Q: Will deflation outpace inflation given the rapid pace of technology?

A: The answer is yes. We will get some inflation but not much. That's why I am calling the top in this interest rate cycle in the bond market at 4% instead of the 6%, 8%, or 10% we saw in earlier economic cycles. There have really been no real wage increases to really affect the big macro picture. Yes, we got the $2 an hour wage increase at Walmart (WMT), but in the grand scheme of things, that's really not much money. You'll make money on those bond shorts but you won't get a bond crash.

Q: What market is the best way to hedge market risk now?

A: The answer is that the S&P 500 (SPY) has the best hedging tools out there. Go with a deep out-of-the-money, long-dated (SPY) put. And when I say deep-out-of-the-money I'd say 10%, so you should be buying $250 puts on the (SPY), and when I say long dated, go out to June or July, or six months so time decay doesn't kill you. In that situation, just a 5% correction in the market will cause your $250 put to double in value. That will give you a 100% return and a lot of hedging value for a little bit of money if you need downside protection, which your financial advisors absolutely need to be putting on right now.

Q: What about the dividends on those puts (SPY)?

A: If you are long a put, you also can become liable for the quarterly dividend payment on the S&P 500. The way to avoid the assignment risk is to put on put option spreads in the Russel 2000, where there is a much lower dividend payment. It's too small to make an exercise worth it. The other way is to never do quarterly expiration options when the dividends are payable in only a few days. Going forward, do February puts, skip March, and then do April, May options to avoid assignment risk.

Q: Do we buy General Electric (GE)?

A: The answer is no. It?'s trading at $17 and the breakup value of this company is $15. This was a classic widow and orphan stock. Everybody in the universe owned this and it was in the Dow average. There's a lot of long term capitulation selling going and they may break the company up. There is a ton of stuff that could happen you have no insider advantage of what is going to happen, so just stay away. This has become a special situation stock. There are too many better things to buy right now than (GE).

Q: How will AMD earnings turn out?

A: The answer is they should be good. I like the whole chip sector. It had a sell off on the intel chip design flaw and the actual fact is that I have another Trade Alert already written to buy the stock with a call spread because the charts for the whole chip sector are setting up pretty nicely. That's my view on (AMD).

Q: Is it time to buy Goldman Sachs (GS)?

A: I would say yes. This is a good entry point. You wanted a dip to buy on? This is the dip. Eventually rising interest rates will bail out (GS) and increase bond trading volume where they really make their money, not on the directional call but on the volume. Last quarter the bond trading volume was terrible that generated losses, and by the way, the tax bill allowed them to take a one off write off of $5 billion on their 2017 earnings. That was included in the loss that they announced this morning. Give it one more day, let it sell off a little more, then look to buy. I doubt it will drop below the 200-day average at $231 and we may not even break the 50-day at $248.

Q: What do you think about Alibaba (BABA)?

A: The answer is I like it as a Chinese FANG. Alibaba is essentially a combination of Amazon (AMZN), Alphabet (GOOGA), and PayPal (PYPL) in China, it has had a near doubling over the past year, and I still think there is more in it. I am positive on the FANG'S this year but I don't think you'll get the same meteoric returns we got last year.

Q: Will NVIDIA (NVDA) really double again?

A: The answer is yes, but only off that $180 low that we got in December, and we are already well on the way there. A year ago, I said Nvidia would double and that was the one stock you had to buy. And this year I am also saying Nvidia is my double for the year. The trends in technology are so overwhelmingly in favor of this one name that you absolutely have to buy it on every dip. Don't even ask any questions.

Q: Is TBT more for trading than investing?

A: It is because you have a negative carry on the TBT of about 6% per year. You have to pay two times the US Treasury coupon on an annualized basis, which today is 2.55%, plus the management fees. So ideally, it's a trade and not a long-term investment. Any short play in a high yielding security like this is going to cost money to run over time.

Q: Where do you think TLT will be at the end of February?

A: I would say lower. I'm hoping we will break the $120 level. So here at the $125 level it looks pretty attractive on the short side. Again, we aren't talking gigantic numbers. When we used to see bond sell offs we were talking about 10 to 20 points, now we are looking at 3 to 5 points.

Q: Should i double my (TLT) short position?

A: The answer is yes, but let's see if we can squeeze a little more upside action out of it to $126 like I just mentioned.

Q: Should I keep buying the CRISPR stocks on dips like Intellia Therapeutics (NTLA) and Editas (EDIT)?

A: Absolutely yes, this is like the first floor of a 100-story building. These CRISPR stocks have a lot more to go, and by the way, every single of one of these guys are a takeover target from a major pharma company. I am very bullish.

Q: What about the Aussie dollar (FXA)?

A: It is a commodity currency and we have a commodity boom going on. Eventually, the Aussie should hit US$1.00, so if Australians have any foreign bills to pay, delay them. They will become cheaper by 10% in the next couple of months. This a classic commodity currency because their biggest exports are iron ore, coal, etc.

Q: Should I sell Baker Hughes (BHGE) now?

A: I would take profits here. This company is 60% owned by (GE) and given all the ruckus going on in (GE), this company could get sold and might threaten the 30% gain in one month that we just had. No one ever got fired for taking a profit.

Q: Should we put on an options bull call spreads in the various oil names?

A: Answer is yes, but I would go deep-in-the-money, so when we get the inevitable correction, you won't get shaken out of your position. Also, I'd go short dated which is another way of controlling your risk by only buying the front month call spreads and just adding new ones as the old ones expire. It's a classic late cycle trading strategy.

Q: Do you have any comments on defense companies?

A: I would stand aside at this point because these stocks, like Raytheon (RTN) and Lockheed Martin (LMT) have all doubled in the last year or two. We've had no new wars and we've had no increase in defense spending approved by congress. Too many other better things to play and it's very late in the cycle for defense at this point.

Featured Trade: (THE BIG WINNER FROM INTEL'S CHIP DESIGN FLAW), (INTC), (NVDA), (AMD), (THE CONTINUING DEATH OF RETAIL), (AMZN), (WMT), (M), (JWN), (TESTIMONIAL)

Buy Intel (INTC) on the dip. That is the only conclusion you can reach after watching the company go through the meat grinder after revelations of its chip design flaws were made public.

After following this company for four decades, that is always the correct kneejerk reaction. Certain industries suffer from inherent idiosyncratic risks unique to them, and this is one of them.

Some 25 years ago, I had dinner with the late Intel CEO Andy Grove (we shared the same doctor), and I asked what was his biggest fear. He answered that the company would spend $1 billion on a new fab, then flipped the switch on opening day, and nothing happed.

Intel has a disaster something like that on its hands today.

Samsung knows this lesson too well from 2016, the makers of the Galaxy S7 smartphone, which took a huge blow when their batteries continually burst into flames in 2016. Apparently, their testers didn't find this flaw until after delivering the first large batch of new phones.

The news went viral and Samsung had a PR disaster of mega proportions, a battery design catastrophe, and quality control crisis on their hands all at the same time. You may recall that every airport had signs at the boarding gate reminding passengers to leave behind their flaming Samsung phones.

In the fickle market of premium smartphones, Samsung was taken out to the woodshed and severely beaten by the Chinese consumer, and their market share in the biggest smart phone market dropped from a robust 18.7% in 2013 to pitiful 2.2% in Q4 2017.

They have never recovered.

Intel's (INTC) disclosure of the design flaw exposed in their CPU was a terrible start to 2018.

Predictably, Intel shares were hammered.

Hardware companies cannot afford sacrificing whole product cycles. The wasted R&D and the brand damage is lamentable and it will take time to recover, not to mention the multibillion dollar cost.

You can bet that a comprehensive review has been set in motion for the designs in all lucrative hardware products at all companies. Expect a gradual trickle of bad news to come out from other players too.

Intel noted the problem was known for "a few months" but did not fix it immediately. This is awful. Brian Krzanich, CEO of Intel, also suspiciously sold a good chunk of Intel stock during this period. He is already in the SEC's sites.

Hiding architectural problems for months does not exactly breed shareholder trust.

Intel replied, "There have been no examples of the flaw being exploited by hackers". Unawareness does not exactly equate to safety. It's highly possible the future trickle of bad headlines will detail the criminal element that took advantage of this gaping hole.

Will the tech naivety continue unabashed? Will the contagion be worse next time?

Hardware reliability is truly something consumers and companies must ponder about.

Companies have more room to maneuver in the future when negotiating CPU contracts with Intel because of this debacle. That will hurt profit margins.

Technically, the patches will slow certain processors by up to 30% according to Intel officials.

The Intel CPU flaw brings up deeper questions. Is it safe to store important data on the cloud? Can hackers steal entire sets of cloud data and resell it to the highest bidder?

Another option is returning to the good old days when data was kept on external hard drive storage away from the tentacles of professional hackers. By the way, that's what we do here at Mad Hedge Fund Trader, who have never trusted the cloud.

The vast amount of data in 2018 makes this strategy highly inefficient for the biggest firms.

If storage risks flare up, the industry shifts closer to an inflection point and alternative measures will float around about how and where to store data.

Running apps on any platform requires more processing power each passing day as we expand the functionality and integration of smartphone and computing apps into our daily lives.

This higher opportunity cost of operating a slower CPU will be passed onto the user, much to their chagrin, but the problem will subside as the design architecture in new CPU's will be absent design defects.

Companies will also increase overhead. Additional quality control and design specialists to ensure that components produce products as advertised will be added to payroll. This will add higher costs, more stringent development guidelines, further pressuring margins.

The tech industry was the darling of Wall Street for many years and still is in most quarters. But some cracks are starting to form around its core foundations and ethos.

Fortunately, Wall Street still favors the tech sector and the accelerated earnings growth narrative remains intact albeit with a small chink in their armor.

The net net is tech companies will take on more operational risk.

Vulnerability will be a key theme in 2018 and entwined in this game of cat and mouse are cybersecurity firms and rogue hackers.

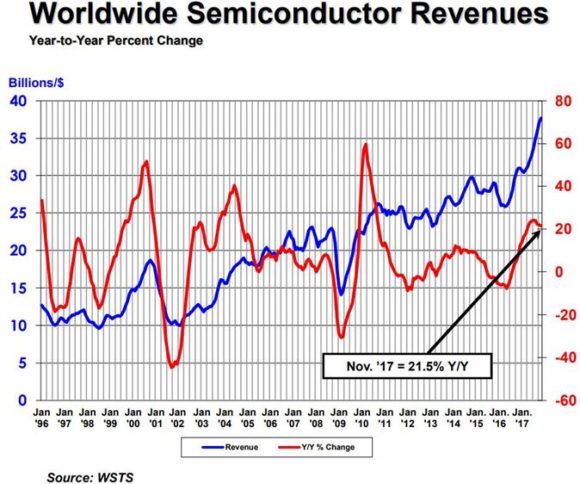

As the total global revenue for semiconductors revs up towards $80 billion, there will be multiple winners as the pie expands. Intel shares look stupidly cheap at 13x forward PE and looks substantially cheaper than AMD which trades at an insane 33x forward PE.

Comparably, the best of breed in this space is NVIDIA (NVDA) which trades at 50x forward earnings and the high multiple is justified as earnings consistently surprises to the upside.

That acrophobic multiple is well deserved, as NVIDIA represents the vanguard of several monster trends in the semiconductor industry and lead in the autonomous driving and AI spaces.

Ultimately, sales of chips could migrate up the industry chain; a natural flight to quality. Intel's slip up highlights Nvidia's top notch quality and the countdown starts again for the next batch of compromised hardware. The losers are the chip companies that are perceived as smaller, lower quality and their sell-offs are dramatic when related names roll over.

As with every other major industry trend, all signs still point to NVIDIA. But I wouldn't mind picking up some (INTC) on this dip either as the CPU market is a duopoly between AMD (AMD) and Intel (INTC).

These days, all problems for equity investors seem to be temporary.

Oops!

https://www.madhedgefundtrader.com/wp-content/uploads/2018/01/intel-chip-e1516139305841.jpg328400Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2018-01-17 01:08:342018-01-17 01:08:34The Big Winner from Intel's Chip Design Flaw

My next global strategy webinar will be held on Wednesday, January 17 at 12:00 PM EST, which I will be broadcasting live from Incline Village, Nevada.

I'll be introducing a new co-host this week. Doug Robertson of OptionsEDU.com is an old friend and a battle-scarred veteran of the equity options market. Readers in the past have found his search for value in the market fascinating. We'll look forward to receiving his insights. I'll forgive him for being an Army veteran, and not a Marine. Semper Fi!

We'll be giving you my updated outlook on stocks, bonds, commodities, currencies, precious metals, and real estate.

The goal is to find the cheapest assets in the world to buy, the most expensive to sell short, and the appropriate securities with which to take positions.

I will also be opining on recent political events around the world and the investment implications therein.

I usually include some charts to highlight the most interesting new developments in the capital markets. There will be a live chat window with which you can pose your own questions.

The webinar will last 45 minutes to an hour. International readers who are unable to participate in the webinar live will find it posted on my website within a few hours. I look forward to hearing from you.

We recently have taken in a large number of new subscribers. If you miss it, the webinar will be posted on the website within the hour.

To register for the webinar, please click on the link we emailed you entitled "Next Bi-Weekly Webinar - January 17, 2018" or click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2018/01/john-truckee.jpg316352Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2018-01-15 01:07:462018-01-15 01:07:46Don't Miss the January 17 Global Strategy Webinar

The S&P 500 (SPY) is up an eye-popping, gob smacking 4.2% so far in 2018, making up a third of my original 12% target for the entire year. Even more incredible is that it has gained nearly 10% in 30 days. If we continue to appreciate at this rate we will see 75,000 by yearend!

Which means we won't. But it is fun to run the numbers. Remember that NASDAQ soared 80% in the final eight months of the Dotcom Bubble until April, 2000 before its final downfall. It took 17 years to match that high again.

Action like this can only be explained by one new factor. After being absent for a decade, the "dumb money" is finally coming back into the stock market after a decade long hiatus.

"Dumb money," as all seasoned veterans know, are individual retail investors gun shy of stocks, thanks to the disastrous outcome of the 2008-09 crash. They have a bad habit of only buying at market tops.

Even after a blockbuster 2017, which saw 20% index gains and many 80% individual stock melt ups, that kept a death grip on their cash. Flows into equity mutual funds last year were virtually flat, while bond funds saw $200 billion worth of net inflows.

Ma & Pa appear to be pouring their money into index funds, which has the effect of focusing buying into the largest cap stocks, like the FANG's. Of course, the evidence is only anecdotal so far, gleaned from checks with the big brokers. We won't get the hard numbers that the dumb money has arrived until next month.

Good luck getting through to your broker though. If you call Interactive Brokers (IBKR) all you get is a recoding telling you how to execute a Bitcoin trade.

All the hoopla over the passage of the tax bill seems to have finally melted the ice. They were not alone.

Big tech (XLK) and oil companies (XLE) also seem to be major buyers of their own stock, front running a new round of buybacks financed by $2.6 trillion of repatriation, also enabled by the tax bill.

All asset classes are drinking the Kool-Aid.

Oil (USO) is also fast approaching my yearend target of $65, and seems hell bent on kissing $70. US oil supplies have seen the fastest ten week draw down in history, some 39 million barrels, thanks to extreme cold and accelerating economic growth. And it looks like the weather is about to hit again.

Some analysts are now forecasting $80 if the current OPEC production quotas are honored through yearend, once considered a long shot.

It's a good thing I rushed you out a research piece two weeks ago pounding the table that oil companies like Occidental Petroleum (OXY) would see the fastest earnings growth of 2018.

Even forlorn gold (GLD) has caught a bid, as the stock market wealth effect spills into other asset classes. I'll get around to writing a piece on how that works one of these days.

Those who have been waiting nine years for a crash in the bond market may be finally getting their wish. US Treasury bonds committed some key technical damage to their long term charts.

The 25-year trend lines for the two and ten year bonds entered bear market territory. I shot out a Trade Alert to sell short the (TLT), (or buy the (TBT)), the day it happened.

The most important announcement of the week was misread by almost everyone. Walmart (WMT), with 1.5 million employees the largest private employer in the US, said it was raising its minimum wage from $9 to $11 an hour as a result of the tax bill.

Here's what really happened. A massive fiscal stimulus on top of the lowest unemployment rate in a decade is creating a severe shortage of workers. As the largest employer and lowest payer, (WMT) will be the first to feel this. Some $2 an hour, or 22.22%, is a big jump. It means that real, card carrying inflation is on the way.

Walmart credited the tax bill for the move to score points with an administration that is at war with it on other fronts. The big one is the overwhelming share of imports from China and Mexico the company sells in its stores, which the administration is trying to cut back.

These days, EVERYTHING, is political.

Friday's December CPI Report was still muted at a 2.1% annual rate. But break down the numbers, and they show that the prices of manufactured goods (the past) have been falling for five years, while the prices of services (the future) are roaring at a 3% plus annual rate. And the overall rate may not be so muted when the Walmart figures his in three months.

As my UCLA Math professor used to lecture me, "Statistics are like a bikini. What they reveal are fascinating, but what the conceal is essential."

Conclusion: SELL MORE BONDS!

We are now into Q4 earnings season so those should be the dominant data points of the coming weeks.

On Monday, January 15, the markets are closed for Martin Luther King Jr. Day.

On Tuesday, January 16 at 8:30 AM EST the December Empire State Manufacturing Survey is published. Citigroup (C) reports earnings.

On Wednesday, January 17, at 9:15 AM EST, we obtain December Industrial Production. Bank of America (BAC) and Alcoa (AA) report earnings.

Thursday, January 18 leads with the 8:30 EST release of the Weekly Jobless Claims. At the same time December Housing Starts are Announced. The weekly EIA Petroleum Status Report is out at 11:00 AM EST.

On Friday, January 19 at 10:00 AM we learn December Consumer Sentiment, which should be very positive.

Then at 1:00 PM, we receive the Baker-Hughes Rig Count, which lately has started gone ballistic. Schlumberger (SLB) and Kansas City Southern (KSU) report earnings.

As for me, we finally got some decent snow at Lake Tahoe, so I'll be up there pounding the slopes in the morning when its cold, and diving into my research in the afternoon. I'm still trying to fix leaks in the roof from last winter's crushing 70 feet of snow.

When the kids are glued to their iPhones upstairs, I will be investigating the considerable assets of one Stormy Daniels. Clearly nature was kind, very kind. I understand the rest of the country is doing the same thing.

What Statistics Conceal is Essential

https://www.madhedgefundtrader.com/wp-content/uploads/2018/01/trump-porn-silence.jpg294232Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2018-01-15 01:06:552018-01-15 01:06:55Market Outlook for the Weeks Ahead, or The Dumb Money Finally Comes Out of the Woodwork

When I ran the equity trading desk at Morgan Stanley, whenever traders got bored they would sit around their desks speculating about which single event would most totally destroy financial markets.

Nuclear war was always a favorite, but that fell by the wayside after the Soviet Union collapsed and we bought all of their excess uranium and plutonium.

A giant earthquake in Japan was another, as they are large global investors. The idea was that they would have to sell all their foreign assets to finance reconstruction at home.

However, for the past decade, a new Armageddon scenario has been circulating the trading community. What would happen if China decided to suddenly dump its US Treasury bond holdings (TLT)?

The general expectation was that the ten-year Treasury bond yield would instantly spike by 100-200 basis points, stocks (SPY) would crash, the US dollar (UUP) would soar, and the world would enter a global recession.

A rumor that this disaster scenario was about to unfold hit the bond markets yesterday. The Chinese immediately branded it as "fake news".

I called my friends at the Bank of China, with whom I've had a relationship since the mid-1970's (yes, it was I who convinced them to buy all those European bonds when they were yielding 10%). They poo pooed the idea, which means it's being seriously considered.

Bond yields rose by 6 basis points, stocks suffered a 100 point one hour correction, and the US dollar went nowhere against most currencies.

However, the writing is on the wall. The Middle Kingdom has been slowing building up their carrier fleet They now have two, compared to America's ten, and a third is under construction, a reverse engineering of a small Russian ship they bought years ago.

These will be used to protect China's extended supply lines all the way to the Persian where they now account for some 80% of all oil exports. You know all the US troops we have in the Middle east? They're there to protect primarily China's oil supply, not ours. Talk about mission creep!

If push comes to shove in the South China Sea, and Trump is clearly headed in that direction, then fantasies of foreign bond liquidation could suddenly become reality. Even a buyer's strike will demolish Trump's hopes huge deficit financing, where the Chinese are expected to buy half the new paper issued.

The resilience of the markets in the face of China's end of the world threats lead me only to one conclusion: stocks markets aren't going down again, ever! The trees WILL grow to the sky!

I am therefore raising my yearend targets for the major stock indexes to $30,000 for the Dow Average and $3,200 for the S&P 500. That increases my projected return on equities from 12% to 20%.

To use Warren Buffet's characterization, chopping the corporate tax rate from 35% to 21% means your take home has risen from 65% to 79%, an eye-popping increase of 21.54%.

That means the value of US stocks jumped by 21.54% overnight when the calendar turned the page from December to January. No wonder the market has gone up every day!

The (SPY) has risen by 3.75% so far in 2018, which means we have another 17.79% to go. And if I'm wrong in my forecast it's not because I got the upside targets wrong, it's because we are about to hit it in March instead of December!

Why are we getting such a belated move in stocks from an event that was advertised daily since November 8, 2016? We only had the Obamacare debacle as a guide for Republican legislative effectiveness until now.

The contents of the tax bill were kept secret until the day after it was signed on December 22, 2017. But by then everyone's accountants were sunning themselves in Antigua or schussing the slopes of Aspen. It wasn't until days later when we learned who got the carrot and who got the stick.

That has allowed the bunching up of reaction into the first half of January this year.

I am holding fire, attempting to scale into my 2017 book slowly, having used the two point rally in bonds (TLT) to add my first short position of the year.

As they teach you in the Marine Corps. Flight School, "There are bold pilots, and there are old pilots, but there are no old, bold pilots."

I am an old pilot. Semper Fi!

The black swans are on my radar ever circling just over the horizon.

https://www.madhedgefundtrader.com/wp-content/uploads/2016/07/John-with-Tiger-Moth-e1469406885370.jpg398400Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2018-01-12 01:07:252018-01-12 01:07:25Raising My 2018 Stock Market Targets

As a large number of new subscribers just poured in, I invite them to sign up for our text messaging service.

Paid subscribers are able to receive instantaneous text messages of my proprietary Trade Alerts. This eliminates frustrating delays caused by traffic surges on the Internet itself, and by your local server.

This service is provided free to paid members of the Global Trading Dispatch or Mad Hedge Fund Trader Pro.

To activate your free service, please contact our customer support team at support@madhedgefundtrader.com. In your request, please insert "Free Trade Alerts" as the subject, include your mobile number and if you are located outside the United States then please include your country code.

Time is of the essence in the volatile markets. Individual traders need to grab every advantage they can. This is an important one.

Good luck and good trading.

John Thomas

https://www.madhedgefundtrader.com/wp-content/uploads/2017/10/john-suit-e1507749585324.jpg201300Arthur Henryhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngArthur Henry2018-01-12 01:06:482018-01-12 01:06:48Sign Up Now for Text Messaging of Trade Alerts

Featured Trade: (NOW THE FAT LADY IS REALLY SINGING FOR TH BOND MARKET), (TLT), (TBT), ($TNX), (GLD), (BITCOIN), (SPY), (THE LIQUIDITY CRISIS COMING TO A MARKET NEAR YOU), (TLT), (TBT), (MUB), (LQD), (TESTIMONIAL)

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.