Getting You Bang per Buck with Alexion Pharmaceuticals

Since nobody can actually control when to get sick or what type of disease to acquire, it makes absolute sense that biotech stocks remain one of the wisest bets if you want to put your hard-earned cash to work.

The question, therefore, is what are the best biotech stocks to buy now?

Looking at the biotechnology stock prices today, I can say that Alexion Pharmaceuticals (ALXN) will give you the most bang for your buck.

For over a decade, this ultra-rare-disease biotechnology company had been regularly valued at roughly 22 to 67 times its cash flow and frequently well above 30 times forward EPS.

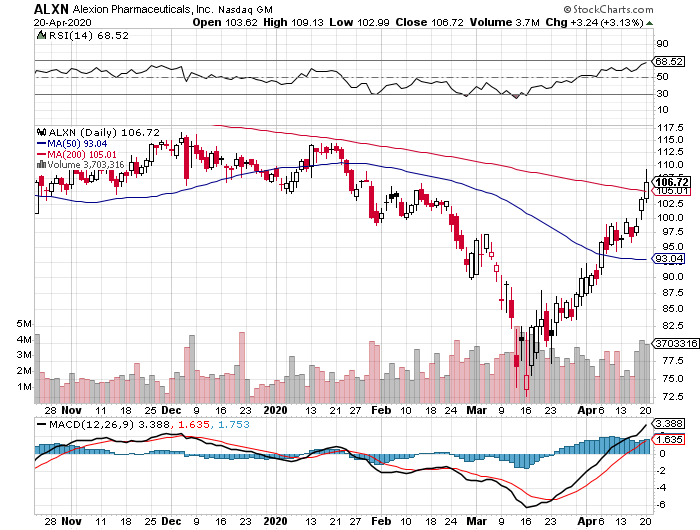

Now, you can buy this top biotech stock for less than eight times its Wall Street profit consensus in 2021 and 10 times its cash flow for next year as well. It definitely doesn’t hurt that its PEG ratio is less than 1, categorizing it as an “undervalued” stock today.

However, its attractive pricing isn’t the only thing that’s putting Alexion in the news these days as this biotech company has been active in the race to find a coronavirus cure since early February.

When news about the pandemic broke, Alexion decided to repurpose its rare chronic blood disease bestseller Soliris as a potential COVID-19 treatment since the drug showed promising results on patients with severe pneumonia or acute respiratory distress syndrome.

Alexion’s efforts have been quite promising so far, with the biotech company targeting to commence a Phase 2 study of Soliris within the month. What we know so far is that this experiment will involve 10 patients as part of the proof-of-concept trial.

Apart from Alexion, other top biotech companies repurposing old drugs in search of a COVID-19 cure are Gilead Sciences (GILD) with Remdesivir, Roche (RHHBY) with Actemra, and Regeneron (REGN) and Sanofi (SNY) with Kevzara.

Outside its coronavirus treatment efforts, Alexion actually prides itself on a promising pipeline. To date, three treatments are projected to turn into blockbusters soon.

The first is Strensiq, which is formulated to treat a rare disease commonly known as hypophosphatasia. Patients with this disorder have an enzyme deficiency, making them unable to properly process calcium and phosphorus. As a result, they end up with malformed bones and teeth.

The second treatment is Kanuma, which is for patients suffering from lysosomal acid lipase (LAP) deficiency. People with this condition lack a key enzyme, preventing them from effectively breaking down fats.

Both conditions are extremely rare. Hypophosphatasia affects only 1 in 100,000 people while LAP is suffered by 1 in 40,000 individuals.

The third treatment is Ultomiris, which is widely regarded as Soliris’ successor.

For years, Soliris has been Alexion’s major moneymaker. However, uncertainties on the company’s hold on its patent exclusivity have started to shake investors’ faith in this stock. With one of Soliris’ key patents set to expire in 2021, the biotech company has to brace itself for the onslaught of generic competition.

This is where Ultomiris comes in.

Alexion has been busy migrating its customers to opt for Ultomiris before Soliris’ key patent expires.

To make this offer enticing, the biotech company has priced the newer drug to be slightly cheaper than the old blockbuster. Ultomiris costs $458,000 while Soliris is priced at $500,000.

To sweeten the deal further, the newer treatment is only required once every eight weeks. In comparison, Soliris’ treatment schedule is bi-monthly.

Basically, it’s as if Alexion has effectively restarted the clock in its patent exclusivity on this ultra-rare disease indication. The company aims to convert at least 70% of its users by mid-2020.

From a financial point of view, Alexion is performing quite well. Its fourth-quarter report showed that the company earned $1.4 billion in revenues, demonstrating a 23% increase from the same quarter in 2018.

Meanwhile, it raked in $5 billion in full-year sales for 2019. This indicated a 21% jump from its relatively paltry sales of $4.1 billion.

Looking at the metrics, Alexion is one of the surprisingly cheap stocks considering its growth. It also has the added bonus of dominating its chosen ultra-rare disease space.

This is typically a good strategy to avoid competition while also being able to seek high price points for its innovative treatments. The fact that insurers generally cover these treatments all but guarantees that Alexion is secure in terms of cash flow predictability.

Despite the panic induced by the coronavirus market, investing opportunities are everywhere --- if you know where to look.

Alexion is a solid company with strong growth prospects and is selling at a reasonable price. Any opportunistic investor worth his salt would know that this is the ideal time to strike.