Francisco headquarters.

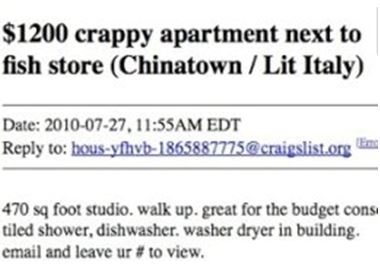

This is adding insult to injury to those in the region who are desperately seeking a home. San Francisco already has the most expensive rentals in the country.

The median rent for a modest two-bedroom apartment in a marginal neighborhood with poor access to public transit and no view is $4,500 a month.

Forget about it if you smoke, have a pet, or suffer from a poor credit rating. That compares to $3,150 a month in New York City, $2,300 in Boston, and $2,250 in Los Angeles.

This is just the latest tsunami of cash to hit the city?s torrid real estate market. Since 1998, Apple (AAPL) has created $700 billion in equity for shareholders, while Google (GOOG) has manufactured a further $450 billion.

In 2012 Facebook (FB) joined their ranks with a $100 billion IPO that quickly went sour. What is hoody wearing Mark Zukerberg?s creation worth today? A stunning $339 billion.

The first thing these newly enriched entrepreneurs do is buy a nice big house. This is not just limited to founding technology nerds and geeks wearing hoodies.

During the early start up days of these cash starved companies, shares are handed out to employees in lieu of better pay, all the way down to the secretary level. When they go public, thousands of millionaires are created and not a few billionaires.

Presto! A housing bubble!

Renters are getting creative in dealing with the high prices. Some are doubling up the use of bedrooms. Others rent out their beds during the day to programmers who often prefer working all night, much like hot sheet hotels of old.

Many have moved into the garage and sleep with the business they are trying to develop. Some homeowners with yards are leasing out spaces to pitch tents, while others are taking advantage of new services on the internet that allow them to rent spare rooms by the night.

There is no way of telling how far this will go. The last technology bubble popped when price earnings multiples hit 100. Most established tech firms are now trading in the 11-18 range, so the day of reckoning could be quite a ways off. Rentals could reach the astronomical levels now seen in London and Hong Kong.

In the meantime, I?m thinking of renting out my tool shed in the garden. My agent says that I could get at least $1,000 a month. The alternative is for home seekers to move to Las Vegas, where they can get a larger two bedroom without the need for heating for only $900 a month.

Do you think it is worth the commute?

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/Bedroom.jpg302396Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-06-10 01:06:252016-06-10 01:06:25San Francisco?s Suffering Renters Take Another Hit

I have reported in the past on the value of the Friday-Monday effect, whereby the bulk of the year's performance can be had through buying the Friday close in the stock market and then selling the Monday close (click here for ?The Friday-Monday Effect Exposed?).

Well, I have discovered a further distillation of this phenomenon. During 2010, the S&P 500 rose by 143 points. Some 134 points of this was racked up on the first trading day of each month, some 12 days in total. That is 94% of the entire return for the year.

I can see where this is coming from. Many pension and mutual funds are completely devoid of any real trading expertise. So they rely on a 'dumb' dollar cost averaging models to commit funds. In a rising market, like we had for most of last year, this produces an ever rising average cost.

More than a few hedge funds have figured this out, front run these executions at the expense of the investors of the other institutions. And you wonder why the public has become so disenchanted with their financial advisors.

The possibilities boggle the mind. Imagine strolling into the office on the last trading day of each month and committing your entire capital line. You then spend the night hoping that a giant asteroid doesn't destroy the earth.

You return to your desk at the next day's close, unload everything, and take off on a 30-day vacation. Every month, you come back for a reprise. At the end of the year you top the performance leagues, and retire richer than Croesus.

It sounds like a nice 12 day work year to me!

Is It Time to Trade Yet?

https://www.madhedgefundtrader.com/wp-content/uploads/2013/10/Man-Sleeping-on-Couch-e1439472331201.jpg266400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-06-03 01:06:292016-06-03 01:06:29The Twelve Day Year

When you look at the profusion of new ETF?s being launched today, you find that they almost always correspond with market tops.

The higher the market, the greater the demand for the underlying, and the more leverage traders pay for it. The resulting returns for investors are disastrous.

But occasionally a blind squirrel finds an acorn, and if you fire buckshot long enough, you hit a barn.

That?s why I am getting interested in the ProShares Short High Yield ETF (SJB). After riding the bull move in junk all the way up with (JNK), (HYG), I have recently turned negative on the sector.

Junk bonds have moved too far too fast. Current spreads for junk paper are now only 200 basis points over equivalent term Treasury bonds, and investors at these levels are in no way being compensated for their risk.

If the stock market starts to roll over this summer, then the junk bond market will follow it in the elevator going down to the ladies underwear department in the basement.

Keep in mind that when shorting the junk market, you run into the same problem you have with the (TBT), a leveraged short ETF for the Treasury bond market.

Buy the (SJB) and you are short a 6.74% coupon, which works out to a monthly costs of more than 50 basis points. That is a big nut to cover. So timing for entry into this fund will be crucial.

Is Shorting Junk Bonds the Way to Go??

https://www.madhedgefundtrader.com/wp-content/uploads/2013/05/Car-Junk.jpg225322Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-22 01:07:422016-04-22 01:07:42Take a Ride in the Short Junk ETF

My former employer, The Economist, once the ever tolerant editor of my flabby, disjointed, and juvenile prose (Thanks Peter and Marjorie), has released its ?Big Mac? index of international currency valuations.

Although initially launched by an imaginative journalist as a joke three decades ago, I have followed it religiously and found it an amazingly accurate predictor of future economic success.

The index counts the cost of McDonald?s (MCD) premium sandwich around the world, ranging from $7.20 in Norway to $1.78 in Argentina, and comes up with a measure of currency under and over valuation.

What are its conclusions today? The Swiss franc (FXF), the Brazilian real, and the Euro (FXE) are overvalued, while the Hong Kong dollar, the Chinese Yuan (CYB), and the Thai Baht are cheap.

I couldn?t agree more with many of these conclusions. It?s as if the august weekly publication was tapping The Diary of the Mad Hedge Fund Trader for ideas.

I am no longer the frequent consumer of Big Macs that I once was, as my metabolism has slowed to such an extent that in eating one, you might as well tape it to my ass. Better to use it as an economic forecasting tool, than a speedy lunch.

The Big Mac in Yen is Definitely Not a Buy

https://www.madhedgefundtrader.com/wp-content/uploads/2011/12/mcdonaldsJapan.jpg240320Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-04-07 01:08:232016-04-07 01:08:23Where The Economist ?Big Mac? Index Finds Currency Value

Apple holders (AAPL) were ecstatic and even apoplectic when they heard that their beloved company would be joining the Dow Average last year.

The move required thousands of portfolio managers to add Apple to their portfolios, like the $32 billion worth of Dow index managers, whether they wanted to or not. From then on it would be illegal for them not to own Apple.

At the very least it put the fear of Jobs into moneymen everywhere, especially if the Dow is the benchmark they are measured against.

The world?s now second largest listed company replaced tired and flagging AT&T (T), one of my perennial favorite short positions.

The symbolism couldn?t be more evident. A former monopoly with a literally rusting infrastructure is getting booted for iPhones, iPads, iTunes, Apps and the Cloud. Oh, how the mighty have fallen.

AT&T was one of the oldest Dow stocks, joining the closely followed index in 1916. The new listing then had a symbolic move of its own, taking place the year after the first-ever transcontinental telephone call was placed.

Who made that call? Alexander Graham Bell in New York telephoned his former assistant, Thomas Watson, in San Francisco in a replay of the first phone call in history 50 years earlier in 1876, from room to room at their lab. ?Mr. Watson, come here, I want to see you,? the first words ever uttered on a phone line, were repeated once more.

AT&T, or ?Ma Bell? as it was known, lost its listing in 2004 after it merged with SBC Communications. It was reinstated a year later when the new firm?s name was changed back to AT&T.

However, Apple shareholders should be careful what they wish for.

There is not exactly a great track record for share price performance after a company joins the Dow, especially a technology stock.

In 1999, Microsoft (MSFT) fell 43% after becoming a Dow 30 stock, while Intel (INTC) shed 52%. Cisco Systems (CSCO) lost 16% after joining the club in 2009.

The problem is that Apple entered the index after a meteoric 18 month, 130% run up. So the Dow, having missed the rise in Apple on the upside, fully participated on the downside in the stock meltdown that followed.

Apple is the second largest component in the Dow, with a hefty $575 billion market capitalization. This means that future Dow corrections will be bigger and more ferocious than they would have been without Apple and with boring AT&T.

The volatility of the lead index has just gone up, a lot.

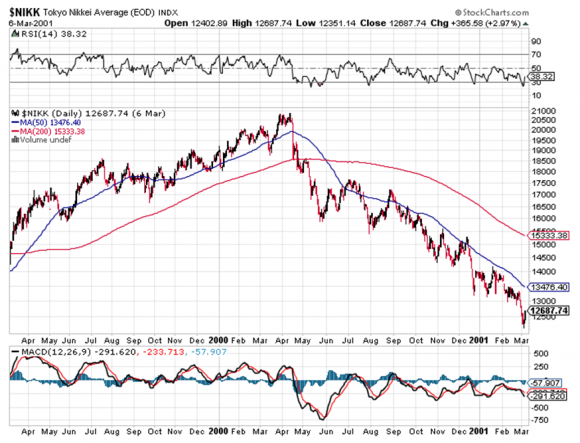

I remember too well that the Japanese made a similar blunder in 2000. The government wanted to have a national stock index that reflected the economy of the future, not of the past.

They had watched with great envy America?s NASDAQ hog the global spotlight, soaring from 1,000 to 5,000 in just a couple of years.

So what did these geniuses do? They reconstituted the Nikkei Average from a 90% boring industrial, 10% technology index to a 50/50 weighting. And they did this mere weeks after NASDAQ peaked!

As a result, the Nikkei Average got the stuffing knocked out of it in the dotcom collapse. It fell a stunning 15% in the week just after the reconstitution announcement. It cratered from 21,000 to eventually bottom at 7,200. Without the reconstitution, it would have sold out at 10,000.

Having missed the dotcom boom on the upside, the Nikkei fully participated on the downside. Apple shareholders please take note.

Apple?s rise was amply chronicled by a steady series of Trade Alerts in this newsletter.

You can go back to my 2012 prediction that Apple would soar from $485 to $1,000 (click here). On a split adjusted basis we? already reached $931.

I followed that up with ?Apple is Ready to Explode? in October, 2013 (click here), when the post split share price was back at $70.

Indeed, I have issued more Trade Alerts to buy Apple over the seven-year life of this newsletter than any other single name.

It looks like I will be issuing a lot more Apple Trade Alerts in the near future as well.

Guess When the Index Reconstitution Took Place?

https://www.madhedgefundtrader.com/wp-content/uploads/2015/03/Apple-Watch.jpg221398Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-03-07 01:06:152016-03-07 01:06:15What Happened When Apple Entered the Dow?

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.