Featured Trade: (FRIDAY, OCTOBER 30 SAN FRANCISCO STRATEGY LUNCHEON)

(SWITCHING FROM GROWTH TO VALUE),

(GE), (BAC), (C), (GS), (HD), (DIS), (AAPL), (MSFT),

(UUP), (FXE), (FXY), (YCS), (CYB), (FXA), (FXC)

General Electric Company (GE)

Bank of America Corporation (BAC)

Citigroup Inc. (C)

The Goldman Sachs Group, Inc. (GS)

The Home Depot, Inc. (HD)

The Walt Disney Company (DIS)

Apple Inc. (AAPL)

Microsoft Corporation (MSFT)

PowerShares DB US Dollar Bullish ETF (UUP)

CurrencyShares Euro ETF (FXE)

CurrencyShares Japanese Yen ETF (FXY)

ProShares UltraShort Yen (YCS)

WisdomTree Chinese Yuan Strategy ETF (CYB)

CurrencyShares Australian Dollar ETF (FXA)

CurrencyShares Canadian Dollar ETF (FXC)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-22 01:08:112015-10-22 01:08:11October 22, 2015

For most of 2015, growth stocks far and away have been the outstanding performers in the US stock market.

Almost daily, I delighted in sending you trade alerts to buy winners, like Palo Alto Networks (PANW), Tesla (TSLA), and the Russell 2000 (IWM).

And so they delivered.

The reasons for their impressive gains were crystal clear.

The expectation all year was that the Federal Reserve would raise interest rates imminently. This gave us a perennially strong dollar (UUP).

Thus, one could only direct focus towards companies that were immune from plunging foreign currencies and falling international earnings.

It really was a year to ?Buy American?.

But a funny thing happened on the way to the bear market for bonds. It never showed up.

The final nail in the coffin was Fed governor Janet Yellen?s failure to move on September 17. She looked everywhere for inflation, but only found the chronically unemployed (the 10% U-6 discouraged worker jobless rate).

Not only did we NOT get the rate hike, the prospects are that WE MAY NOT SEE A SUBSTANTIAL INCREASE IN THE COST OF MONEY FOR YEARS!

At this point, the worst-case scenario is for the Fed to deliver only two 25-basis point rises over the next six months, AND THAT?S IT!

This reinforces my belief that the top of the coming interest rate cycle may only reach the bottom of past cycles, since deflation is so pernicious, and so structural.

All of a sudden, the bull case for the dollar, which has been driving our US stock selection all year, went wobbly at the knees.

Europe, Japan, and China are all now in between new quantitative easing and stimulus cycles, giving a decided bud to the Euro (FXE), the Yen (FXY), (YCS), the Yuan (CYB), the Aussie (FXA), and the Loonie (FXC).

New round of QE will come, but those could be months off.

Therefore, I am sensing a sea change in the market leadership. Rushing to the fore are the shares of companies that benefit from flat interest rates and a flagging greenback.

Those would be value stocks.

Value stocks are easy to find. Do any quantitative screen based on low price earnings multiples, low price to book value, and low price to cash flow, and you will find thousands of them. This is what the big boys do.

There is another reason to refocus on value stocks, but it is more psychological than analytical.

We are now into our sixth year in this bull market, one of the strongest in history. Portfolio managers are very wary of paying high multiples at market tops, as many did at the summit of the Dotcom bubble in 2000.

At least if they buy cheap share at market highs they have adequate job preserving explanations for their actions. There is also some inherent built in safety in increasing weightings in companies that haven?t appreciated very much.

I probably don?t know you personally (although I call about 1,000 of you a year), but I bet you don?t have 100 in-house analysts at hand to help you sift through the wheat and the chaff.

So let me do the heavy lifting for you. I?ll distill down the value play to a handful of high quality, high probability sectors.

1) Industrials ? Remember those, the decidedly unsexy, heavy metal bashing companies that you have been ignoring for years? With global businesses and hefty borrowing for capital spending, they do very well in a flat interest rate environment. What?s my favorite industrial? The former hedge fund that made light bulbs, General Electric (GE). They make really cool jet engines and diesel electric locomotives too.

2) Consumer Discretionary ? Finally, people are spending their gas savings, now that they realize it is more than a temporary windfall. A housing market that is on fire is creating enormous demand for all the things owners stuff in their homes, both in new purchases and upgrades. Low rates will keep the 30-year mortgage under 4% for longer. You already know my best names here, Home Depot (HD), and Disney (DIS).

3) Old Technology ? Tired of paying 100 plus multiples for the latest non yielding cloud highflyer? Mature old technology stocks offer some of the cheapest valuations in the market. As, yes, they pay dividends now! I?ll go with Microsoft here (MSFT) as the action in the options market has suddenly seen a big spike.

And what about the biggest old tech stock of all, Apple (AAPL)? I think this will be a 2016 story, and investors reposition themselves to take advantage of the run up to the iPhone 7 launch in a year. But as the recent price action shows, some portfolio managers may not want to wait.

4) Financials ? Are not the first sector to leap to mind when looking for a low interest rate play. Overnight interest rates will remain depressed as far as the eye can see. However, rates at the long end, maturities of five years or more, are rising.

This steepening yield curve is where it really matters for banks, as it allows them to expand their profit margins. On top of that, bank valuations are at the bargain basement end of the market, with many still trading at below book value. Go for Citibank (C), Bank of America (BAC), and Goldman Sachs (GS).

New leadership from low-priced sectors could give us the rocket fuel for a melt up in the indexes into the end of 2015. It could take us right to the low end of my forecast yearend range for the S&P 500 I made on January 6 of 2,200-2,300 (click here for ?My 2015 Annual Asset Class Review?).

After five months of derisking, both institutions and hedge funds are underweight stocks and shy of exposure. As a result this underperforming year has ?chase? written all over it.

Keep your fingers crossed, but stranger things have happened.

It?s My Turn to Do the Heavy Lifting

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/John-Thomas1.jpg351357Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-22 01:06:102015-10-22 01:06:10Switching From Growth to Value

?They ring a bell at the bottom, and right now the bell is ringing,? said Robert Reynolds, a manager at Putnam Investment Fund.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Town-Cryer-e1445455384988.jpg202300Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-22 01:05:512015-10-22 01:05:51October 22, 2015 - Quote of the Day

I came up to my Tahoe lakefront mansion in Nevada this week so I could get in some serious mountain climbing after the markets closed every day.

What did I get? Three days of torrential downpours. The rain was hitting the roof so hard last night that it kept me awake.

Flash floods are wreaking havoc in Los Angeles. Poisonous sea snakes indigenous to Southern Mexico are appearing on California?s golden beaches.

Local fishermen are hooking Mahi Mahi normally found in Hawaiian waters.

And guess what? The first great white shark in 100 years was spotted devouring a seal inside of San Francisco Bay. It looks like I am going to have to reconsider my plans to run the Escape From Alcatraz triathlon this year.

There is absolutely no doubt about it. El Ni?o is arriving with a vengeance. And so is the impact on your trading and investment portfolio.

The potential consequences for your trading and investment portfolio are huge.

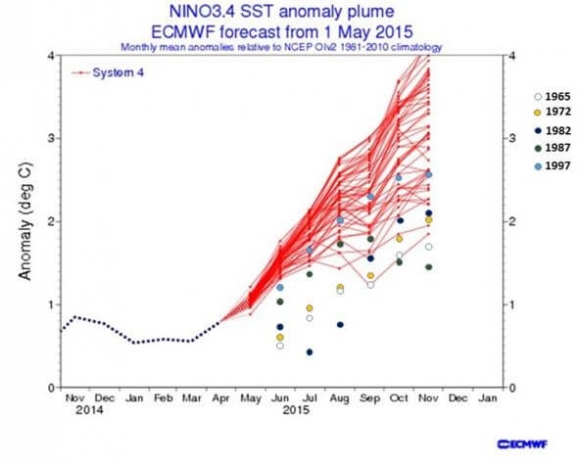

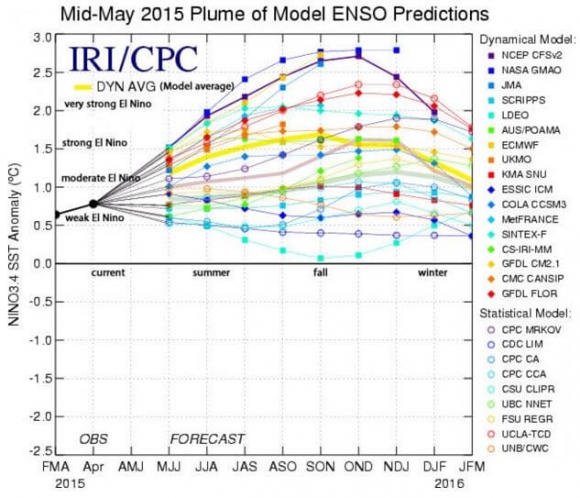

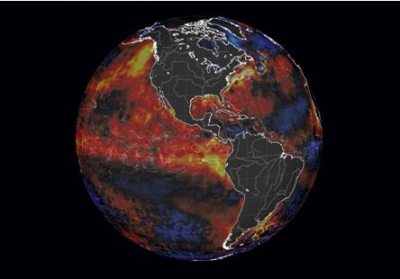

The Australian Bureau of Meteorology (click their link http://www.bom.gov.au/climate/enso/) has even gone as far as to predict that this will be a very big El Ni?o year, the kind that occurs only twice a century. The last two major events occurred in 1982-1983 and 1997-1998.

That emergency caused $550 million worth of damage in California alone.

These tumultuous weather events are caused by a differential in Pacific Ocean temperatures off the west coast of South America, in what is called the ?El Ni?o Southern Oscillation Zone.?

A weak event is triggered by temperatures 0.5-0.9 degrees centigrade more than average, a moderate one 1.0-1.4 degrees warmer than average, and a very strong event more than 2 degrees above average. As of October 13, the temperature was 1.4 degrees above average and rising.

The implications of an El Ni?o winter are global in scale.

Australia will almost certainly face a severe drought, destroying much of the grasslands on which the nation?s livestock industry depends.

You can also expect the wheat crop there to fail, as irrigation is rarely used Australia to cut costs.

Southeast Asia will also be dry, damaging rice production in Thailand, the world?s largest exporter. Sugar will also take a hit.

The drought could extend to India, reducing crops for grain, rice, sugar, and cotton. As Indian incomes fall, the gold market could be impacted, as the country is the largest buyer of the precious metal.

El Ni?o also decimates the annual anchovy catch in South America, which competes in the international markets with soybean meal.

El Ni?o?s bring mosquito blooms and the diseases they cause, bringing sudden epidemics for Malaria and Dengue fever. If you?re headed to Latin America this year, be sure to get your shots and take your pills.

It is estimated that the 1998 El Ni?o caused 16% of the planet?s coral reefs to die off.

The opposite effects occur in the Northern hemisphere, with El Ni?o bringing torrential downpours.

I remember the last one all too well.

In 1998, I led a troop of Boy Scout volunteers to fill sand bags to save a levee in California?s Central Valley. We returned two days later, covered from head to toe in mud and exhausted, living on granola bars.

This time around, El Ni?o would be welcomed by the Golden State with open arms, as it would bring to an end a four-year drought, the most severe in history. Everyone here is now subject to strict water rationing and hefty fines for water hogs.

Indeed, when I was recently in Las Vegas, I couldn?t help but notice that the tap water at the Bellagio Hotel had become undrinkable.

The water level in nearby Lake Mead is now so low that it has fallen below the intake pipes for the city. The hotel was unable to resupply bottled water in the shops fast enough.

For the trading universe, this could all finally bring the long bear market in agricultural commodities to an end. Whether there is too little rain, or too much, abnormal weather of any kind brings plummeting crop yields, and higher prices.

So far, the price action in the ags has been very encouraging as El Ni?o continues its relentless march northward.

Affected have been the commodity prices of corn, (CORN), wheat (WEAT), soybeans (SOYB), ag stocks like John Deere (DE), Caterpillar (CAT), Potash (POT), and Monsanto (MON), and many basket ETF?s, such as the PowerShares DB Agriculture Fund (DBA) and the Market Vectors Agribusiness Fund (MOO).

The term ?El Ni?o? translates from Spanish as the ?Christ Child?. It is so named because the event was first discovered in South America just before Christmas about 50 years ago.

They have been occurring throughout human history. The crop failures they brought are thought to be responsible for the collapse of several pre Columbian civilizations. One historian even posits that it was a major cause of the French Revolution in 1789.

El Ni?o?s are also legendary for bringing enormous snowfalls in the High Sierras during the winter. While a student, I was working a part time job at the Mammoth Mountain ski resort in California when a legendary one hit in 1968.

An incredible 35 feet of snow fell in one weekend. Entire buses were buried and lost in the storm. I spent a week helping trapped people dig out from that one.

This is one big catch to all of these prognostications, as there always is. El Ni?o winters have been predicted in the past and not shown up, most recently two years ago. After all, models are just models, not certainties.

Betting on the weather can be hazardous to your wealth.

Besides the trading opportunities, an El Ni?o would make the coming ski season up here at Lake Tahoe look pretty good. I am shopping for new equipment already.

?

Looks Like Rain to

Me

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Mud-Slide-e1445367907691.jpg285400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-21 01:07:192015-10-21 01:07:19El Ni?o is Closing In On Your Portfolio

Featured Trade:

(LAST CHANCE TO ATTEND THE FRIDAY, OCTOBER 23 INCLINE VILLAGE, NEVADA STRATEGY LUNCHEON),

(OCTOBER 21 GLOBAL STRATEGY WEBINAR),

(ARE YOU IN THE 1%?),

(SNE), (HMC)

Sony Corporation (SNE)

Honda Motor Co., Ltd. (HMC)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-20 01:09:452015-10-20 01:09:45October 20, 2015

Come join me for lunch at the Mad Hedge Fund Trader?s Global Strategy Update, which I will be conducting in Incline Village, Nevada on Friday, October 23, 2015.

An excellent meal will be followed by a wide-ranging discussion and an extended question and answer period.

I?ll be giving you my up to date view on stocks, bonds, currencies, commodities, precious metals, and real estate. And to keep you in suspense, I?ll be throwing a few surprises out there too. Tickets are available for $198.

I?ll be arriving at 11:30 and leaving late in case anyone wants to have a one on one discussion, or just sit around and chew the fat about the financial markets.

The lunch will be held at the premier restaurant in Incline Village, Nevada on the sparkling shores of Lake Tahoe. Those who live there already know what it is. The precise location will be emailed with your purchase confirmation.

I look forward to meeting you, and thank you for supporting my research.

https://www.madhedgefundtrader.com/wp-content/uploads/2014/02/Lake-Tahoe-View-e1410283987626.jpg241400Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-20 01:08:402015-10-20 01:08:40SOLD OUT Friday, October 23, 2015 Incline Village, Nevada Global Strategy Luncheon

You would never guess Dr. Ben Bernanke was once one of the most powerful men in the world, indeed in all of human history.

There he sat across the table from me in a popular San Francisco Italian restaurant wearing a poorly made grey suit and a cheap pair of shoes, with rubber soles.

Only the occasional interruption from an autograph seeker belied his true importance.

I managed to snare Ben for a couple of hours on his national book tour promoting his just released "The Courage to Act." Out only days, it was already at the top of the New York Times Best Seller list.

Ben is a different guy now. For a start, you can now call him "Ben" instead of "Governor."

Remember those carefully parsed, measured, and deliberate words he used to use to explain Federal Reserve monetary policy and his future intentions? That guy is long gone.

The new Ben is funny, in a subtle, but wickedly clever manner. He is also instructional, thoughtful, even professorial. At the end of the day, Ben Bernanke is now your favorite faculty member.

Ben's big revelation to me was that there were no potential triggers out there for another 2008-09 type financial crisis.

American banks have been recapitalized to the extent that they now have a stronger safety net with which to weather any future volatility. US banks are bigger than ever.

The big global concern right now is with emerging markets, where trillions of dollars worth of US dollar-denominated debt have been borrowed, collateralized by depreciating local currencies.

Another worry is the perceived "Fed put," which is allowing investors to get complacent with their risk-taking.

Bernanke believes that rising income inequality is the biggest structural problem we face. It means that not all are benefiting from an improving economy, a goal of Fed policy.

This has been unfolding for 40 years, and won't be solved in a day, as several presidential candidates are promising.

As a result, the "Horatio Alger" effect, whereby the poorest can rise to success through brains, hard work, and thrift, is now much less likely to occur than in the past.

Bernanke himself is a perfect example of that phenomenon.

Ben and I spoke at length about the dark days of the crash, and he remembered the emails I used to pepper his staff with proposing fixes or patches on an almost daily basis.

Regulation dating from the 1930s had become outmoded and was woefully out of touch with modern-day finance. It was far too lax in the run-up to the crisis.

For example, insurance giant AIG was monitored by the Office of Thrift Supervision, which was utterly clueless when it came to pricing mathematically complex derivatives.

Bernanke warned President Bush as early as 2005 that real estate prices were getting too high and that a crash was coming.

His predecessor, Alan Greenspan, had cautioned during the 1990s that Fannie Mae and Freddie Mac had a flawed business model that would eventually blow up and take down the financial system with it.

In the end, every major financial institution was tottering on the edge.

Bernanke had the benefit of completing his Ph.D. thesis on the causes and mistakes of the Great Depression, once an arcane area of economic study.

Thanks to the laissez-faire philosophy of the 1920s, the Fed let the money supply collapse, and one-third of all banks went under, some 8,000 in total. This froze the entire credit system.

Eight decades later, Ben, therefore, saw the answer to another looming depression in an inflated money supply, which we saw with QE 1, 2, 3, and 4.

He also helped engineer the $700 billion TARP that bailed out the 20 biggest banks, which he described as "the most successful, but most hated government policy in history."

When it was wound down, the US Treasury made a $15.3 billion profit on the program.

Part of the problem in selling the TARP, and later, President Obama's 2009 $831 billion stimulus budget, was that while the crisis started in New York and Washington, it was slow to reach the hinterlands.

One Republican congressman in Iowa called local car dealers in his district and asked what the big deal was. Ben said, "Just wait," and General Motors filed for bankruptcy months later.

I asked Ben who was his favorite president, as he was appointed by both George W. Bush and Barack Obama. He confirmed that he liked working for the two men, but that Bush was the natural practical joker.

When Chairman of the Council of Economic Advisors, Bernanke was required to give a weekly briefing on the state of the economy. Once he committed the grievous sartorial error of wearing tan socks with his trademark grey suit.

Bush complained, stating that the White House had dress standards to maintain.

Bernanke answered that he thought the Bush administration was one of fiscal responsibility, and that he had bought a four-pack of the controversial socks at the Gap for only $10.

When Ben attended the next meeting a week later, he wore the required grey socks with his grey suit. He couldn't help but notice that everyone else at the meeting was wearing tan socks with their navy suits, including the president.

When Bush met Bernanke to discuss his appointment as Chairman of the Federal Reserve in 2006, he asked if he had any political experience.

Bernanke replied that he had served two terms on the Montgomery County, Maryland Board of Education. Bush said, "that was fine."

Bernanke is an extremely intelligent man. You can almost hear the wheels whirring when he is thinking.

I asked him my "gotcha" question.

Wasn't quantitative easing just a means of bridging the demographic chasm of the 2010s, when 85 million baby boomers are retiring? Isn't it just a way to pull growth forward from the 2020s?

He paused for a moment, and then changed the subject.

Finally, I had to ask if Bernanke ever got a chance to read The Diary of a Mad Hedge Fund Trader while Fed Chairman. He diplomatically responded that the "Fed takes great pains to take in all views."

To buy "The Courage to Act" at discount Amazon pricing, please click here.

https://www.madhedgefundtrader.com/wp-content/uploads/2015/10/Bernanke-The-Courage-to-Act-e1445182316976.jpg400269Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-19 01:06:452020-03-26 14:44:55Dinner with Ben Bernanke

Featured Trade: (OCTOBER 21 GLOBAL STRATEGY WEBINAR), (FRIDAY, OCTOBER 23 INCLINE VILLAGE, NEVADA STRATEGY LUNCHEON), (THE FINAL WORD ON THE TAX ?WASH SALE RULE?), (TESTIMONIAL)

https://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.png00Mad Hedge Fund Traderhttps://madhedgefundtrader.com/wp-content/uploads/2019/05/cropped-mad-hedge-logo-transparent-192x192_f9578834168ba24df3eb53916a12c882.pngMad Hedge Fund Trader2015-10-16 01:10:332015-10-16 01:10:33October 16, 2015

Legal Disclaimer

There is a very high degree of risk involved in trading. Past results are not indicative of future returns. MadHedgeFundTrader.com and all individuals affiliated with this site assume no responsibilities for your trading and investment results. The indicators, strategies, columns, articles and all other features are for educational purposes only and should not be construed as investment advice. Information for futures trading observations are obtained from sources believed to be reliable, but we do not warrant its completeness or accuracy, or warrant any results from the use of the information. Your use of the trading observations is entirely at your own risk and it is your sole responsibility to evaluate the accuracy, completeness and usefulness of the information. You must assess the risk of any trade with your broker and make your own independent decisions regarding any securities mentioned herein. Affiliates of MadHedgeFundTrader.com may have a position or effect transactions in the securities described herein (or options thereon) and/or otherwise employ trading strategies that may be consistent or inconsistent with the provided strategies.