Real estate brokers are still reeling from the news that December existing home sales rocketed by a blockbuster 14.7%, to an annualized 5.46 million units.

And now I hear that Apple (AAPL) is planning on building a second new research and development campus that will need 20,000 new high tech workers. The housing crisis here in the San Francisco Bay area just went from bad to worse.

It is all fresh fuel for a continuation in the bull market for US residential real estate, not just for this year, but for another decade.

Friends in the industry tell me the eye popping numbers were due to the implementation of the TILA-RESPA Integrated Disclosure (TRID) in October.

Dubbed the ?Know before you owe? requirement, TRID is the inevitable outcome of the 2008 subprime housing crash.

If you weren?t born yet in 2008, or were living in a cave on a remote Pacific island back then, go watch the movie ?The Big Short? for a further explanation of those dark days.

As a result, real estate closings now take at least a week longer, and sometimes more, thanks to a new requirement for several three day ?cooling off periods.?

When the new law kicked in, TRID nearly brought he industry to a halt, and firms were sent scurrying to their attorneys to draw up the new disclosure forms to stay within the law.

TRID undoubtedly was responsible for the slowdown in the market in the run up to December.

Although prices seem high now, I am convinced that we are only at the beginning of a long term secular bull market in housing. Anything you purchase now is going to make you look like a genius ten years down the road.

The best is yet to come.

The big driver will be demographics, of course.

From 2022 onward, 65 million Gen Xer?s will be joined by 85 million late blooming Millennials in bidding wars for the same houses. That will create a market of 150 million buyers, unprecedented in the history of the American real estate market.

In the meantime, 80 million baby boomers, net sellers and downsizers of homes for the past decade, will slowly die off and disappear from the scene as a negative influence. Only one third are still working.

The first boomer, Kathleen Casey-Kirschling, born seconds after midnight on January 1, 1946, will become 76 years old by then. A former school teacher, she took early retirement at 62.

The real fat on the fire here is that 5 million homes went missing in action this decade, thanks to the financial crisis. They were never built.

This is the result of the bankruptcy of several homebuilders, and the new found ultra conservatism of the survivors, like DR Horton (DHI), Lennar Homes (LEN), and Pulte Group (PHM).

Did I mention that all of this makes this sector a screaming ?BUY?, once the market moves into ?RISK ON? mode later in the year?

Talk to any real estate agent and they will complain about the shortage of inventory (except in Chicago, the slowest growing market in the country).

Prices are so high already that flippers have been squeezed out of the market for good. Bottom feeders, like hedge funds buying at the bankruptcy auctions, are a distant memory. Some now own more than 20,000 homes.

Income taxes are certain to rise in coming years, and the generous deductions allowed homeowners are looking more attractive by the day.

And let?s face it, ultra low interest rates aren?t going to be here forever. Borrow at 3% today against a long term 3% inflation rate, and you are essentially getting you house for free.

The rising rents that are turning Millennials from renters to buyers may be the first sign of real inflation beyond the increasingly dear health care and higher education that we're are already seeing.

And Millennials are having kids that demand a bigger living space! Who knew?

I may become a grandfather yet!

Looks Like a ?BUY? to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2016/01/Home-House1-e1453928682856.jpg300400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-28 01:07:442016-01-28 01:07:44Why the Real Estate Boom Has a Decade to Run

?Almost all asset markets are bubbles and mispriced,? said Bill Gross of bond giant PIMCO.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/04/Kids-Bubbles.jpg283426Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-28 01:05:532016-01-28 01:05:53January 28, 2016 - Quote of the day

Featured Trade:

(2015 TRADE ALERT REVIEW),

(AAPL), (GILD), (GS), (PANW), (IWM), (SPY),

(GLD), (TLT), (LINE), (VIX), (XIV),

(SIGN UP NOW FOR TEXT MESSAGING OF TRADE ALERTS)

Apple Inc. (AAPL)

Gilead Sciences Inc. (GILD)

The Goldman Sachs Group, Inc. (GS)

Palo Alto Networks, Inc. (PANW)

iShares Russell 2000 (IWM)

SPDR S&P 500 ETF (SPY)

SPDR Gold Shares (GLD)

iShares 20+ Year Treasury Bond (TLT)

Linn Energy, LLC (LINE)

VOLATILITY S&P 500 (^VIX)

VelocityShares Daily Inverse VIX ST ETN (XIV)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-27 01:08:332016-01-27 01:08:33January 27, 2016

When is the Mad Hedge Fund Trader a genius, and when is he a complete moron?

That is the question readers have to ask themselves whenever their smart phones ping, and a new Trade Alert flashes on their screens.

I have to confess that I wonder myself sometimes.

So I thought I would run my 2015 numbers to find out when I was a hero, and when I was a goat.

The good news is that I was a hero most of the time, and a goat only occasionally. Here is the cumulative profit and loss for the 100 Trade Alerts that I closed during calendar 2015, listed by asset class.

Profit by Asset Class Equities +32.90% Foreign Exchange +8.82% Energy +0.48% Precious Metals -1.51% Volatility -3.14% Fixed Income -5.63%

The first thing you will notice is that the above numbers total +31.62%, compared to the +38.87% profit that I reported as my 2015 performance.

That?s because we mark all positions to market daily, like a real hedge fund does, including the first and last days of the years. The P&L figures above are for only closed trades, hence the -7.25% shortfall.

All in all, some 71% of my Trade Alerts were profitable last year, less than in 2014, but still beating all competitors. That?s better than a poke in the eye with a sharp stick.

Crucial in 2015 was to stop out of losers quickly. I followed that discipline most of the time, but not always. Sometime you can?t, like when the Dow opens down 1,200 points, which it did in the summer.

Equities were far and away my most successful asset class in 2015, thanks to the tremendous volatility we endured. They accounted for 73 of my Trade Alerts, generating an impressive +32.90% profit.

Some 63% of my equity trades were profitable, with almost all of the losers showing up in the final quarter of the year, when the indexes flip flopped their way to a small annual loss.

The first half of 2015 saw me putting the pedal to the metal with an aggressive ?RISK ON? approach, picking up Apple (AAPL), Gilead Sciences (GILD), Goldman Sachs (GS), Palo Alto Networks (PANW), the Russell 2000 (IWM), and the S&P 500 (SPY).

Then I executed an abrupt about turn, ?selling in May, and going away?. That got me out of the biotech and cyber security sectors at the absolute top.

We even made money on the short side, with positions in trouble QUALCOMM (QCOM) and expiring AT&T (T).

The foreign exchange market was a nice little earner for me, chipping in a +8.52%, with 13 Trade Alerts.

Seeing a coming tidal wave of European quantitative easing, I totally nailed the collapse in the Euro (FXE) against the dollar early in the year. Betting against the Japanese yen (FXY) also helped.

However, in the run up to the Federal Reserve?s first interest rate hike in a decade, foreign currency trading opportunities became few and far between.

Incredibly, I picked up a modest 0.48% trading energy, with only a single trade in Linn Energy (LINE). But my big call here was to avoid the sector like the plague. A lot of fingers were lost catching falling knives, with near weekly calls for the bottom in oil by others.

Mercifully, I only executed one trade in gold (GLD) in 2015, and that one was a loser for -1.51%. But we chopped a lot of wood here putting in a major long-term bottom, and I now think the opportunities in precious metals will be to the upside.

Trading the Volatility Index (VIX) was a nightmare in 2015, and it cost me -3.14%. But I was able to limit my losses by making money selling short those big upward spikes during the fourth quarter through the (XIV).

Fixed income (TLT) was my big loser last year, thanks to a single trade, a short position on the fateful August 24 flash crash. The rest of the eight trades I executed for the year was profitable, and on the short side.

All in all, it was a pretty good year.

What was my best trade of 2015? I made 2.47% with a long position in Apple in April in the run up to a positive earnings report.

And my worst trade of 2015? I got hit with a horrific 5.59% speeding ticket with a short position in the S&P 500 (SPY) during the October melt up which I held on to just a bit too long.

But I lived to fight another day, making all the money back the following month.

After a rocky start, 2016 promises to be another great year. That is, provided you ignore my advice on fixed income. But who knows? It is a different world now, with a fresh array of opportunities.

As of yesterday?s writing, I was up +1.98% on the year, compared to a heart rending plunge in the Dow Average of -10.7%. It was the worst start to trading in market history.

Up small in a market crash? I?ll take that all day long. I bet you will too.

Here is a complete list of every trade I closed last year, sorted in chronological order.

2015 Trade Alert Summary

?

?

?

?

?

?

?

?

Date

?

Asset

Long/

Profit/

Closed

Position

Class

Short

Loss

?

?

?

?

?

1/6/15

(IWM) 2/$103-$118 call spread

equities

long

-4.78%

1/8/15

(FXE) 2/$122-$124 put spread

equities

long

2.01%

1/8/15

(FXE) 2/$120-$122 put spread

equities

long

2.33%

1/8/15

(BAC) 2/$16 calls

equities

long

-1.82%

1/9/15

(GILD) 1/$85-$90 call spread

equities

long

1.36%

1/9/15

(TBT) short Treasury Bond ETF

fixed income

long

-2.51%

1

/12/15

(OXY) 2/$70-$75 call spread

equities

long

-2.66%

1/14/15

(BAC) 2/$15-$16 call spread

equities

long

-1.84%

1/21/15

(BAC) 2/$14-$15 call spread

equities

long

-0.24%

1/29/15

(QCOM) 2/$75-$80 put spread

equities

long

2.13%

2/2/15

(SPY) 2/$189-$194 call spread

equities

long

0.80%

2/2/15

(IWM) 2/$107-$112 callspread

equities

long

1.22%

2/2/15

(LINE) unit

MLP

long

-3.72%

2/4/15

(AA) 2/$17-$18 put spread

equities

long

0.25%

2/6/15

(T) 2/$35-$37 put spread

equities

long

1.20%

2/20/15

(GILD) 2/$87.50-$92.50 call spread

equity

long

1.84%

2/20/15

(SPY) 2/$199-$202 call spread

equity

long

1.96%

2/20/15

(FXY) 2/$84-$87 put spread

foreign exchange

long

1.33%

3/2/15

(IWM) 4/$116-$120 call spread

equity

long

1.67%

3/6/15

(CSCO) 3/$27-$29 call spread

equity

long

0.35%

3/6/15

(SPY) 3/$200-$204 call spread

equity

long

0.52%

3/6/15

(FXE) 4/$112-$115 put spread

foreign exchange

long

2.02%

3/9/15

(GLD) 3/$107-$112 call spread

precious metals

long

-0.59%

4/9/15

(FXE) 4/$109-$112 put spread

foreign exchange

long

1.64%

4/10/15

(IWM) 4/$116-$119 call spread

equity

long

1.64%

4/15/15

(GS) 4/$175-$180 call spread

equity

long

1.40%

4/15/15

(FCX) 5/$16-$17 call spread

equity

long

2.25%

4/23/15

(LEN) 5/$45-$49 call spread

equity

long

-2.81%

4/27/15

(FXY) 6/$82-84 put spread

foreign exchange

long

0.65%

4/28/15

(AAPL) 5/$115-120 call spread

equity

long

2.47%

4/29/15

(FXE) 5/$99-$102 call spread

foreign exchange

long

1.68%

4/30/15

(FCX) 5/$17 calls

equity

long

1.25%

4/30/15

(DXJ) Japan Hedged Equity ETF

equity

long

0.29%

4/30/15

(GOOG) 5/$520-$540 call spread

equity

long

-2.25%

5/1/15

(PANW) 5/$125-$135 call spread

equity

long

1.44%

5/1/15

(IWM) 5/$119-$122 call spread

equity

long

-0.92%

5/6/15

(AAPL) 6/$115-$120 call spread

equity

long

-1.08%

5/12/15

(SPY) 5/$215-$218 put SPREAD

equity

long

1.18%

5/12/15

(SPY) 5/$212-$215 put spread

equity

long

0.67%

5/12/15

(UVXY) Proshares Ultra VIX ETF

volatility

long

1.02%

5/15/15

(DXJ) Japan Hedged Equity ETF

equity

long

0.10%

5/15/15

(GS) 5/$185-$190 call spread

equity

long

1.38%

5/15/15

(SPY) 5/$213-$216 put spread

equity

long

1.79%

5/22/15

(UVXY) Proshares Ultra VIX ETF

volatility

long

-1.70%

6/3/15

(SPY) 6/$202-$207 call spread

equities

long

0.00%

6/5/15

(FXE) 6/$113-$116 put spread

foreign exchange

long

1.29%

6/17/15

(FXY) 7/$83 put

foreign exchange

long

0.95%

6/19/15

(SPY) 6/$201-$204 call spread

equities

long

1.51%

6/19/15

(SPY) 6/$214-$217 put spread

equities

long

0.79%

7/24/15

(FXY) 8/$82-$84 put spread

equity

long

1.65%

7/29/15

(AAPL) 8/$110-$115 call spread

equity

long

1.56%

7/29/15

(SPY) 8/$195-$200 call spread

equity

long

1.58%

8/12/15

(SPY) 8/$214-$217 put spread

equity

long

1.88%

8/13/15

(TLT) 8/$125-$128 put spread

fixed income

long

0.76%

8/17/15

(SPY) 8/$214-$217 put spread

equity

long

1.92%

8/20/15

(SPY) 9/$214-$217 put spread

equity

long

1.36%

8/20/15

(FXE) 9/$112-$115 put spread

foreign exchange

long

0.51%

8/21/15

(IWM) 9/$125-$128 put spread

equity

long

1.00%

8/21/15

(SPY) 9/$215 puts

equity

long

1.62%

8/24/15

(LEN) 9/$50-$52.50 call spread

equity

long

-2.59%

8/24/15

(SPY) 9/$190-$195 call spread

equity

long

-1.61%

8/24/15

(TLT) 9/$128-$131 put spread

fixed income

long

-1.52%

8/24/15

(FXY) 9/$80-$82 put spread

foreign exchange

long

-4.85%

8/28/15

(SPY) 9/$204-$208 put spread

equity

long

-0.70%

9/1/15

(SPY) 9/$207-$210 put spread

equity

long

1.64%

9/3/15

(SPY) 9/$171-$176 call spread

equity

long

1.94%

9/3/15

(XIV) Short Volatility ETN

volatility

long

1.03%

9/8/15

(SPY) 9/$174-$179 call spread

equity

long

0.86%

9/9/15

(SPY) 9/$204-$207 put spread

equity

long

0.74%

9/11/15

(XIV) Short Volatility ETN

volatility

long

0.67%

9/21/15

(HD) 10/$105-$110 call spread

equity

long

0.62%

9/22/15

(SPY) 10/$204-$207 put spread

equity

long

1.19%

9/24/15

(SPY) 10/$203-$206 put spread

equity

long

2.18%

9/25/15

(XIV) Short Volatility ETN

equity

long

0.97%

9/28/15

(SPY) 10/$202-$205 put spread

equity

long

1.33%

9/29/15

(SPY) 10/$201-$204 put spread

equity

long

2.07%

9/30/15

(SPY) 10/$175-$180 call spread

equity

long

0.40%

10/2/15

(XIV) Short Volatility ETN

equity

long

0.47%

10/5/15

(SPY) 10/$198-$201 put spread

equity

long

-5.59%

10/5/15

(SPY) 10/$199-$202 put spread

equity

long

-4.68%

10/7/15

(TSLA) 11/$200-$220 call spread

equity

long

-0.60%

10/7/15

(TLT) 10/$130-$133 put spread

fixed income

long

2.16%

10/20/15

(SPY) 11/$207-$210 put spread

equity

long

-0.72%

10/29/15

(TLT) 11/$128-$133 puts spread

fixed income

long

1.50%

11/3/15

(SPY) 11/$213-$216 put spread

equities

long

-0.12%

11/6/15

(TLT) 11/$125-$128 put spread

fixed income

long

1.00%

11/11/15

(AAPL) 12/$105-$110 call spread

equity

long

-0.17%

11/20/15

(SPY) 12/$185-$190 call spread

equity

long

0.92%

11/23/15

(FXE) 12/$111-$114 put spread

foreign exchange

long

1.33%

11/30/15

(FXY) 12/$82-$84 put spread

foreign exchange

long

1.12%

12/3/15

(TLT) 12/$124-$127 put spread

fixed income

long

1.55%

12/4/15

(XIV)

equity

long

0.84%

12/8/15

(TLT) 1/$112-$115 call spread

fixed income

long

0.81%

12/9/15

(FXE) 12/$108-$111 put spread

foreign exchange

long

-1.70%

12/11/15

(MSFT) 1/$50-$52.50 call spread

equity

long

0.48%

12/11/15

(JPM) 1/$60-$65 call spread

equity

long

-1.51%

12/11/15

(BAC) 1/$15-$16 call spread

equity

long

-0.46%

12/14/15

(FXE) 1/$108-$111 put spread

foreign exchange

long

-1.99%

12/15/15

(XIV) Short Volatility ETF

equity

long

0.58%

What a Year!

Looks Like We?re In New Territory

https://www.madhedgefundtrader.com/wp-content/uploads/2014/08/John-Thomas-Beach-e1416856744606.png400276Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-27 01:07:342016-01-27 01:07:342015 Trade Alert Review

Featured Trade:

(THE COMING BULL MARKET IN GOLD),

(GLD), (GDX), (ABX)

(WILL GOLD COINS SUFFER THE FATE OF THE $10,000 BILL), (GLD),

(THE PRICE OF STARDOM AT DAVOS)

Loyal followers of the Mad Hedge Fund Trader are well aware that I have been bearish on gold for the past five years.

However, it may be time for me to change that view.

A number of fundamental factors are coming into play that will have a long-term positive influence on the price of the barbarous relic. The only question is not if, but when the next bull market in the yellow metal will begin.

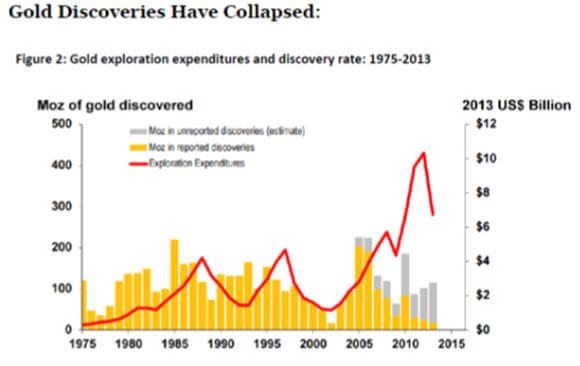

All of the positive arguments in favor of gold all boil down to a single issue: they?re not making it anymore.

Take a look at the chart below and you?ll see that new gold discoveries are in free fall. That?s because falling prices have caused exploration budgets to fall off a cliff.

Gold production peaked in the fourth quarter of 2015, and is expected to decline by 20% for the next four years.

The industry average cost is thought to be around $1,400 and ounce, although some legacy mines can produce for as little as $600. So why dig out more of the stuff if it means losing more money?

It all sets up a potential turn in the classic commodities cycle. Falling prices demolish production, and wipe out investors. This inevitably leads to supply shortages.

When the buyers finally return, there is none to be had and price spikes can occur which can continue for years. In other words, the cure for low prices is low prices.

Worried about new supply quickly coming on-stream and killing the rally?

It can take ten years to get a new mine started from scratch by the time you include capital rising, permits, infrastructure construction, logistics and bribes. It turns out that the brightest prospects for new gold mines are all in some of the world?s most inaccessible, inhospitable, and expensive places.

Good luck recruiting for the Congo!

That?s the great thing about commodities. You can?t just turn on a printing press and create more, as you can with stocks and bonds.

Take all the gold mined in human history, from the time of the ancient pharaohs to today, and it could comprise a cube 63 feet on a side. That includes the one-kilo ($38,720) Nazi gold bars stamped with German eagles upon them, which I saw in Swiss bank vaults during the 1980?s.

In short, there is not a lot to spread around.

The long-term argument in favor of gold never really went away. That involves emerging nation central banks, especially those in China and India, raising gold bullion holdings to western levels. That would require them to purchase several thousand tonnes of the yellow metal!

So watch the iShares Emerging Market ETF (EEM). A bottom there could signal the end of the bear market for gold as well.

Sovereign wealth funds from the Middle East have recently been dumping gold to raise money. The collapse of oil prices has made it impossible to meet their wildly generous social service obligations.

Hint: governments in that part of the world that fail to deliver on promises are often taken out and shot.

When this selling abates, it also could well signal the final low in gold. That?s why I have been strongly advising readers to watch the price of Texas tea careful, as both it an gold should bottom on the same day.

Let me throw out one more possibility for you to cogitate over. Another big winner of rising precious metal prices is residential real estate, which people rush to buy as an inflation hedge. Remember inflation?

Tally ho!

Looks Like A ?BUY? to Me

https://www.madhedgefundtrader.com/wp-content/uploads/2016/01/Gold-Ingot-e1453762150306.jpg400311Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-26 01:08:502016-01-26 01:08:50The Coming Bull Market in Gold

Featured Trade: (A DAY IN THE LIFE OF THE MAD HEDGE FUND TRADER), (SPY), (SPX), (QQQ), (AAPL), (VIX), (FSLR), (SCTY), (TLT), (TBT), (FXE), (GLD), (GDX), (USO)

SPDR S&P 500 (SPY)

S&P 500 Index (SPX)

PowerShares QQQ (QQQ)

Apple Inc. (AAPL)

VOLATILITY S&P 500 (^VIX)

First Solar, Inc. (FSLR)

SolarCity Corporation (SCTY)

iShares 20+ Year Treasury Bond (TLT)

ProShares UltraShort 20+ Year Treasury (TBT)

CurrencyShares Euro Trust (FXE)

SPDR Gold Shares (GLD)

Market Vectors Gold Miners ETF (GDX)

United States Oil (USO)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-25 01:07:512016-01-25 01:07:51January 25, 2016

Featured Trade: (HOW TO TRADE A CRASH), (TEN STOCKS TO BUY AT THE BOTTOM), (SPY), (QQQ), (USO), (IWM), (JNK)

SPDR S&P 500 ETF (SPY) PowerShares QQQ Trust, Series 1 (QQQ) United States Oil (USO) iShares Russell 2000 (IWM) SPDR Barclays High Yield Bond ETF (JNK)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2016-01-21 01:08:242016-01-21 01:08:24January 21, 2016

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.