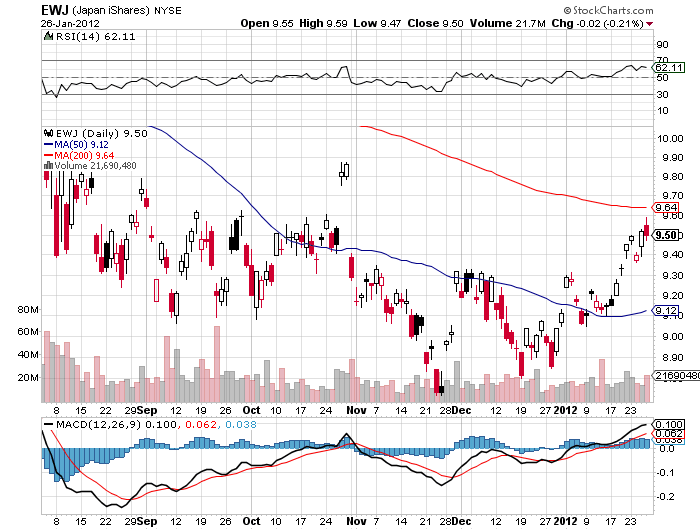

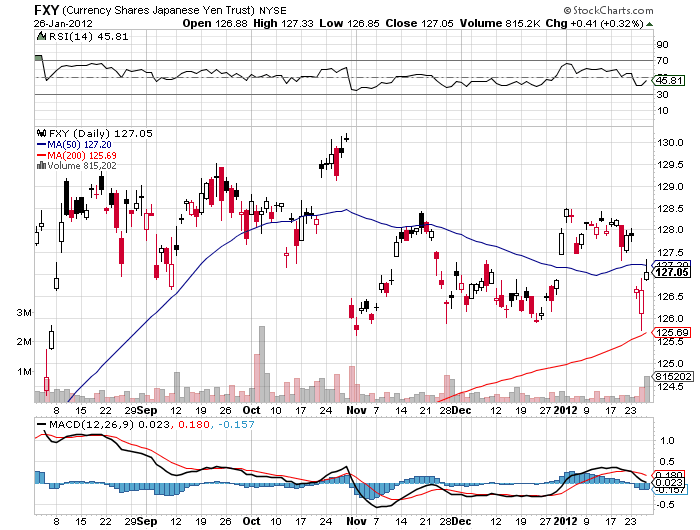

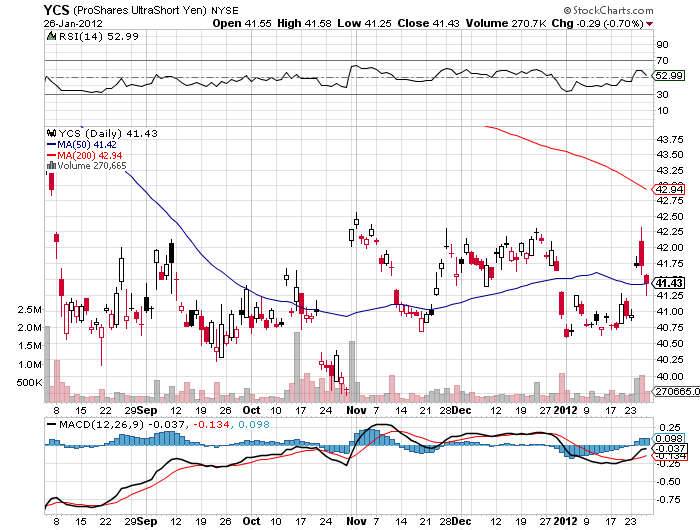

Is This the Chink in Japan?s Armor?

?Oh, how I despise the yen, let me count the ways.? I?m sure Shakespeare would have come up with a line of iambic pentameter similar to this if he were a foreign exchange trader. I firmly believe that a short position in the yen should be at the core of any hedged portfolio for the next decade, but so far every time I have dipped my toe in the water, it has been chopped off by a samurai sword.

I was heartened once again this week when Japan?s Ministry of Finance released data showing that the country suffered its first annual trade deficit since 1980. Specifically, the value of imports exceeded exports by $39 billion. Japan still ran healthy surpluses with the US and Europe. But it ran a gigantic deficit with the Middle East, its primary supplier of energy.

You can blame the March tsunami and the Fukushima nuclear meltdown that followed for much of this. Japan depended on nuclear power for 25% of its electric power generation, and since then the number of operating plants has been cut from 54 to just 5. Conventional plants powered by oil and LNG have had to make up the difference, causing a surge in imports. Crude?s leap from $75/barrel in the fall to $100 made matters worse.

It also hasn?t helped that Japan has offshored much of its low end manufacturing to China over the last 30 years, as America has done. Exacerbating the problem were the Thai floods, which caused immense supply chain problems, further eroding exports.

To remind you why you hate all investments Japanese, I?ll refresh your memory with this short list of the other problems bedeviling the country:

* With the world?s weakest major economy, Japan is certain to be the last country to raise interest rates.

* This is inciting big hedge funds to borrow yen and sell it to finance longs in every other corner of the financial markets.

* Japan has the world?s worst demographic outlook that assures its problems will only get worse. They?re not making Japanese any more.

* The sovereign debt crisis in Europe is prompting investors to scan the horizon for the next troubled country. With gross debt exceeding 200% of GDP, or 100% when you net out inter-agency crossholdings, Japan is at the top of the hit list.

* The Japanese long bond market, with a yield of 0.98%, is a disaster waiting to happen.

* You have two willing co-conspirators in this trade, the Ministry of Finance and the Bank of Japan, who will move Mount Fuji, if they must, to get the yen down and bail out the country?s beleaguered exporters.

When the big turn inevitably comes, we?re going to ?100, then ?120, then ?150. That could take the price of the leveraged short yen ETF (YCS), which last traded at $41.43, to over $100.? But it might take a few years to get there. The fact that the Japanese government has come on my side with this trade is not any great comfort. Many intervention attempts have so FAR been able to weaken the Japanese currency only for a few nanoseconds.

If you think this is extreme, let me remind you that when I first went to Japan in the early seventies, the yen was trading at ?305, and had just been revalued from the Peace Treaty Dodge line rate of ?360. To me the ?78 I see on my screen today is unbelievable.

Noted hedge fund manager Kyle Bass says he is already in this trade in size. All he needs for it to work is for Japan to run out of domestic savers essential to buy the government?s domestic yen bond issues, who have pitifully had sub 1% yields forced upon them for the past 17 years. Then the yen, the bond market, and the stock market all collapse like a house of cards. Kyle says that could happen as early as the spring.

It?s All Over For the Yen