May 15, 2023

(MAY 10, 2023, WEBINAR SUMMARY)

May 15, 2023

Hello everyone,

Welcome to a new week.

I hope Mother’s Day celebrations went well. Traditionally, you gave your mother a white flower on Mother’s Day to thank her for all she did. Now, it’s become commercialised. I still love the white flower sentiment. It’s simple and refined and repels the commercial taint that has become ubiquitous.

So, this Post will be a summary of John’s latest webinar, which was conducted last week on May 10, 2023.

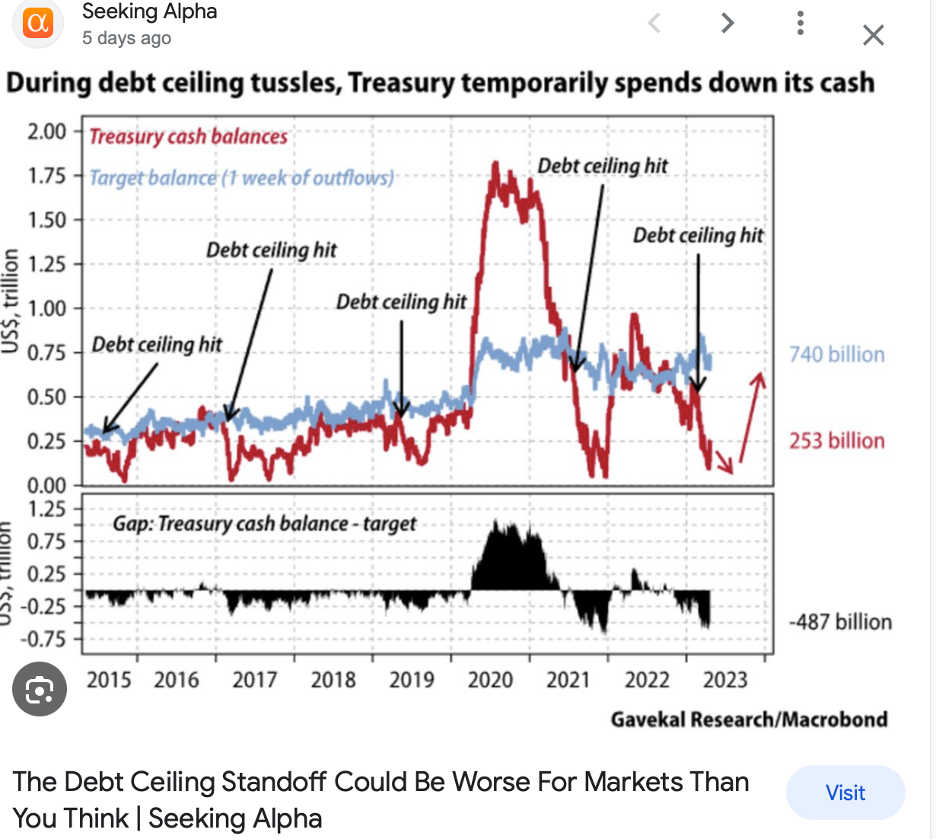

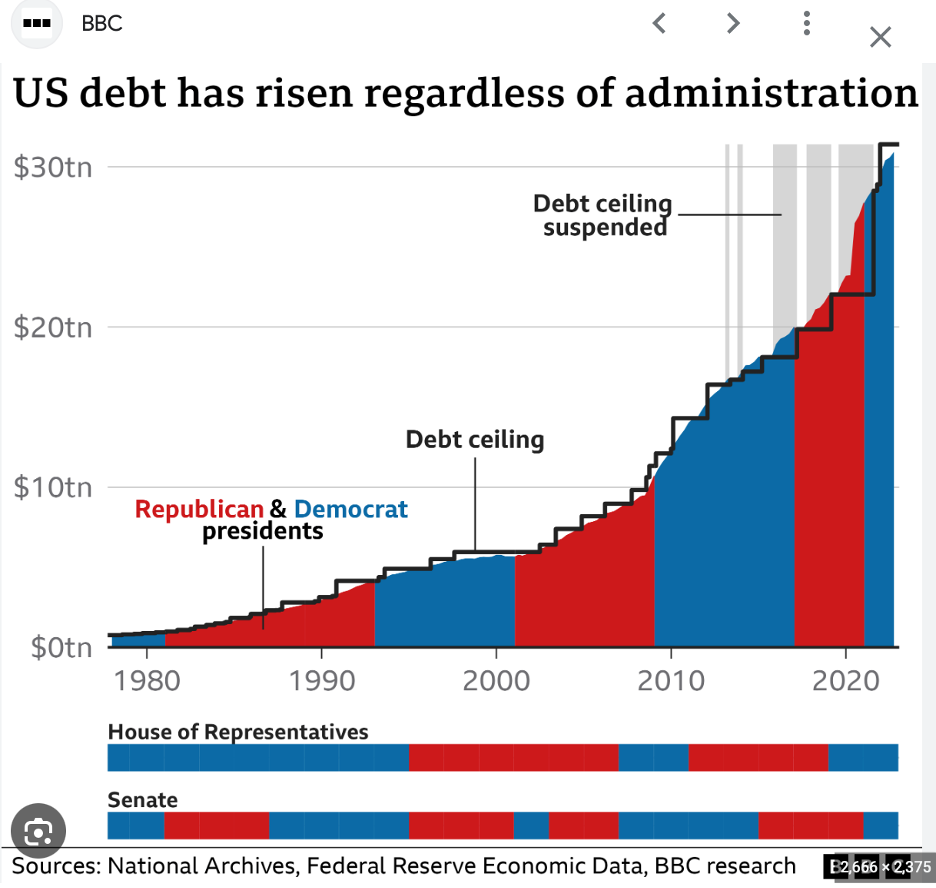

TITLE: DEBT CEILING DEBACLE

Lunches

May 16 Key West Strategy Luncheon

May 18 Tampa, Florida

May 19 Boca Raton, Florida

July 6 New York

July 13 Seminar at Sea On Queen Mary II

July 19 London

Trade Alert Performance:

40 out of 43 trade alerts are profitable

March 20.85%

April 15.13%

May to date 0.75%

2023 year to date 61.76%

120.45% trailing one-year return

48.86% average annualized return

Debt ceiling debacle has frozen all markets driving volatility to 2-year lows at $15.

Trading volumes shrinking by the day.

Summer will present the best buying opportunity of the year.

Precious metals and commodities should be at the top of the “BUY” list to cash in on an economic recovery.

Be patient. Let the market come to you.

ADVICE: Take a look at Schwab LEAPS.

The Global Economy- Hard, Soft, Hard, Soft

Fed raises rates 0.25%. is this the last move this cycle and is this the last move up in the next two years?

Non-farm payrolls jump by 253,000. Unemployment rate jumped by 3.4% suggesting rate hikes are to come. (Perhaps the Fed is looking at the wrong numbers as AI is creating jobs faster than the Fed can create unemployment by raising rates and making everything expensive and unaffordable for many)

Fed Financial Stability Report highlights risk to the economy.

Tightening of bank lending is a concern, so is commercial real estate with elevated valuations.

Europe ekes out 0.1% growth in Q1 versus a 1.1% rate for the U.S.

New car loans are in free fall. Collateral damage from the regional banking crisis, hastening a coming recession.

Stocks – Dead Weight – Debt Ceiling

The Regional Banking crisis spreads with Phoenix Bank Western Alliance Bancorp (WAL) down a staggering 65% on the week.

Consensus (SPY) earnings are currently $220 a share giving expensive price/earnings multiple of 18.77x.

According to John, you only need to buy 7 stocks this year. Apple, Amazon, Google, Meta, Nvidia, and Salesforce.

All technical are now flashing red. Seasonals are now turning strongly against stocks.

Volatility plunges to $15 putting the market to sleep.

First half flat, second half strong to take us to 4,800 by year-end.

QUESTION: Is it too late to buy LEAPS?

Two Year LEAPS are a good bet.

Big tech – all in LEAP territory – 1-2 years out.

Netflix – LEAP candidate – 1 year LEAP

Nvidia – John’s advice – try a 300-310 LEAP one year out.

Commodities in free fall – stocks have been slaughtered.

US Steel (X) – 2-year LEAP at the money

BONDS

Bonds back in buy territory.

Bonds are showing default fears. Yellen warns of economic catastrophe if debt ceiling is not raised.

10-year yields back to up 3.55%

Keep buying 90-day T-bills – now pushing 5.2% risk-free yield.

Still looking like 2.5% yield by end of 2023.

Keep buying TLT calls, call spreads, and LEAPS on dips.

Junk bonds ETF – JNK and HYG are great high-yield plays.

FOREIGN CURRENCIES

WEAK US$. Will accelerate on any debt default. Any strength in the dollar will be temporary. Look for new lows in the dollar by the end of 2023.

Buy FXE, FXY, FXB, FXA on dips.

ENERGY AND COMMODITIES

The Oil collapse is signaling a recession, as is weakness in all other commodities, even Lithium.

Widespread EV adoption is finally making a big dent, as are the price wars there. Buy USO on dips as an economic recovery play.

Buy Caterpillar (CAT)

UNG – 2-year LEAP territory

FCX - LEAP territory – John expects this stock to be around $100 in two years.

PRECIOUS METALS

Chile nationalizes the Lithium industry, sending (SQM) and (ALB) into a tailspin. The official reason for this was to make the industry more efficient.

The real reason is so the government can spin off the profits in this exploding industry.

Child is the world’s second largest producer of lithium, which is essential for EV batteries.

Gold is headed for $3000 by 2024. It’s resting now.

The new drivers are the soon-to-be falling interest rates and the current winter season in crypto.

Russia and China are also stockpiling gold to sidestep international sanctions. A severe short squeeze in copper is developing leading to a massive price spike later in 2023.

REAL ESTATE

Home prices are still rising, even in worse-hit markets, like San Francisco.

Pending Home Sales plunge 5.2%

New Home sales pop to 683,000

S&P Case Shiller Rises 2% in February – the first time in 9 months.

Investors are trying to front-run the next leg of the bull market in residential real estate, which should start when interest rates plunge at year-end.

Wishing you all an extraordinary week.

Cheers,

Jacque

We don’t stop playing because we grow old.

We grow old because we stop playing.

UNKNOWN