Global Market Comments

August 8, 2019

Fiat Lux

Featured Trade:

(HOW TO KNOW IF THE BULL MARKET IS WELL AND TRULY OVER),

(THE TALE OF TWO ECONOMIES),

(FB), (AAPL), (AMZN)

Global Market Comments

August 8, 2019

Fiat Lux

Featured Trade:

(HOW TO KNOW IF THE BULL MARKET IS WELL AND TRULY OVER),

(THE TALE OF TWO ECONOMIES),

(FB), (AAPL), (AMZN)

I have lately been besieged with emails from followers asking if they should sell everything, put all their money into cash, and if the great bull market is well and truly over.

My answer is the same to all. If a full-throated and affirmative “NOT YET”. Things may look scary now, but they could get a lot worse, and eventually, that will take place.

I’ll tell you why. I have a laundry list of issues that could kill the bull once and for all. And while some of them are flashing alarm signals, many aren’t. I’ll go through them one by one.

Inequality

The Trade War – is far and away the biggest risk to the market. If each escalation is met with Chinese retaliation, then both countries will slide into recession. At some point, cooler heads may prevail but that is no sure thing. Having met several men who endured the 1936-38 Long March, I can assure you that the Chinese have a far better ability to sustain pain than we do. And the Chinese don’t have an election next year.

Cyber Terrorism – Imagine that you sat down to turn on your computer one day and nothing happened. The Internet was down, all financial transactions ceased, the power went out, and all food distribution ceased. America’s Internet infrastructure is far more vulnerable than most people realize. That's why I have been recommending cybersecurity stocks for the past decade. Certainly, my own local utility, PG&E (PGE) doesn’t maintain security to a military standard. It should.

Debt Levels in China – It’s easy to forget that perhaps 40% of China’s government-owned financial institutions are de facto bankrupt. They have been accumulating bad loans for decades and hiding them on their balance sheets and essential negative net worths. If one suddenly goes under, it could easily lead to a cascading series of bankruptcies much as we saw in the US during the 2008 financial crisis that spills over to the US and Europe. Back then, we lost Lehman Brothers and Bear Steans, and could have lost everyone if the government hadn’t stepped in.

Debt levels in the US – Passage of the latest spending bill means the US national debt is about to soar from $22 to $24 trillion over the next two years. The markets are ignoring this for now. It won’t forever.

Movement to the Left – Trump has run the most radically right-wing government in American history. Can you believe that we are now in the concentration camp business? The risk is that the electorate responds by installing a radical left-wing government in 2020 in reaction. That would bring a return of 90% personal tax rates, the elimination of long term capital gains treatments, and other policies with a strong anti-business tilt.

Global Interest Rates at Zero – We seem to be well on our way there. Once at zero, central banks will be powerless to get us out of recessions by cutting rates. Just look at how Japan has done over the past 30 years.

2020 Election – Is going to be loaded with fireworks to be sure. The rancor may get so extreme on both sides that it literally scares people out the market.

Middle East War – War with Iran, which is now threatened daily by the administration, will be an enormous drag of the US economy. Investment shifts from machinery to weapons, which have no impact on productivity.

Trump Blows Up – The president implements a policy that is so deleterious to the US economy that the stock market panics. Some would argue we are already there.

Climate Change Accelerates – That is already happening but is hurting countries closer to the equator than ourselves, like India and Egypt. The US military certainly considers this an existential threat. Increased severe hurricanes, heat caused crop failures, wildfires, and more frequent flooding are already having severe localized effects. Imagine all that getting much worse. And there are severe impacts which we haven’t even thought about yet. The first effect we have already seen? Higher insurance premiums for everyone. Good luck getting new fire insurance in California or flood insurance in Florida.

I’m looking at my screens this morning and virtually every stock sold short by the Dairy of a Mad Hedge Fund Trader cratered to new six-month lows.

Call it lucky, call it fortuitous. All I know is that the harder I work the luckier I get.

If you are in the right economy, that of the future, you are having another spectacular year. If you aren’t, you are probably posting horrific losses for 2019. Call it the “Tale of two Economies.”

I suspected that this was setting up over the last couple of weeks. No matter how much bad news and uncertainty dumped on these companies, the shares absolutely refused to go down. Instead, they flat lined just below their 2019 highs. It was a market begging for a selloff.

When the Facebook (FB) hacking scandal hit, investors were ringing their hands about the potential demise of Mark Zuckerberg’s vaunted business model and the shares plunged to $123.

However, while analysts were making these dire productions, I knew that Facebook itself was signing a long-term lease for a brand new 46-story skyscraper in downtown San Francisco just to house its Instagram operations.

Months later, and the company that misused Facebook’s data, Steve Bannon’s Cambridge Analytica, is bankrupt, and (FB) is trading at $185, a new high. Facebook was right, and the Cassandras were wrong.

Amazon was given up for dead during the February melt down as the shares withered from a daily onslaught of presidential attacks threatening antitrust action. Today, the shares are up a mind-blowing 38% above those lows.

And when Apple announced its earnings, the shares tickled $222, putting it squarely back into the ranks of the $1 trillion club ($949 billion at today’s close).

It turns out that technology companies are immune from most of the negative developments that have caused the rest of the stock market to drag. I’ll go through these one at a time.

Falling Interest Rates

Tech companies are sitting gigantic cash mountains, some $245 billion in Apple’s case, which means that as net lenders to the credit markets, they are beneficiaries of the credit markets. This makes tech companies immune from the credit problems that will demolish old economy industries during the next rate spike.

Rising Oil Prices

While tech companies are prodigious consumers of electricity, many power these with massive solar arrays and they sell periodic excess power to local utilities. So as net energy producers, they profit from rising energy prices.

Rising Inflation

Since the output of technology companies is entirely digital, they can handily increase productivity faster than the inflation rate, whatever it is. Traditional old economy companies, like industrials and retailers can’t do this.

Remember that while analogue production grows linearly, digital production grows exponentially, enabling tech companies to handily beat the inflation demon, leaving others behind in the dust.

Share Buybacks

While technology companies account for only 26% of the S&P 500 stock market capitalization, they generate 50% of the profits. Thanks to the massive tax breaks and low tax repatriation of foreign profits enabled by the 2017 tax bill, share buybacks are expected to rocket from $500 billion to $1 trillion this year. Companies repurchasing their own shares have become the sole net buyers of equities in 2019.

And companies with the biggest profits buy back the most stock. This has created a virtuous cycle whereby higher share prices generate more buybacks to create yet higher share prices. Old economy companies with lesser profits are buying back little, if any, of their own shares.

Of course, tech companies are not without their own challenges. For a start, they have each other to worry about. FANGs will simultaneously cooperate with each other in a dozen areas, while fight tooth and nail and sue on a dozen others. It’s like watching Silicon Valley’s own version of HBO’s Game of Thrones.

Also, occasionally, the tech story becomes so obvious to the unwashed masses that it creates severe overbought conditions and temporary peaks, like we saw in January.

“The rule book on how things are done and how they will play out you can just throw away right now,” said Scott Minerd of Guggenheim Partners.

Global Market Comments

August 7, 2019

Fiat Lux

Featured Trade:

(WHY I SOLD SHORT MACYS’),

(AMZN), (WMT), (M), (JWN), (KOL)

(TESTIMONIAL)

Sorry, the Trade Alert to sell short Macys’ (M) went out late yesterday. I was speaking to a retail expert and his list of things wrong with the marquee name was so long that I couldn't get off the phone. New Yorkers are going to have to find something else to do on Thanksgiving Day than attend their famous parade.

His bottom line? Retail is in a death spiral from which it will never recover. Trying on clothes in a shopping mall will soon become a thing of the past, going the way of the buggy whip, black and white TV, and six-track tapes.

If you had to pick the biggest loser of our ongoing trade wars, which have just been ratcheted up in intensity, it would be the retail industry (XRT). Higher costs and tariffs can’t be passed on, minimum wages are rising in the big cities, lower selling prices are lower, and a massive inventory glut is NOT what money-making is all about.

The stocks have delivered as expected, providing one of the worst-performing sectors of 2019. Half of them probably won’t even make it until 2020.

In fact, Sears (S) and Macy’s (M) have announced more store closings nationwide. The overhead is killing them in a micro margin world.

So, I stopped at a Walmart (WMT) the other day on my way to Napa Valley to find out why.

I am not normally a customer of this establishment. But I was on my way to a meeting where a dozen red long-stem roses would prove useful. I happened to know you could get these for $10 a dozen at Walmart.

After I found my flowers, I browsed around the store to see what else they had for sale. The first thing I noticed was that half the employees were missing their front teeth.

The clothing offered was out of style and made of cheap material. It might as well have been the Chinese embassy. Most concerning, there was almost no one there, customers OR employees.

The Macy’s downsizing is only the latest evidence of a major change in the global economy that has been evolving over the last two decades.

However, it now appears we have reached both a tipping point and a point of no return. The future is happening faster than anyone thought possible. Call it the Death of Retail.

I remember the first purchases I made at Amazon 20 years ago. Even though I personally knew the founder, Jeff Bezos, from my Morgan Stanley days, the idea sounded so dubious that I made my initial purchases with a credit card with only a low $1,000 limit. That way, if the wheels fell off, my losses would be limited.

And how stupid was that name Amazon, anyway? At least, he didn’t call it “Yahoo” because it was already taken.

Today, I do almost all of my shopping at Amazon (AMZN). It saves me immense amounts of time while expanding my choices exponentially. And I don’t have to fight traffic, engage in the parking space wars, or wait in line to pay.

It can accommodate all of my requests, no matter how bizarre or esoteric. A WWII reproduction Army Air Corps canvas flight jacket in size XXL? No problem!

A used 42-inch Sub Zero refrigerator with a front-door icemaker and water dispenser? Have it there in two days, with free shipping at one fifth the $17,000 full retail price.

So I was not surprised when I learned this morning that Amazon accounted for 25% of all new online sales in 2018 in a market that is already growing at a breathtaking 20% YOY.

In 2000, after the great “Y2K” disaster that failed to show, I met with Bill Gates Sr. to discuss his foundation’s investments.

It turned out that they had liquidated their entire equity portfolio and placed all their money into bonds, a brilliant move coming mere months before the Dotcom bust and a 16-year bull market in fixed income.

Mr. Gates (another Eagle Scout) mentioned something fascinating to me. He said that unlike most other foundations their size, they hadn’t invested a dollar in commercial real estate.

It was his view that the US economy would move entirely online, everyone would work from home, emptying out city centers and rendering commuting unnecessary. Shopping malls would become low-rent climbing walls and paintball game centers.

Mr. Gates’ prediction may finally be occurring. Some counties in the San Francisco Bay area now see 25% of their workers telecommuting.

It is becoming common for staff to work Tuesday-Thursday at the office, and from home on Monday and Friday. Productivity increases. People are bending their jobs to fit their lifestyles. And oh yes, happy people work for less money in exchange for personal freedom, boosting profits.

The Mad Hedge Fund Trader itself may be a model for the future. We are entirely a virtual company with no office. Everyone works at home in four countries around the world. Oh, and we all use Amazon to do our shopping.

The downside to this is that whenever there is a snowstorm anywhere in the country, it affects our output. Two storms are a disaster, and at three, such as last winter, we grind to a virtual halt.

You may have noticed that I can work from anywhere and anytime (although sending a Trade Alert from the back of a camel in the Sahara Desert was a stretch), so was sending out an Alert while hanging on the cliff face of a Swiss Alp, but they both made money.

Moroccan cell coverage is better than ours, but the dromedary’s swaying movement made it hard to hit the keys.

The cost of global distribution is essentially zero. Profits go into a bonus pool shared by all. Oh, and we’re hiring, especially in marketing.

It is happening because the entire “bricks and mortar” industry is getting left behind by the march of history.

Sure, they have been pouring millions into online commerce and jazzed up websites. But they all seem to be poor imitations of Amazon with higher prices. It is all “Hour late and dollar short” stuff.

In the meantime, Amazon soared by 49% from December to the May high, and was one of the top performing stocks of 2018. There are now a cluster of Amazon analyst forecasts around the $3,000 mark.

And here is the bad news. Bricks and Mortar retailers are about to lose more of their lunch to Chinese Internet giant Alibaba (BABA), which is ramping up its US operations and is FOUR TIMES THE SIZE OF AMAZON!

There’s a good reason why you haven’t heard much from me about retailers. I made the decision 30 years ago never to touch the troubled sector.

I did this when I realized that management never knew beforehand which of their products would succeed, and which would bomb, and therefore were constantly clueless about future earnings.

The business for them was an endless roll of the dice. That is a proposition in which I was unwilling to invest. There were always better trades.

I confess that I had to look up the ticker symbols for this story as I never use them.

You will no doubt be enticed to buy retail stocks as the deal of the century by the talking heads on TV, Internet research, and maybe even your own brokers, citing how “cheap” they are.

Never confuse a low stock price with “cheap.”

It will be much like buying the coal industry (KOL) a few years ago, another industry headed for the dustbin of history. That was when “cheap” was on its way to zero for almost every company.

So the next time someone recommends that you buy retail stocks, you should probably lie down and take a long nap first. When you awaken, hopefully the temptation will be gone.

Or better yet, go shopping at Amazon. The deals are to die for.

To read “An Evening with Bill Gates Sr.”, please click here.

Global Market Comments

August 6, 2019

Fiat Lux

Featured Trade:

(I HAVE AN OPENING FOR THE MAD HEDGE FUND TRADER CONCIERGE SERVICE),

(DON’T MISS THE AUGUST 7 GLOBAL STRATEGY WEBINAR),

(HAVE WE SEEN “PEAK AUTO SALES”),

(GM), (TM), (F), (HMC), (TSLA), (NSANY),

My next global strategy webinar will be held live on Wednesday, August 7, at 12:00 PM EDT.

Co-hosting the show will be Mad Day Trader Bill Davis.

I’ll be giving you my updated outlook on stocks, bonds, commodities, currencies, precious metals, and real estate.

The goal is to find the cheapest assets in the world to buy, the most expensive to sell short, and the appropriate securities with which to take these positions.

I will also be opining on recent political events around the world and the investment implications therein.

I usually include some charts to highlight the most interesting new developments in the capital markets. There will be a live chat window with which you can pose your own questions.

The webinar will last 45 minutes to an hour. International readers who are unable to participate in the webinar live will find it posted on my website within a few hours.

I look forward to hearing from you.

To log into the webinar, please click on the link we emailed you entitled, "Next Bi-Weekly Webinar – August 7, 2019" or click here.

There is no limit to my desire to get an early and accurate read on the US economy, which at the end of the day is what dictates the future returns on our investments.

I flew over one of my favorite leading economic indicators only last week.

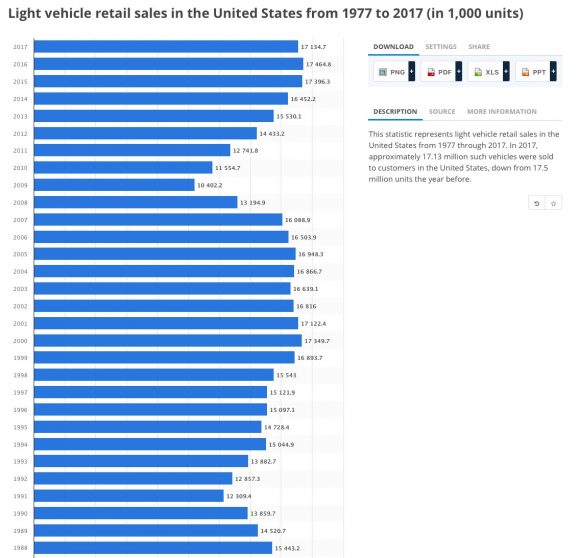

Honda (HMC) and Nissan (NSANY) import millions of cars each year through their Benicia, California facilities where they are loaded on to hundreds of rail cars for shipment to points inland as far as Chicago.

In 2009, when the US car market shrank to an annualized 8.5 million units, I flew over the site and it was choked with thousands of cars parked bumper to bumper in their white plastic wrappings, rusting in the blazing sun and bereft of buyers.

Then, “cash for clunkers” hit (remember that?). The lots were emptied in a matter of weeks, with mile-long trains lumbering inland, only stopping to add extra engines to get over the High Sierras at Donner Pass. The stock market took off like a rocket, with the auto companies leading.

I flew over the site last weekend, and guess what? The lots are full again. Not only that, the trains lined up to take them away are gone. US Auto Sales peaked in October 2017 when they fell just short of a 19 million annualized rate. As of the end of June this year, they had fallen to a 15.1 million annualized rate. July is looking worse still.

And this is what I’m worried about. Auto Sales may not only be peaking for this economic cycle. They may be peaking for all time.

This is my logic.

As they slowly age, Millennials are about to become the principal buyers of automobiles. The problem is that Millennials are purchasing cars at a far slower rate than previous generations.

This is because they have a much higher concentration in urban areas where the cost of car ownership is the most expensive in history. $40 for parking for an evening? Give me a break. But good luck finding free on-street parking, and if you do, your windows will probably get smashed.

In cities like San Francisco, public transportation, bicycles, and electric scooters are the preferred mode of transportation.

It doesn’t help that this generation is shouldering the burden of the bulk of $1.5 trillion in student loan debt. When you owe $2,000 a month in interest, there is little room for a car payment, and you probably don’t have the credit rating to buy a car anyway.

When they do buy cars, all-electric is their first choice, if they can get access to overnight charging. A lot of companies are making this easy by offering free charging for electric commuters in corporate parking lots. This explains why Tesla (TSLA) has taken deposits from 400,000 for their low-end Tesla 3, which has a two-year waiting list for new buyers.

When Millennials do drive, such as on business, for weekend trips or summer vacations, they either rent or “share.” Driving around the city, you see cars parked everywhere with bizarre names like Upshift, Getaround, Zipcar, Turo, and Casual Carpool.

Indeed, Detroit takes the car-sharing threat so seriously that the Big Three have all bought into the technology, with General Motors taking a stake in Maven. (GM) plans to start its own peer-to-peer car-sharing service this summer.

This is all a mystery for my generation, which grew up tearing apart old cars and putting them back together. I spent a year trying to put the engine on my 1955 Volkswagen back together. When I gave up, I towed the car and a big box full of greasy parts to a local mechanic, a German Army veteran. When he finished, even he had four parts left over.

Do you know who believes my rash, possible MAD theory? Investors in auto stocks, one of the worst-performing sectors of the stock market this year. Shares like those of General Motors (GM) keep breaking new valuation lows.

What was (GM)’s price earnings multiple today? Try a miserable zero since the company loses money, one of the lowest of all S&P 500 stocks. Hapless portfolio managers keep getting sucked into the shares, which have become one of the ultimate value traps.

It is all further evidence that my cautious view on the US economy is correct, that multiple crises overseas are ahead of us, and that the stock market could drop 5%-10% at any time. The auto industry should lead the charge to the downside, especially General Motors (GM) and Ford (F).

As for Tesla (TSLA), better to buy the car than the stock.

Sorry, the photo is a little crooked, but it's tough holding a camera in one hand and a plane's stick with the other while flying through the turbulence of the San Francisco Bay’s Carquinez Straight.

Air traffic control at nearby Travis Air Force base usually has a heart attack when I conduct my research in this way, with a few joyriding C-130s having more than one near miss.

Global Market Comments

August 5, 2019

Fiat Lux

Featured Trade:

(MARKET OUTLOOK FOR THE WEEK AHEAD, or TAKING THE ELEVATOR DOWN),

($INDU), (SPY), (TLT), (IWM), (WMT), (FXB)